VAL - Valaris: Shares Still Cheap

2023-07-21 09:29:07 ET

Summary

- Valaris, an offshore drilling contractor, is an attractive investment opportunity due to strong underlying fundamentals and a compelling valuation.

- We expect Valaris to start benefiting from higher day rates as legacy contracts expire and cold-stacked rigs are reactivated.

- At a conservative multiple, Valaris offers 30% upside, and we recommend building a long position on Valaris shares.

In a previous note , we presented a long thesis on Seadrill (SDRL) highlighting the strong underlying fundamentals of offshore drilling contractors, an attractive valuation, and potential catalysts. We have explored other offshore drillers, and we hereby present our note on Valaris. We think Valaris is an attractive investment opportunity offering significant upside.

Introduction to Valaris

Valaris (VAL) is an offshore drilling contractor providing services to the oil and gas industry. Valaris was created in 2019 by the combination of two leading offshore drillers with many decades of experience: Ensco plc and Rowan Companies plc. The new company was headquartered in London, and listed on NYSE. Following a substantial downturn in the energy sector, which was exacerbated by the Covid-19 pandemic, Valaris filed for bankruptcy in August 2020, reducing its debt load substantially and wiping out existing equity holders. In May 2021, Valaris emerged from bankruptcy, with a new capital structure, having eliminated $7.1 billion of debt.

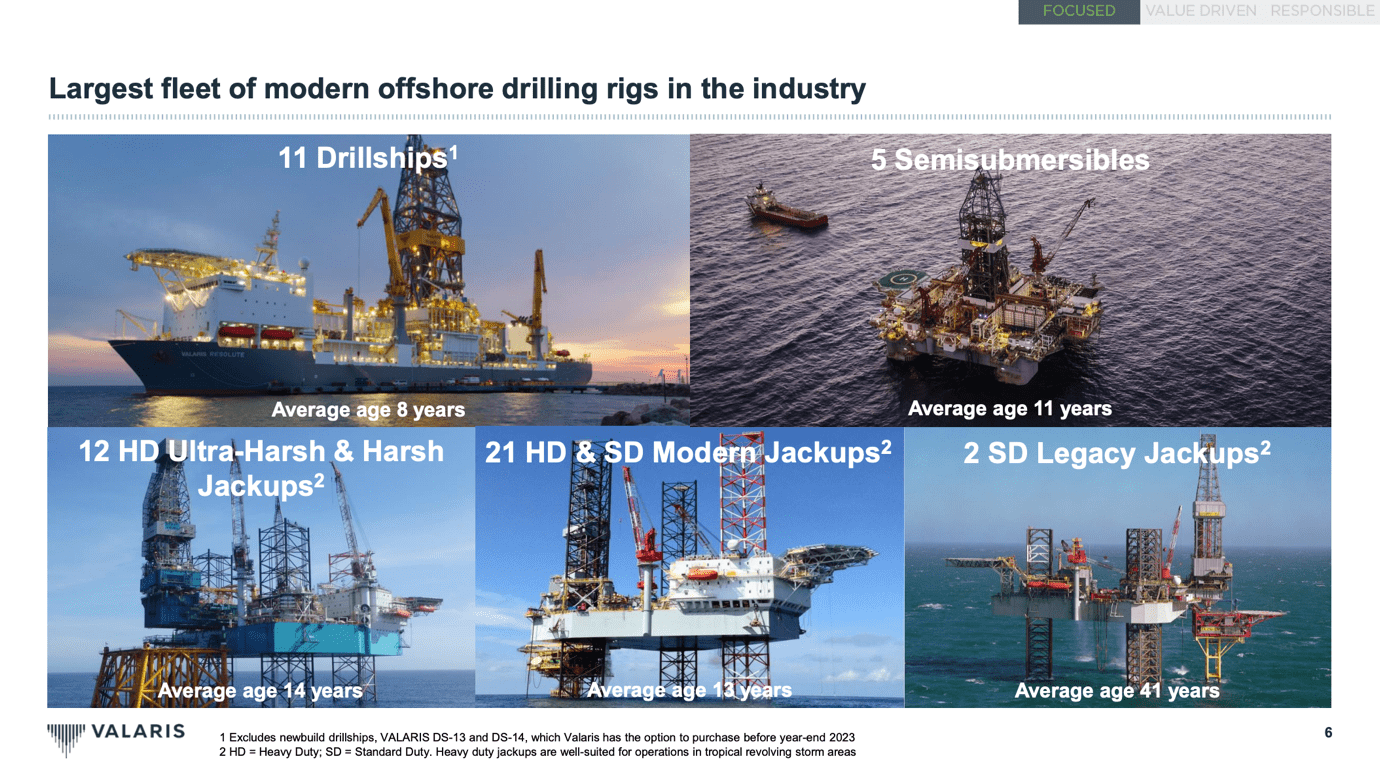

Valaris currently has the largest fleet of modern offshore drilling rigs in the industry: 11 Drillships, 5 Semi-submersibles, 12 HD Ultra-Harsh and Harsh Jackups, 21 HD & SD Modern Jackups, and 2 SD Legacy Jackups. Valaris has strong customer relationships with major international oil companies, national oil companies, as well as independents; and is attractively positioned in key basins that are expected to drive future demand for rigs. Moreover, Valaris boasts industry-leading cost structures with average SG&A costs of $11.9 million per weighted active rig

We believe Valaris is well-positioned to benefit from attractive underlying market fundamentals. We will do a deep dive into the market fundamentals, analyze key issues and drivers, and assess the potential implications for investors.

{kind=link}

Market Fundamentals

Market fundamentals have been thoroughly discussed in our note on Seadrill. We would highly suggest readers check that section of our note, as it is relevant to Valaris as well.

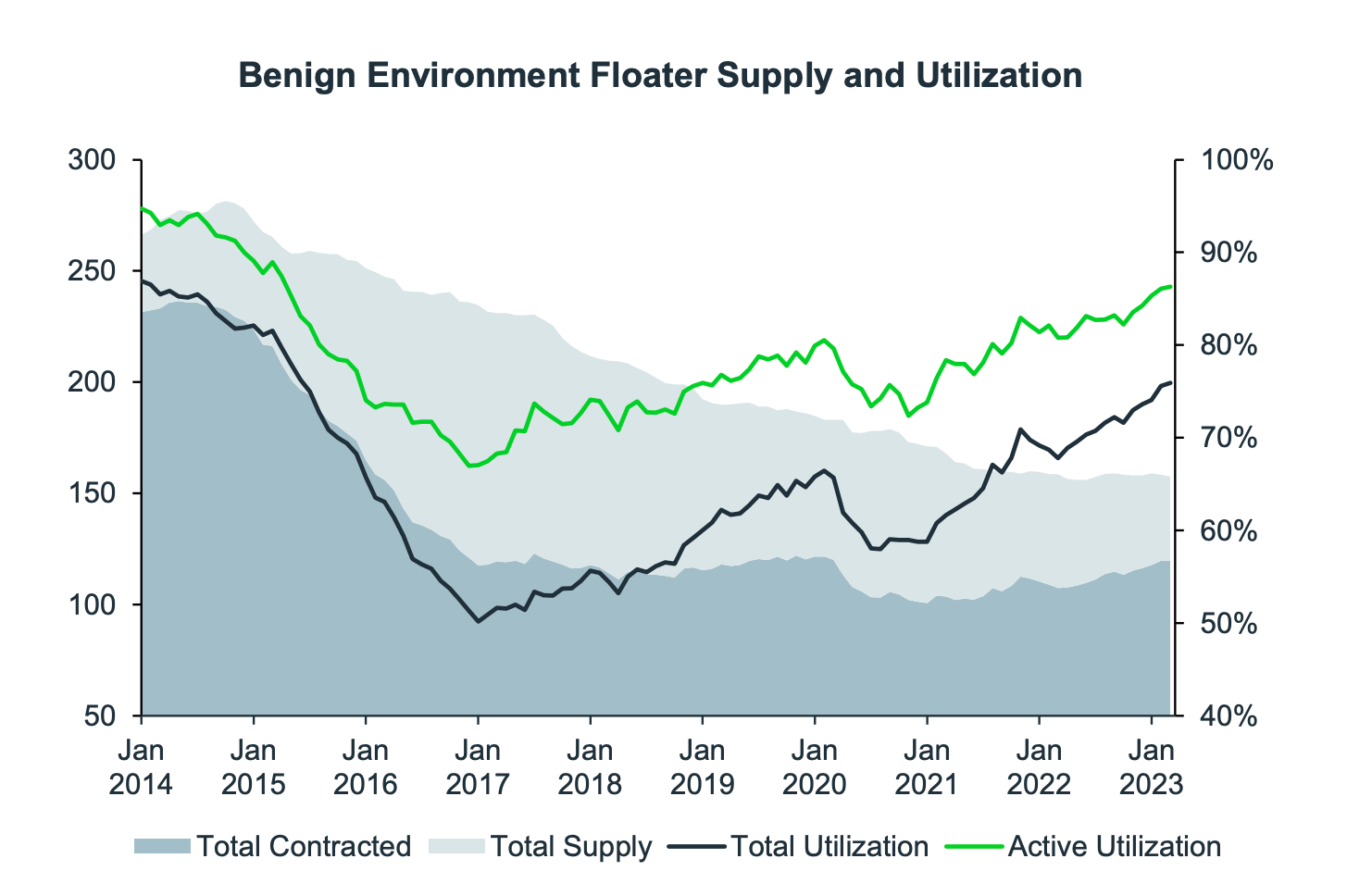

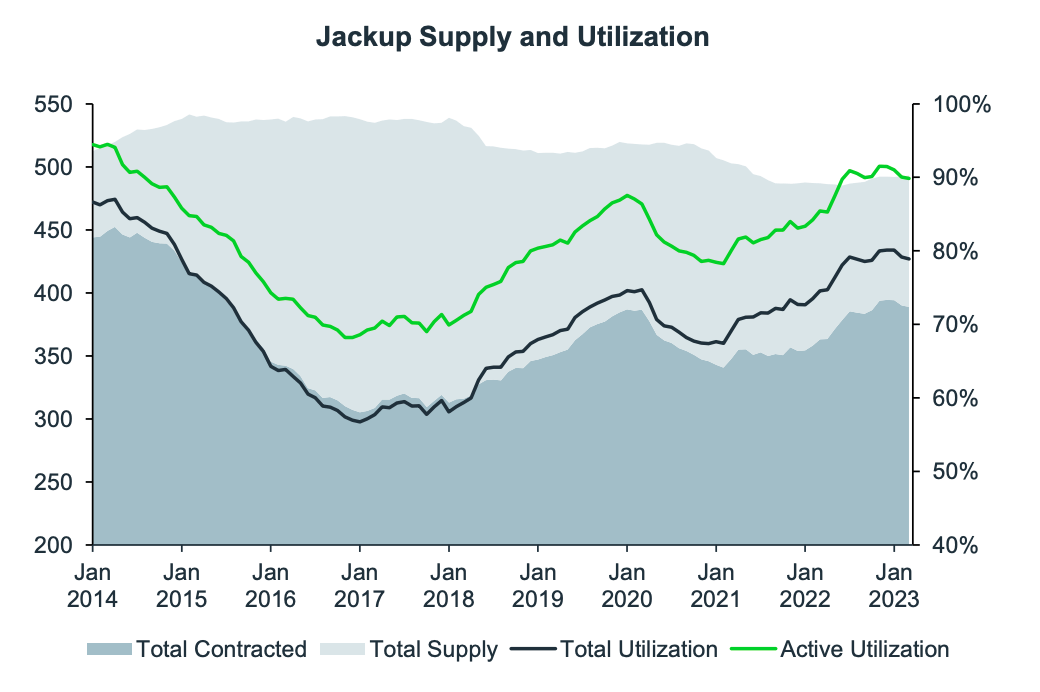

In addition to our previous note, we would like to highlight the supply rationalization mentioned in Valaris' investor presentation. This supply rationalization should allow for a sustained upcycle. Benign environment floater supply has declined by 44% to 157 from the peak in 2014, and there are only 8 newbuilds in Korean shipyards, two of which belong to Valaris. The company believes that given high costs and no / very little capacity of shipbuilders, another newbuild cycle is highly unlikely. We agree with this view, as mentioned in our Seadrill note. Moreover, Jack-up supply has declined by 9% to 493 from its peak in 2015, and 1/3rd of the current supply is older than 30 years and many of the stacked Jack-ups are not competitive due to age and capabilities/performance. Jack-up newbuilds are also not likely to pick-up, and currently, there are only 18 newbuilds 13 of which are in China and likely to remain part of the Chinese local market.

{kind=link}

{kind=link}

Investment Case and V aluation

As was the case with Seadrill, our investment case on Valaris does not rely on what seems to be the beginning of a multi-year upcycle and expectations of further day-rate increases, as Valaris is quite appealing at mark-to-market levels.

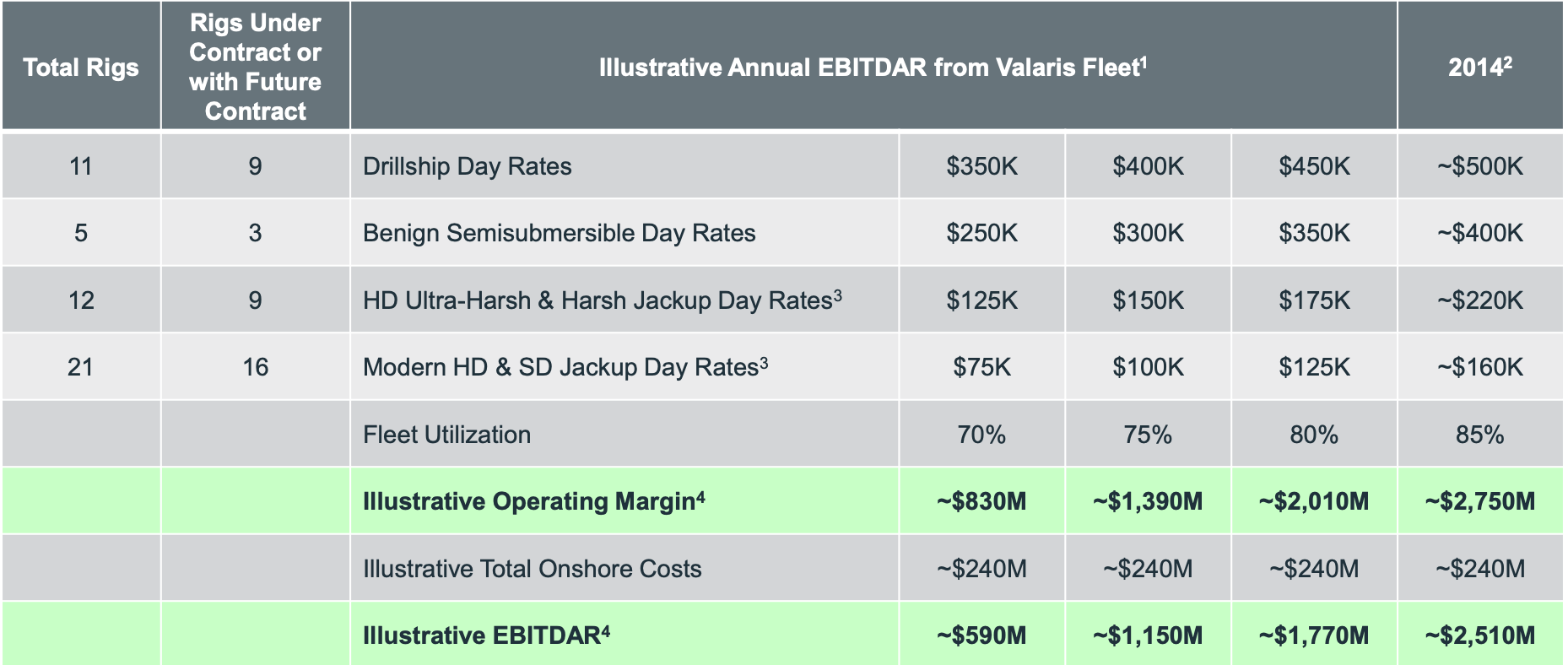

We forecast $200 million of EBITDA in 2023. The company has guided to an EBITDA range of $180 million to $220 million. With a market capitalization of $5.5 billion, a net cash position of $257 million, and an enterprise value of ca. $5.2 billion, Valaris is trading at c.26x EBITDA. Based on our 2024 and 2025 forecasts the multiple drops very sharply. We forecast $705 million of EBITDA in 2024 and $1.6 billion in 2025. Valaris is respectively trading at 7x EBITDA'24e and 3x EBITDA'25e.

We would like to point out that all 9 operational drillships are working at rates lower than $300k / day, while market rates are higher than $450k / day. As contracts expire, we expect Valaris to start benefiting from the rise in day rates. Moreover, we would like to draw attention to the fleet of stacked rigs. Valaris has a stacked fleet that includes 11 high-quality modern assets with a total build cost of $3.5 billion, with two uncontracted high-specification drillships providing operational leverage. Reactivation economics are very attractive, with an EBITDA payback period of nearly 7 months. We expect the last cold-stacked rigs to be active by early 2025 adding $400+ million of EBITDA.

Moreover, Valaris has the lowest implied steel value per ultra-deepwater equivalent rig at $207 million. Recent market transactions for drillships have averaged $300 million per drillship or nearly 1.5x.

{kind=link}

We expect modest cash generation in 2023 and 2024 due to reactivation expenses and legacy contacts. However, this should change in 2025, providing an important catalyst for the stock.

We value Valaris at 5x EBITDA 2025, arriving at an EV of $8 billion in 2025. We discount this back to the present at a cost of capital of 10% (based on a 3.8% Risk-Free Rate, 1.1 Beta - Damodaran estimate for oil and gas services and equipment, and 5.9% Equity Risk Premium) and get an enterprise value of $6.9 billion, a market capitalization of $7.15 billion and a share price of $95 / share, or 30% upside. Valuing the company at 6x EBITDA'25e and discounting back would imply 56% upside, or a share price of $114.

Catalysts

Multiple contracts will be expiring between Q3'23 and Q2'24 allowing Valaris to benefit from the new day rates. Moreover, we expect all cold stacked rigs to be active by early Q1'25. We believe these are the two key catalysts for the stock. We also applaud the $300 million buyback program and deem it a prudent capital allocation decision as shares are so undervalued. We expect more color on capital returns in future quarters, and we expect considerable shareholder distributions from 2025 when cash generation increases.

Risks

Risks include but are not limited to a decline in crude oil prices, an increase in newbuilds leading to excess supply and deterioration of market fundamentals, delays in the rig reactivation processes, inability to reactivate cold-stacked rigs, value destructive M&A resulting in an increase in net leverage, technological improvements in shale, changes in drilling technology and customer demand for upgraded technology, accidents, and weather events.

Conclusion

Valaris shares have risen by 14% year-to-date and 230% since IPO, reflecting the underlying fundamentals. We believe there is considerable upside left, at least 30% on a conservative valuation, and as EBITDA and FCF rise sharply and 2025 estimates are unrisked this value should be unlocked. We recommend building a long position on Valaris shares.

For further details see:

Valaris: Shares Still Cheap