VAL - Valaris: Uncovering Cash Flow Potential To Buy Back Shares

2023-10-05 12:41:11 ET

Summary

- Valaris Limited is positioned for substantial cash flow growth from its highly valuable offshore drilling fleet.

- Industry supply constraints and high entry barriers create a favorable market landscape for Valaris Limited.

- The restructured balance sheet, the increase in free cash flow and management commitment to returning capital to shareholders through share buybacks will be catalysts for stock appreciation.

Executive Summary

Investment Thesis: Valaris Limited ( VAL ) is positioned for substantial growth and value appreciation in the offshore drilling industry. The company's strategic advantages, including a diverse fleet of highly valuable offshore drilling rigs and a favorable market landscape, make it a compelling investment opportunity. Key factors contributing to this thesis include:

Supply Constraints: The offshore drilling sector is witnessing rising demand from major oil companies, and the supply of new drilling rigs is constrained after a severe and long downturn. This scarcity of "new tools" is driving up leasing rates, potentially boosting Valaris Limited's, earnings and cash flow. The current industry order book is minimal.

High Entry Barriers: Building new drillships is a capital-intensive and time-consuming process, with an estimated cost of at least $1 billion and several years for completion. This substantial entry barrier limits competition and enhances Valaris Limited's market position.

Deepwater Reserves: Valaris Limited is well positioned to help the major oil companies to tap into the vast and promising deepwater oil reserves, which are believed to be larger and more sustainable than onshore reserves. This provides a long-term growth opportunity as offshore exploration and production activities continue to expand.

Restructured Balance Sheet: Following its bankruptcy in 2020/21, Valaris Limited has successfully restructured its balance sheet and eliminated debt, resulting in a stronger financial foundation. The company now has a clean slate to focus on value creation and returning capital to shareholders.

Ownership Transformation: The ownership structure, initially dominated by former bondholders, is evolving, which could lead to increased investor interest and liquidity in Valaris Limited's stock.

Target Price: Valaris Limited is significantly undervalued at its current market price. I have set a target price of $250 per share within the next 12-24 months, reflecting the company's growth in free cash flow from its highly valuable fleet, and its commitment to buy back shares.

Background and Ownership

The company, formerly known as Ensco, underwent several acquisitions, including Pride International in 2011, Atwood Oceanics in 2017, and eventually Rowan Companies in 2019. This series of acquisitions led to the company changing its name to Valaris plc, which is now known as Valaris Limited. In 2020, the company experienced a bankruptcy process and successfully emerged from it in May 2021. Following the emergence, its new stock began trading in the low $20s, resulting in a market capitalization of $1.6 billion. Through the bankruptcy proceedings, the company managed to eliminate $7.1 billion in debt and was left with $550 million in debt in the form of a second lien note maturing in 2028, along with $615 million in cash. The company relocated its headquarters from London, UK, to Houston, Texas, as part of the restructuring.

Valaris Limited currently owns 52 rigs, including 11 drillships (with options for 2 more), 36 jackup rigs, and 5 semi-submersible platform rigs. These rigs are primarily contracted to major players in the oil industry over extended periods. BP stands as the company's largest client, contributing to 15% of its revenue in 2022, and Valaris Limited also maintains a significant joint venture partnership with Saudi Aramco.

Currently, there are 74 million shares outstanding along with 5.645 million warrants set to expire on April 29, 2028, with an exercise price of $131.88. These warrants were initially issued to former common stockholders. However, due to the bankruptcy proceedings, ownership transitioned to the former bondholders , with Oak Hill Advisors becoming the largest owner as of June 30, 2023. It's worth noting that in August 2023, Oak Hill Advisors sold nearly half of its holdings, reducing its ownership to 4.76 million shares, equivalent to 6.5% of the total shares. The largest shareholder is now Blackrock, a passive index-tracking investor, with ownership of 6.878 million shares, accounting for 9.3% of the total. Orbis Allan Gray Ltd, whose founder Allan Gray passed away in 2019, holds 5.076 million shares, representing 6.9% of the shares.

Several former bondholders still hold 1-3 million shares, including Lodbrok Capital, managed by Mikael Brantberg, a former investment professional at Farallon Capital, Och Ziff, and Goldman Sachs. Adage Capital, led by Phil Gross, another distressed bond investor, also retains a position within this range. Elliott Investment Management has been gradually reducing its stake but still maintains ownership within this range. Notably, there has been turnover in ownership, with larger stakes being acquired by funds like Lingotto Investment Management and Coronation Fund Managers, both of which have made recent substantial additions to their holdings.

The executive team consists mainly of new executives who bring with them extensive industry expertise. Anton Dibowitz, who took on the role of CEO in September 2021, came from Seadrill (SDRL), a competitor in the industry, bringing valuable experience with him. Chris Weber, who became the CFO in August 2022, also possesses industry knowledge gained from working in various roles at several oil and gas companies. Gilles Luca, the COO, has been part of the company since 1997 and has served in various capacities over the years.

The management team has made it clear in recent earnings calls and industry conference presentations that they are committed to returning capital to shareholders through share buybacks. They have already initiated share buyback programs and have more in store, with a program worth $300 million.

Financial Performance

Valaris Limited underwent a comprehensive balance sheet restructuring process through the courts and successfully emerged in May 2021 with a healthy balance sheet and all its assets intact. Since then, the company has experienced improvements in its earnings, but the best is yet to come. This optimism stems from the expectation that they will be able to charge higher day rates for their assets, and as they replace older contracts with contracts at market rates, there should be significant enhancements in earnings and cash flow.

In 2022 , the company reported revenues of $1.6 billion, up from $1.55 billion in 2021, with operating income of $37.2 million, a remarkable improvement from the previous year's operating loss of $897.4 million. Furthermore, the company achieved positive operating cash flow for the year, amounting to $127.5 million, compared to a negative $66 million previously. Although the pace of these improvements slowed in the first half of 2023, it was mainly due to the necessity of mobilizing assets from the less favorable Norwegian North Sea to more desirable locations. Notably, day rates have continued to rise.

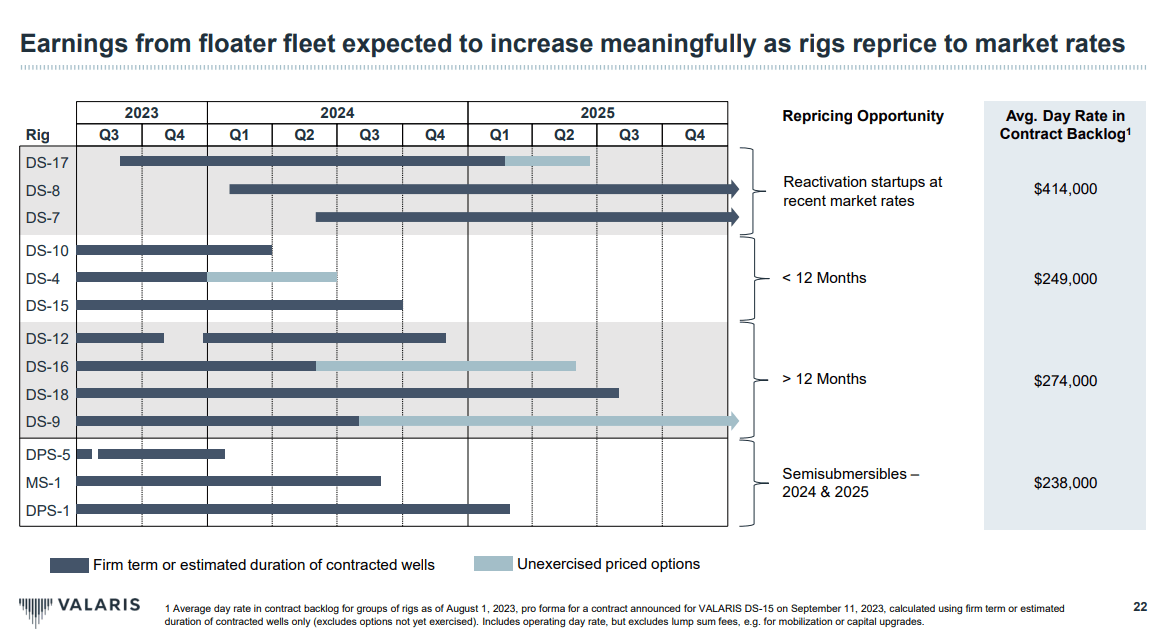

For the second quarter of 2023 , revenue increased only by 0.5%, and operating income remained negative at -$10 million, however, the company sustained positive operating cash flow, totaling $122.6 million for the first half of 2023, compared to a negative $114 million in the first half of 2022. The expectation is that as the company secures contracts at market rates, its earnings should experience substantial growth. The first year where these improvements are expected to be fully realized is in 2025. The company recently posted a comprehensive presentation which a few of the slides been used through this report. See below for timing of contract expirations.

Contract Expirations (Valaris Investor Presentation Sep 2023)

{kind=link}

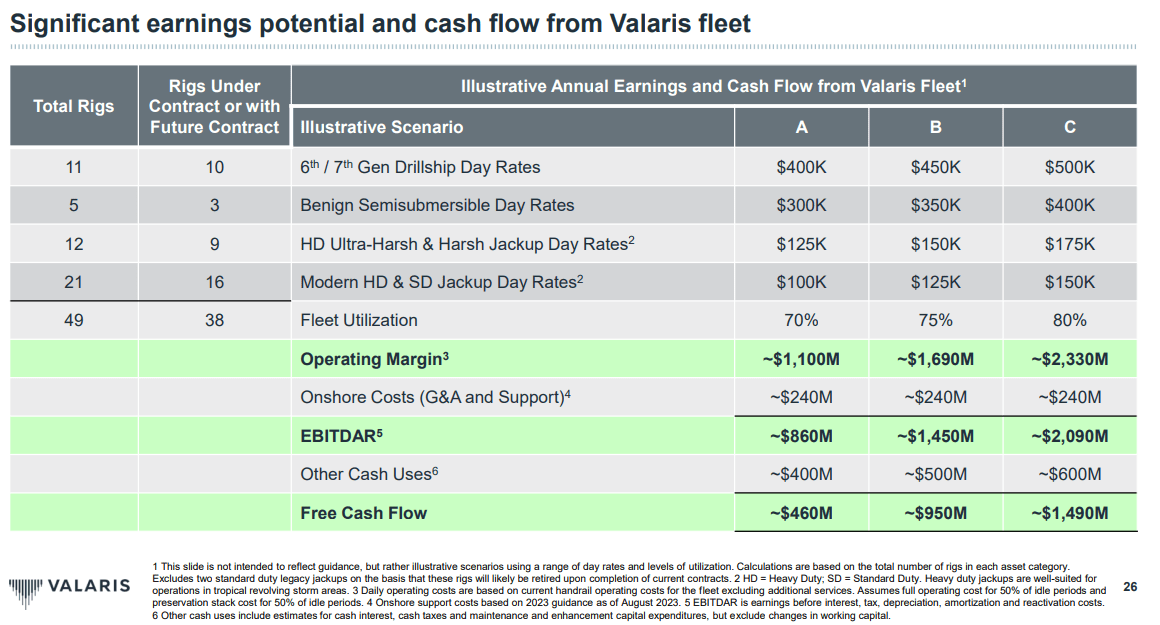

The company's recent presentation has shed light on the potential impact of these developments on earnings and free cash flow. As day rates most likely continues higher the new contracts signed in 2024 could generate results surpassing the threshold represented by the "C column" in the graph below.

Potential Free Cash Flow (Valaris Investor Presentation Sep 2023)

{kind=link}

If the company adheres to the "illustrative" $1.5 billion free cash flow, as emphasized by management in above slide, the company has the theoretical capacity to repurchase approximately 25-30% of the outstanding shares per year. This calculation is based on the current shares outstanding, which stand at 74 million shares, and a share price of $70.

In essence, the company's commitment to returning capital to shareholders through share buybacks, combined with the anticipated improvements in earnings and free cash flow resulting from new contracts and higher day rates, could have a substantial impact on its financial performance and shareholder value in the coming years.

The company has already initiated a smaller buyback program, originally planned for $150 million for the year but later extended to $200 million for 2023. As of now, in 2023, they have already repurchased $94 million worth of shares. This commitment to buybacks reflects the company's intention to return capital to its shareholders and not buy new drillships or jackups.

Additionally, the company has an unconsolidated joint venture with Saudi Aramco called ARO Drilling, in which both entities share a 50/50 ownership. ARO Drilling has been performing well, with 16 rigs currently operating for Saudi Aramco and a substantial contract backlog of $1.5 billion as of the end of the second quarter of 2023. In 2022, ARO Drilling generated $422 million in revenue and had an EBITDA of $99 million. This joint venture, with its high utilization rate and stable cash flow, is expected to contribute positively to the company's stock value.

In terms of the balance sheet, the company maintains a strong financial position with $1.2 billion in cash and $1.08 billion in debt. In August 2023, the company issued an additional $400 million in 2nd lien notes at an interest rate of 8.375%, due in 2030. The proceeds from this issuance will be used to finance the exercise of options for the newbuild drillships, VALARIS DS-13 and VALARIS DS-14. These drillships were acquired at a lower cost compared to current market prices, with a total price of $337 million ($119 million for DS-13 and $218 million for DS-14). Industry experts suggest that the clearing prices for similar drillships are likely to be $300 million or higher.

Furthermore, the company has older drillships like VALARIS DS-10 (used to be called ENSCO DS-10) and VALARIS DS-11 (used to be called Atwood Advantage), which were built a decade ago and had significantly higher construction costs of $625 million and $600 million, respectively. VALARIS DS-11, in particular, was contracted out for $585,000 per day for three years to Noble Energy, starting in the fourth quarter of 2013. The acquisition of VALARIS DS-14, along with VALARIS DS-13 and the uncontracted stacked VALARIS DS-11, presents potential upside to the company's earnings.

Industry Landscape

The oil and gas industry is well-known for its cyclical nature, characterized by significant boom and bust cycles that also affect the rig and drilling segment. The most recent boom occurred following the global financial crisis in 2008/09 and lasted until the summer of 2014. Subsequently, there was a sharp downturn, marking the start of the latest bust cycle, peaking with a remarkable crash in crude oil futures pricing in April 2020.

This last downcycle had a severe and lasting impact on rigs, with many of them being permanently decommissioned, and a substantial number being placed in cold stack status. However, the industry is currently experiencing an upcycle, primarily driven by an increase in oil prices and somewhat higher capital expenditure (capex) spending by major oil companies.

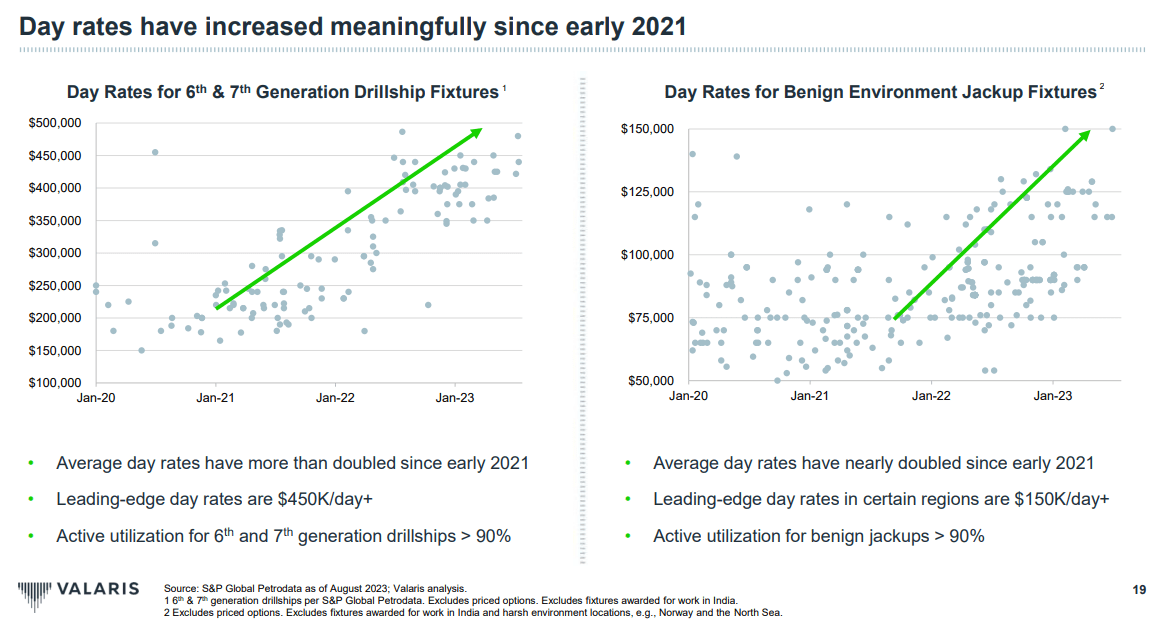

In the offshore rig and drillship segment, there has been a notable resurgence. Day rates have doubled from their lows in 2020/21 to their current levels, standing at approximately $450,000 for drillships and $150,000 for jackup rigs. This upturn reflects a more favorable environment for the industry, with increased demand and pricing power for offshore drilling services.

Day Rates (Valaris Investor Presentation Sep 2023)

{kind=link}

Indeed, the current dynamics in the offshore drilling industry present some unique challenges. The absence of a substantial order book is a notable factor, and the last drillships ordered and constructed are now being delivered at considerably lower prices compared to the cost of ordering and building new ones in the current market. The cost for a new drillship has escalated to over $1 billion, making it a substantial investment.

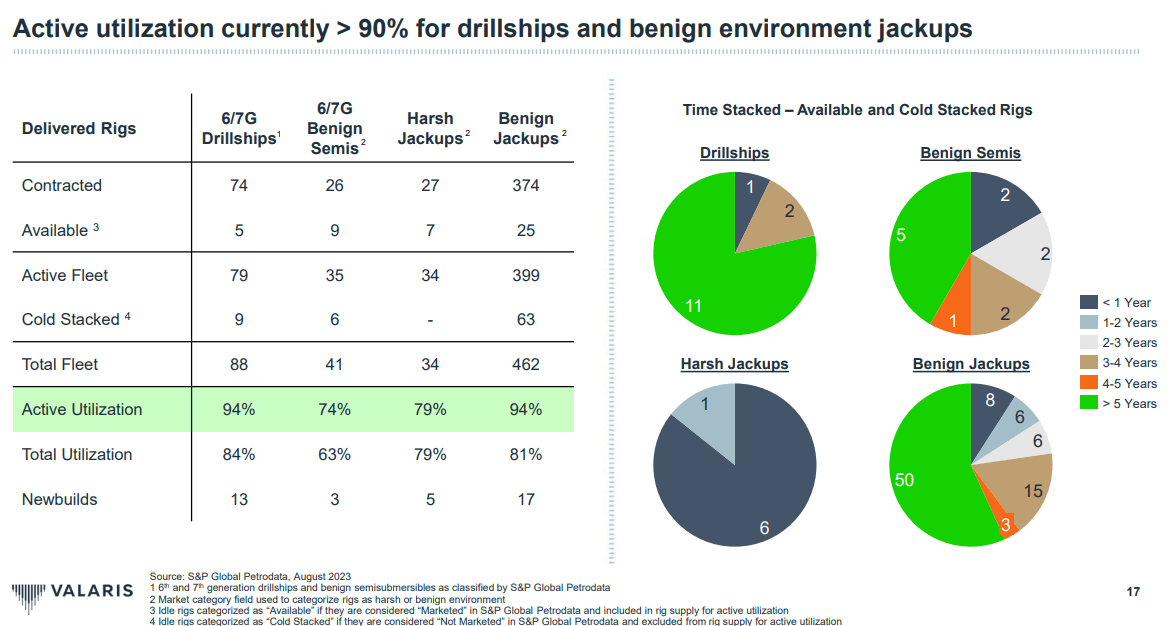

Similarly, for stacked rigs, the high utilization rates, with the majority of rigs now active, mean that there are fewer available for reactivation. This situation can create constraints for companies seeking to expand or renew their drilling fleet, as the supply of new builds is limited, and reactivating stacked rigs may not be a feasible option due to their reduced availability.

Industry Fleet Utilization (Valaris Investor Presentation Sep 2023)

{kind=link}

These market dynamics underscore the cyclical and capital-intensive nature of the offshore drilling industry, where timing and cost considerations play a crucial role in the decision-making process for companies operating in this sector.

The CEO's statement in the Valaris Limited's presentation at the Barclays conference highlights the considerable challenges and high barriers to entry in the offshore drilling industry. To justify the investment in a new drillship, day rates would need to substantially increase to around $900,000, which is approximately double the current rates. This requirement is based on the assumptions of high utilization rates (90%) sustained over a 30-year time horizon to achieve a reasonable return on the investment.

These assumptions underscore the fact that the conditions for launching a new build cycle in the industry appear quite distant. Such a scenario would not only require significantly higher day rates but also a sustained demand for drilling services over an extended period.

Furthermore, the limited shipyard capacity in Korea , which is historically a key hub for shipbuilding in the industry, poses an additional challenge. Even if a company were willing to order a new drillship, the constraints in shipyard capacity would make it extremely difficult to do so.

Overall, these factors collectively contribute to the current complexities and uncertainties facing the offshore drilling sector, emphasizing the cautious approach that companies must take when considering new investments in this

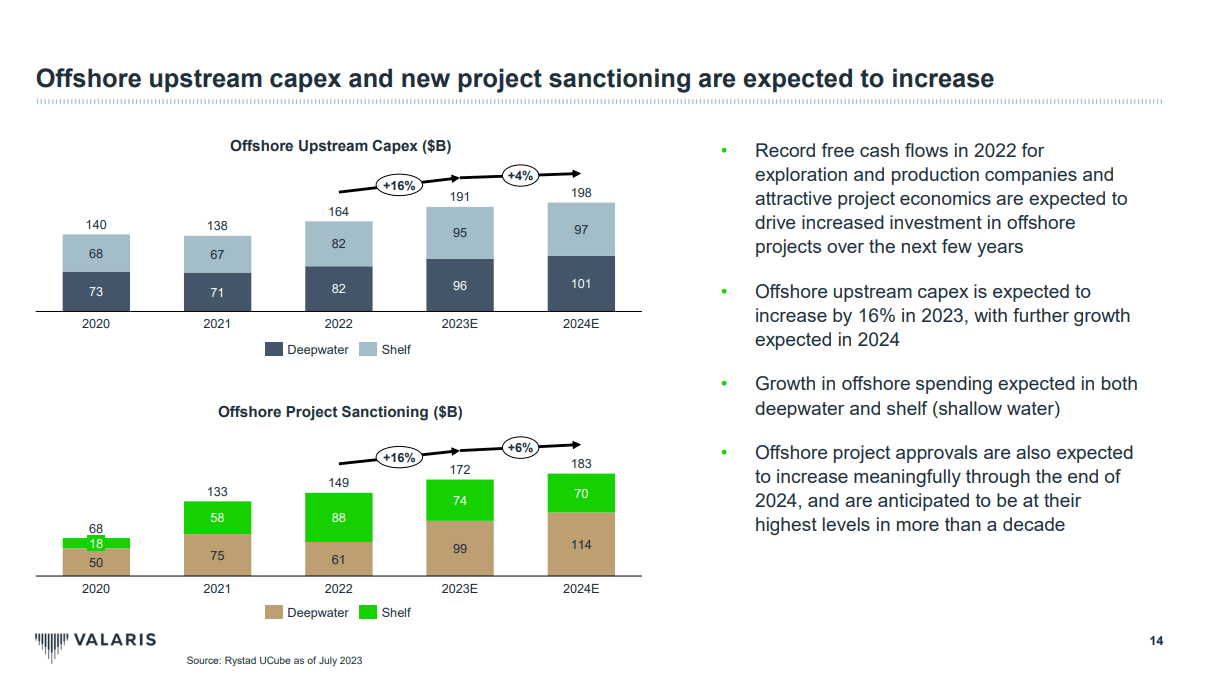

Demand in the offshore drilling industry has shown positive signs, with major oil and gas companies actively exploring and investing in offshore drilling projects. Several recent explorations and discoveries have occurred in offshore regions, such as Namibia, Guyana, Brazil , and the coast of China . These discoveries highlight the ongoing interest and investment in offshore exploration.

These offshore projects are characterized by their substantial scale and long-term nature, requiring massive investments that extend over many years. The exploration and development of offshore reserves often involves complex operations, advanced technology, and significant financial commitments. However, the potential rewards, including access to vast reserves of hydrocarbons, make these investments attractive to major players in the energy industry.

While onshore exploration may have slowed down in some areas, the offshore sector continues to offer opportunities for growth and resource development. As technology advances and companies pursue new discoveries, it is likely that offshore drilling activity will continue to see improvements and expansion, driven by the need to secure future energy resources and meet global energy demands.

Offshore Spend (Valaris Investor Presentation Sep 2023)

{kind=link}

The industry has experienced a prolonged and consistent decline. During this period, many ships and rigs were decommissioned and permanently removed, and companies also merged. For example, Valaris Limited was formed through several mergers, and now owns 51 drillships and jackups. Some of the major companies in the industry, include Transocean LTD ( RIG ) with 38 assets, Shelf Drilling Ltd ( SHLLF ) with 36 assets, Noble Corporation ( NE ) with 32 assets, Borr Drilling Ltd ( BORR ) with 24 assets, Seadrill with 19 assets, and Diamond Offshore Drilling Inc ( DO ) with 12 assets.

According to Rystad Energy, Valaris Limited not only has the largest fleet but also boasts the highest-ranked fleet. They have a stronger financial position compared to a company like Transocean, which never underwent a restructuring and is burdened with over $7 billion in debt, the same amount of debt that Valaris Limited managed to clear through the Chapter 11 process.

Value Proposition

As previously mentioned, the company is poised to experience a significant increase in earnings by 2025. Free cash flow could potentially reach above $1 billion, or perhaps even $1.5 billion. This implies that the stock is currently trading at a multiple of 3.5x to 5.5x of free cash flow. There is minimal risk of significantly increased capital expenditure (capex), and the proceeds from operations will be directed toward share buybacks. Consequently, by the end of 2025, the total number of shares outstanding could decrease to 60 million shares, even if the stock is repurchased at a price of $100 per share.

The use of a double-digit free cash flow multiple is reasonable because these assets can be productive for many years, and a new build cycle seems unlikely in the next 5-10 years. By applying a 10x multiple to the projected 2025 annual free cash flow of $1.5 billion, the enterprise value is $15 billion. With only 60 million shares in circulation, this equates to a stock price of $250.

This calculation assumes that day rates will remain at their current levels, which range from $450k to $500k. However, it's important to consider a potential scenario where day rates approach the new build parity level of $900k. In such a case, the upside potential for Valaris Limited's stock would be substantial.

| Sensitivity Analysis - Share Price with different Free Cash Flow and Multiple |

| FCF in |

| 750 |

| 1000 |

| 1250 |

| 1500 |

| 1750 |

| 2000 |

| Multiple |

| 5 |

| 52.28 |

| 69.18 |

| 86.07 |

| 102.96 |

| 119.85 |

| 136.74 |

| 7.5 |

| 77.62 |

| 102.96 |

| 128.30 |

| 153.64 |

| 178.97 |

| 204.31 |

| 10 |

| 102.96 |

| 136.74 |

| 170.53 |

| 204.31 |

| 238.09 |

| 271.88 |

| 12.5 |

| 128.30 |

| 170.53 |

| 212.76 |

| 254.99 |

| 297.22 |

| 339.45 |

| 15 |

| 153.64 |

| 204.31 |

| 254.99 |

| 305.66 |

| 356.34 |

| 407.01 |

| Shares o/s |

| 74 |

| Net Debt |

| -119 |

| FCF in |

| 750 |

| 1000 |

| 1250 |

| 1500 |

| 1750 |

| 2000 |

| Multiple |

| 5 |

| 64.48 |

| 85.32 |

| 106.15 |

| 126.98 |

| 147.82 |

| 168.65 |

| 7.5 |

| 95.73 |

| 126.98 |

| 158.23 |

| 189.48 |

| 220.73 |

| 251.98 |

| 10 |

| 126.98 |

| 168.65 |

| 210.32 |

| 251.98 |

| 293.65 |

| 335.32 |

| 12.5 |

| 158.23 |

| 210.32 |

| 262.40 |

| 314.48 |

| 366.57 |

| 418.65 |

| 15 |

| 189.48 |

| 251.98 |

| 314.48 |

| 376.98 |

| 439.48 |

| 501.98 |

| Shares o/s |

| 60 |

| Net Debt |

| -119 |

An alternative way to capitalize on this potential upside is by acquiring the warrants due in April 2028, with a strike price of $131.88. If the stock reaches $250 by April 2026, these warrants would be $120 per share "in the money," and investors would still have two years until expiration. Currently, the warrants are trading at around $13 per share and could potentially provide a tenfold return.

Now, let's assess the worth of the company's assets in terms of replacement cost. Most of the drillships were initially constructed for approximately $600 million. However, as mentioned, a new generation drillship would now cost over $1 billion. The two most recently delivered ships are estimated to be worth around $300 million each. Using this rough valuation, the 13 drillships alone would be worth $7 billion, which equates to $95 per share. Alternatively, considering this hypothetical current build cost, the value would be approximately $11.6 billion, or $157 per share.

In addition, the company owns 36 jackup rigs and 5 semi-submersible platform rigs. Recent newbuild prices for jackups approached roughly $175 million , as of 2020. If using a highly conservative comparable value of say $50 million per jackup, these assets would add at least another $1.8 billion in value to the stock, or $24 per share. Doubling this estimate to $100 million per jackup would still represent a significant discount to the actual new build price and provide an add-on value per share of $50.

Finally, when considering the five semi-submersible platform rigs, which cost between $425 million and $500 million each to build, this represents an additional theoretical value of at least $2 billion, or $27 per share. When combined, the estimated replacement cost of these assets' ranges from $175 to $225 per share, with a substantial discount applied to the jackup rigs.

This comprehensive analysis underscores the potential undervaluation of Valaris Limited's shares when compared to the upcoming free cash flow and the replacement cost of its assets.

Risks

The main overarching risk involves the potential decrease in oil demand, combined with specific industry challenges like fewer offshore oil discoveries. There's also a political risk, particularly in regions with unstable leadership, and the overall trend towards higher taxes on offshore drilling due to climate change concerns. This has been especially noticeable outside Norway, leading to increased mobilization costs for Valaris Limited and higher opportunity costs. Furthermore, the risk of a major oil spill, similar to the BP Deepwater Horizon incident in 2010, could severely impact the industry's reputation and its day-to-day operations.

On a company-specific level, there are various risks to consider:

Re-contract Risk: The uncertainty surrounding the renewal or extension of contracts for offshore drilling assets is a significant concern. Changes in market conditions or industry dynamics could impact the ability to secure favorable terms for new contracts.

Damage to Rigs: The risk of damage to drilling rigs, whether due to accidents, adverse weather conditions, or other unforeseen events, can lead to costly repairs, downtime, and potential disruptions in operations.

Counterparty Risk: When breaking longer-term contracts, there is the inherent risk associated with counterparties not fulfilling their obligations. This could result in financial losses and legal complications for the company.

These risks underscore the importance of robust risk management strategies and contingency planning within the offshore drilling industry. Companies in this sector must carefully assess and mitigate these challenges to ensure their long-term sustainability and resilience in a dynamic and potentially volatile market.

Conclusion

We foresee a continuation of the positive trend in day rates for both drillships and jackups due to strong demand and a constrained supply. As we approach 2024, the submarket-priced contracts are set to expire. When the company secures contracts at prevailing market rates, we anticipate a substantial increase in cash flow. This enhanced cash flow position is expected to enable the company to implement a sizable share buyback program in 2025.

Furthermore, we believe that these positive developments will prompt a reassessment or reevaluation of the company's stock price. This perspective is rooted in the belief that improved financial performance, specifically significant free cash flow, and shareholder-oriented initiatives, such as share buybacks, can positively influence the valuation of the company's stock and enhance investor confidence.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!"

For further details see:

Valaris: Uncovering Cash Flow Potential To Buy Back Shares