BORR - Valaris: Upgrading Shares On Improved Financial Flexibility And Strong Buyback Commitment

2023-06-05 06:02:54 ET

Summary

- Last month, Valaris reported better-than-expected Q1/2023 results and reiterated its full-year outlook, with improved profitability expected for the second half.

- The company also released a new fleet status report with a total backlog up by almost 15% sequentially to $2.8 billion.

- Subsequent to quarter-end, the company managed to improve its capital structure thus adding almost $500 million in incremental liquidity.

- After increasing its share repurchase authorization to $300 million, the company intends to spend $150 million for share buybacks until the end of the year.

- With Valaris moving closer to an earnings inflection point, substantially improved financial flexibility, and a resulting strong commitment to share repurchases, I am raising my rating on the stock to "Buy" from "Hold" and would urge investors to initiate or add to existing positions on any sign of weakness.

Note:

Valaris Limited ( VAL ) has been covered by me previously, so investors should view this as an update to my earlier articles on the company.

Last month, leading offshore driller Valaris Limited or "Valaris" reported better-than-expected first quarter 2023 results but on the conference call , management attributed the outperformance mostly to the timing of certain projects with the company's full-year outlook remaining unchanged from the updated guidance provided in March.

In addition, management projected a sequentially weaker Q2.

That said, the company's reported 99% revenue efficiency was impressive.

Moreover, Valaris generated $95.4 million in free cash flow for the quarter thanks to improved margins, positive working capital movements and particularly a $46 million tax refund.

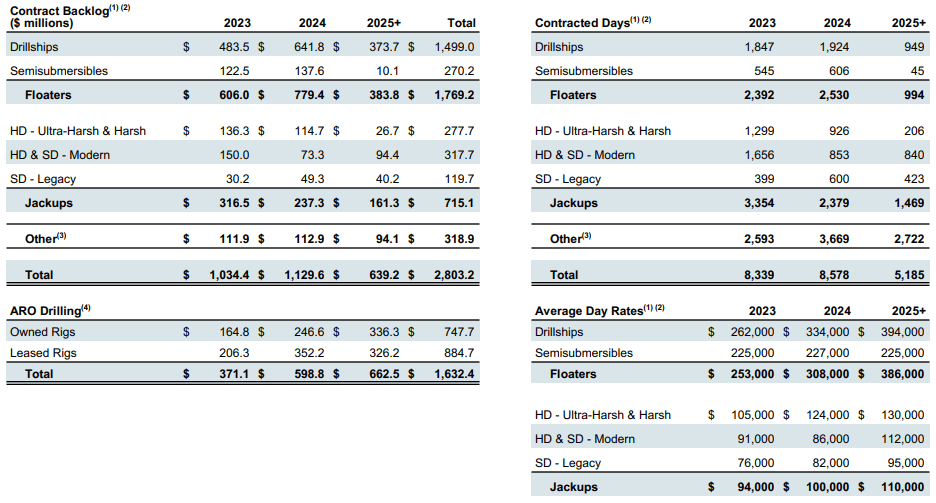

The company also released a new fleet status report with total backlog up by almost 15% sequentially to $2.8 billion. Please note that this number does not include the backlog of ARO Drilling, the company's 50:50 joint venture with Saudi Aramco (ARMCO).

{kind=link}

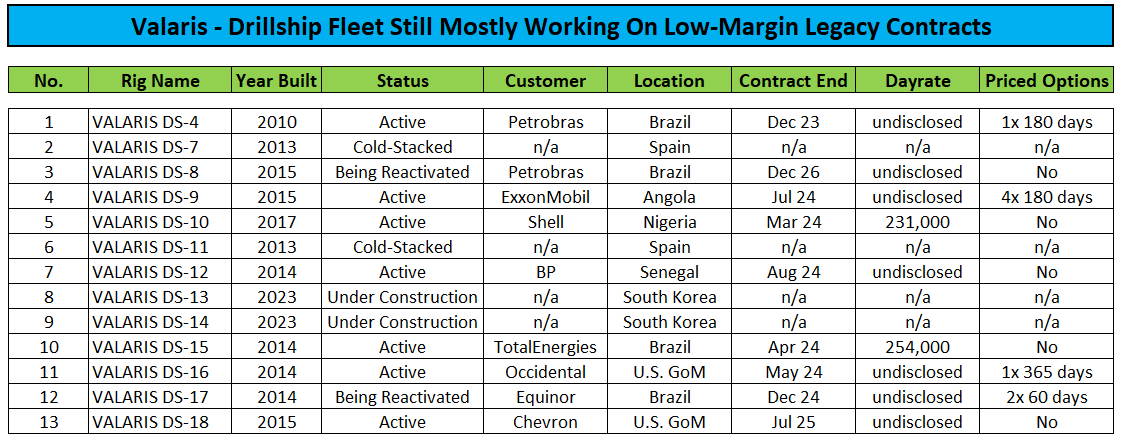

That said, the strong sequential improvement was mostly a result of competitor Transocean's ( RIG ) surprise decision to pull the Deepwater Athena , a cold-stacked 7th generation drillship from a recent Petrobras ( PBR ) tender.

While Transocean's management was allegedly concerned about " the timeline that Petrobras was going to execute upon " and contract economics not meeting the company's internal return requirements, Valaris happily inherited the three-year contract with an estimated value of $500 million. The campaign will be carried out by the currently cold-stacked drillship Valaris DS-8 which will be reactivated over the next couple of quarters with estimated capex requirements of $60 million in 2023.

In contrast to Transocean, Valaris has ample experience in reactivating cold-stacked latest generation drillships and already completed a number of projects on time and on budget.

Subsequent to quarter end, the company managed to improve its capital structure and liquidity substantially through

- The issuance of $700 million in new 8.375% second lien notes in an upsized offering for net proceeds of $685 million.

- Entering into a $375 million senior secured revolving credit agreement which may be increased by an additional $200 million under certain conditions.

- Redemption of the company's onerous $550 million first lien notes.

In total, Valaris added almost $500 million in incremental liquidity while getting rid of the restrictive and expensive first lien notes issued upon the company's emergence from bankruptcy two years ago.

That said, given the requirement to put up a number of rigs as collateral for the new revolving credit facility, I would have expected the company to secure somewhat higher commitments from lenders.

Following these transactions, the Board of Directors ("BoD") increased the company's share repurchase authorization from $100 million to $300 million.

In the earnings press release, CEO Anton Dibowitz stated Valaris' intent " to repurchase $150 million of shares by the end of the year " which apparently has not been sufficient to satisfy long-term investor Lodbrok Capital.

In a recent letter to the BoD, Lodbrok Capital demanded Valaris to take aggressive action including, among other things:

- A separation of the company's jackup and floater fleets

- The immediate return of " any excess cash " to shareholders

Quite frankly, given what happened to the industry over the past decade, Valaris would be well-served to keep liquidity high and leverage low for the time being, particularly considering the likely opportunity to reactivate additional drillships in the quarters ahead and potential exercise of purchase options for two newbuild drillships later this year.

On the conference call, management provided additional color on a potential option exercise:

In addition to our stacked fleet, we have options to take delivery of newbuild drillships, VALARIS DS-13 and DS-14 by year-end 2023. Both drillships are amongst the highest specification assets in the global fleet and both have two BOPs, which remains a preference for customers globally.

The $119 million shipyard price of VALARIS DS-13 is clearly very attractive. And based on our current market outlook, we expect to exercise the option for this rig. The $218 million price for VALARIS DS-14 is more in line with recent market transactions for other similar assets. We will continue to evaluate this against other uses of capital.

Please note that according to statements made by Transocean's management on the company's recent first quarter conference call , activation costs for a newbuild high-specification drillship could reach $150 million while Valaris recently estimated this number to be in a range of $80 million to $100 million.

Given this issue, the company's reluctance to commit to Valaris DS-14 isn't exactly surprising. On the flip side, both newbuilds will be equipped with two BOPs which translates to an incremental value of approximately $50 million.

Given the strong demand for high-specification drillships, I would expect Valaris to ultimately take delivery of both newbuilds with an initial negative impact on liquidity, cash flow and profitability.

With the majority of the company's floater fleet still cold-stacked, under construction or working at painfully low legacy rates and substantial investment requirements for the activation of cold-stacked or newbuild drillships, investors shouldn't expect Valaris to initiate a quarterly dividend in addition to the share repurchase program anytime soon.

{kind=link}

To be perfectly honest, I would like to see the company abstaining from aggressive share buybacks until capital expenditures will be mostly limited to maintenance requirements again.

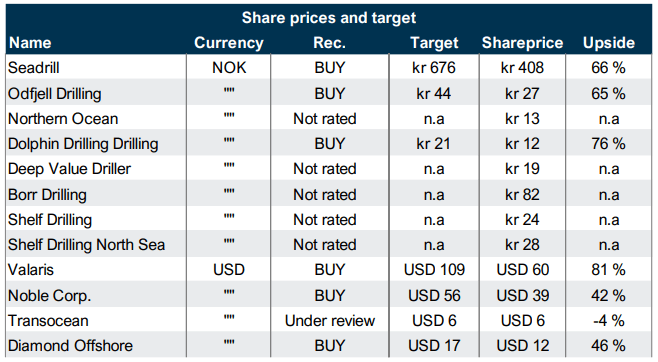

In a recent industry report released by Pareto Securities ("Pareto"), the company stacked up favorably to the majority of its peers based on a number of key metrics. Consequently, Pareto is seeing the highest upside potential for Valaris' shares:

{kind=link}

Bottom Line

Largely due to changes in project timing, Valaris reported better-than-expected first quarter results and reiterated its full-year outlook.

While the company's second quarter results will be nothing to write home about, management expects profitability to improve very substantially in the second half of the year as new contract commencements at higher dayrates start to kick in and activity in the North Sea increases.

True earnings inflection is currently expected for next year as evidenced by the Seeking Alpha analyst consensus:

{kind=link}

Please note that additional rig reactivations and the likely exercise of the purchase options for the newbuild drillships Valaris DS-13 and Valaris DS-14 would result in pressure on near-term cash flows and profitability but improve the company's long-term earnings power substantially.

With Valaris moving closer to an earnings inflection point, substantially improved financial flexibility and a resulting strong commitment to share repurchases, I am raising my rating on the stock to " Buy " from " Hold " and would urge investors to initiate or add to existing positions on any sign of weakness.

At this point, I remain positive on the entire industry, including leading U.S. exchange-listed players Transocean, Seadrill Limited ( SDRL ), Noble Corp. ( NE ), Diamond Offshore Drilling, Inc. ( DO ), Borr Drilling Limited ( BORR ), Helix Energy Solutions Group, Inc. ( HLX ) and offshore drilling support providers like Tidewater Inc. ( TDW ) and SEACOR Marine Holdings Inc. ( SMHI ).

For further details see:

Valaris: Upgrading Shares On Improved Financial Flexibility And Strong Buyback Commitment