VAL - Valaris: Benefiting From Offshore Boom

Summary

- Valaris is the world's largest offshore driller by fleet numbers.

- Following a widescale industry bust, offshore drilling is progressively coming back online.

- Despite a fleet requiring calibration, Valaris is likely to benefit from this.

Macroeconomic Overview

Boom and bust cycles are nothing new for your everyday economics PhD, analyst, or data donkey. They have happened in housing, credit, and even technology during the Dot.com bubble.

Yet fast-paced reversals, the likes of which we are witnessing in global energy, seem few and far between. From a state of crisis where economies froze up, throwing oil futures into a state of flux, to one where disliked energy supermajors topped the charts for risk adjusted returns.

You would be forgiven if you missed the wave and probably initially chastised those who made such an outlandish call.

In my recent article regarding Noble Corporation ( NE ), I argued that complex economic forces had pushed a boom-and-bust cycle rarely as pronounced as the latest one in global energy. Business cycle theory has been known for decades – economists Arthur F. Burns (remember him?) and Wesley C. Mitchell vividly wrote about them in the 1946 piece “Measuring Business Cycles”.

“The economy of the Western World is a system of closely interrelated parts. He who would understand business cycles must master the workings of an economic system organized largely in a network of free enterprises searching for profit. The problem of how business cycles come about is therefore inseparable form the problem of how a capitalist economy functions”

Arthur F. Burns.

What Burns misread was the growing importance of social license, not only in today’s political panorama but modern economies. Perhaps in the space of 20 years, we have gone from a world of open borders, big energy, free-trade, and interconnectivity to one of disparate states fighting for resource nationalization, a shuttering of world trade and a wave of insourcing, even at the expense of margins. These phenomena are highly bullish for global energy.

It positions us nicely to discover another drilling contractor – Valaris ( VAL ). This offshore drilling contractor borne out of a pandemic-induced bankruptcy reorganization is positioned well as energy exploration starts to ramp. My outlook for the firm remains bullish with a caveat regarding its fleet of units. Let us find out more.

Company Introduction

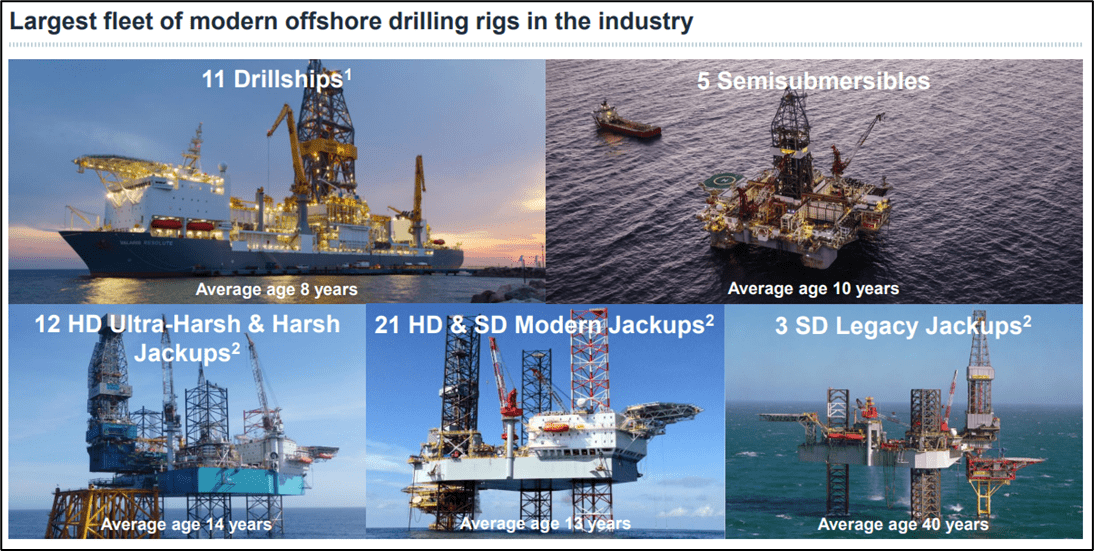

Valaris Limited in an industry leader in offshore drilling providing services to energy supermajors. With a fleet of more than 50 rigs, it is also the largest drilling contractor, at least by fleet numbers. Currently the venture operates 11 drill ships, 5 semisubmersibles and 36 jack-ups with a book value more than $8B.

It’s a large drilling contractor with Texan pedigree that has grown through a wave of mergers, tie-ups, and reorganizations. Following a merger with Rowan Companies in 2019, the company rebranded itself to Valaris. By mid-2020, at the height of the pandemic, the company filed for bankruptcy, emerging roughly one year later.

{kind=link}

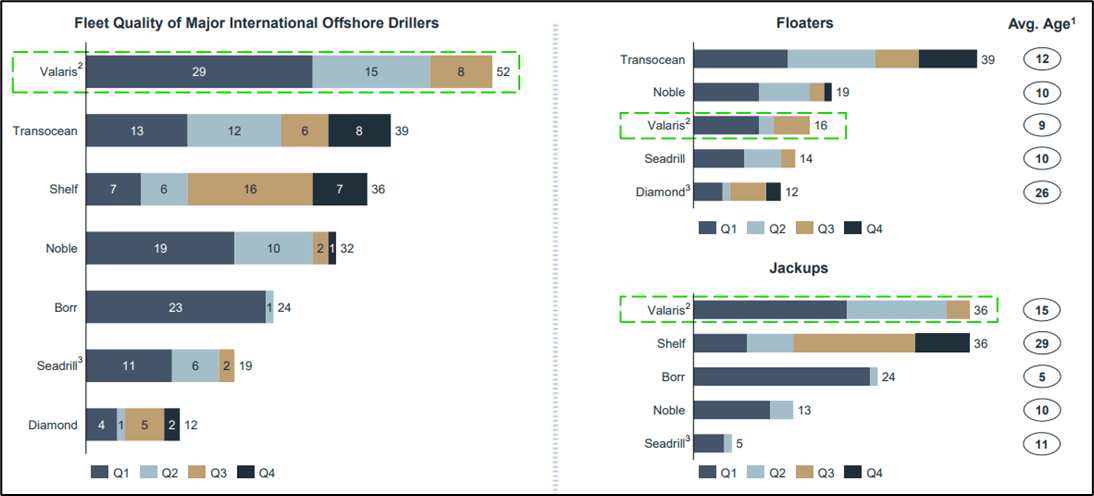

Valaris has a diverse set of units, covering all operating conditions but remains perhaps too exposed to shallow water.

Fleet Composition

Valaris' fleet tells us a lot about prospects – its deep-water segment showcases a lot of (relatively) new kit, with 6 th generation drill ships making the starting line-up, along with a handful of semisubmersibles.

These ultra-deep-water beasts are best primed for costly and complex exploration campaigns in Latin America & West Africa. They command lofty day rates (upwards of $500K/day) and compete in a highly lucrative niche of the offshore drilling segment. Project sanctioning in Brazil’s deep-water pre-salt fields and in Guyana’s fledgling oil leases are likely to sap a considerable amount of this supply.

{kind=link}

Despite having a large fleet, Valaris is heavily exposed to less lucrative shallow water campaigns.

The standout feature, however, is the amount of old-school jack-ups on the company’s books. Not only are they old (average age 13 years) but they occupy a niche that is less lucrative and presents less meaningful barriers to entry. Want an ultra-deep-water 6 th generation drillship? You are only going to find that with a handful of players in the world capable of delivery. But want a shallow water jack-up? Almost every man and his dog could front one. Ok, I exaggerate.

{kind=link}

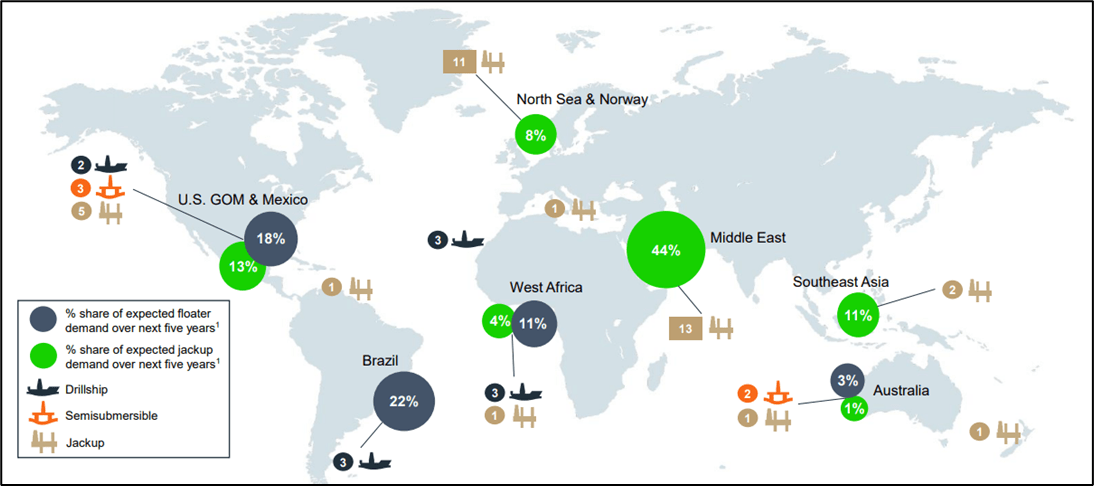

The company’s focus on shallow water middle eastern oil and the North Sea underline shifts in energy production in a post-Brexit era.

In any case, jack-ups are most common in the harsh climes of the North Sea, the Middle East, and select parts of shallow water Southeast Asia. They command significantly lower day rates (~$100k to $200k) and occupy a fiercely competitive niche.

That is the underlying issue with Valaris – its fleet is squarely aimed at small margin, big competition part of the playing field. Consequently, expect assets to continue to be reshuffled with select offloading of older, out-of-date shallow water units.

{kind=link}

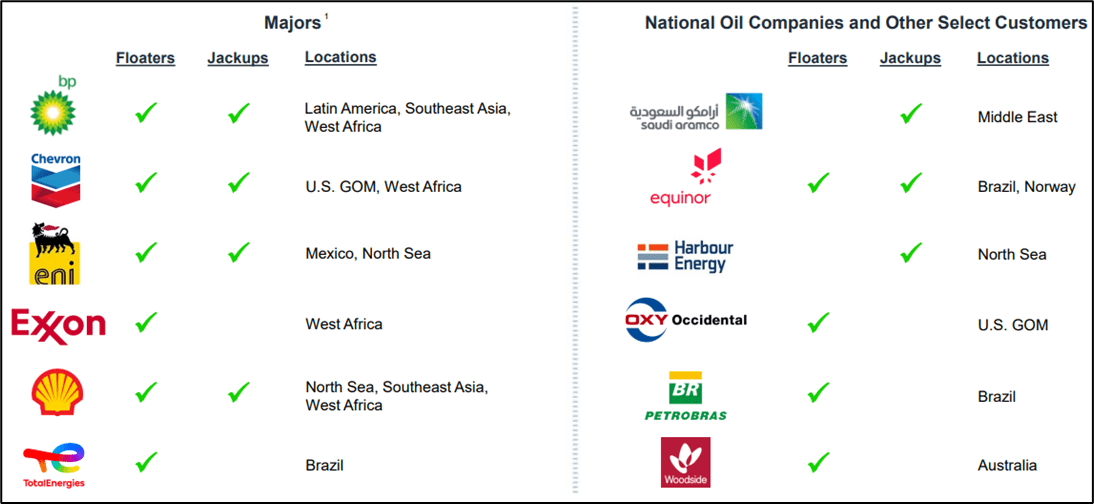

The company boasts a nice mix of international and national oil companies.

Company Financials

Valaris has undisputedly a strong financial footing, remnants of a bankruptcy reorganization that saw equity holders wiped out. It is one of only two major offshore drillers holding a net cash position ($406M over LTM and an additional $220M in liquid short-term investments).

That’s great news but the organization’s beefed-up balance sheet is more a product of the bankruptcy reorganization than prudent and conservative financial stewardship. The company holds $550M of senior secured notes due 2028 and a cash interest expense of around $45M.

Understandably, a knife has been taken to operating expenses with selling, general and administrative costs diving from $200M (FY 2020) to $60M over the last 12 months.

Sales during that same period have been roughly $1.4B – still a long way away from the glory days almost a decade ago when sales were well above $4B. Net incomes have often been hard to decipher with offshore drillers that use asset-write downs and impairments to manage earnings.

{kind=link}

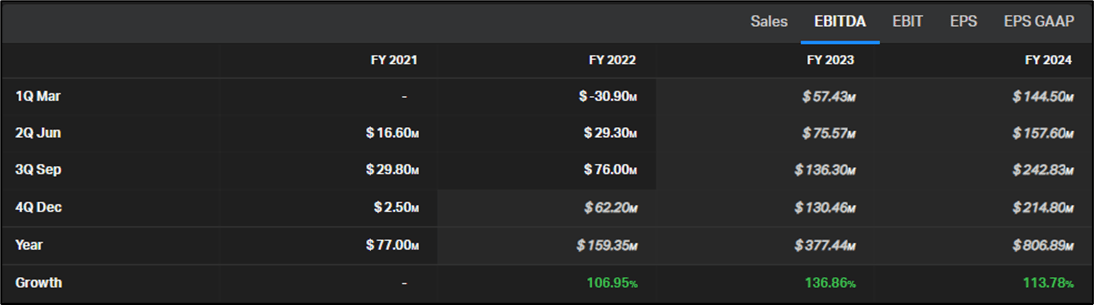

Analysts have forecast big growth in company EBITDA, reflective of the general industry outlook.

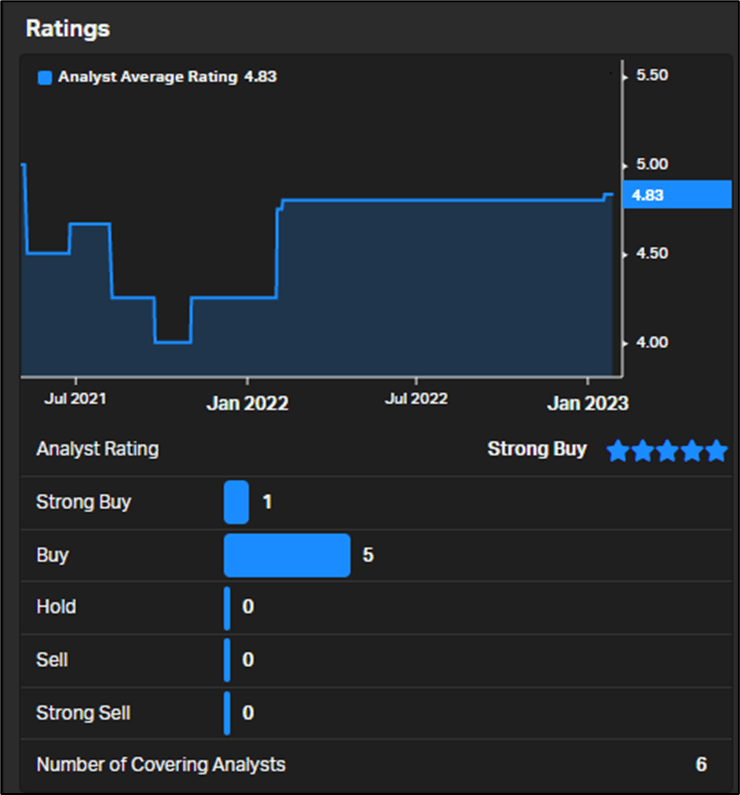

Expect an uptick in results nonetheless – analysts have penned in sales of $1.59B (FY 2022) and $1.85B (FY 2023) matched by a boost in EBITDA, from $159M (FY 2022) to $377M (FY 2023). That is positive news for holders of the equity. The collective bullishness persists in price targets for Valaris, with consensus for a twelve-month stock price being not far from $100 – roughly 28% higher than the firm’s current level.

{kind=link}

The 6 analysts covering the stock have tabled buy or strong buy ratings with a 12-month average price target of $95.67

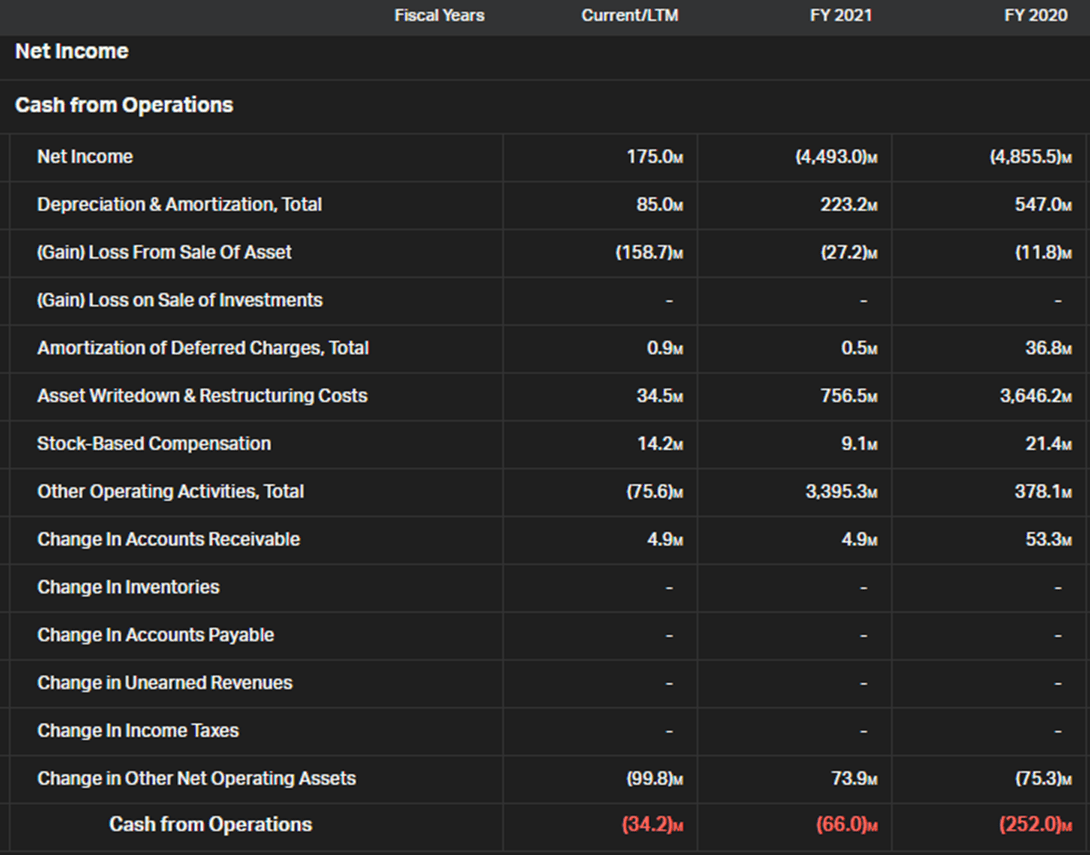

Cash flows from operations are still negative but the margin is narrowing – from -$252M (FY 2020) to -$34M over the last 12 months. That trend is likely to follow as super majors, pressured by governments and incentivized by oil prices, start to bring new exploration campaigns online.

{kind=link}

Negative cash flows from operations are reducing as exploration campaigns come back online.

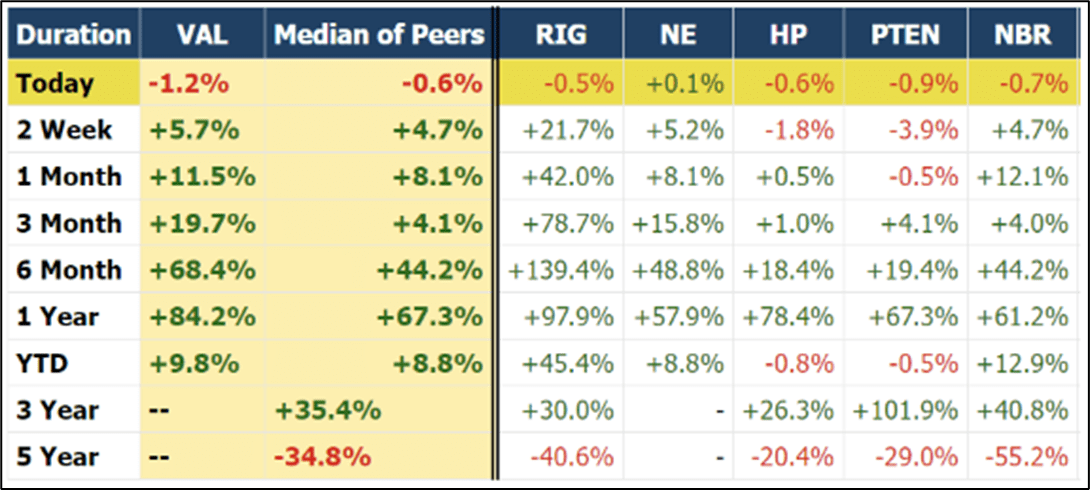

Momentum has been remarkable in the oil drilling space of late. Over the past 6 months, all the major players have seen a revival of their stock prices with a median gain of +44%. All have stood out over the past few months with Transocean ( RIG ) really making a mark for itself (+78% over past 3 months). All in, it makes for buoyant conditions for positive equity price action in the near term.

{kind=link}

Risks

The offshore drilling industry is a tumultuous one with risks not too far. Project watchers and industry pundits know all too well of the recent Covid-induced bust cycle that saw a whole heap of players lining up for bankruptcy protection.

It’s a cyclical big-ticket capex, big risk game, heavily correlated with global energy prices and credit cycles. Reorganizations came at the right time – just when interest rates were tightening but that does not mean investors take a blind eye to over-leveraged players.

Valaris presents a company-specific risk linked to its asset base – too many old-school jack-ups. This niche is highly competitive and fails to deliver the juicier day-rates found in the deep-water space. The company does have a sizable park of deep water assets but may need to recalibrate its fleet in the future.

Key Takeaways

The global drilling space is roaring back to life. As energy demands come back online following a global pandemic that wiped out a large chunk of the industry, corporate re-organizations and tie-ups have helped calibrate it with an upswing in the demand cycle.

That’s bullish for players like Valaris that, despite needing some fleet recalibration, looks primed to reap the rewards of a painful but necessary restructuring.

For further details see:

Valaris: Benefiting From Offshore Boom