VAL - Valaris: Buy On Strong Medium-Term Earnings Outlook And Inexpensive Valuation

2023-08-21 21:52:05 ET

Summary

- Valaris reported somewhat better-than-expected Q2 results, but unfavorable working capital movements and higher capex resulted in substantially negative free cash flow.

- Required reactivation of the drillship Valaris DS-7 caused management to lower near-term profitability expectations.

- However, with a number of reactivated drillships scheduled to commence higher-margin contracts in the near future, 2024 and 2025 should see very strong earnings growth and substantial cash flow generation.

- The company decided to exercise its purchase options for the newbuild drillships Valaris DS-13 and Valaris DS-14, thus increasing earnings power even further.

- Considering the strong industry outlook in combination with Valaris' inexpensive valuation based on my estimates for 2025, investors should use any major weakness in the shares to initiate or add to existing positions.

Note:

Valaris Limited ( VAL ) has been covered by me previously, so investors should view this as an update to my earlier articles on the company.

Two weeks ago, leading offshore driller Valaris Limited or "Valaris" reported somewhat better-than-expected Q2/2023 results, primarily due to higher-than-expected utilization as well as lower rig operating expenses.

However, unfavorable working capital movements and higher capex requirements resulted in negative free cash flow of approximately $100 million for the quarter.

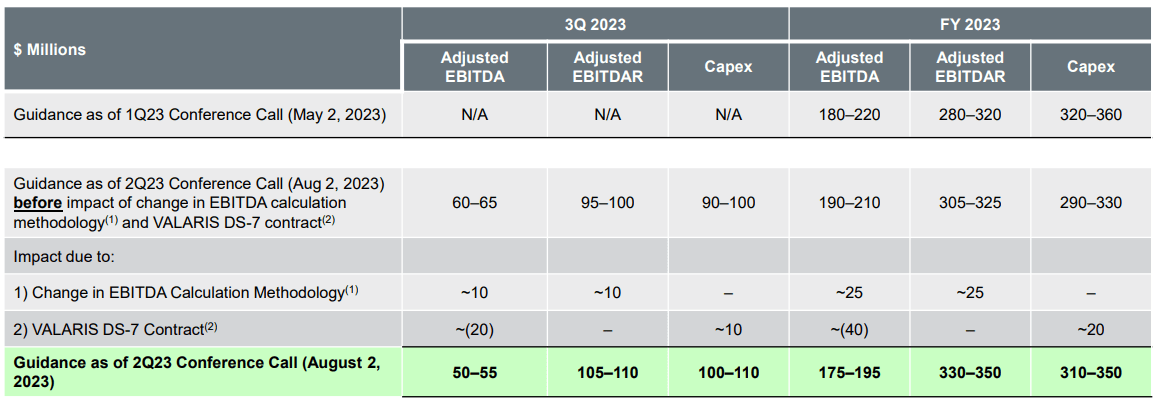

As a result of the recent contract award for the drillship Valaris DS-7 , required reactivation of the rig will result in additional near-term pressure on profitability and cash flow. That said, with an anticipated payback period of less than one year, the long-term gain appears to be well worth the short-term pain:

Company Presentation

Consequently, management reduced full-year expectations despite some benefits from recent changes in the company's Adjusted EBITDA calculation:

{kind=link}

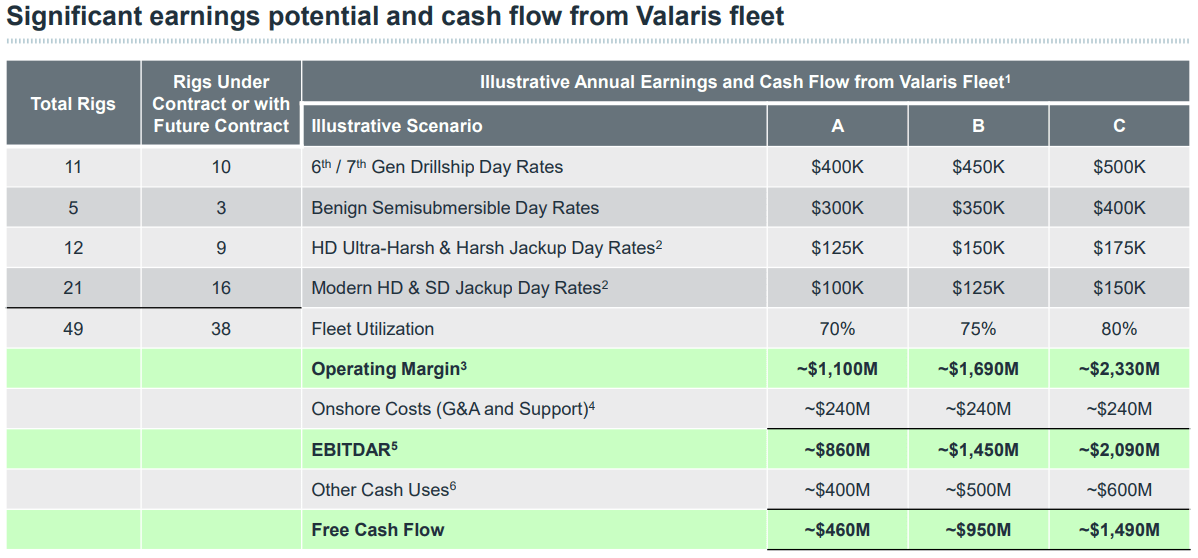

However, the investment thesis isn't really tied to the company's near-term performance as Valaris is still working through a large number of low-margin legacy contracts while at the same time facing challenging market conditions in the North Sea jackup market.

{kind=link}

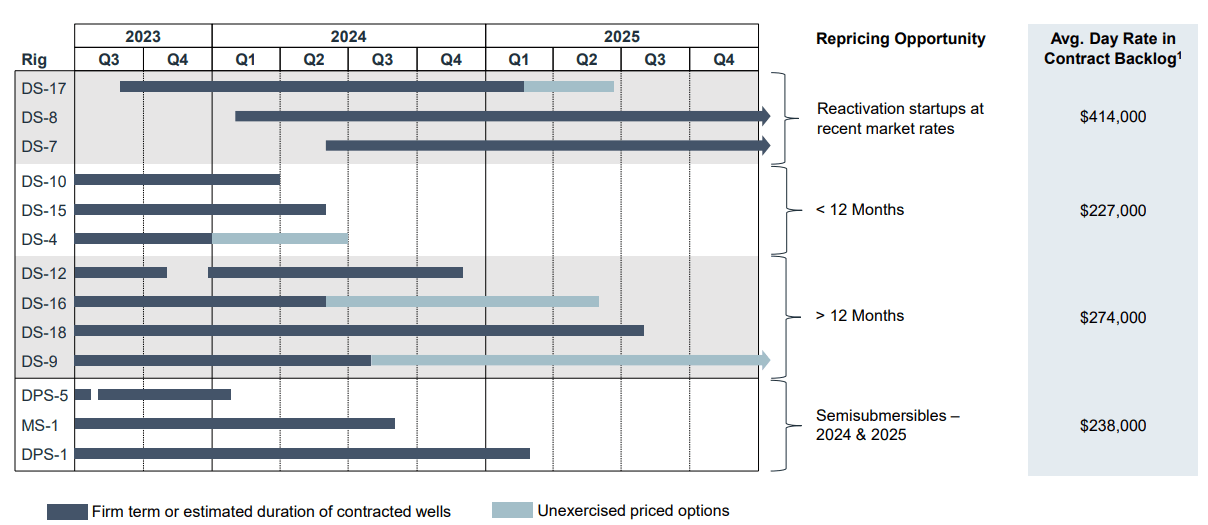

But with a number of reactivated drillships scheduled to commence higher-margin contracts over the next 12 months, Valaris' profitability and cash flow generation is expected to improve substantially in both 2024 and 2025:

{kind=link}

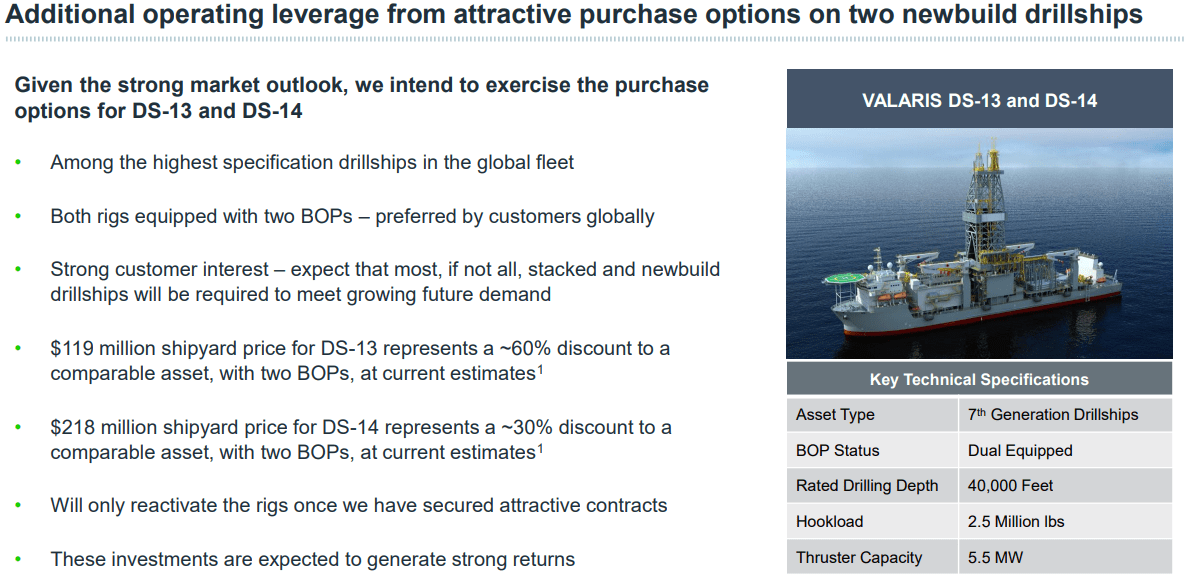

In addition, the company decided to exercise its purchase options for the newbuild drillships Valaris DS-13 and Valaris DS-14 thus increasing earnings power even further:

{kind=link}

However, absent any near-term contract awards, management expects both rigs to be stacked alongside Valaris DS-11 in Las Palmas.

Market participants apparently cheered the decision as the company's related offering of additional 8.375% senior secured notes due 2030 saw strong demand and was upsized from $350 million to $400 million.

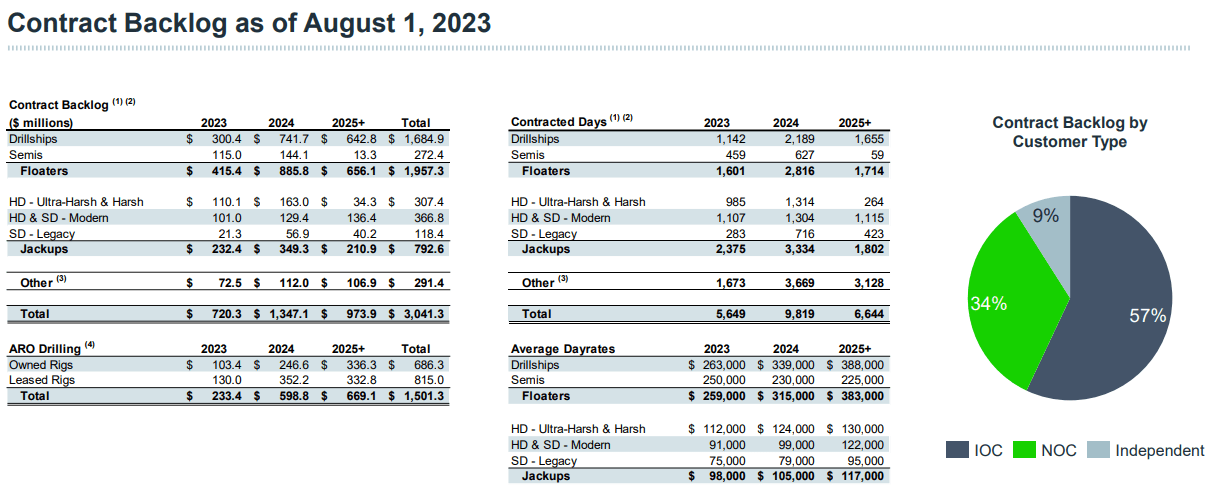

Contract backlog as of August 1 increased by 8.5% sequentially to slightly above $3 billion largely due to the above-discussed $364 million contract award for the drillship Valaris DS-7 offshore Brazil:

{kind=link}

During the quarter, the company utilized approximately $65 million in cash to repurchase 1.1 million shares at an average price of $58.82. Valaris remains committed to repurchase $200 million in shares for the full year.

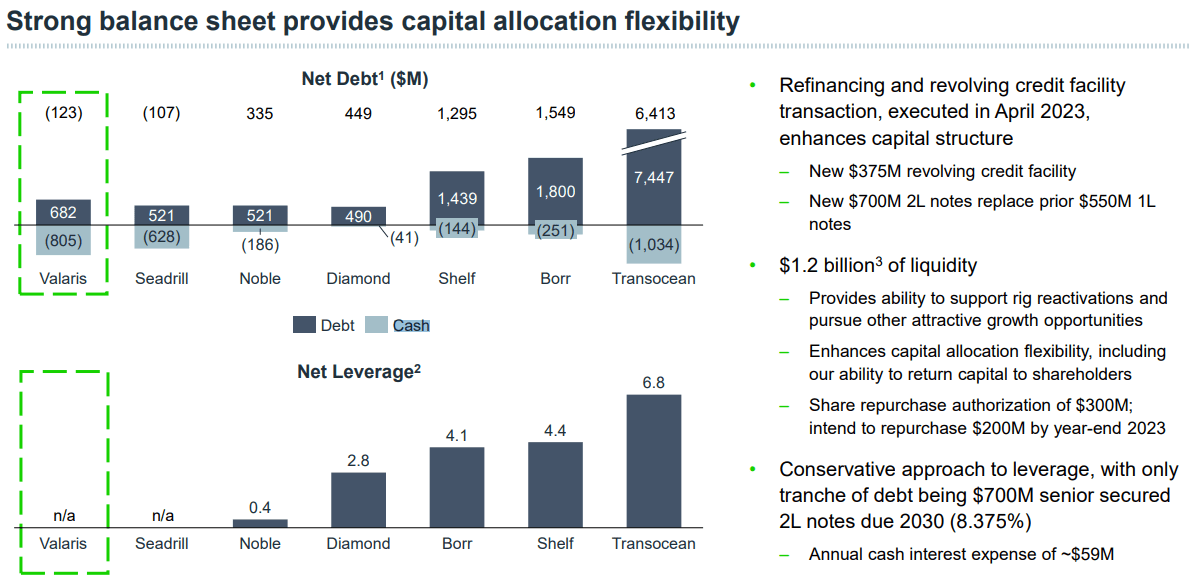

The company's balance sheet and liquidity continue to be strong and with $400 million in additional senior notes issued subsequent to quarter-end, exercising the purchase options for Valaris DS-13 and Valaris DS-14 as well as reactivating Valaris DS-7 won't be a major issue.

{kind=link}

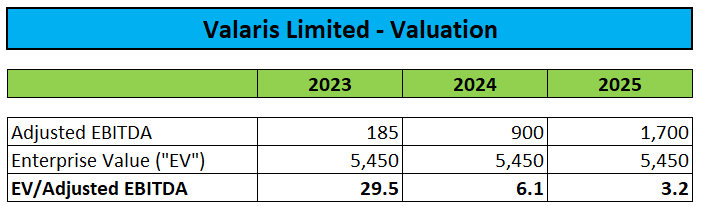

Valuation-wise, Valaris currently trades at an estimated 2024 EV/EBITDA ratio of approximately 6x, essentially in line with a number of competitors but the company remains dirt cheap based on my expectations for 2025:

{kind=link}

Assigning a 2025 EV/EBITDA multiple of 6x would result in a $109 price target for the shares and this does not even account for anticipated, substantial free cash flow generation starting next year.

Risks

Not surprisingly, offshore drilling stocks remain heavily correlated to oil prices so any sustained downmove in the commodity would almost certainly result in Valaris' shares taking a hit.

Bottom Line

While Valaris reported somewhat better-than-expected Q2 results, the upcoming reactivation of Valaris DS-7 caused management to lower near-term profitability expectations.

However, with a number of reactivated drillships scheduled to commence higher-margin contracts over the next 12 months and three high-specification drillships still waiting in the wings, the company commands substantial future earnings power.

Considering the strong industry outlook in combination with Valaris' inexpensive valuation based on my estimates for 2025, investors should use any major weakness in the shares to initiate or add to existing positions.

For further details see:

Valaris: Buy On Strong Medium-Term Earnings Outlook And Inexpensive Valuation