VAL - Valaris: Downgrading Shares On Muted Near-Term Outlook

Summary

- Leading offshore driller reports Q4 results in line with recently lowered expectations and provides disappointing 2023 guidance.

- With the majority of the drillship fleet still working on legacy contracts at painfully low rates, near-term improvements in cash flow and profitability are likely to remain limited.

- Conditions in the North Sea markets have deteriorated even further thus resulting in the decision to cold-stack a modern, harsh-environment jackup rig.

- Company needs to optimize its capital structure to gain financial flexibility and keep its options regarding the newbuild drillships VALARIS DS-13 and VALARIS DS-14.

- Considering the company's muted outlook in conjunction with the recent rally in offshore drilling stocks, I am downgrading Valaris from "Buy" to "Hold".

Note: Valaris ( VAL ) has been covered by me previously, so investors should view this as an update to my earlier articles on the company.

On Monday, leading offshore driller Valaris reported fourth quarter and full-year 2022 results largely in line with the lowered outlook provided by management on the Q3 conference call .

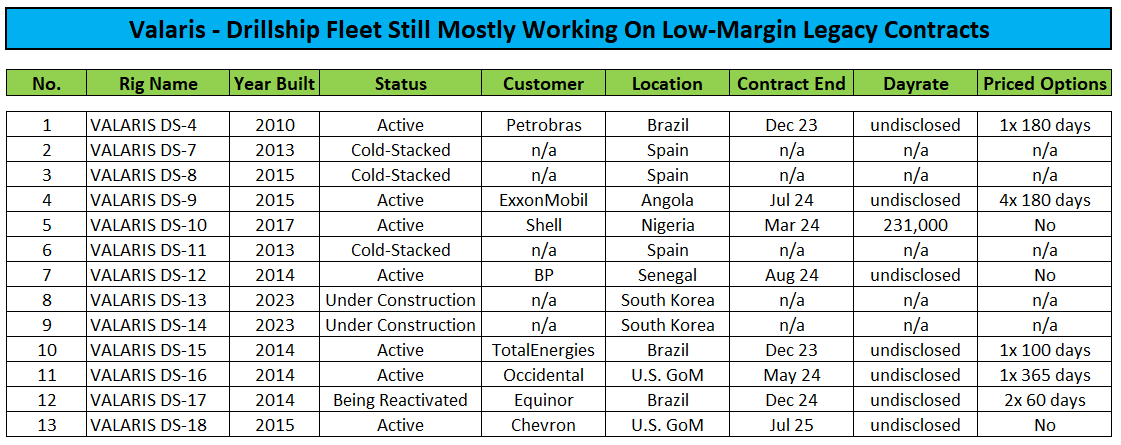

The company also issued a new fleet status report which was nothing to write home about either. While backlog increased by 3% month-over-month to approximately $2.5 billion, this was partially due to a subsidiary of Shell ( SHEL ) exercising a 330-day priced option for the drillship VALARIS DS-10 at a dayrate of just $231,000, almost 50% below current market rates.

At this point, the majority of Valaris' drillship fleet remains either cold-stacked, under construction or working under legacy contracts at painfully low or even entirely undisclosed rates:

{kind=link}

Even worse, the company has granted additional priced options to a number of customers which are very likely to get exercised in the current market environment, thus resulting in the respective rigs working even longer at below-market rates.

As a result, eagerly-awaited improvements in earnings and cash flows are likely to take longer than many market participants might like.

On the conference call , management projected 2023 EBITDA to be in a range of $240 million to $280 million, approximately doubling from very weak 2022 levels but actually a far cry from the guidance recently provided by much-smaller jackup pure play Borr Drilling ( BORR ) and a tiny fraction of floater market leader Transocean ( RIG ).

Particularly the first half of 2023 will be weak for Valaris with just 20% of full-year EBITDA expected to be generated in H1.

On the call, management pointed to further deterioration in the North Sea markets as one of the main reasons for the disappointing first half guidance (emphasis added by author):

As highlighted on our third quarter call, we do not expect opportunities to materialize in Norway until 2024. In addition, the outlook for the rest of the North Sea has softened as we are now also seeing more projects delayed in the UK with customer siding the uncertainty created by changes to fiscal policy related to windfall taxes.

Our three Keppel FELS N-Class rigs, which are capable of operating in Norway, are all now located in the UK with only the Valaris Norway partially contracted for the year ahead. The Stavanger is currently undergoing a special periodic survey, and we are actively marketing both The Stavanger and The Norway for projects in the North Sea as well as further afield. We do not see sufficient prospects over the next 12 to 18 months to keep all three of these rigs working. And as a result, we are preservation stacking the Viking in Dundee to reduce costs while the rig is idle. This uncertainty is expected to have a negative impact on our business in 2023, particularly in the first half.

While management expects the company to generate positive cash flow this year, guidance does not account for additional rig reactivation expense beyond the remaining work on VALARIS DS-17 which is scheduled to commence a new contract offshore Brazil with Equinor ( EQNR ) in June.

But Valaris will almost certainly incur substantial, additional reactivation expense as drillship VALARIS DS-8 has reportedly been awarded a long-term contract offshore Brazil by Petrobras ( PBR ). On the conference call, management more or less confirmed the award and in the question-and-answer session hinted to approximately $75 million in reactivation expense for the rig.

While there's nothing wrong with reactivating a cold-stacked asset for a long-term, high-margin contract, the negative impact on 2023 EBITDA and cash flow expectations would be very material.

In addition, management was surprisingly reluctant to commit to the company's newbuild drillships VALARIS DS-13 and VALARIS DS-14 .

As a reminder, the company has the right but not the obligation to take delivery of VALARIS DS-13 and VALARIS DS-14 for a purchase price of $119 million and $218 million respectively by year end.

Given recent acquisition prices of stranded newbuilds, one would have expected Valaris to happily exercise its purchase options for these high-specification drillships but on the call, management hinted to additional activation and mobilization expense of up to $100 million per rig.

As a result, the company has decided to prioritize the reactivation of cold-stacked drillships over newbuild deliveries but it's actually hard to envision Valaris giving up on two of the world's most advanced drillships right at the beginning of a potential multi-year upcycle.

That said, the company might also choose to sell its purchase options to a competitor which could result in an estimated cash inflow of $150 million.

On the conference call, management also spent a great deal of time discussing the company's capital structure which remains far from perfect.

While Valaris ended the year with $724 million in unrestricted cash, the company would be well-served to address its expensive and rather restrictive $550 million first lien high-yield notes and agree on terms for a revolving credit facility as soon as possible to gain additional flexibility.

Otherwise, assuming reactivation of VALARIS DS-8 and taking delivery of VALARIS DS-13 and VALARIS DS-14 , the company would have to shell out more than $600 million in cash next year including initial activation and mobilization costs for the newbuilds which doesn't look like a viable option at this point given the fact that the company needs a certain amount of cash on hand to conduct business across multiple regions of the world.

Bottom Line

Quite frankly, it's hard to get excited over Valaris' near-term prospects.

While management expects 2024 to represent an inflection point in the company's results with an increasing number of drillships expected to work at market rates and anticipated improvements in the North Sea, investors should be wary of the potential negative impact of priced options and potential additional rig reactivation expense.

Given these issues, I would expect 2025 to show a more meaningful step up in profitability and cash flow.

Considering the company's muted outlook in conjunction with the recent rally in offshore drilling stocks, I am downgrading VAL stock from " Buy " to " Hold ".

For further details see:

Valaris: Downgrading Shares On Muted Near-Term Outlook