GOOS - V.F. Corporation: Chances Of Remaining An Aristocrat

Summary

- V.F. Corporation is down nearly 57% in one year.

- V.F. Corporation is a dividend aristocrat that might not be able to retain that title.

- With a dividend that exceeds 5-year average free cash flow and a high debt load, a cut may be on the horizon.

- After looking at the risk reward profile, this is a position I am buying as a logical bet.

One of the highest yielding aristocrats

As 2023 rolls around, one of my favorite things to do to start the new year is check on the Dogs of the Dow and the dividend aristocrats list. Amongst the aristocrats was a stunner, V.F. Corporation ( VFC ), a 6.63% yield in an aristocrat? Seemed too good to be true and it may be. A yield this high amongst an aristocrat could only mean that the price had cratered, and of course, that is the case:

{kind=link}

A 56.9% one-year drop and the ominous Seeking Alpha dividend cut warning were blasting me in the face. This certainly deserved closer observation to see if this nice juicy dividend that I can drip and compound at depressed prices was truly at risk. After looking at the risk-reward trade-off, this is a position I am now buying in my portfolio.

The story up to here

What they do from the most recent 10K :

VF is diversified across brands, product categories, channels of distribution, geographies and consumer demographics. We own a broad portfolio of brands in the outerwear, footwear, apparel, backpack, luggage and accessories categories. Our largest brands are Vans®, The North Face®, Timberland® and Dickies®.

The brick-and-mortar retail locations for V.F. corporation, which they depend on for much of their sales were a bit of a mixed bag. Covid in Europe and Asia saw many of their stores open and close depending on the outbreak situation. The chart below shows the Asia-Pacific region being the final holdout for "reopening". With 48% of revenue represented by non-domestic markets, a full China reopening should be a catalyst:

{kind=link}

Further goals to improve the business from the 2022 10K are as follows:

•Drive and optimize our portfolio. Investing in our brands to realize their full potential, while ensuring the composition of our portfolio positions us to win in evolving market conditions;

•Distort investments to Asia, with a heightened focus towards China. Investing in and scaling our business across the Asia-Pacific region, especially China, to unlock growth opportunities for our brands in this fast-growing region;

•Elevate direct channels. Investing in our direct-to-consumer business to make it the pinnacle expression of our brands, and prioritizing serving consumers through e-commerce and digitally enabled transactions; and,

•Accelerate our consumer-minded, retail-centric, hyper-digital business model transformation. Becoming consumer- and retail-centric to meet and exceed consumers' needs across all channels, and operate our business differently - from the design studio to the factory floor to the point of sale - by thinking and acting more like a vertically integrated manufacturer and retailer.

Having been a frequent business traveler to China in the past, I can say that I observed the transition from ultra-luxury, Prada, Gucci, Chanel, etc. brands being the only upper-class brands, to outdoor brands gaining traction. Camping amongst retirees has become particularly popular, with mini RV/Van conversion dealers popping up across the country. Camping has become "cool" in China.

Hiking has always been a major leisure attraction in China and more and more North Face, Canada Goose ( GOOS ), and Columbia ( COLM ) products were popping up everywhere. Another positive observation I made between my first visit in 2007 and my last in 2017, was the near banning of knockoff goods. It used to be easy to buy a fake Columbia jacket and a Rolex in any major Chinese city. By my last visit, all the knockoff shops in Shanghai had been shuttered and the Silk market in Beijing or Shekou in Shenzhen were the only two well-functioning knockoff markets. The fewer of those the better, as outdoor brands were easy knock-offs.

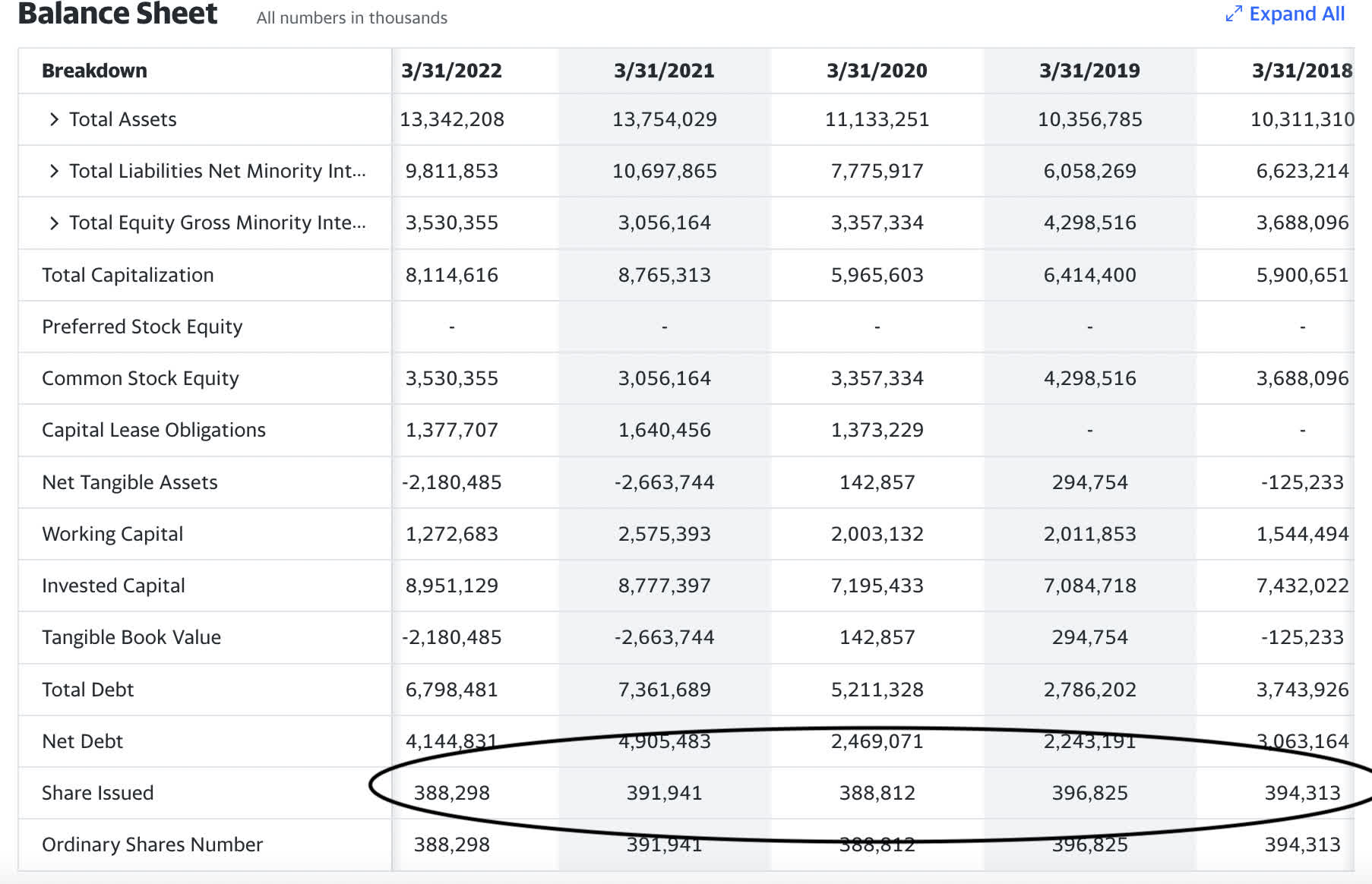

The balance sheet

{kind=link}

For big dividend payers in the aristocrat category, watching shares issued is an important factor. They function similar to REITS, often times taking on leverage and diluting equity in order to maintain and increases their dividend payments. The equation is certainly a combination of debt versus using equity to make up for shortfalls in free cash flow to issue dividends and pay down debt. Total debt peaked in 2021, ramping up significantly between 2019 and 2021 when the FED cut rates to zero. With $5 of their roughly $7 Billion in long term debt being taken on in the periods of ultra-low rates, this debt may not be as serious as it's made out to be, for now.

The dividend

V.F. Corporation is a dividend aristocrat. They have been paying uninterrupted dividends for at least 25 years without interruptions or cuts. Let's take a look at their historical data and see what the compound annual growth rate in dividends has been.

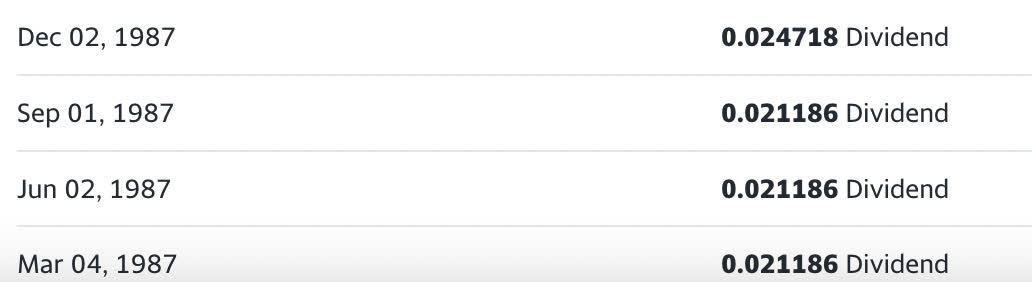

First full year of payments :

VF first full year of dividends (yahoo finance)

{kind=link}

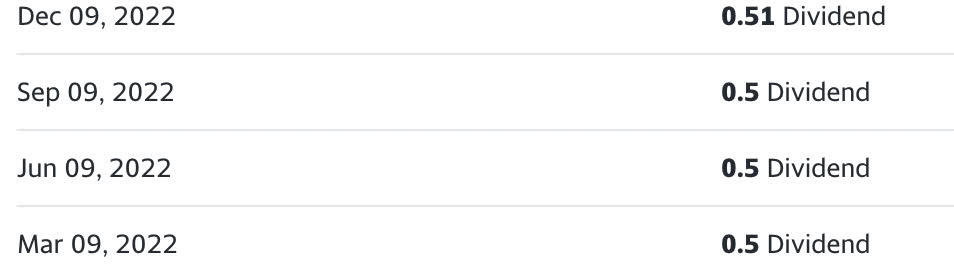

Last full year :

VF 2022 dividends (yahoo finance)

{kind=link}

The first full year of payments for Yahoo Finance's historical data from V.F. corporation was 1987, with a total of 8.827 cents a share. For the year ending 2022, the total dividend payments were $2.01 a share. In total, this is a compound annual growth rate of 9.4%, very solid indeed.

{kind=link}

This is a compound dividend model with drip. This assumption has the current dividend of 6.63% as the starting point and zero appreciation over 10 years, "even Steven". A 9.4% average dividend increase over the available historical data of the company is being assumed to be maintained over the 10-year investment going forward. With just those two elements as your return, the dividend, and the increase, you could triple your investment in 10 years without any appreciation with a 19.84% average annual return. The dividend cut rumor is circulating, but V.F. Corporation has been through years of negative free cash flow before and still maintained its dividend.

The high debt level is a worry, with rates on the rise. If the company can navigate around this inflationary period, just the dividend thesis alone might make the risk worth the reward to some people in this scenario. Also the obvious, if V.F. even achieves half of this dividend growth average over the next 10 years, there is sure to be some annual share price appreciation.

Dividend coverage

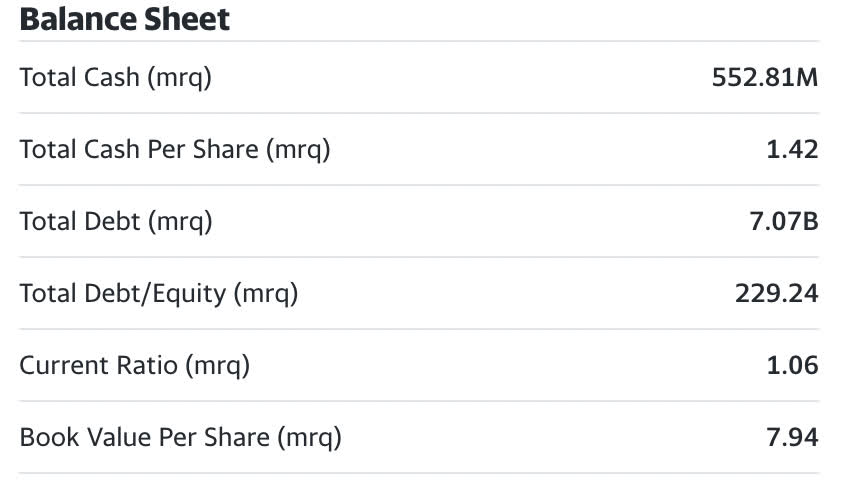

Trying to predict forward dividend coverage could lead us to all kinds of models and assumptions. I like to consider a couple of factors, firstly are they paying a lot of interest on loans and if they do will it reduce their tax liability?

{kind=link}

With a debt-to-equity ratio of 229%, this is a large number indeed. We can reasonably expect interest expense to significantly reduce tax expense, leading me to the conclusion that using Non-GAAP EBIT/EBITDA as a measure to gauge forward dividend coverage is valid in this instance.

Invert, always invert

One of my favorite mental models from Poor Charlie's Almanac refers to Charlie Munger's quotation of German mathematician Carl Gustav Jacob Jacobi:

Invert, always invert, Jacobi said. He Knew that it is in the nature of things that many hard problems are best solved when they are addressed backward.

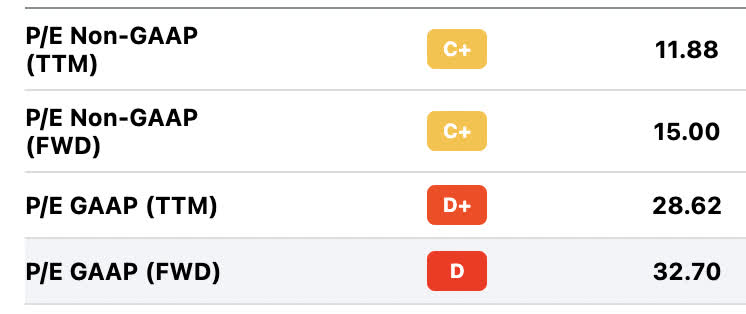

The inversion model is one that I like to relate to earnings yield versus P/E ratio. Simply, the yield is the inversion of the ratio. Treating stocks more like bonds to break down their possible yields leads to easier visualization of simple risk-free rate discounting and assumptions about dividend coverage.

{kind=link}

Focusing on Seeking Alpha's Non-GAAP current and forward yields we get the following. The current Non-GAAP yield is 1/11.88= 8.41% and the forward estimate is 15 which is equivalent to 6.66%. With many estimating that due to Covid restrictions worldwide being almost a done deal, earnings may improve with increased foot traffic and better direct-to-consumer initiatives. If we average the TTM and forward numbers we get an average Non-GAAP earnings yield of 7.5%. With the forward dividend being 6.55%, we can assume that the dividend may be covered by Non-GAAP earnings with 1% of the yield to spare. The payout ratio of Non-GAAP earnings would be 6.55/7.5=87.33%.

87.33% is a high ratio, but if you observe the V.F. Corporation balance sheet, they teeter-totter from year to year between increasing and decreasing the share float. I would predict 2023 would be a year of dilution to pay down debt or reinforce their cash buffer, but if the Non-GAAP earnings yields hold up, V.F. Corporation should be able to maintain the dividend.

Catalysts

Morningstar analyst reports are expecting some of V.F. Corporations' margins to expand. Analyst David Swartz predicts margins increasing to 18% led by Supreme and Vans, hailing their reconfiguration of the Men's skating brand (Vans), into one that is now everyday apparel. One amazing fact that Swartz pointed out is that 60% of Vans customers are now purchased by girls and women. Having grown up in the era of skater apparel, seeing the transition and survival of Vans is a rarity amongst the mishmash or brands that went from popular to non-existent . Continued success in margin expansion that should happen naturally as the cost of goods sold and inflation cool is my #1 catalyst. V.F. Corporation's brands are priced mid-range versus their high-upper-end competition such as Canada Goose, RAB, or Kuhl. They should be able to maintain their sales demographic in a possible recession.

Risks

More global shutdowns or a deteriorated market share could force a dividend cut. While Window shopping my local Scheels the other day, I spotted a couple more prominent outdoor brands I hadn't noticed before, RAB and Kuhl. One is a high-end British outdoor wear company and the other is German. They are not new, but when they start marketing at the average Joe's everyday sporting goods shop is something I hadn't noticed before. North Face's price point in this segment is still below the European brands or Canada Goose, but any sales in their territory that didn't happen before could reduce V.F. Corporation's revenue in the outdoor segment which is rapidly gaining new entrants.

Conclusion

This is a risk versus reward question. The obvious value is the company's historical ability to pay and raise dividends through crafty financial engineering. You don't often see dividend aristocrats yielding such lofty dividend payments. I am going to assume that dividend aristocrats know that they are lumped into this list and pride themselves on it. Forward Non-GAAP earnings predictions show that V.F. Corporation might be able to make dividend coverage with minimal share dilution.

Come heck or high water I think they will do everything in their power to maintain the dividend or else surrender their badge of honor that places it in dividend investor's portfolios. The company should cut its dividend and pay down debt further, but I have an inkling that they'll find a way to pay it. I like the risk-reward payoff here. Any appreciation is just icing on the cake. I just want the dividend sustained and increased. I'm cautiously betting that it will happen. This is a buy for those with above average risk tolerance.

For further details see:

V.F. Corporation: Chances Of Remaining An Aristocrat