UWMC - UWM Holdings: Growth Remains On Hold But Stocks Still A Hold On Dividend Strength

Summary

- UWM Holdings Corporation experiences hammered growth that may persist this year.

- But it remains viable and liquid, allowing it to navigate the stormy market.

- Mixed market conditions have advantages and disadvantages to the company.

- Dividend payments continue with attractive yields and adequate capacity.

- The stock price remains low after taking a nosedive recently.

The real estate market volatility remains evident. Despite the recent inflation lull, property prices and mortgage rates stay elevated. As such, market sales are starting to cool down recently. UWM Holdings Corporation (UWMC) experiences market backlash with its hammered performance. Despite this, its prudence and efficiency matched with mixed market conditions, generate stable income. Even better, it maintains solid liquidity, allowing it to cover borrowings and sustain its operations. So it is no surprise the company sustains its well-covered and consistent dividends.

Meanwhile, the stock price appears slightly divorced from the fundamentals. It has not bounced back yet after the recent plunge. Nevertheless, it does not appear cheap despite the attractive dividend yields.

Company Performance

UWM Holdings Corporation feels the scourge of mortgage market volatility. Its growth contraction has been evident in recent quarters as home sales cool down. Home prices and mortgages stay fired up, hitting home loan demand and valuation this year.

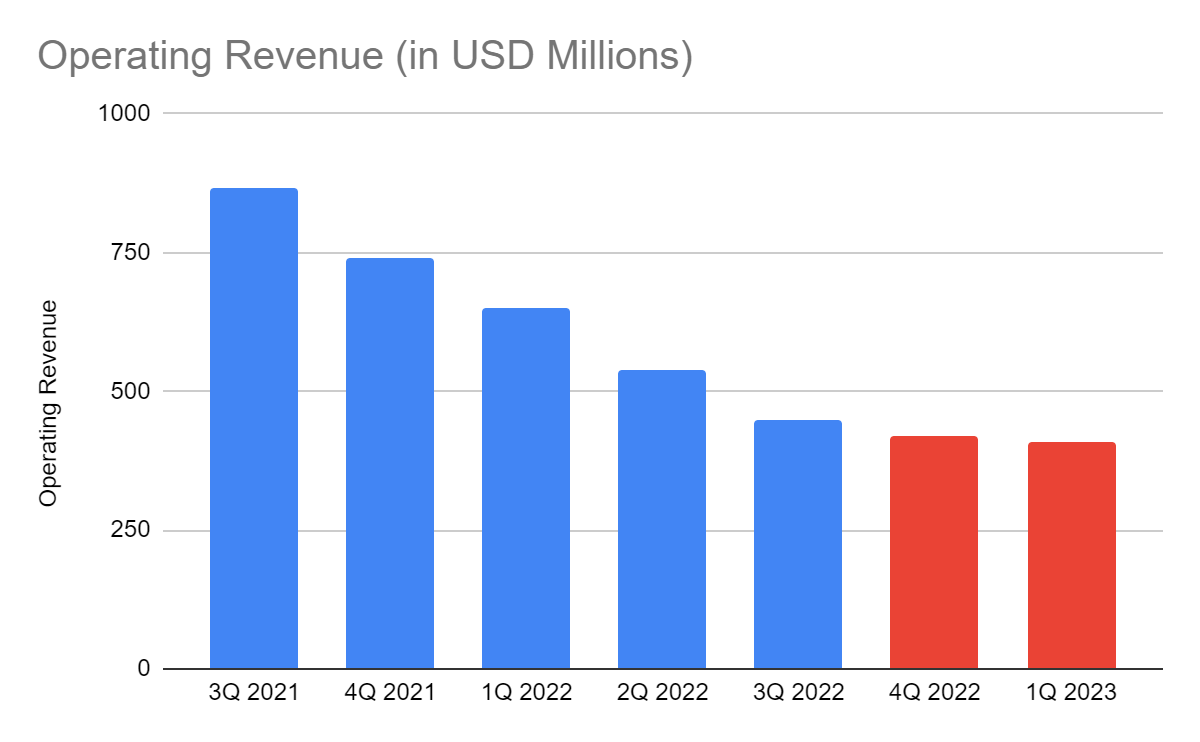

The current company's performance reflects these trends with its hammered revenues. At $447 million, the operating revenue shows a 48% year-over-year decrease. Even more noticeable is the sequential decrease since the first quarter of 2022. It is primarily driven by two of its primary components. First, loan production income dropped by over 70%. We can attribute it to the higher primary loan losses and lower origination fees. It should not be a surprise, though, given the massive reduction in mortgage loans' fair value. Note that even if inflation goes into a lull, the rate remains elevated. The massive uptrend in inflation and mortgages has a noticeable impact. It limits their capacity to maintain loan rate levels that will not erode the purchasing power of buyers. With an inflation rate of 7.1% and a mortgage rate of 6.7%-6.8%, fair value losses are visible.

The interest income of $78 million is also lower by 24%. We can also attribute it to lower mortgage loans in its Balance Sheet. Also, its securities are mostly investment and debt securities. These are less inflation-linked. As such, they have less cushion to valuation reduction and inflationary headwinds. Thankfully, UWM’s service demand stays high. Its broker channel momentum keeps speeding up. It has already overtaken Rocket Mortgage ( RKT ) as the leading mortgage lender in the US. Its increased market presence and technology investments are paying off. Its mortgage servicing rights are now 30% higher than in 2021, raising returns by 13%. It does not offset revenue reduction, but this factor shows the company's strategy to withstand market volatility and cope with risks.

Operating Revenue (MarketWatch)

{kind=link}

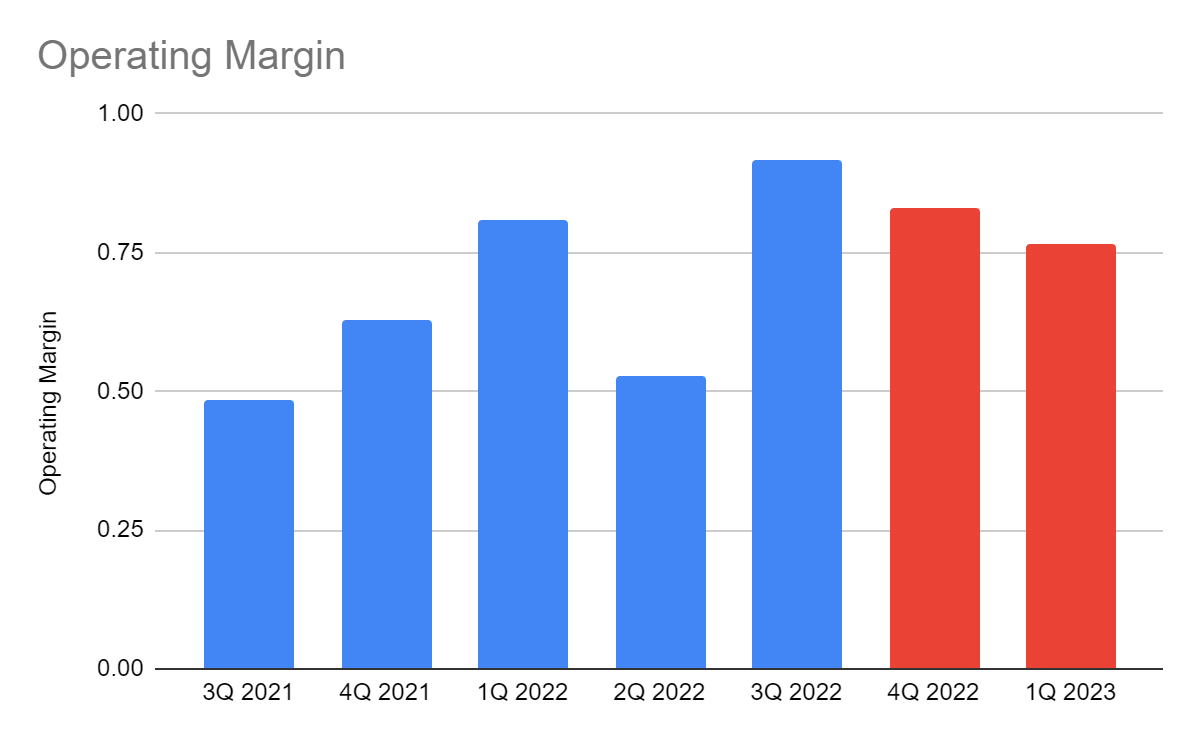

Moreover, it makes up for its loan devaluation through its prudent and efficient asset management. It continues to stabilize its costs and expenses amidst inflation. Even better, its operational strategies and core strengths in broker and servicing channels pay off. The fair value of its mortgage servicing rights shows a drastic increase. It is more than enough to offset revenue reduction and costs and expenses changes. With that, the operating costs and expenses are only $37 million, only 8% of the comparative amount. The operating margin of the company is 92%, the highest in recent quarters. It is way higher than in the comparative quarter and sequential time series. We can attribute it to the impact of inflation and company strategies to cope with it.

Despite this, the company must not be too complacent. The housing market remains volatile, which can have a substantial impact on its performance. I expect a continued downtrend in 4Q 2022 and 1Q 2023. I believe the cooling down of home sales and mortgage loan fair value has yet to peak. It must watch out for the looming recession. Mortgage rates and interest rates may still increase, although increments may slow down. To be more conservative, the revenue downtrend may continue. But I also expect the decrease rate to cool down due to the increased momentum of its broker channels. Mortgage servicing rights can partially offset these reductions, so values may be more stable. Regarding costs and expenses, they may be more manageable as inflation lulls some more. Margins may not be as overwhelming as in 3Q 2022, but they still surpass comparative levels. They may improve and stabilize in the second half of this year and rebound. Its returns may expand again with the long-run improvement in inflation and mortgage rates.

Operating Margin (MarketWatch)

{kind=link}

How UWM Holdings Corporation May Stay Sound

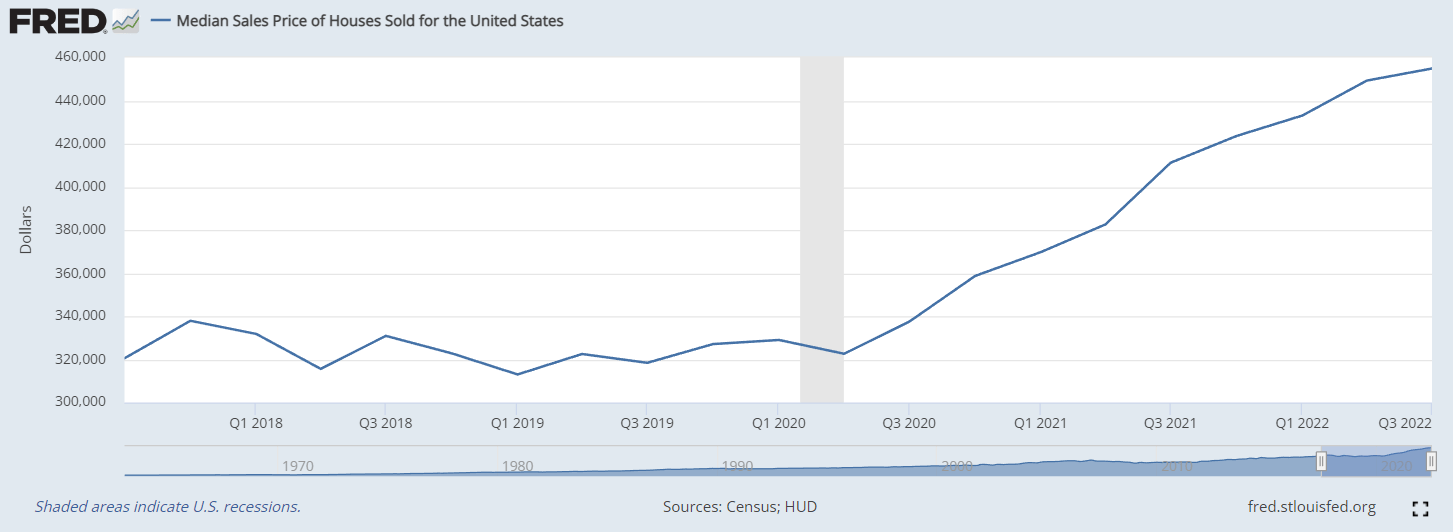

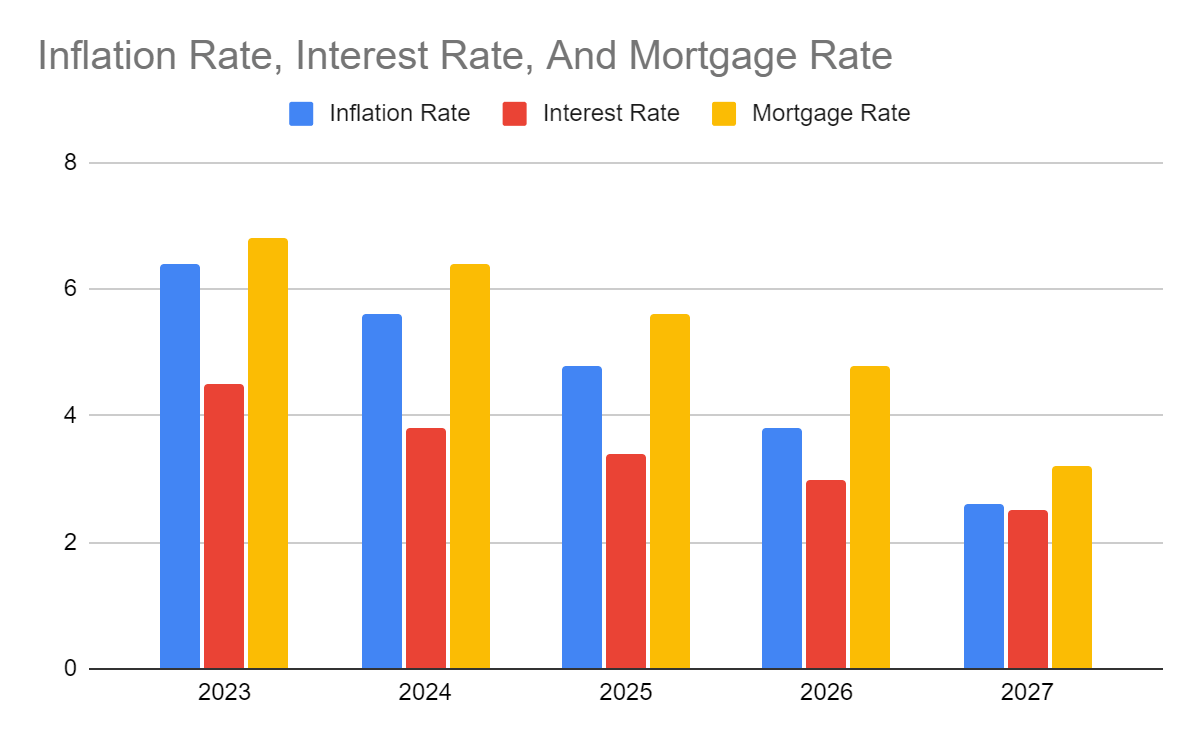

The macroeconomic changes in the US are still overwhelming. Analysts worry about the looming recession as estimates remain bleak. Yet, I choose to be more optimistic as inflation shows a continued cooling down. At 7.1%, it is still elevated but way lower than the 2022 peak. Indeed, the Fed is on the right track to managing it better, but it must not let its guard down. Interest rates may keep increasing, but increments may be lower than expected. From the 5-5.25% estimates, I project interest rates at 4.5-4.8% this year before decreasing again. The same goes with mortgage rates as house prices remain elevated. I expect it to decrease in the long run as sales and prices stabilize.

Median Home Prices (ST. LOUIS FED) Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

{kind=link}

{kind=link}

It is consistent with my long-run view of UWM’s performance. It will pay off through its strategies of working with brokers. It may be costlier than what its competitors like RKT do. However, it allows the company to set competitive pricing despite the initial margin compression. Its increased work with brokers improved its market presence. It is supported by its investment in technology to enhance efficiency. So, this move allows the company to make up for near-term lower loan valuation and production.

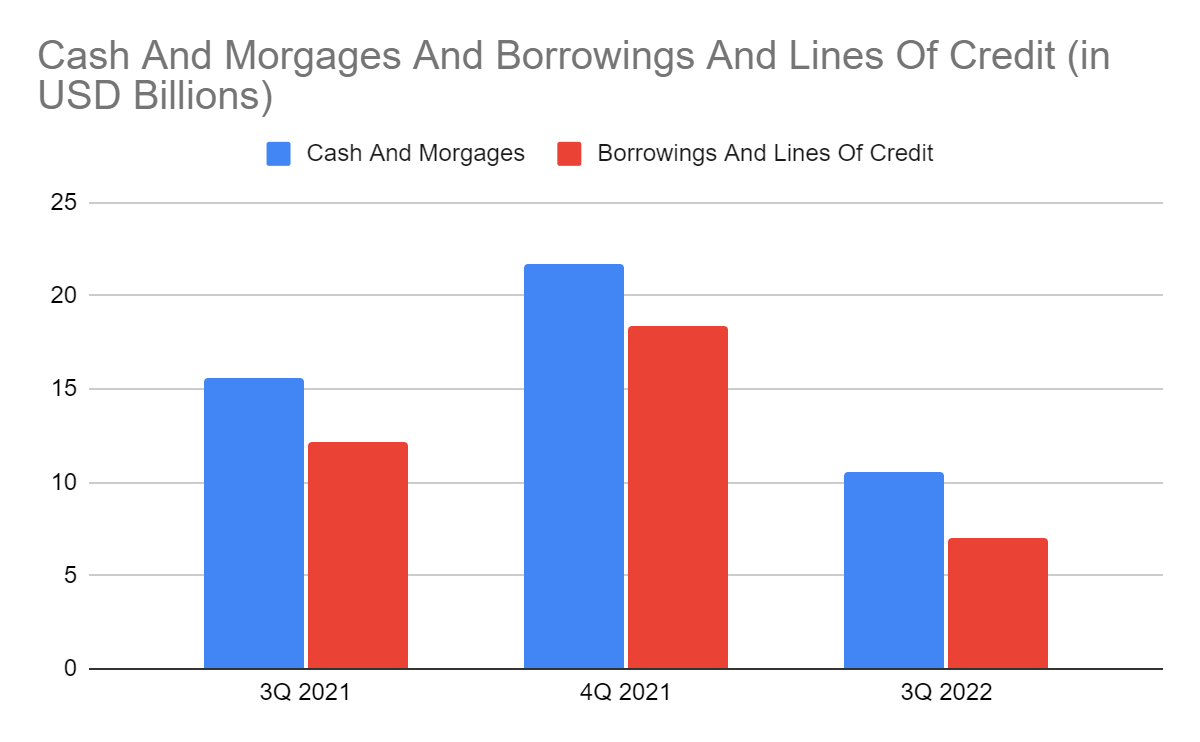

Moreover, the company shows an adequate capacity to sustain its operations. Despite the massive reductions in earning assets, the Balance Sheet remains sound. Liquidity remains solid, as shown by cash and mortgages versus borrowings and lines of credit. The primary liabilities only comprise 67% of the earning assets compared to 78% and 84% in 3Q and 4Q 2021. It proves the prudent management of the company to stabilize returns. Also, its Net Debt/EBITDA Ratio is still reasonable at 3.56x. The company has enough operating income to cover its financial leverage. It still has more space to expand. It can withstand market headwinds and suffice its potential rebound.

Cash And Mortgages And Borrowings And Lines Of Credit (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of UWM Holdings Corporation remains in a downtrend. It has not rebounded yet after its recent plunge. At $3.51, it is 35% lower than the comparative value. But it does not appear very cheap despite the low price-earnings multiple of 6.31x. If we multiply it by NASDAQ EPS estimates of $0.46-0.5, the target price only ranges from $2.9-3.16. My EPS estimation is more optimistic but still has a lower target price of $3.49.

Despite the pessimism, dividends are enticing, given the consistent payouts. It has an attractive yield of 11.14%, way higher than the S&P 400 average of 1.37%. However, its annualized dividend payout ratio is a bit high at 74% compared to 2021. To assess the stock price better, we will use the DCF Model.

FCFF $272,200,000

Cash $915,000,000

Borrowings $6,800,000,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 92,575,551

Stock Price $3.51

Derived Value $3.08

The derived value also shows potential overvaluation. There may be a 13% downtrend in the next 12-18 months. It may not be a good entry point to make a buy position.

Conclusive Thoughts

UWM Holdings Corporation remains solid despite its hammered revenue growth. It has improved viability and liquidity. Its strategies allow it to withstand market competition and navigate a disruptive environment. However, the stock price may be too high to reflect the intrinsic value of the company. It adheres to the fundamental trend but is relatively high. I want to consider it a buy, given its enticing dividend yields. But it still has to prove its dividend payout consistency since its market is more volatile than the rest of the financial sector. There may be massive changes in the core operations that may affect its viability. Although I am optimistic about its performance this year, market headwinds must not be discounted. The recommendation, for now, is that UWM Holdings Corporation is a hold.

For further details see:

UWM Holdings: Growth Remains On Hold But Stocks Still A Hold On Dividend Strength