VLN - Valens: Don't Miss Out The New Potential Semiconductor Star

2023-09-28 03:32:48 ET

Summary

- Valens Semiconductor stock has experienced a significant decline this year due to weak second-half-of-the-year guidance, but the pessimism is already priced in.

- The company is committed to innovation and has a strong customer base, indicating the quality of its products.

- VLN is on track to achieve free cash flow profitability next year, and the valuation is ridiculously cheap.

Investment thesis

Valens Semiconductor's ( VLN ) stock is suffering tough times this year since the stock price almost halved year-to-date. The massive pessimism was caused by the weak second half of 2023 guidance due to the harsh macro environment, which weighs on the company's revenue growth. However I consider these headwinds temporary and not secular, and my valuation analysis suggests that massive pessimism is already priced in the current market cap. I like the company's firm commitment to innovation, and its customer list suggests that it provides superior-quality products. The company is on its path to achieving free cash flow profitability next year, which is also a solid bullish sign. All in all, I assign the stock a "Strong buy" rating.

Company information

Valens provides semiconductor products targeted for various applications like high-speed video and data distribution for the automotive and audio-video industries. The company is domiciled in Israel.

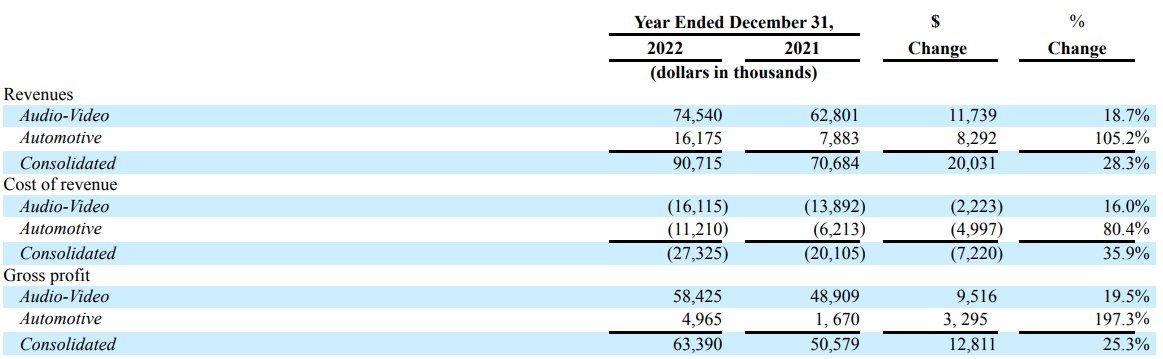

The company's fiscal year ends on December 31. Valens operates its business in two segments: Audio-video and Automotive. According to the latest annual SEC filing , the company's Audio-video segment is by far larger and more profitable.

VLN's latest annual SEC filing

{kind=link}

Financials

Valens Semiconductor went public via the SPAC merger in 2021, so we have a short track record of financial performance. Over the last four years, the company's revenue compounded at almost 15% CAGR, which is impressive. The operating margin has a positive trend, which improved by 15 percentage points but is still in the negative zone. The levered free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] has been consistently negative in the last four years.

Author's calculations

VLN invests heavily in innovation, which is a solid long-term bullish sign to me. The R&D to revenue ratio has shrank notably as the business scaled up, but VLN still allocates more than half of its sales to invest in R&D.

Consistently negative FCF does not look like a big problem early in the company's lifecycle. The aggressive capital allocation to innovate looks sound to me since the company needs to sustain its revenue growth momentum and expand its revenue streams. Moreover, it is crucial to underline that VLN had a massive net cash position of above $130 million as of the latest reporting date. To add context, the company's burn rate was $25 million in the latest full fiscal year. The company has enough financial resources to fund its operations for the next five years. Leverage is almost zero, and liquidity metrics are in excellent shape.

Seeking Alpha

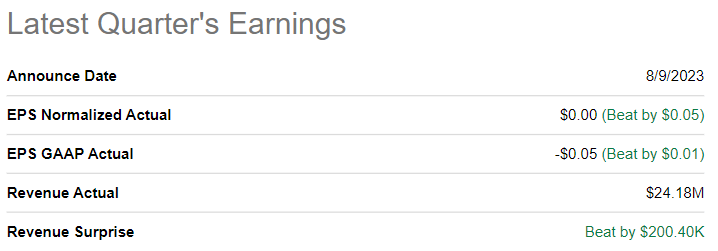

The latest quarterly earnings were released on August 9, when the company topped consensus estimates. Revenue demonstrated a solid 7.5% YoY growth, and the EPS improved notably from -$0.10 to -$0.05. It is crucial to mention that the non-GAAP EPS has achieved its breakeven in the latest quarter. The operating margin has improved substantially, from -35% to -21%, which is a bullish sign to me.

{kind=link}

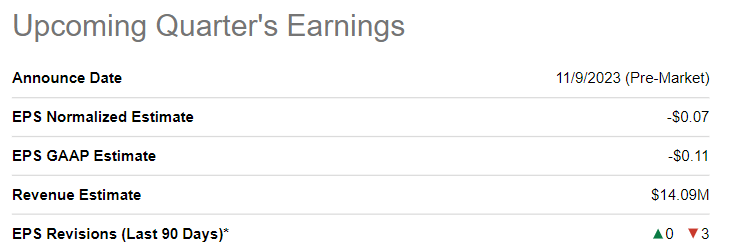

The upcoming quarter's earnings are scheduled for release on November 9. Consensus estimates forecast quarterly revenue at $14 million, which is a huge YoY drop of 42%. The adjusted EPS is expected to return to the negative zone.

{kind=link}

The management expects the harsh macro environment to substantially weigh on the revenue growth till the end of this year. It is a bad sign for investors, but these fears are already priced into the current market cap. It is also important to underline that these challenges are temporary due to the weak macro environment. It does not mention the company's fundamental weakness, apart from the lack of diversification of revenue stream. However, the company is young, and its strong commitment to innovation suggests that VLN is highly likely to be able to expand its portfolio of offerings to be less vulnerable to economic cycles. From the secular perspective, the company is well-positioned to demonstrate impressive revenue growth, and I like the management's target to become cash flow profitable in 2024.

The company's audio-video segment powers millions of products produced by global consumer electronic leaders like Samsung, Sony, and many other strong brand names. Having all these legendary OEMs as the company's clients means VLN indeed provides superior quality and technologies compared to its competitors.

VLN's latest earnings call presentation

{kind=link}

The company's aim to penetrate the automotive industry also looks promising. Modern vehicle architecture requires cutting-edge technologies, including multiple cameras for safer driving, driver cameras to detect the driver's attention, multiple radars, and LiDARs for "autopilots," which require reliable, high-quality connectivity solutions. According to the latest earnings presentation , Valen's automotive offering is the only high-speed connectivity solution supporting multi-gigabit connectivity over unshielded harnesses. It is crucial to mention that the iconic Mercedes-Benz car manufacturer is one of the company's automotive segment's clients. Being one of the suppliers of Mercedes-Benz is a huge quality sign to me.

VLN's latest earnings presentation

Valuation

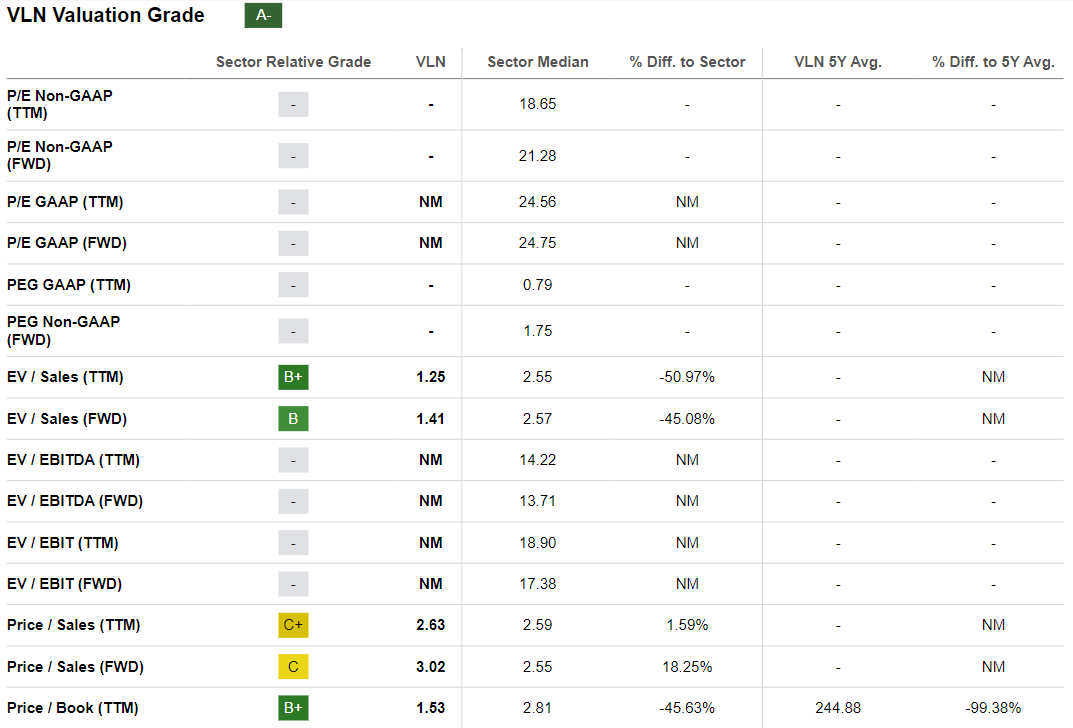

The stock price declined 43% year-to-date, significantly underperforming the broader U.S. market. Seeking Alpha Quant assigns the stock a decent "A-" valuation grade, mainly thanks to substantially lower EV-to-sales ratios than the sector median. Price-to-sales ratios are approximately in line with peers. Multiples suggest that the stock is attractively valued.

{kind=link}

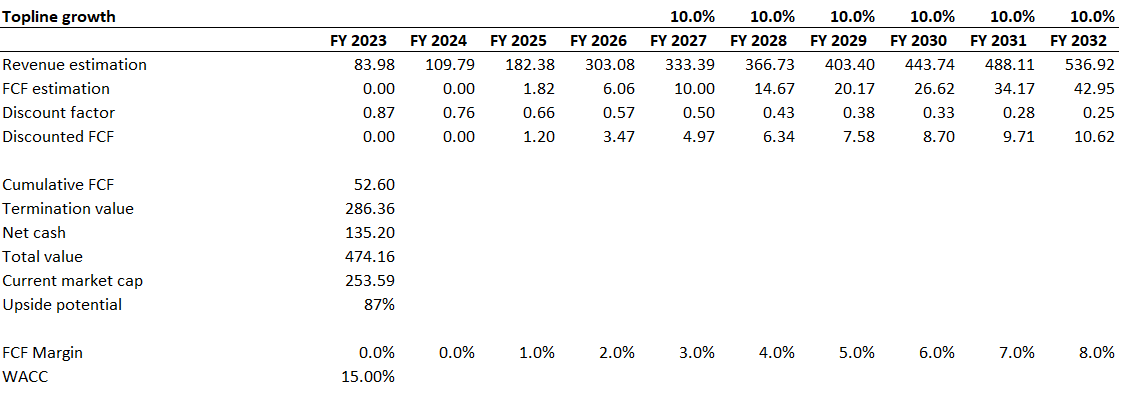

To get more evidence regarding the fairness of VLN's valuation, I want to simulate the discounted cash flow [DCF] model. Due to the vast uncertainty of the FCF breakeven and revenue growth rate, I use an elevated 15% WACC for discounting. I expect the FCF margin to be zero in 2023-2024 with a further yearly one percentage point expansion. Consensus revenue estimates are available up to FY2026, projecting revenue to increase by almost four times in the upcoming four years. For the years beyond, I project a more moderate 10% revenue CAGR.

{kind=link}

According to my DCF simulation, the stock is massively undervalued. Considering the company's substantial net cash position, the business's fair value is approximately $474 million, which indicates a massive 87% upside potential. That said, the stock's fair price is approximately $4.7.

Risks to consider

Valens Semiconductor is a small-cap aggressive growth company, and its valuation significantly depends on several assumptions with a very high level of uncertainty regarding the reliability of these assumptions. While my valuation assumptions are very conservative, there is still a substantial risk that the company might fail to deliver the projected growth trajectory. Any hints of the company's revenue growth decelerating faster than expected will lead to massive investor disappointment. Investors might start selling off the stock in case of disappointing earnings or guidance downgrades, which will drive the stock price down. Investors should realize that investing in companies like VLN is highly risky and that risks are comparable to the massive upside potential.

The company is vulnerable to changes in economic cycles, meaning that weakness in the broader environment is likely to undermine the company's financial performance. The current macro environment is harsh, and there is little uncertainty regarding how long it will last. Interest rates in the developed world are at their highest in several decades, which weighs on the global economy. Geopolitical tensions in different parts of the world do not add optimism to the near-term global economic outlook. While the company has enough resources to weather the storm, its plans to achieve profitability targets might be delayed due to unfavorable external factors.

Bottom line

To conclude, VLN is a "Strong buy". Yes, the company is poised to suffer a challenging second half of this year, but its balance sheet is stronger than enough to weather this temporary storm. It is crucial that the vast pessimism is already priced in since the stock has a massive upside potential to almost double in price. The company continues to innovate rapidly, and its rich, iconic customer portfolio suggests that VLN's innovations are indeed very effective.

For further details see:

Valens: Don't Miss Out The New Potential Semiconductor Star