VLEEF - Valeo: A Good Investment For The EV/ADAC Upside

2023-12-21 07:30:00 ET

Summary

- Valeo is a French automotive supply and tech company positioned to benefit from the growth in EV, electrification, and ADAS.

- The company has restored profitability, generated free cash flow, and has a balanced sales split across different business areas.

- Despite some downsides, Valeo has the potential for significant earnings growth and is currently undervalued, making it a solid investment choice.

Dear readers/followers,

In this article, I'll show you why I believe that Valeo (VLEEY) (VLEEF), a French company in automotive technologies and EV as well as ADAS, will be a solid investment for both the short term and, more importantly for the long term. This investment that I am starting here is based on the stance that we're at the start of a period of transformation in the mobility sector, with significant growth in EV, electrification, and ADAS.

I'm not against investments in EVs and this type of automotive. In fact, I own several of the leading manufacturers - just not Tesla (TSLA) or any of the Chinese companies in this sector either.

My choice is instead to bet on the legacy players, both in straight automotive manufacturing, but also in parts and ancillary products.

That's where Valeo comes in, and it's what Valeo does.

These are trends and markets that are set to grow explosively over the next few years and decade, up to the year 2025. I believe firmly that Valeo will be one of the leaders in Europe and potentially in the world for these trends.

In this article, I will make clear to you what the reason is for believing this.

Valeo - Solid automotive upside from a leader in electrification and ADAS.

Valeo is a bet on the following two trends.

{kind=link}

You may not have heard of, or really be aware of this company or what it does. So let me present to you exactly what Valeo does, and how good it is compared to other companies in the same sector.

Valeo is French, it's an automotive supply and tech company that manages revenues of over €22B on an annual basis, and over the past decade and more has been on a transformative journey that is nearing its end.

However, the company has not been rewarded for this. If anything, over the past year, it has been punished, despite a growing profit margin and profit amount.

These sorts of trends always interest me, because they actually tend to be "wrong" in my experience.

Valeo is in a factually good position. I mean that the company has restored profitability, generated plenty of free cash flow, and has deleveraged to a significant degree where debt is no longer as much a concern as it once was.

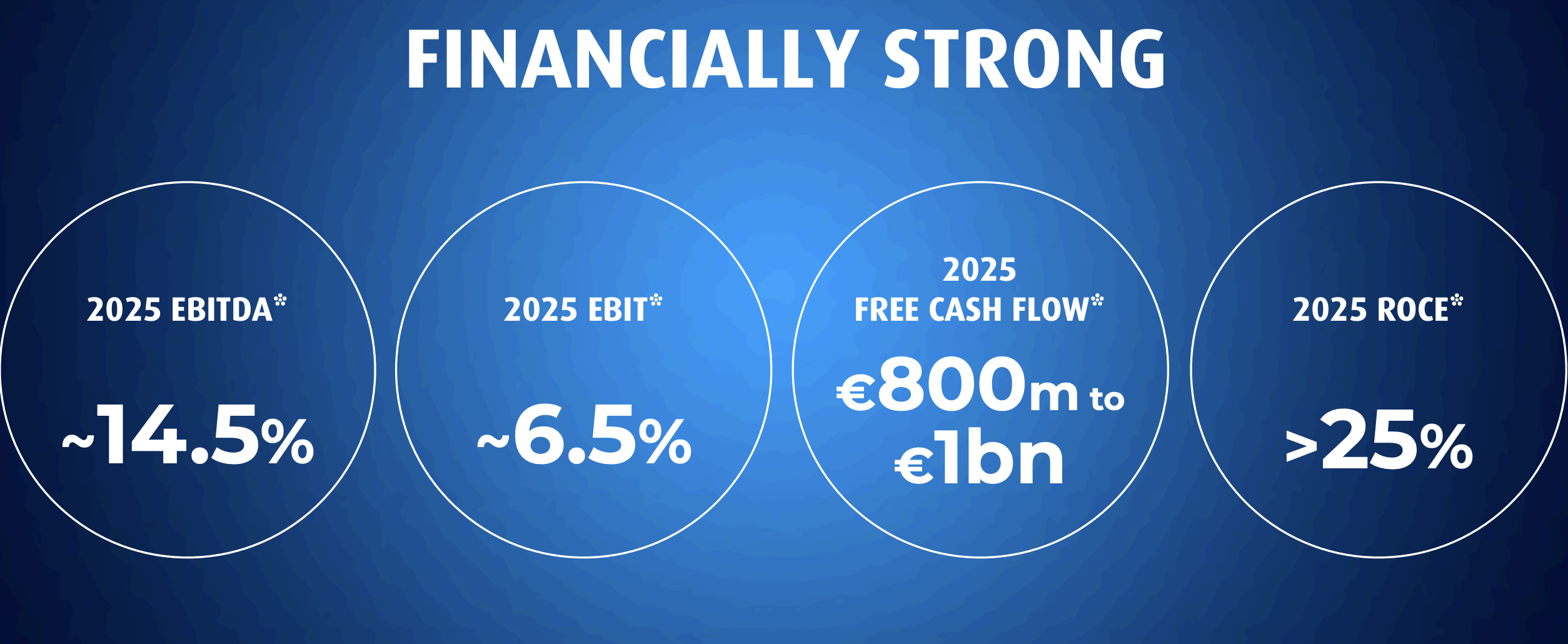

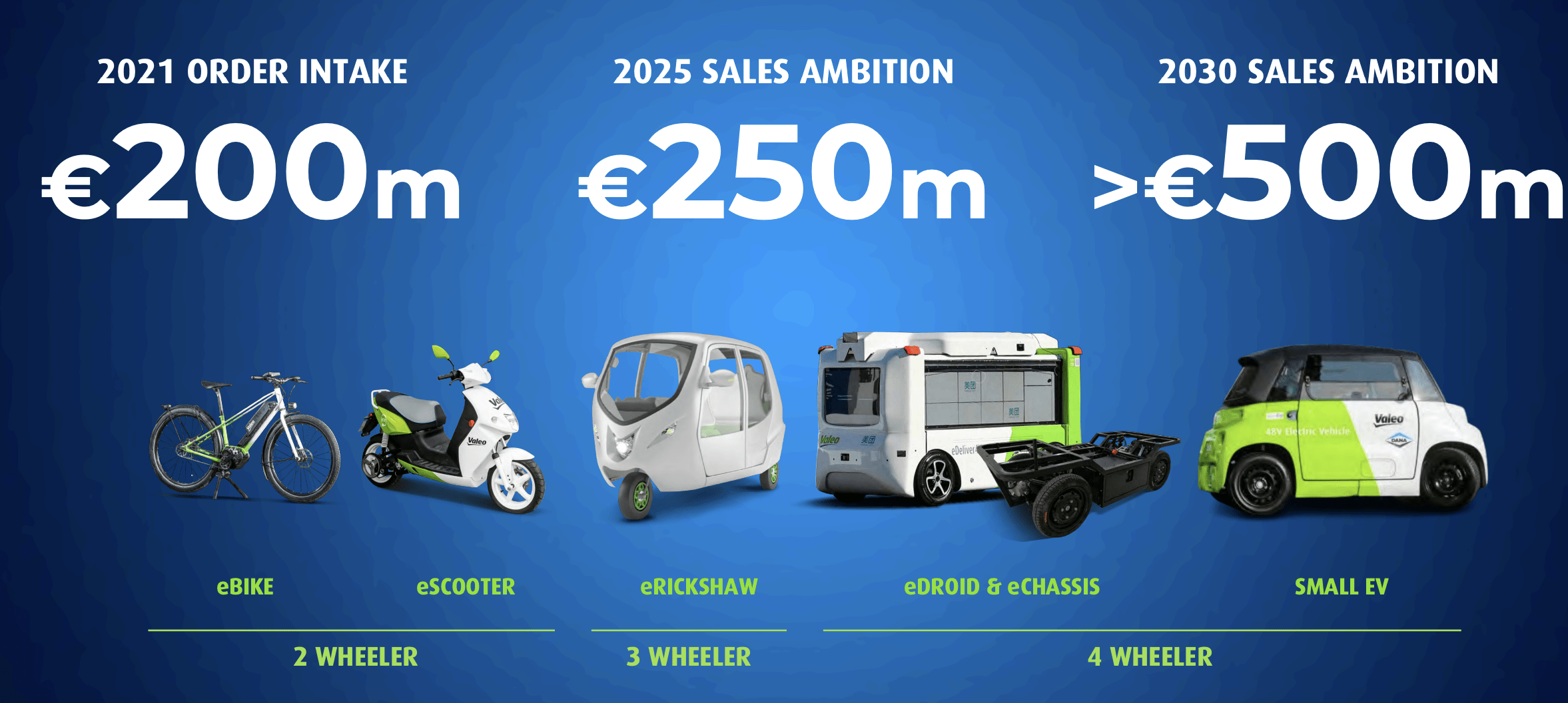

The company's targets for 2025E are as follows.

{kind=link}

And this is not as unlikely as it might sound to some. The company very recently during 9M23 reaffirmed not only the sales guidance but the EBIT and EBITDA margin guidance, as well as the FCF forecast for the year. Sales are expected to come in €3B above 2022, with a double-digit margin on the EBITDA side, and 3-4% on the operating side.

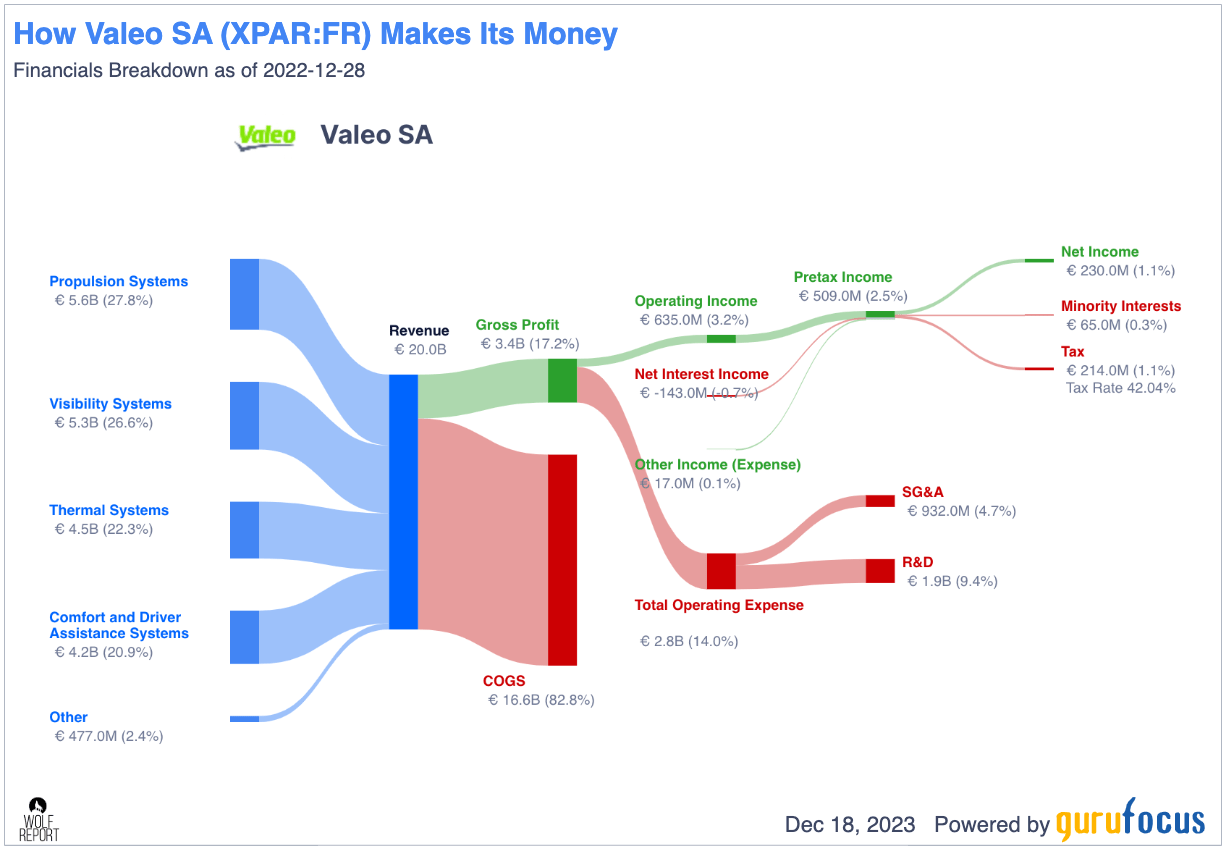

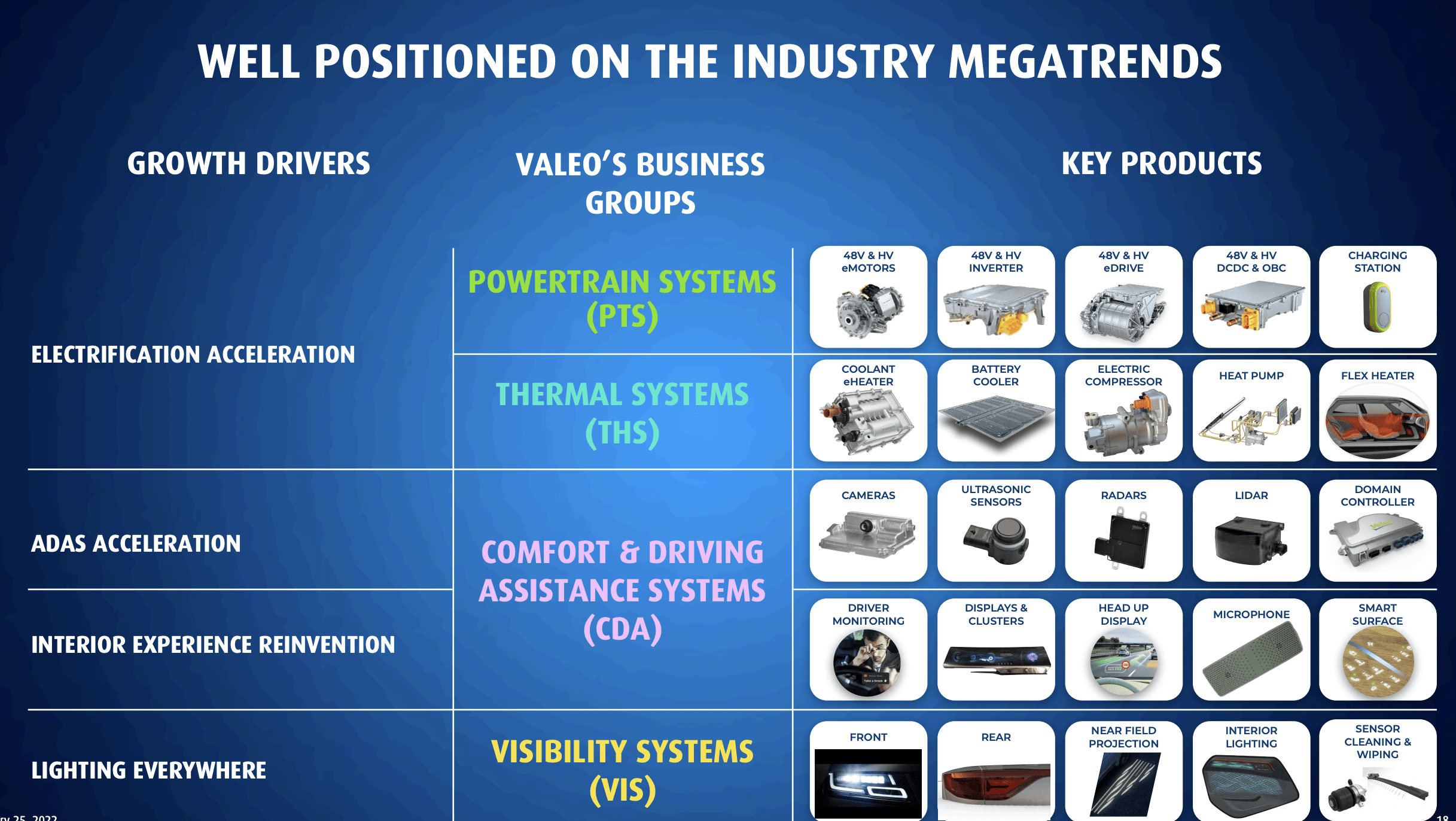

The company is a mix of business areas - and it's market-leading in several of them. Valeo develops and sells propulsion, visibility, thermal, and Comfort/Assistance systems.

They do this at a very impressive sales split - no segment has more than 30% or less than 20% of 2022 sales, which means the company is very balanced. Criticism levied at the business model has strictly to do with COGS - 82.8% is too high, and this is what the company has been addressing this year and in the coming few years.

{kind=link}

Valeo has interesting partnerships with Mobileye in the ADAS segment, and while some of the sectors have volatility in the recent trends for 3Q23, the overall picture for the company is a continuation of the strategic targets and upsides. We're talking confirmation of divestment, we're talking successful inflation negotiations set to be completed in 4Q23, and we're talking a very impressive overall earnings trend for the year.

All the positive things I am saying, I want to be clear that there are some downsides to this business.

First, the yield isn't all that great. 2.7% is below the risk-free rate, and I don't see that dividend massively increasing in the near term despite what is being said from forecasts here.

The company also comes in at BB+ . It's junk-rated, even if barely. I do not view this rating to be all that valid any longer at a sub-46% long-term debt to capital, but I understand the necessity of a company "proving" itself here.

Valeo simply has a very poor track record of stability, but at the same time has a very impressive time tracing its long-term 13-15x P/E.

{kind=link}

As you can see, the company has gone up and down like a JoJo several times. It has the real potential of trading above €60/share, and it also has the potential to go negative earnings during bad times. Its forecast accuracy numbers give us very little comfort here. This is one of the reasons why investors no doubt are a bit dubious about the company at this time.

However, what I am telling you is that these trends are in fact superb. We're talking a solid sales growth in the single digits, up 14% for the 9M period in OEM, and 4% in aftermarket. The company managed over €5B of sales in a single quarter, confirming the theoretical run-rate here.

Here is a high-level picture of what makes Valeo a solid choice for investors here, as I see it.

{kind=link}

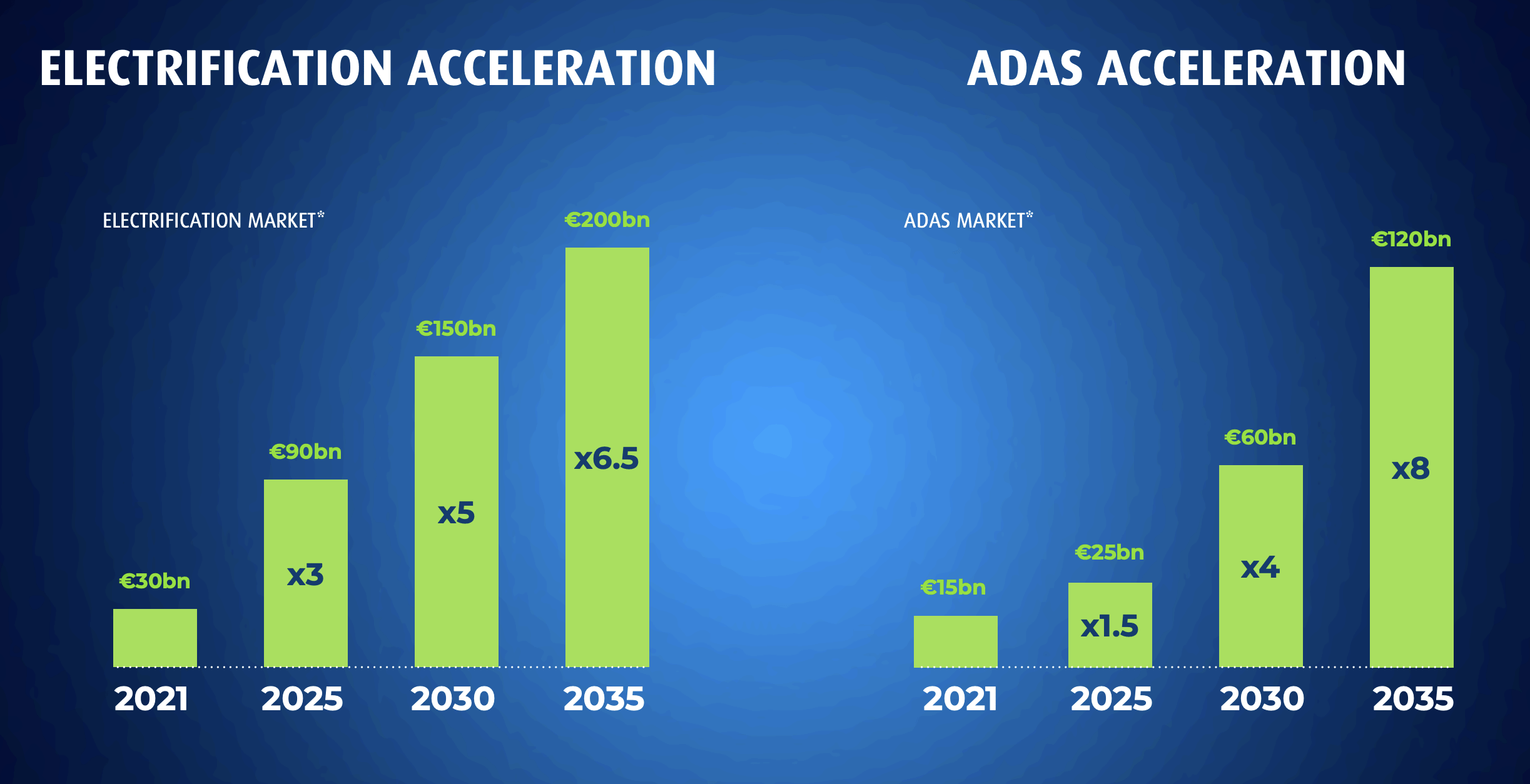

Very little of this business is legacy. It's a very pure play EV company with a future appeal to either EV or xEV products, or products that are not dependent on either ICE or EV as a technology but need to work either way. Less than 8% of sales in 2025E is expected to be ICE, and less than 5% in 2030. Currently, it's going below double digits of the sales mix.

Beyond that, the company is incredibly balanced, and its customers involve every single relevant car brand on the planet, as I see it.

{kind=link}

The company's business model combining product development, its own production systems, and supply integration systems gives Valeo total control over the entire process.

What's more, we can already see over time just how quickly electrification has enhanced this company's sales and improved its margins - and the likelihood for this development to if not continue at the same pace, at least continue in the same direction.

{kind=link}

It's also wrong to only view Valeo as an automotive supply company. The company has ancillary appeal in many areas that are not often thought of here, but which actually are highly relevant here.

{kind=link}

What I want to say about Valeo is that it is a long-term potential investment in electrification, powertrain, and ADAS. With improved fundamentals and earnings, I believe the overall risk factor is actually much lower now than previously. Let me show you where I see the risks and concerns with this company.

Risks & Upside for Valeo

The risks to Valeo are fairly clear. We're talking about a company that's coming out of an environment where it was highly leveraged, and where also margins have not been the greatest for a year or three. Several years the past 20 years have been negative in terms of adjusted EPS. There is no question that Valeo is in fact very volatile - and has the potential to be volatile again.

This needs to be discounted.

The upside that I can find here, however, takes all of that potential risk and almost invalidates it given the sheer upside that is not only visible here, but fairly certain (unless certain fundamental factors change). Even if we assume that the company only manages half of the upside and earnings growth that is currently being estimated, that's still an outsized amount of growth - and much of that near-term is already in the backlog.

The sheer forecast here for the EPS growth we're seeing, and the company's quality coupled with the market and the overall macro situation gives me enough confidence here to go into this investment, despite the risks that can be seen.

Let me clarify the upside in the company valuation.

Valuation for Valeo

Valuation for Valeo is looking very good . I don't use that lightly, or often.

The company is currently trading at a blended 11x P/E, compared to a 5-year average of 16x. But forget 16, let's go 14-15x P/E, discount it straight away, and ignore any premium the company might be deserving, despite being in a very good position for outperformance here.

Even at a discounted P/E, with the current forecasts of 35-50% EPS growth for the next few years each year, that's an upside of no less than 75% annually at 14.5x. That's annually, not in total. Total is over 200%, implying in turn a share price of over €42.5/share here.

You might say that even this discounting isn't enough.

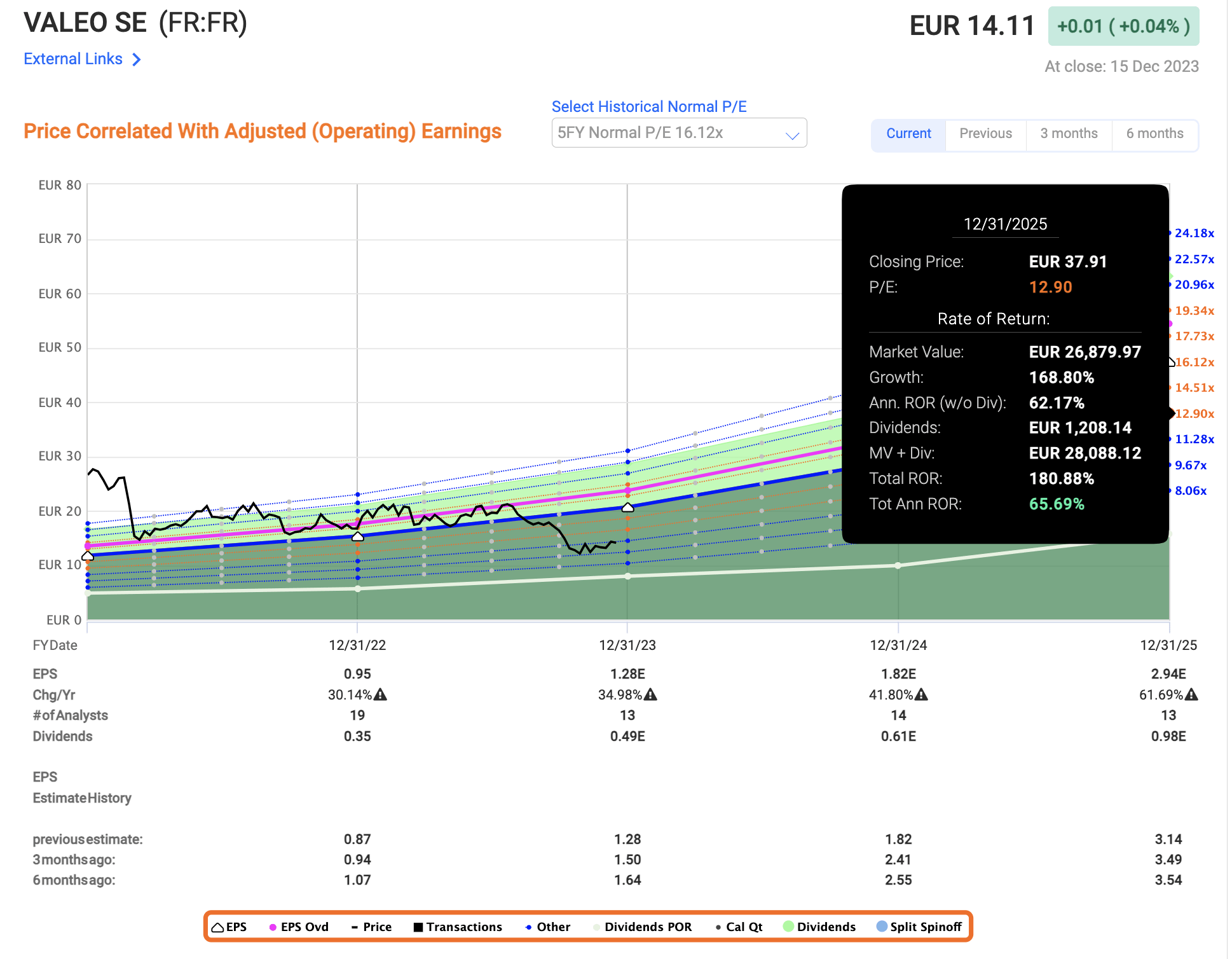

Fine, let's forecast at 12-13x P/E.

{kind=link}

As you can see, even at 12-13x, this company manages over 60% per year or over 170% in total RoR in a few years. This showcases just how much the upside is based on whether these improvements materialize or not - and I believe they actually will.

The macro speaks its own language on this matter. If you want to go contrary to Valeo, you need to go contrary to the entire electrification push, and while I personally believe that it's a bit overhyped and I won't be switching to an EV anytime soon, what I see around me, and what I read in terms of official numbers confirm this upside.

S&P Global gives the company a very conservative set of targets. From a €13/share low, which essentially forecasts the company not being able to grow or achieve any of its operational targets, to a high of €30/share, which is essentially an 11-12x forward P/E, that I myself am using as the lowest possible price target that I consider likely for Valeo.

17 analysts follow the company. Out of those 17 analysts, 9 are at a "BUY" with the remainder at a "HOLD", and only one at a "SELL". The overall picture is that some analysts are looking to see more improvements before going in, but there is little doubt that the company is "going up" for the long term - at least how I interpret the current trends.

From this, I give you the following thesis for the company.

Thesis

- Valeo is one of the more solid automotive suppliers I've been able to find and one that's perfectly aligned with where I believe the overall current automotive sector is moving. Its fundamentals are prepared better for what may be happening.

- The company is currently in that perfect sweet spot where the market has not yet caught up to or underestimated the fundamental improvements that this company is capable of. It's "lagging" the trends of the company here, for lack of a better term.

- Because of this, I am highly positive about Valeo here, and would even at a discounted rate consider it worth at least €30/share for the long term.

- Because of this variation between valuation and what may happen, I give this company a firm "BUY" rating here.

- I bought Valeo today and may buy more.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

For further details see:

Valeo: A Good Investment For The EV/ADAC Upside