NILSY - Vale: Poised To Benefit From Russia's Supply Cut And China Reopening

Summary

- The market for nickel, cobalt, and copper is expected to remain tight for several years as the West avoids the largest Russian producer of these metals, NILSY.

- The reopening of China will have a positive impact on mining companies' stock prices, especially those of emerging market players such as Vale.

- Additionally, the political tensions between China and the West are expected to persist, potentially leading China to purchase more iron ore from Brazil, which would benefit Vale.

- In the short term, Vale, as the most reliant on iron ore in its group, is well-positioned to benefit from the shortage in structural metal supply compared to the rising trend in battery materials production.

- I believe that investors should consider investing in VALE stock at its current price.

Introduction

The last time I wrote about Vale S.A. ( VALE ) was on March 1, 2022. Since then, as you probably know, a lot of interesting events have happened in the world that has somehow influenced my thesis - so after many months of silence, I decided to update my thesis today.

I wanted to share with you how my previous articles on VALE are holding up. Thankfully, my earlier prediction of high dividends and a stable stock price has been holding up well even amidst the changing global scenario. As a result, the VALE stock has not only managed to stay afloat but has also outperformed the S&P 500 Index ( SPX ) in terms of total return performance:

| Change |

| Total return |

| S&P 500 change |

| 1st article |

| -9.72% |

| -5.33% |

| 2nd article |

| -0.97% |

| -7.30% |

| 3rd article |

| 14.18% |

| -7.00% |

| 4th article |

| -2.62% |

| -3.95% |

| Average |

| 0.22% |

| -5.90% |

| Outperformance/underperformance = |

| 6.11% |

Source: Author's selection based on Seeking Alpha

That is, if a hypothetical investor averaged his position after each of my calls, he/she would not lose money and would bypass the broader market.

Today's article will differ slightly in its specifics from my earlier ones. I will look at Vale as a global supplier of base and precious metals - so for a comprehensive analysis, I need to compare the company to some sort of analogs, or peers. I will also try to understand how recent global events affect the company's operations and what its growth prospects are.

Demand-Supply Story

As the famous book Capital Returns - which is basically a collection of investor letters and essays of Marathon Asset Management - says, investors should always focus primarily on supply, not demand, which is always much easier to predict than supply. In my opinion, it's better to look at the big picture to make better predictions.

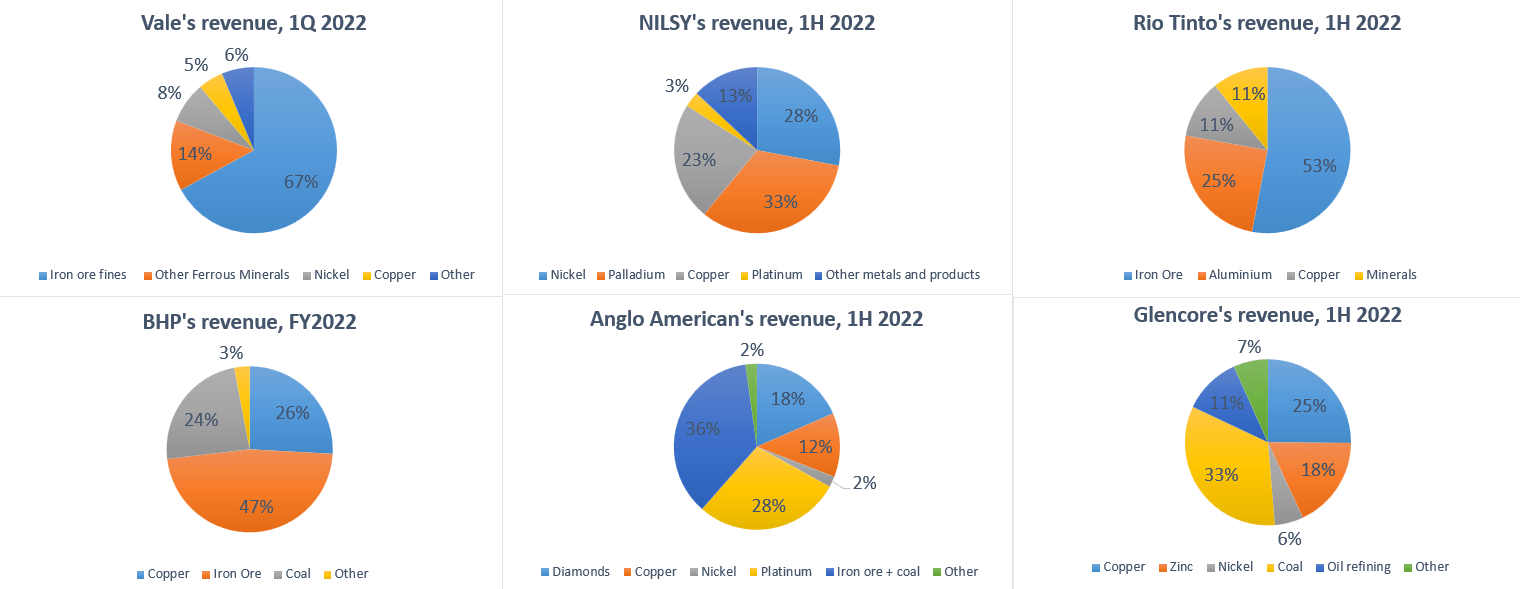

So, Vale S.A. is one of the largest mining companies in the world and is in the top ranks of various top-5 and top-10 ratings depending on what metal is in question. Below I provide a comparison table of the 6 largest mining companies in the world with their relative dependence on the different metals [as of the latest financial data on hands]:

{kind=link}

Note: Norilsk Nickel's ( OTC:NILSY ) market cap is about $31 billion, according to Reuters [USDRUB = 72.5 ]

It would be more correct to put Norilsk Nickel on a par with Sibanye Stillwater ( SBSW ) and Impala Platinum ( OTCQX:IMPUY ) because their operating characteristics are similar - the 3 are pure plays in PGM metals . However, I include NILSY specifically for the demand and supply side discussion.

Norilsk Nickel had very good prospects that were always clear - until the war broke out in Ukraine. Since then, trading in depositary receipts has been suspended, and the sanctions have completely changed the company's focus - management left the West and began to look hard for a market in the East:

Nornickel boss Vladimir Potanin, one of Russia’s richest men, said on Monday that the metals giant was reworking its strategy and building closer ties with countries such as China, Turkey and Morocco because of Western sanctions on the Russian economy.

Source: Mining.com [January 23, 2023]

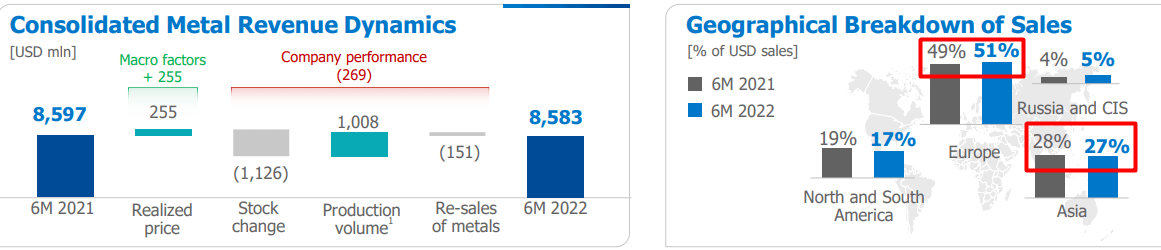

?Norilsk Nickel's H1 2022 results , which show an increase in the European share of the company's revenue, did not reflect this transition - Europeans actively purchased the company's metals in the first 6 months of FY2022:

{kind=link}

The thing is that the news about the transition appeared relatively recently [look at the date of the quote above] - FY2022 and 2H became the real turning point for the company and the whole industry:

{kind=link}

European markets shot themselves in the foot, to say the least, and began to abandon the company's products - NILSY was the largest supplier of the most important and scarce metals in this region.

Against a backdrop of declining shipments to Europe and a lack of logistics capacity to divert the same volume of metal flows to Asia, NILSY management has proposed cutting the annual dividend for FY2022 to $1.5 billion, down from $6.3 billion paid for FY2021.

Investors interested in the industry know that the company has increased CAPEX by 59% year-on-year to $4.3 billion in 2022, while a) over the last 9 years, the average CAPEX has been about $1.7 billion annually and b) in FY2022, most equipment suppliers have left the Russian market. How then did NILSY manage to complete its investment program in FY2022 and will these investments lead to an increase in production in the nickel and copper market in the coming years?

The company's most recent financial reports show that the value of construction in progress at the end of 2022 increased 1.5 times to $7.8 billion. This amount includes advances to suppliers and contractors. So the "huge paper CAPEX" most likely will not lead to an increase in production in the foreseeable future.

In addition, management itself is forecasting a decline in production for all metals to 12-14% in FY2023. Therefore, I expect rather meager supply growth in the copper and nickel markets this and maybe next year.

Mr. Potanin is a man who has been subjected to rather harsh sanctions by the West. Certainly, this poses a significant risk to the company. Norilsk Nickel is a closed company, and its reports do not give clear information about the possible consequences. Only in the fall will the true impact of the sanctions become clear. Norilsk Nickel is taking significant risks if Potanin, the major shareholder, remains at the helm of the company.

So I think it is obvious that a company with such leadership will be shunned in the future under the current conditions. Stocks of Russian metals in LME warehouses are increasing, with some consumers shunning Russian copper and nickel [by Norilsk Nickel], the Financial Times reports. I do not doubt that Western companies would still buy Norilsk Nickel's products - the presence of top management on sanctions lists cast too much shadow, negatively impacting this major global PGM player.

This paints an interesting picture: first, NILSY's CAPEX growth looks nominal, and therefore nickel and copper market supply could be even lower than everyone now expects; second, the demand side itself does not want to deal with Mr. Potanin - everyone wants to minimize their risks. So the other global players have received a double tailwind in 2022, which will probably continue for more than a year.

When there is a production cut in one part of the world, the other part - the most adapted one - tries to compensate for the loss. This is especially true in markets that are growing as fast as the battery metals market . NILSY was to be replaced by Impala Platinum and Sibanye, whose operations are mostly in South Africa. But this region is affected by another force - the energy crisis.

South Africans have endured power cuts for years, but 2022 saw more than twice as many blackouts as any other year, as aging coal-fired power plants broke down and state-owned power utility Eskom struggled to find the money to buy diesel for emergency generators.

The intermittent power supply is hobbling small businesses and jeopardizing economic growth and jobs in a country where the unemployment rate already stands at 33%.

South Africa's GDP growth is likely to more than halve this year to 1.2%, the International Monetary Fund has forecast, citing power shortages alongside weaker external demand and "structural constraints."

Source: CNN Business [February 10, 2023]

The excessively high unemployment in this region, as well as the physical inability to keep mines operating when there are constant interruptions in the energy supply, significantly increase the risks of investing in Sibanye and Impala, in my view. Norilsk Nickel could - if it were not for the sanctions against its management - replace part of the SA's volume decline in the global market for PGM metals, but alas.

So the ball in the demand game is now in the hands of Vale, Glencore ( OTCPK:GLCNF ), Rio Tinto ( RIO ), and BHP Group ( BHP ). All except Glencore are primarily iron ore producers - and since iron ore is primarily consumed in China [recall the zero-Covid policy], I've been leaning more towards Glencore lately.

{kind=link}

Now the situation has changed - China's reopening has caused iron ore prices to rise 60% since November, and the USD has also weakened 10% since then. It would seem that Vale should have outgrown other peers from the developed market because a) its total revenues are 81% dependent on ferrous metals [way more than others] and b) a weak dollar helps the company. However, the outperformance did not materialize:

VALE's divergence of 10-11% from RIO and BHP looks too impressive. Moreover, Vale has a significant advantage over these companies - a much friendlier relationship with China.

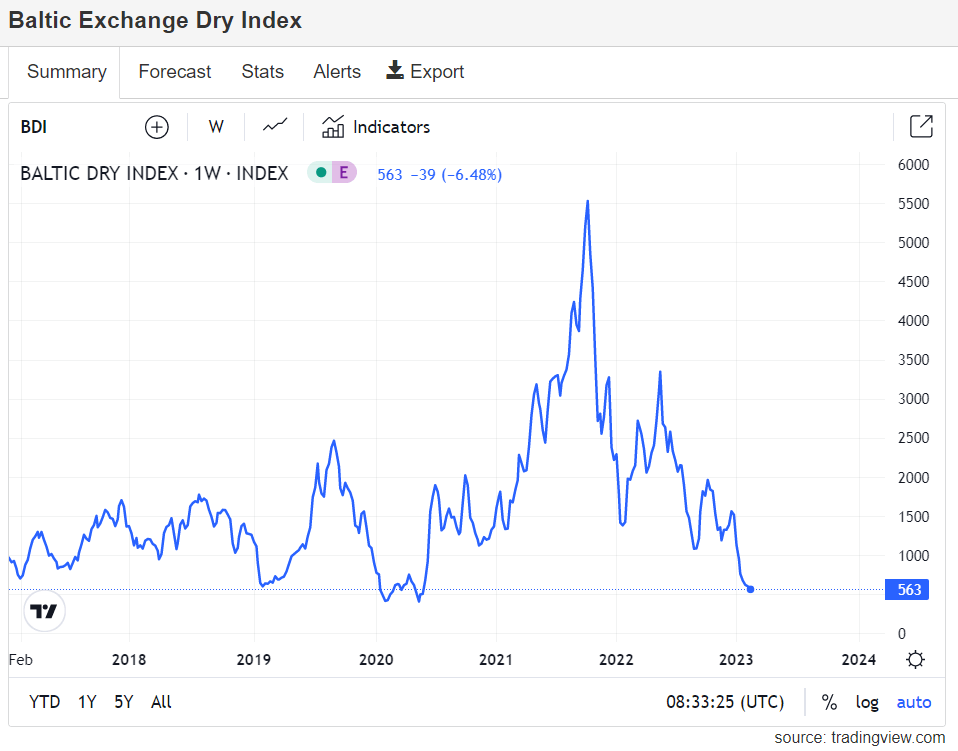

I have exposed this side of the thesis before, but now - after the invasion of unidentified flying objects on both sides of the Atlantic - it seems even more appropriate. I expect that China will be much more willing to buy iron ore from Brazil in the coming years - something that was not possible before , but now that the Baltic Dry Index is cooling off , it seems much more possible.

{kind=link}

The current situation paints an asymmetrically more positive picture for Vale and the Brazilian market as a whole - analysts at JPMorgan (JPM) agree with this view, pointing to a possible additional catalyst from the Brazilian government that could attract more investors to the region:

[surging iron ore prices and weaker dollar] are incontestably favorable to a Brazil rally. Add to this the fact that multiples are among the cheapest within EM, no matter how one decides to look at it. Performance could be unleashed if the new government unveils a fiscal rule that is credible and feasible (April). This is at least what foreign investors have been banking on, considering that they have poured USD 2.5 bil in Brazil in January, on top of more than USD20 bil in 2022.

Source: JP Morgan's Global Markets Strategy report [February 13, 2023 - proprietary source]

In addition, although the iron ore market with its long-term projected market growth of 4.51% lags ~2 times behind the projected growth of the battery metals market, in the shorter term [1H 2023], structural metals will dominate the relative performance, according to analysts at Goldman Sachs [proprietary source]:

Over the next quarter, whilst we see a progressively more constructive fundamental path on structural metals (aluminium, copper, iron ore, zinc), we also hold a bearish view on battery raw materials (cobalt, lithium, nickel). This differentiation reflects the relative supply conditions of the two subsets, with divergent capex cycles since the mid-2010s now generating stagnation in structural metal supply compared to surging battery material production trends.

Source: Goldman Sachs [February 9, 2023]

Thus, I draw the following intermediate conclusions:

- The market for nickel, cobalt, and copper will be extremely tight for the foreseeable future as the West avoids the largest Russian producer of these metals - supply will remain limited for many years to come;

- The reopening of China, which has already greatly boosted the rise in iron ore prices, will continue to have a positive impact on mining companies' stock prices - against the backdrop of a weaker USD, emerging market players, among which Vale is the largest and most obvious, should benefit the most;

- Political tensions between China and the West, which only began to grow because of the mystical appearance of flying objects, are likely to continue - China will continue to try to buy more iron ore from Brazil, and cheaper transportation costs will help it;

- Vale is the most dependent on iron ore within its group. In the short term, this should play into the company's hands due to the aforementioned stagnation in structural metal supply compared to rising production trends in battery materials.

In other words, Vale appears to be very well positioned today, both for continued growth in the future [expanding battery metal production] and to take advantage of the processes here and now [China's iron ore needs].

To complete the picture, let's take a look at the comparative valuation of the company.

Valuation

With a dividend yield of ~8.75% and second only to Rio Tinto, Vale trades at an EV/EBITDA of just 4.167x (fwd) - 4% below its peers' average multiple if one includes the clear outlier Glencore:

Note: Glencore trades at 2.96x forwarding EV/EBITDA.

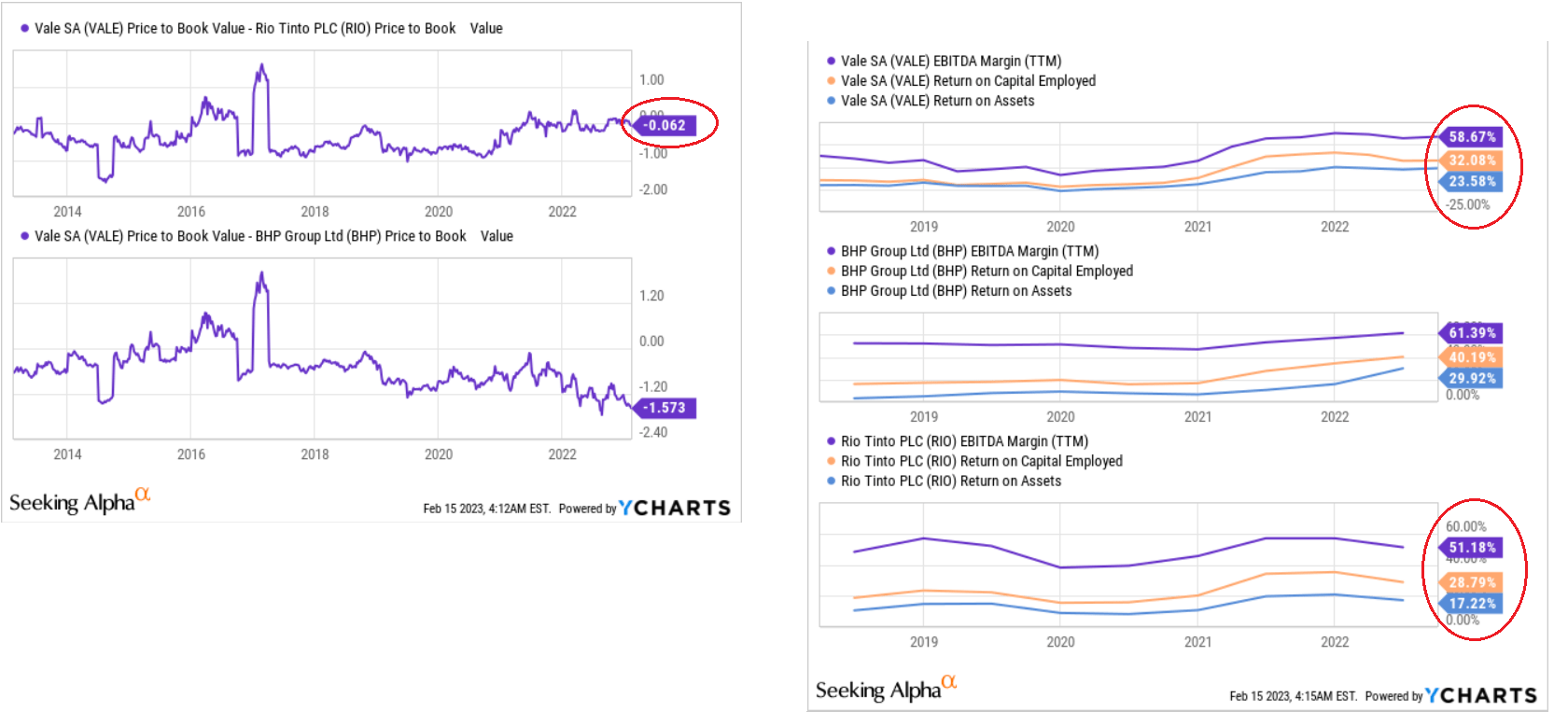

At the same time, the stock is trading slightly cheaper with a price-to-book ratio compared to RIO. In terms of the most important financial metrics - EBITDA margin, ROCE, and ROA - the VALE stock easily outperforms its competitor [RIO]. This fact, in my opinion, also indicates the existing undervaluation of the Brazilian giant:

{kind=link}

However, this undervaluation can be explained by existing risks that must also be taken into account.

Risks To Consider

Investing in Vale S.A. stock carries several risks that potential investors should consider. One of the most significant risks is the potential impact of a weakening global economy on demand for Vale's products. Vale is highly dependent on demand from China, which is a major consumer of iron ore and other base metals. If the Chinese economy were to slow significantly, this could lead to a decline in demand for Vale's products and a decline in the company's share price.

Another risk to Vale is the fierce competition it faces from other mining companies. Chinese companies have recently turned to Russian mining companies, sucking up their "resources not needed elsewhere ," reducing demand for Brazilian metals.

Geopolitical issues in Brazil also pose a significant risk to Vale. Brazil is prone to political instability and social unrest that can disrupt the company's operations and supply chains. In addition, Vale operates several mines located in environmentally sensitive areas, which can lead to regulatory scrutiny and fines if the company violates environmental regulations.

In recent years, Vale has faced some high-profile disasters that have damaged the company's reputation and caused significant financial losses. In 2015 , for example, a dam burst at one of Vale's mines in Brazil, causing a massive environmental disaster and killing 19 people. In 2019 , another dam broke at another Vale mine in Brazil, killing more than 270 people and causing significant environmental damage. These disasters have led to increased regulatory scrutiny of Vale's operations and damaged the company's reputation among investors.

Finally, Vale's stock price is highly dependent on the price of iron ore, which can be volatile and subject to rapid fluctuations. The price of iron ore is influenced by several factors, including supply and demand, global economic conditions, and geopolitical risks. A decline in the iron ore price could have a material adverse effect on Vale's share price, particularly if the decline continues for an extended period.

Summary Thesis

In spite of the aforementioned risks, I believe that investors should consider investing in Vale's stock due to several factors. The market for nickel, cobalt, and copper is anticipated to continue experiencing tightness for several years, as global production is expected to remain limited due to the cut in supply from the largest Russian producer, NILSY. The reopening of China will have a positive impact on mining companies' stock prices, especially those of emerging market players such as Vale. Additionally, the political tensions between China and the West are expected to persist, potentially leading China to purchase more iron ore from Brazil, which would benefit Vale. In the short term, Vale, as the most reliant on iron ore in its group, is well-positioned to benefit from the shortage in structural metal supply compared to the rising trend in battery materials production.

For further details see:

Vale: Poised To Benefit From Russia's Supply Cut And China Reopening