UWMC - UWM Holdings: A 'Hold' Until More Clarity Is Had

2023-07-14 04:40:08 ET

Summary

- UWM Holdings Corporation, a residential mortgage lending business in the US, offers a 6.7% yield and has a 7.7% market share, making it a potential strong dividend play.

- Despite a high-interest environment, UWMC has seen momentum due to its competitive rates, which have helped it increase its market share even as overall loan volume has decreased.

- The company's valuation is high compared to the sector, and its future performance depends on interest rate outlooks and loan volumes; currently, the company is rated as a 'hold'.

Introduction

Wanting to add a strong dividend play to a portfolio might have you looking at UWM Holdings Corporation (UWMC). Yielding over 6% right now and trading at the highest it has ever had in the last 12 months, does it offer a good risk/reward ratio right now? Well if we are looking at the P/E and the P/B for the company then I would say no. The FWD P/E of 24 and a FWD P/b of 2.79 doesn't paint a good enough investment thesis here, I think.

But for investors already in the company, I think the 6.7% yield is worth sticking around for and will be rating UWMC a hold as a result. As an overall mortgage lender in the US, it has captured a 7.7% market share and this paired with growing this in a rising interest rate environment makes me confident that UWMC might still provide some solid results.

Company Structure

UWM Holdings Corporation is a residential mortgage lending business in the United States. They originate mortgage loans through wholesale channels, those being primarily conforming and government loans. Founded in 1986 it has grown into a dominant position in many of the areas it operates in.

Market Position (Investor Presentation)

Why UWMC is seeing momentum still despite a higher interest environment seems to be because they are undercutting the industry and offering a lower rate, at 6.2% compared to the industry's 6.37%. This will over the long term help them secure an even stronger base of customers that are likely to stay loyal for long periods.

Loan Growth (Earnings Presentation)

But even as the overall loan volume has decreased, the market share has increased for the company, which goes to show that the competitive rates they are offering are working very well to take market share away from the competition. When we enter into a period of lower interest rates, the growth of loan volumes paired with the larger market share should be incredibly beneficial to the business. The outlook for interest rates seems to right now be that we might have one or two more hikes this year, and then a pause before going lower. That would be a bullish sign for the real estate market and I think we would see an increase in loan volumes for UWMC.

Mortgage Rates (themortgagereports)

Historically, we are at some of the lowest mortgage rates in recent history. Going lower would ignite growth for the purchase of new homes I think. As for ROE with UWMC, it sits at just under 6% currently, below the sector's 11%. This highlights some of the concerns I have still with UWMC, when we enter a period of lower interest rates, will the increased loan volumes result in a higher ROE, or will stay flat? If the latter is the result then I think UWMC will be a disappointing investment. For the moment, the housing market seems to be struggling as sales and prices are still dropping and some regions and markets are seeing larger setbacks than others.

Earnings Transcript

On May 10th, UWM Holdings Corporation announced their first quarter report to 2023. A comment from the CEO sheds some light on the strong operation performance that UWMC has had despite the tough market conditions.

-

"We reported a net loss of $139 million. But at the same time, there's a fair value marked down of over $337 million. Operationally with higher margins. In great volumes, we actually made money and if you look at it, compared to Q1 of 2022, actually, core wise made more money operating than we did in 2022, which is still a good quote in the industry. Making money profitably right now is a big deal. And UWM is doing it and we're going to continue to do it going forward, UWN has never been better positioned for the growth and success going forward".

I think this shows why the lower rates they are offering are such an advantage in times like this. Seeing still somewhat decent volumes makes downturns less harmful and results can remain consistent quarter to quarter more easily. The market goes in cycles and losing money or at least mitigating losses as much as possible is more important than anything else right now, and I think UWMC has done a great job with it. But that isn't to say it's a good time to invest yet.

Valuation & Comparison

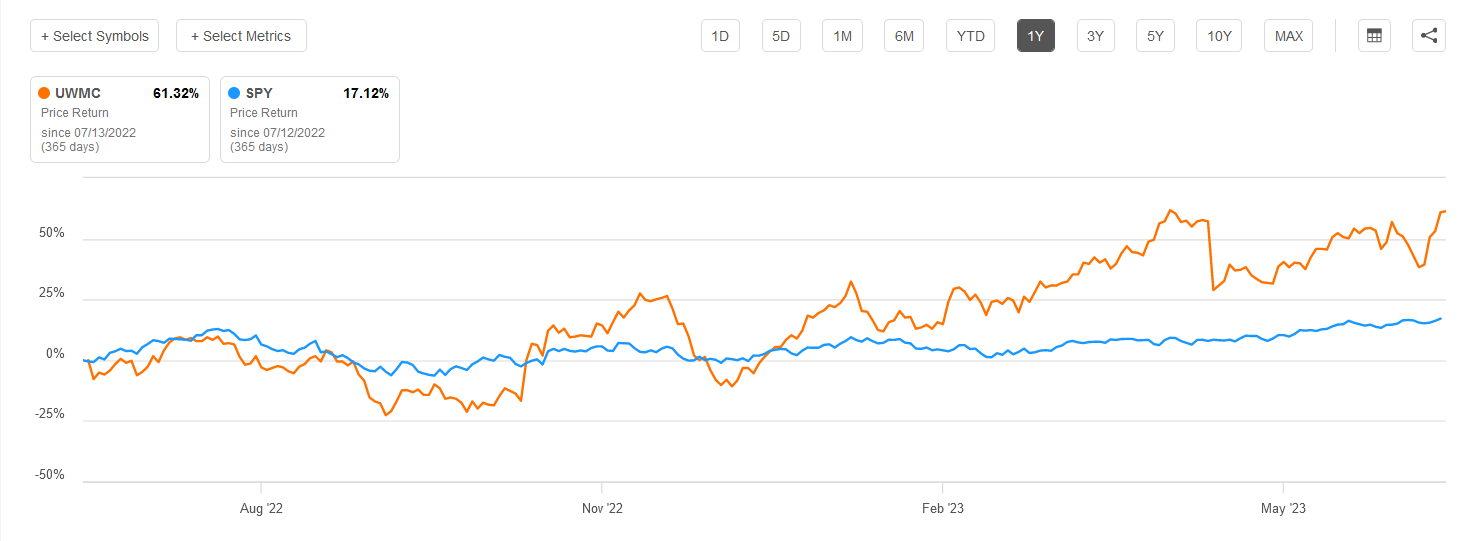

Over the last 12 months, UWMC has been able to outperform the S&P 500 quite decently with a 61% return compared to 17%.

{kind=link}

The strength in the business model of UWMC is a reason I can think this has happened. But, it should be mentioned that the P/E of UWMC has risen quickly as it now sits around 25 on a forward basis. The short interest is very high as well for UWMC which might aid in the short-term in keeping potential share price growth suppressed. Currently, the shirt interest sits at 23%.

Comparison (My Own Estimates)

The comparison above highlights why I think that UWMC is far ahead of many of the companies in the same industry. The downside of going with UWMC is the vast premium it trades at compared to the sector, 160% higher. But it has the best efficiency ratio and the highest yield out of the companies. Besides that, it's trading at a big discount to its NAV price of around $30 per share. But the pessimism regarding the housing market seems to weigh on UWMC here. If they can raise margins the P/E will look far better and the share price could go up to match the NAV. But until that, I think there still is some clarity necessary in terms of both interest rate outlooks and loan volumes for UWMC before a buy case could be fabricated.

Risk Associated

The current upward trajectory of interest rates presents an additional challenge for UWM Holdings Corporation. As interest rates rise, there is a potential impact on mortgage affordability, which can be a concern for both borrowers and the company. This is particularly relevant as UWM Holdings Corporation has been encountering rate buy-downs from borrowers.

With higher interest rates, borrowers may face increased monthly mortgage payments, potentially limiting their ability to afford or qualify for loans. This could result in reduced demand for mortgages and a decline in origination volumes, impacting UWM Holdings Corporation's revenue and profitability.

Investor Takeaway

As a leader in mortgage lending, the approach that UWMC took with offering lower rates than competitors has netted them a strong market share position despite loan volumes decreasing YoY. The yield of 6.7% makes it appealing to still maintain a position in the company and the rating for UWMC will be a hold from me.

For further details see:

UWM Holdings: A 'Hold' Until More Clarity Is Had