SAIC - V2X: A Great Play In Aerospace And Defense With Low CapEx

2023-11-01 14:01:49 ET

Summary

- V2X, the merged company of Vectrus and Vertex, is projected to diversify revenues in the aerospace & defense industry with low capital costs and high potential for expansion.

- The company specializes in software, logistics, and training support for the military and other government agencies, with a focus on expanding services to non-military clients.

- V2X has shown strong revenue growth, low capital expenditure costs, and traction with large government contracts, making it an attractive investment opportunity.

Investment Thesis

V2X ( VVX ) is the new combined name of Vectrus and Vertex that completed their merger in Q2 of 2022 . Beyond the synergy of their company names, the merger is projected to diversify revenues of two very strong earners in aerospace & defense with low capital costs and high potential opportunities for expansion given the ongoing conflict in the Middle East. Short term, I expect a bump in earnings due to seasonality of the business - the US government’s fiscal year ends on September 30 th , when additional awards may be assigned - and synergized operations coming to fruition; longer term, the combined performance and growth of the company looks bright.

Upcoming earnings call on November 6 th , 2023.

Market Opportunities

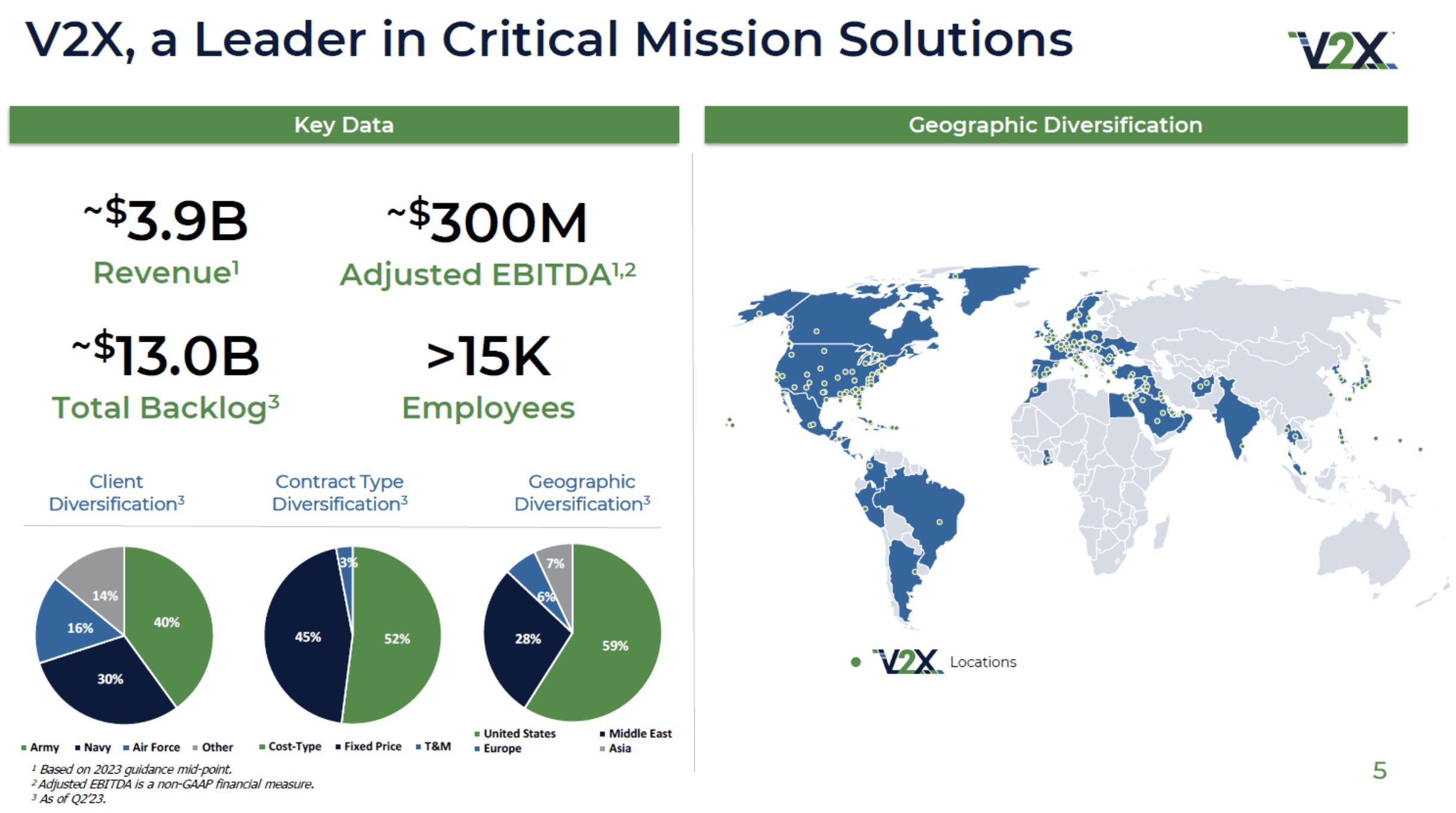

V2X Presentation (V2X Investor Relations)

{kind=link}

V2X, compared to peers like General Dynamics ( GD ) and SAIC ( SAIC ), is a small defense contractor that specializes in software, logistics, and training support for the military, other government agencies and commercial clients. 48% of its revenues are currently from overseas US contracts, but the services and support V2X offers to the military is being expanded to non-military as well. V2X operates the largest cyber-center outside of the US for the Army currently.

Management of aircraft maintenance and supply chain is just one area the firm focuses on and is expanding; aerospace supply chain improvements are desperately needed in military and non-military applications. Their solutions also expand to base and security operations management, support for national security efforts such as border and airport security programs and software, and training services to provide fully integrated customer solutions.

V2X focuses on services, software development and training support, so it has extremely low capital expenditures costs compared to a defense manufacturer, providing protections from high interest rate environments. In my view, it only has more expansion potential with commercial and overseas clientele as it carries the marketing ‘gravitas’ of working with large military clients.

The merger in 2022 was an excellent combination of highly similar firms, with varying clients and slightly better margins from Vectrus. Financing cost of the merger is creating some noise in the financials, but looking operational cash flow tells the story of a growing, profitable firm.

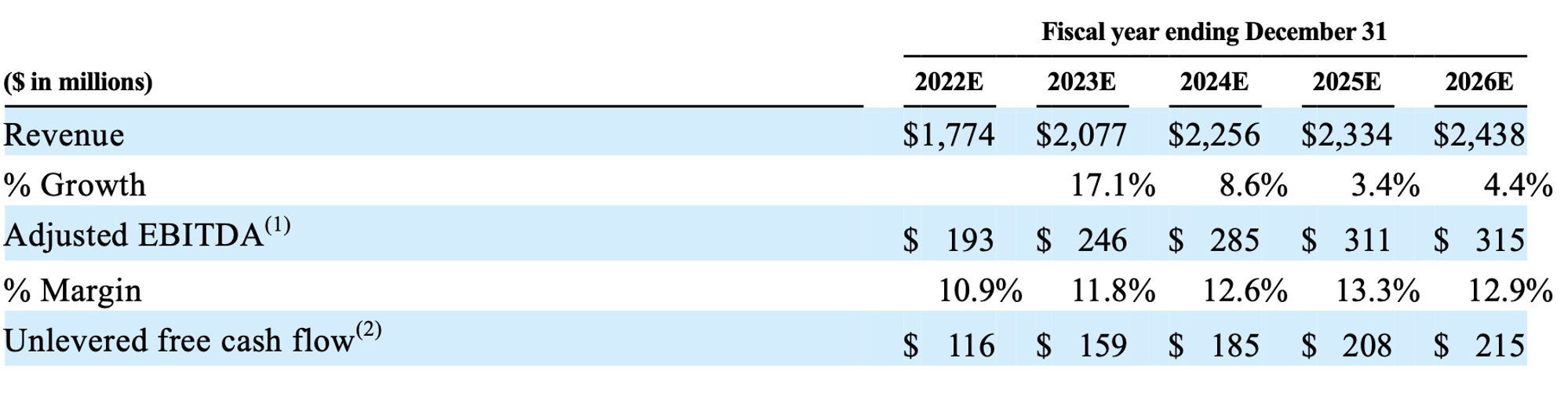

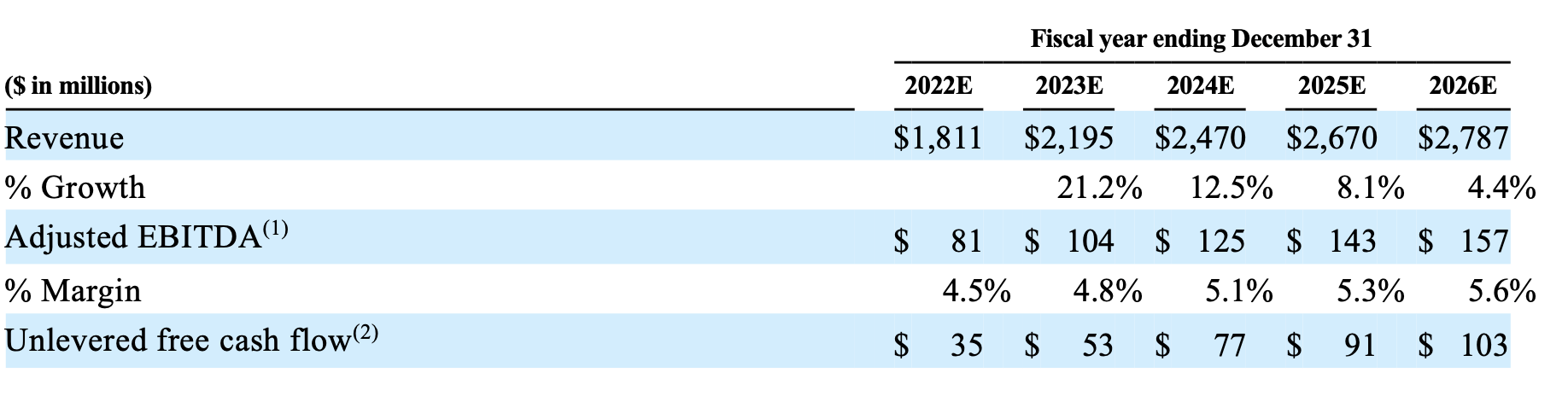

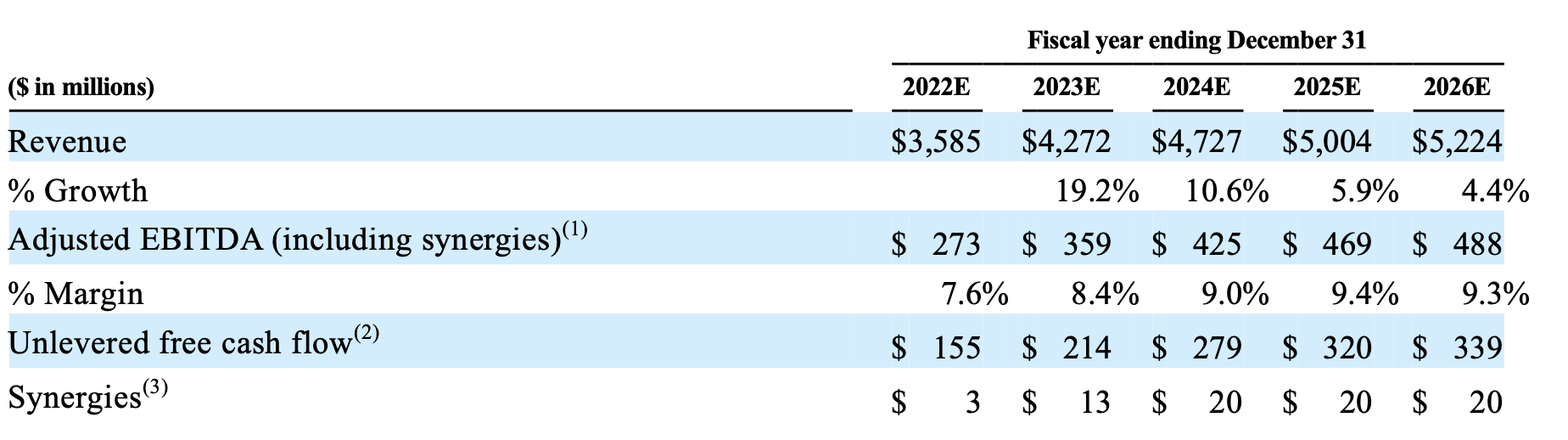

Merger Projections from 2022 Proxy Statement :

Pre-Merger (Vectrus)

Vectrus Pre-Merger (V2X Proxy Statement)

{kind=link}

Pre-Merger (Vertex)

Vertex Pre-Merger (V2X Proxy Statement)

{kind=link}

Post-Merger

Post Merger Financials (V2X Proxy Statement)

{kind=link}

I like the consistent revenue growth of the firm, the low cost of capital expenditures going forward, and the traction the firm has made with large government contracts.

Valuation

To strip away some of the merger noise and get to an apples-to-apples comparison of how the business is functioning compared to peers post-merger, I looked at General Dynamics and SAIC’s Operating Cash Flows for the trailing 12-months for comparison. Because V2X is primarily software and services, I’m less interested in looking at investing and financing cash flows because the bread and butter of the company is delivering profitable services over the long-term and the synergies of acquisition targets (of course you can use Free Cash Flow as well below, which I get to later).

| Market Cap |

| Operating Cash Flow ((TTM)) |

| Market Cap/Op. Cash Flow |

| SAIC |

| $5.67 Billion |

| $505 Million |

| 11.23 |

| GD |

| $65.1 Billion |

| $4.178 Billion |

| 15.58 |

| V2X |

| $1.58 Billion |

| $152 Million |

| 10.39 |

While SAIC and GD are clearly much larger entities, V2X only has more upside in terms of end of year increases in operating cash flow due to the seasonality of their contracts and their ability to scale existing business lines globally with new government agencies. To me, it’s reasonable to think they should trade at 11-15 x Operating Cash Flow.

| Operating Cash Flow 2023* |

| Multiple |

| Market Cap |

| Low |

| $115 Million |

| 11 |

| $1.265 Billion |

| High |

| $135 Million |

| 15 |

| $2.025 Billion |

*Provided in Investor Guidance: Q2 Earnings Presentation

With TTM already at $152 million in operating cash flows as of Q2 2023, I see no reason why they won’t hit their high guidance of $135 million or exceed it. Even with an 11x that would place them around their current price ($1.485 Billion Market Cap), but as they continue to show traction from the merger and new opportunities come from more defense and security spending across the world, I see major upside. My target is hitting $2 billion in market cap before year end, putting the share price at $64+ ($2B Market Cap/31.19 Million Shares Outstanding).

Or just look at Free Cash Flow: projections expected in the proxy statement for the merger in 2022 called for $175 million FCF and less than 1% of revenues in capital expenditures – but FCF in the TTM V2X has already hit $188 million and .53% of revenues in capital expenditures. The merger was well planned and is outperforming those targets, which is very promising. Price / Cash Flow ((TTM)) as of Oct 31 st is 10.37 at V2X, 11.23 at SAIC, and 15.56 at GD.

All of this analysis doesn’t include the long-term growth potential for the firm; with a $160 billion market opportunity and $3.8 billion in TTM net revenues, V2X has only begun to scratch the surface of what’s possible.

Downside Risks

Like all large government contractors, defense spending is always at risk of government cuts and bureaucratic disfunction. The pending government shutdown woes seem to be ebbing with Goldman less concerned than they were previously , but it’s still a risk for defense contractors. However, one could counter this argument right now with expected increases in government defense spending due to conflicts in Ukraine and the Middle East looming, however.

It’s also a highly competitive space and contracts can be taken away from large companies as contracts may be awarded to small business or other priority companies. Different government contract types can carry more financial risk than others, like fixed-price contracts that could face cost overruns.

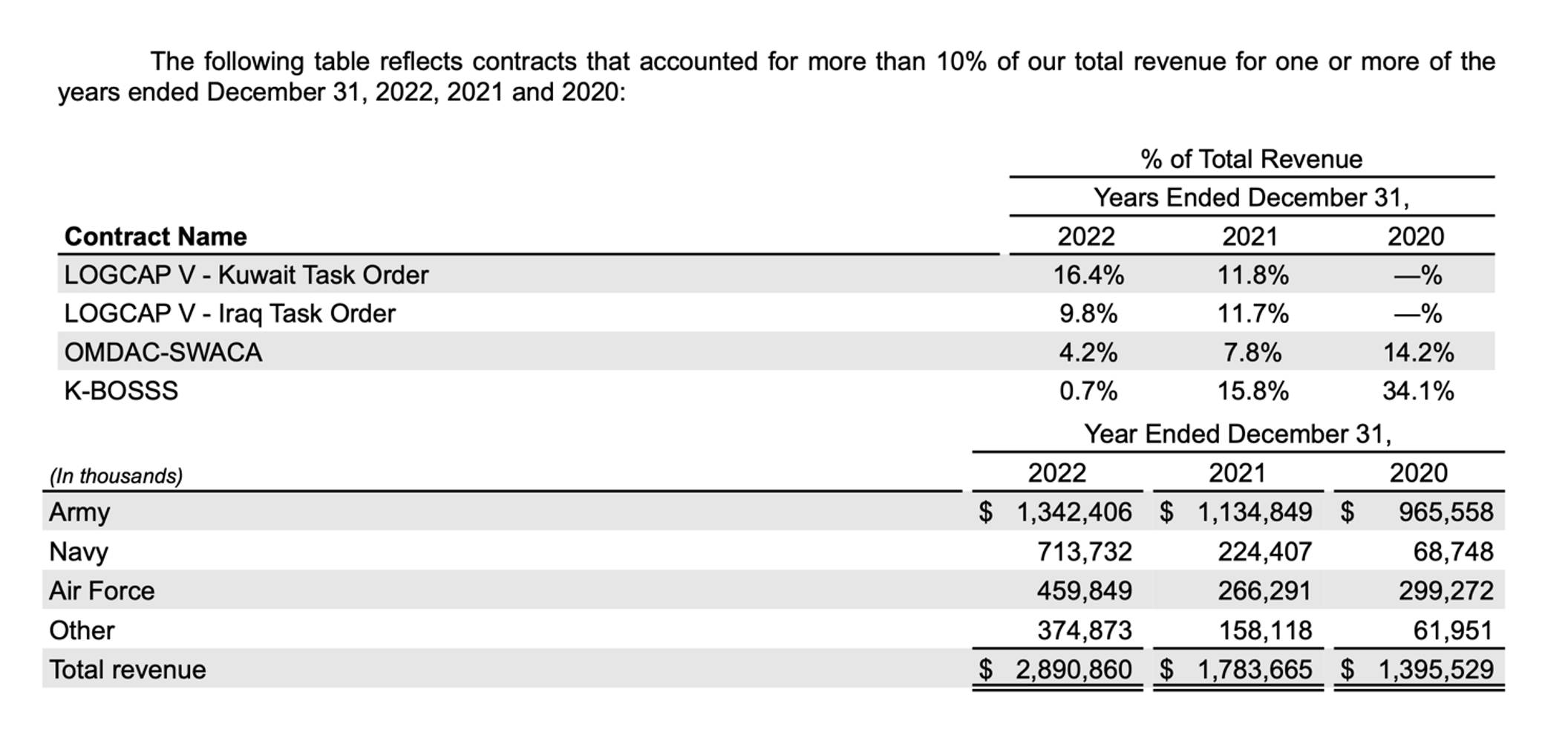

Customer and contract diversity is a key concern when looking at defense contractors, and V2X has their fair share. Tables below on this mix from the 2022 10K . The LOGCAP V – Kuwait Task Order contract is a whopping 16.4% of 2022’s revenue with its first possible end-date, depending on the Army’s option to renew, ends June of 2024.

{kind=link}

Lastly, labor concerns continue to hit every sector and 35% of V2X’s labor is unionized . They have workers in high-risk and dangerous work in war zones, and V2X could incur substantial costs due to these risks.

Summary

V2X has shown considerable traction and solid management for years. Any aerospace & defense contractor is going to carry similar risk factors, but with the state of world affairs, I believe it’s a great time to be looking for value in this sector. Beyond war-related support, V2X is expanding its footprint into non-military areas and diversifying its customer base. The need to maintain equipment and aircraft and security services is only growing in commercial and government sectors globally.

For further details see:

V2X: A Great Play In Aerospace And Defense With Low CapEx