VCSA - Vacasa: Positive Signs Appearing But Still Not Enough

2023-12-01 10:17:47 ET

Summary

- Vacasa reported strong 3Q23 results, beating revenue estimates and showing improved profitability.

- The decline in gross bookings was a deliberate strategy to drive occupancy levels higher and attract budget-conscious consumers.

- The issue of home supply churn is being addressed with increased sales force productivity, but more visibility is needed for improved demand trends and stabilization in the supply situation.

Investment action

I recommended a hold rating for Vacasa (VCSA) when I wrote about it the last time , as I believed there wasn't any catalyst to re-rate the stock higher and also that supply churn issues continue to persist. Based on my current outlook and analysis of VCSA, I recommend a hold rating. I think there are positive signs popping up in VCSA performance, like the improvement in EBIT margin and the potential for the home supply situation to ease. I think more has to be done. I would wait for more visibility into the demand trend and stabilisation in the supply-churn situation before turning bullish.

Review

VCSA reported pretty strong 3Q23 results, though it was supported by strong summer season demand. The company reported $379 million in revenue, beating consensus estimates by 9%. This is a very good start to showing that management execution is on point and is beating the street's expectations. While gross bookings of $830 million fell by 14.3% year over year (but were still up 33.4% sequentially), note that the decline was almost entirely driven by the 13.8% y/y decline in pricing, or, in other words, gross booking value per night. This does not represent any weakness in the VCSA business; rather, it was a deliberate strategy by management to drive occupancy levels higher. I thought this was a well-thought-out strategy that fits the current macro climate. Consumers are being strict on their wallets now, and instead of sticking to pricing, amidst the industry-wide pricing pressure, reducing prices and growing via volume made a lot more sense. This could also be seen as a form of marketing, where VCSA attracts consumers who are "trading down" from more premium vacation rental places.

{kind=link}

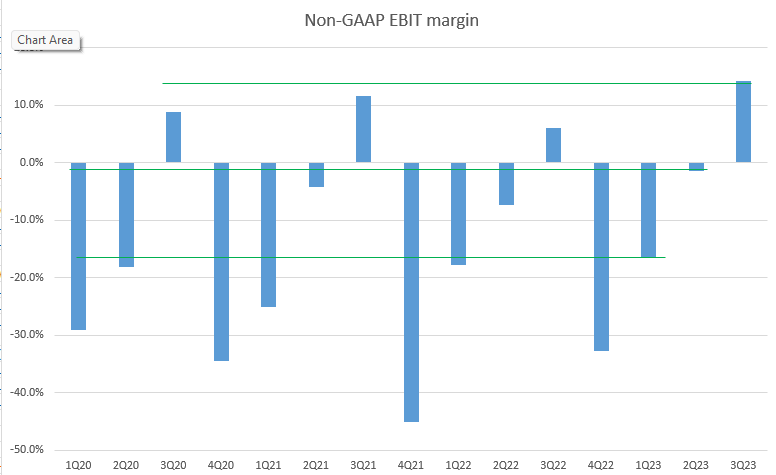

Importantly, management execution on improving profitability is on point as well. Relatively to the past 3 years, the 3Q23 non-GAAP EBIT margin is the highest. Significant improvements can also be seen in 1Q23 and 2Q23 as well. These improvements tell me that management is seeing success in optimising operating expenses, driving local market efficiencies, and making technology improvements.

These technology tools bring efficiency to our local market operations and more immediately to communications with homeowners, a win for our homeowners, a win for our guests and a win for Vacasa. 3Q23 call

Regarding the issue with home supply, macro concerns are driving elevated levels of home supply churn (homeowners not listing) as rental income rates are coming down. While management cannot do anything to solve the macro issue - they are at the mercy of the Fed adjusting rates - I thought it was encouraging that management is pushing its local sales force to bring more supply to the platform. Notably, there was increased productivity compared to last year. For readers who are unaware, this home churn issue has been a major drag on the VCSA stock narrative over the past few quarters, as this directly impacts growth in the near term. The reasoning is that, with less home supply, the VCSA platform becomes less attractive, which draws in less demand (a chicken and egg problem). Now that VCSA is seeing increased productivity, this should elevate concerns about a lack of supply weighing on growth.

While I do believe VCSA is making progress, I am waiting for some near-term indicators to improve before I become bullish. For example, I think many of the present trends, such as the normalisation of traveller demand for domestic and non-urban vacation rentals, will continue to affect growth and homeowner retention, and management expects these trends to persist. For now, I'd rather wait for the effects of normalisation to fade. Additionally, I am concerned about the volatility of margin improvements due to VCSA's continued focus on investments in customer support and platform improvement through new product rollouts. These investments are usually upfront, which could mean pressure on margin in the near future.

Reiterating my original viewpoint on VCSA, in the long run, I think the bull case is that VCSA is exposed to the secular tailwinds of the alternative accommodations market. However, I am looking for better visibility into the normalization of demand trends and stabilization in the home supply situation.

Valuation

Author's work

Updating my model, I am using management FY23 guidance for my FY23e estimates, which I think is achievable based on 3Q23 and 9M23 performance. However, with lower visibility on demand trends, I am keeping a very conservative stance on FY24 performance, assuming that it will be a year of stabilisation (flat growth). In FY25, I am assuming the industry will normalise and VCSA will be able to grow slightly below Airbnb's FY24 expected growth rate (11.4%). While I expect FY25e to see normalised growth, I think the market will not rerate the valuation until the trend has stabilised (maybe in late FY25e, when management gives commentary about FY26). As such, I am assuming the same 0.3x forward revenue multiplier. My model showcased the potential upside; however, I am giving it a hold rating until there is more visibility.

Risk and final thoughts

The upside risk is that faster growth in travel demand could cause bookings and revenue growth to outperform my estimates, which the market will take as a very positive sign that this is the start of the anticipated recovery cycle. In summary, despite positive signs emerging in VCSA performance, I maintain a hold rating due to ongoing uncertainties. Concerns persist regarding demand normalization, home supply stability, and potential margin pressure from ongoing investments. The narrative around supply issues, impacting growth, seems to be alleviating with increased sales force productivity. However, I think VCSA needs to show in the results that the supply situation is improving before the market will give credit for this improvement.

For further details see:

Vacasa: Positive Signs Appearing, But Still Not Enough