VLO - Valero: Despite Massive Strength I'm Considering Selling (Rating Downgrade)

2023-09-26 10:00:41 ET

Summary

- Valero Energy Corporation has experienced significant growth, returning almost 200% excluding dividends since the depths of the pandemic.

- The refining industry is thriving due to favorable margins and supply-related factors, such as inadequate crude-processing capacity and unexpected outages.

- Valero's strategic growth and financial discipline, including a sub-0.3x net leverage ratio, indicate a commitment to shareholder returns, but the current risk/reward may warrant selling some shares.

Introduction

It's time to discuss an investment that has been with me since I started my current dividend growth portfolio in 2020. I bought Valero Energy Corporation ( VLO ) during the depths of the pandemic when we had no vaccine and no light at the end of the tunnel.

While I was unable to buy it at the bottom (I was down more than 20% at some point), the stock has turned into one of my best investments, returning almost 200%, excluding dividends.

I'm bringing this up because the company has gone from an underperformer with many issues and a high risk of dividend cuts to a company that is firing on all cylinders.

Not only is it benefiting from ongoing strength in gasoline demand, favorable margins, and past tailwinds that have resulted in a tsunami of cash, but also new geopolitical developments benefiting North American refiners.

The bull case has gotten so good that I'm considering taking some money off the table - especially in light of potential economic issues down the road.

In this article, I will share my thoughts and discuss the company's risk/reward so investors know what's going on in my mind.

Let's start with the bigger picture.

Refining Is In A Great Place

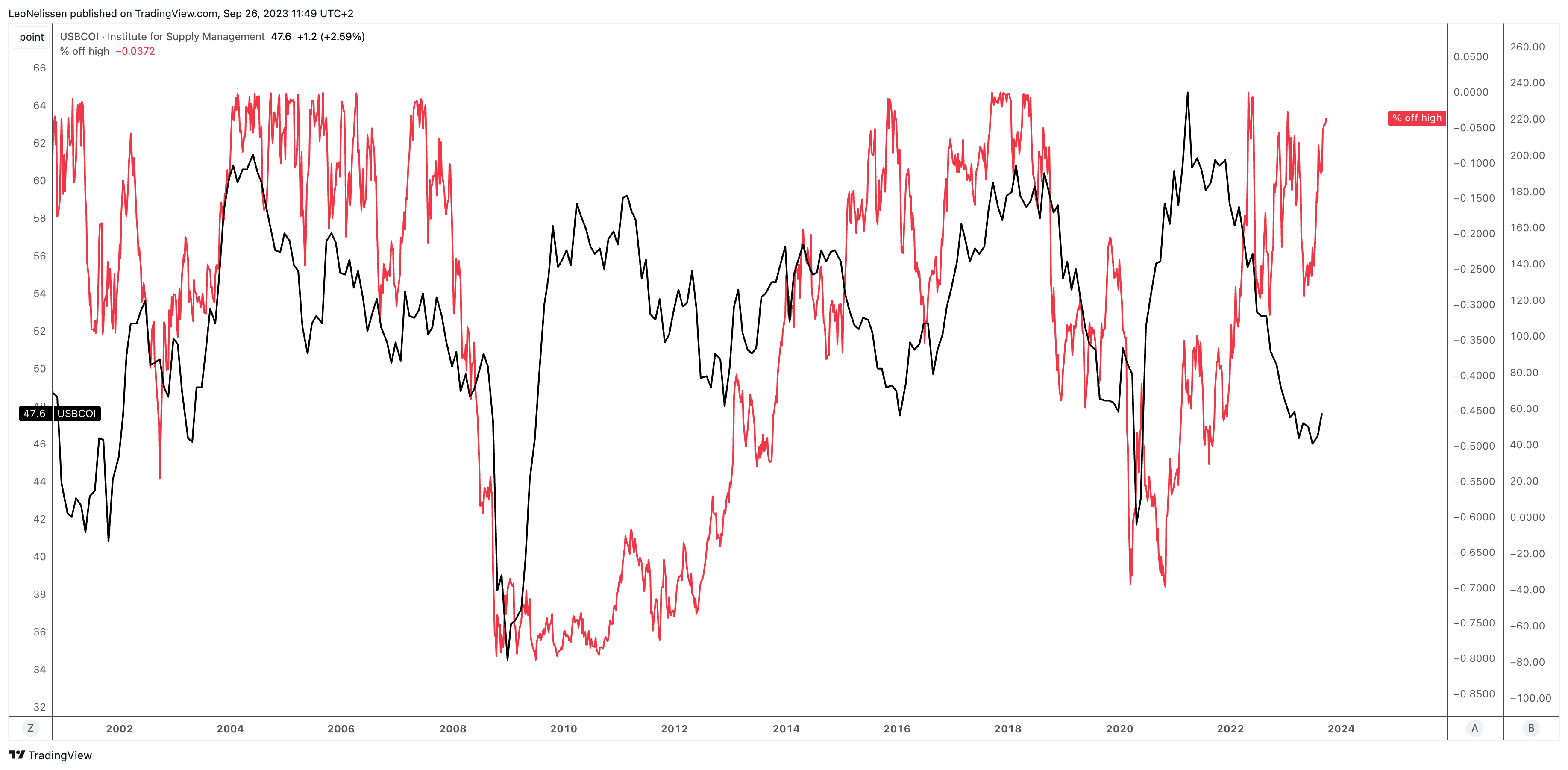

The chart below shows the relationship between the VLO stock price (% below its all-time high) and the ISM Manufacturing Index, my favorite leading indicator for economic growth.

TradingView - VLO (% off its all-time high), ISM Index

{kind=link}

While the correlation is far from perfect, we see that economic downtrends almost always result in steep losses for VLO investors. Almost always.

Right now, VLO shares are up 16% year-to-date, less than 4% below their all-time high.

Meanwhile, the ISM Index has been below 50 (the neutral line between growth and contraction) for ten consecutive months.

Despite economic headwinds, refining companies enjoy strong tailwinds that are mainly supply-related.

{kind=link}

Earlier this month, Bloomberg highlighted some of the biggest issues driving favorable refining margins.

According to the article, oil executives are seeing a critical issue of inadequate crude-processing capacity due to a lack of investment, coupled with more frequent shutdowns, as refiners prioritize higher margins and defer planned maintenance.

This pattern emerged during the APPEC by S&P Global Insights conference held in Singapore. The consequence of this situation is the heightened vulnerability of fuel prices, particularly diesel and gasoline, to abrupt fluctuations whenever unexpected outages occur.

Bloomberg

For example, unplanned plant shutdowns have been occurring almost weekly in Europe.

According to Bloomberg, Frederic Lasserre, global head of research & analysis at Gunvor Group Ltd., makes the case that many refiners have delayed routine maintenance, making them susceptible to unexpected technical glitches resulting in surprise outages.

Especially after the pandemic, too much supply was offline, which forced refineries to produce at elevated utilization rates.

Not only is this an issue in Europe, but stockpiles are tight in general.

In the United States, inventories for finished products are dropping faster than expected.

Gasoline stockpiles fell by 831,000 barrels to 219.5 million barrels, compared with analysts’ expectations of a 500,000-barrel increase.

Distillate stocks, which are mostly diesel fuel, dropped by 2.9 million barrels to 119.7 million barrels, and are now about 14% below the five-year average, the EIA said. Analysts had forecast distillates inventories would fall by just 200,000 barrels last week. - Wall Street Journal .

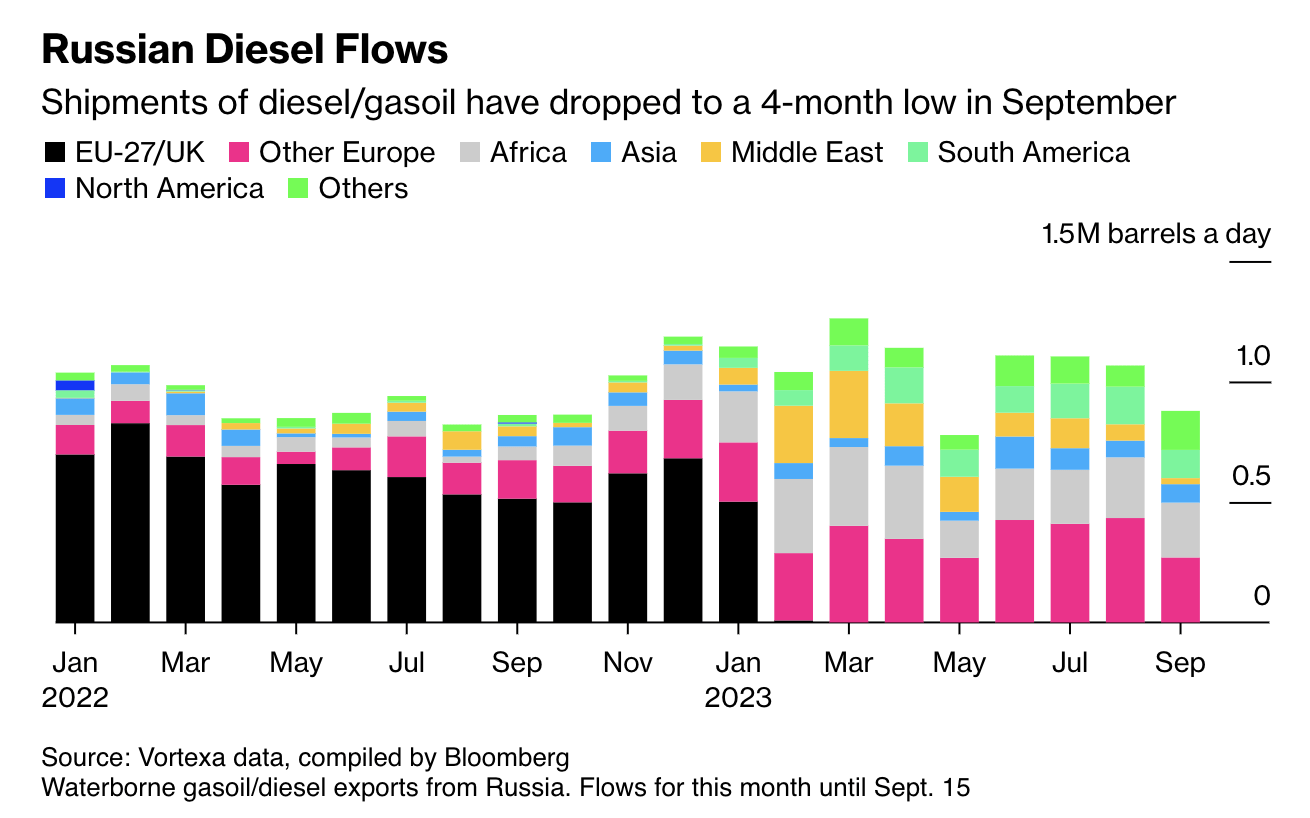

To make things worse, Russia is increasingly using its energy leverage.

On September 21, Bloomberg reported that Russia is temporarily banning exports of diesel in order to support domestic supplies. This hurts Europe and global supply in general. After all, if one region sees a lower supply, it needs to import from other regions.

Diesel prices in Europe jumped on concern the measure will aggravate global shortages. The world’s oil refiners are struggling to produce enough of the fuel amid curbed crude supplies from Russia and Saudi Arabia, the biggest producers within the Organization of Petroleum Exporting Countries and its allies.

“Despite this being only a temporary ban, the impact is significant as Russia remains a key diesel exporter to global markets,” said Alan Gelder, vice president of refining, chemicals and oil markets at consultancy Wood Mackenzie Ltd. “The global refining system will struggle to replace those lost Russian volumes at a time when global diesel inventories are already at low levels.”

{kind=link}

Having said all of this, instead of easing prices due to new post-pandemic supply, the situation remains tight, pressured by outages, persistent demand, and new geopolitical issues.

Refinery companies are winning big time.

Over the past three years, America's two pure-play refinery stocks, Marathon Petroleum ( MPC ) and Valero Energy, are up 439% and 234%, respectively. I excluded Phillips 66 ( PSX ) due to its massive footprint in chemicals.

With this in mind, what do we make of VLO at these prices?

The Valero Risk/Reward

In the second quarter, the company massively benefited from the aforementioned tailwinds.

Its refineries had a throughput capacity utilization of 94%, capitalizing on tight product supply and strong product demand in the U.S.

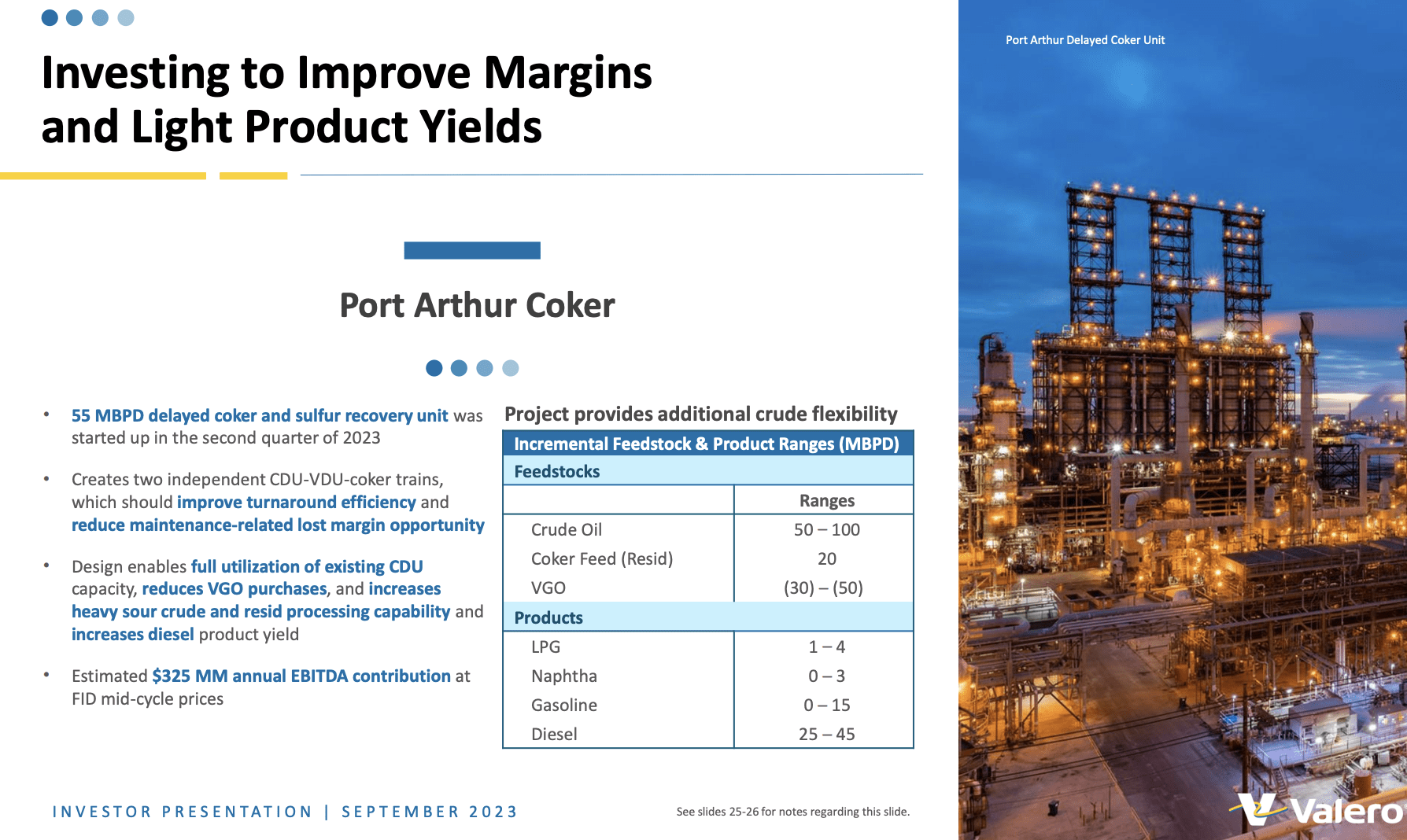

The company also started its Port Arthur coker, which has the capability of adding up to 100 thousand barrels of crude oil capacity to the company's daily capacity.

Valero also expanded its renewable products.

Our Renewable Diesel segment set records for operating income and sales volumes in the second quarter, driven by incremental production volumes from Diamond Green Diesel, Port Arthur. The Diamond Green Diesel sustainable aviation fuel project at Port Arthur is progressing on schedule. - Valero 2Q23 Earnings Call .

{kind=link}

Looking forward, Valero anticipates that low global light product inventories and tight supply-and-demand balances will continue to support refining fundamentals.

Global demand for transportation fuels has rebounded substantially, with gasoline and diesel demand on par with pre-pandemic levels and steady growth in jet fuel demand.

This outlook reinforces the company's dedication to its core strategy of operational excellence, capital discipline, and delivering on its commitment to shareholder returns.

When it comes to its commitment to shareholder returns, the company is seeing tailwinds that were unimaginable a few years ago.

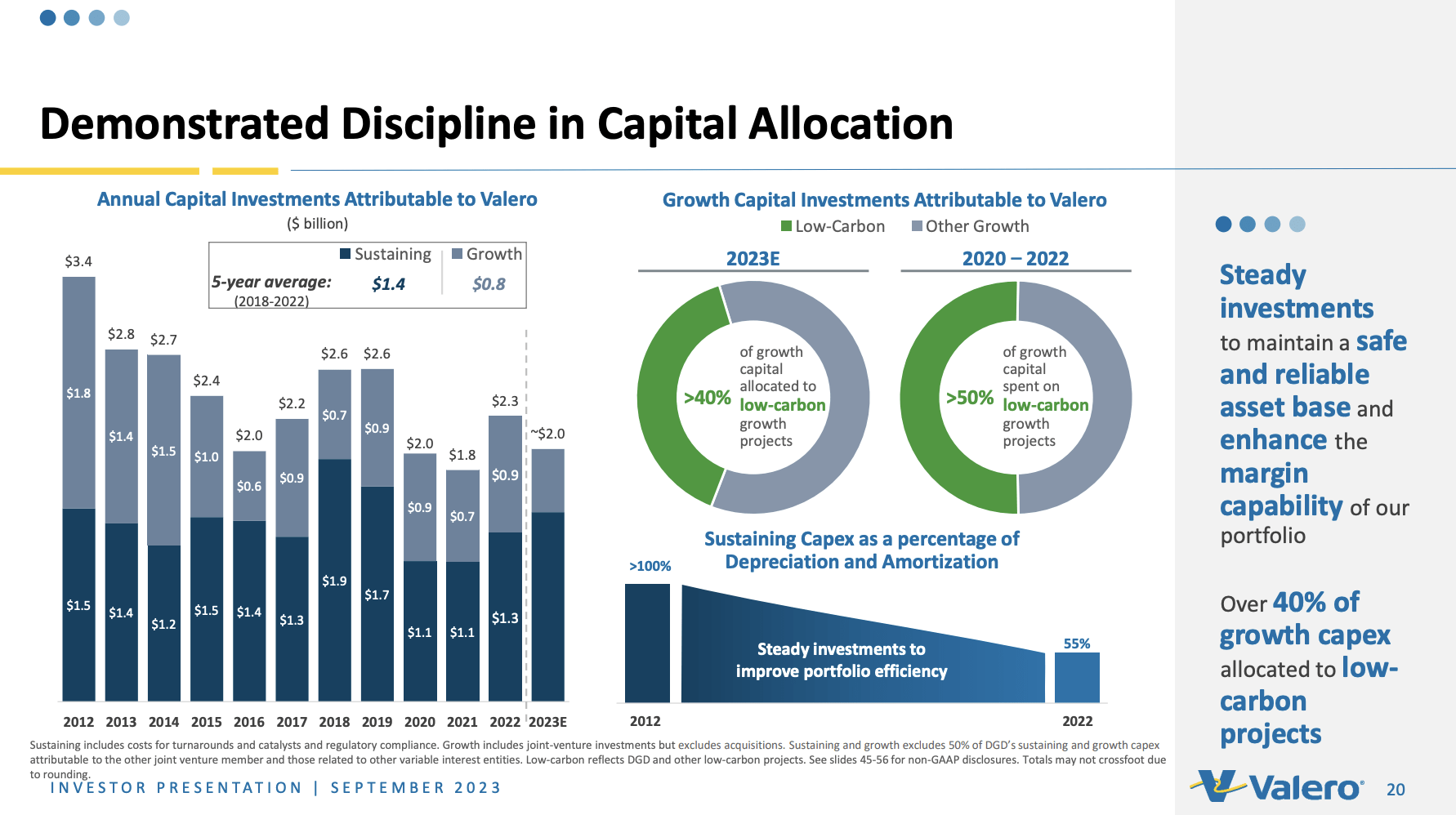

For example, in 2012, the company spent more than 100% of depreciation and amortization on sustaining capital expenditures. In 2022, that number was 55%, indicating much more efficient operations.

{kind=link}

Furthermore, the company's total CapEx requirements are below the longer-term average, thanks to lower growth CapEx, as major projects have progressed nicely over the past few years, generating additional earnings.

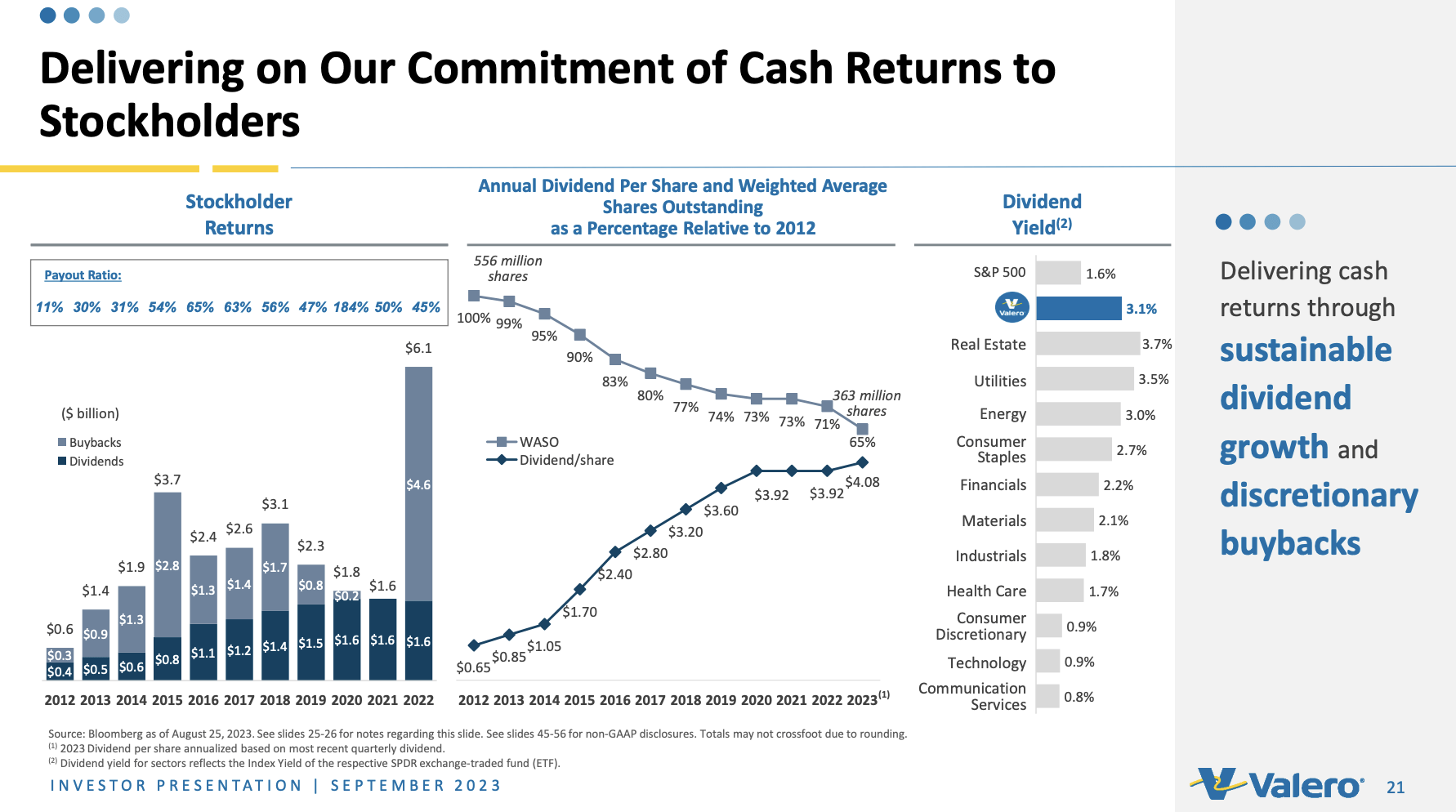

Hence, after spending 2020 and 2021 protecting the balance sheet , the company is now back on track, repurchasing stock and raising its dividend.

Last year alone, the company distributed $6.1 billion to shareholders, which was a blowout record and still less than 50% of its net income.

{kind=link}

In the second quarter, the company made clear that it has a strategy of balancing dividends with share repurchases to ensure an optimal allocation of capital to provide returns to shareholders.

As the overview above shows, Valero's share repurchase program is a fundamental element of its capital allocation strategy.

The significant allocation of funds, amounting to $951 million in the second quarter for the repurchase of shares, shows the company's confidence in its growth trajectory and belief in the intrinsic value of its shares (buying back shares when the valuation looks attractive).

The repurchase of roughly 8.4 million shares in the quarter alone reflects the proactive steps Valero is taking to manage its outstanding shares and potentially enhance shareholder value.

Having said that, the current dividend yield is 2.8%, which is nothing to write home about, at least not in the energy sector, where drillers often pay much higher yields.

On January 31, the company hiked by 4.1%, which shows that it is still mainly focused on buybacks instead of hiking its quarterly dividend commitment.

Nonetheless, going forward, I expect dividend growth to pick up.

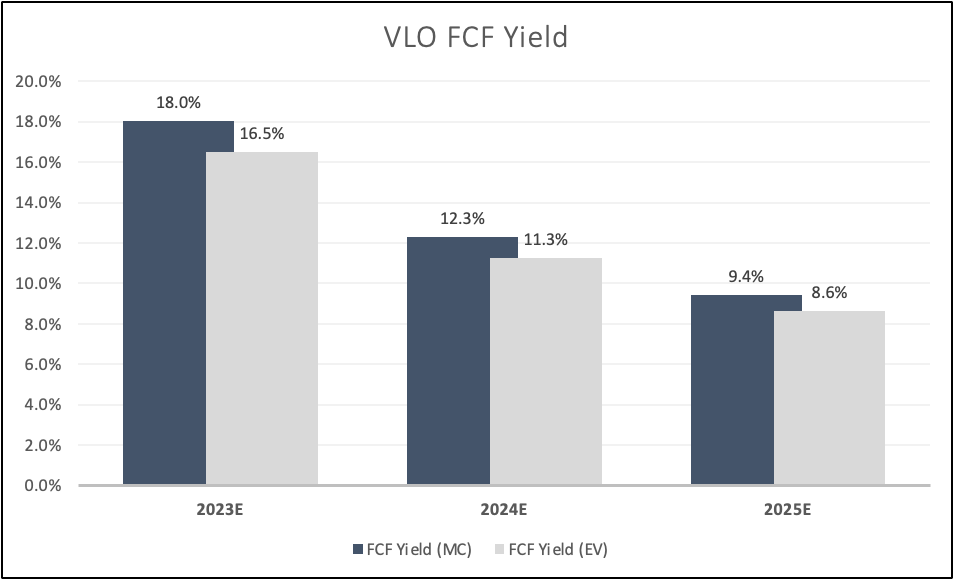

The company has a sub-0.3x net leverage ratio, which is one of the best numbers in its sector. It is expected to lower net debt to less than $3 billion next year, and free cash flow expectations indicate a >12% free cash flow yield next year.

Leo Nelissen (Based on analyst estimates)

{kind=link}

In other words, if the company were to spend every penny of free cash flow on distributions, it could distribute 12.3% of its market cap to shareholders.

I'm not saying that will happen, but it shows how much cash this company is generating.

Note that free cash flow is expected to fall in the years ahead. This is not an indication that Valero is doing something wrong. It shows that analysts are expecting a normalization in refining margins, as no analyst is willing to incorporate prolonged geopolitical issues and other supply forces in their estimates. I can get behind that.

However, it means that any tailwinds could lead to higher expectations for the quarters and years ahead.

Valuation

This part is so tricky. Not only because nobody knows how long refinery margins will remain tight but also because the global economy isn't doing so well right now. We could easily run into a scenario where demand destruction offsets tight supply.

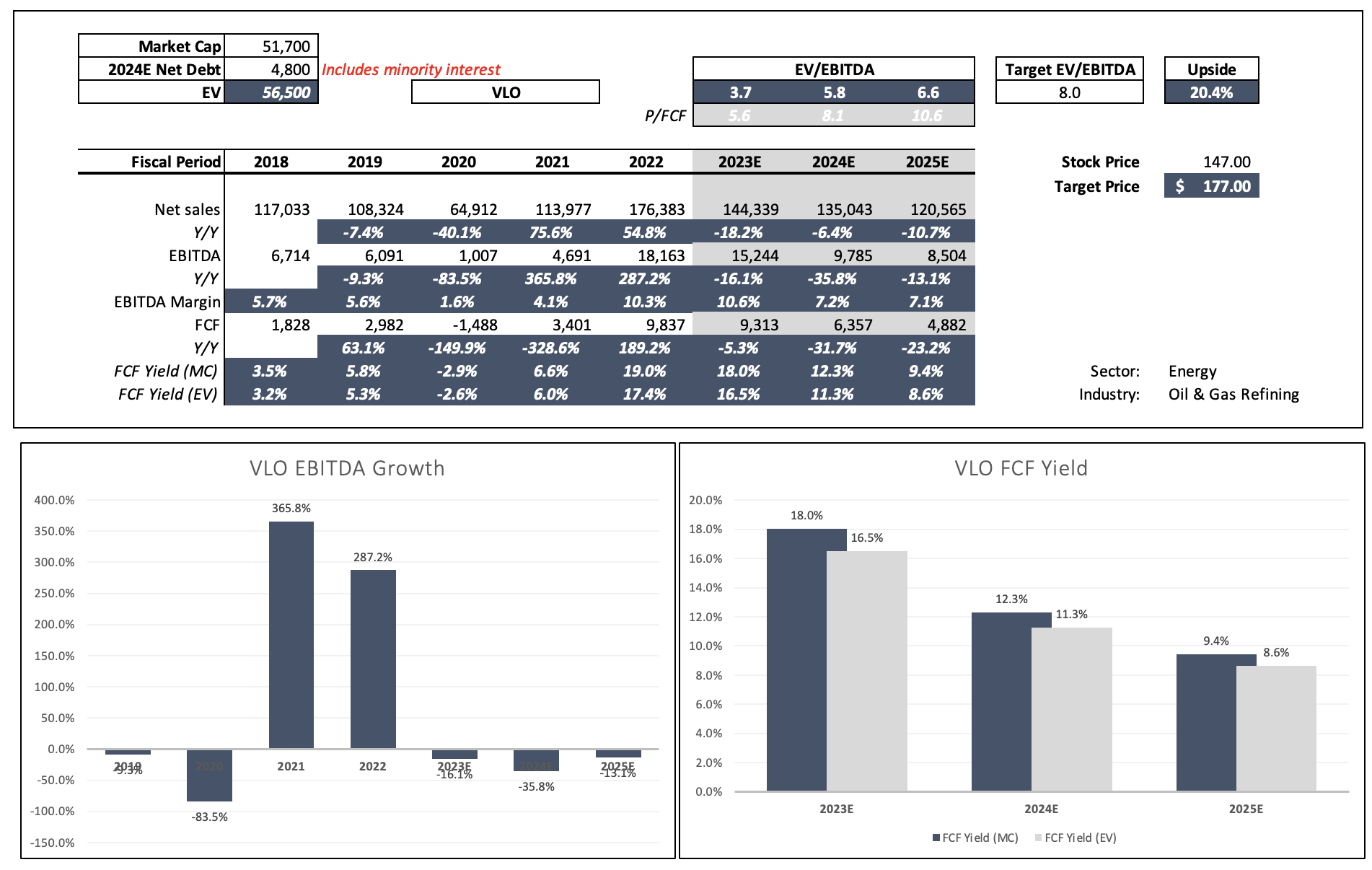

Having said that, the company is trading at less than 4x 2023E EBITDA. That number rises to 6.6x 2025E EBITDA due to the aforementioned decline in expected margins.

Leo Nelissen (Based on analyst estimates)

{kind=link}

If we apply an 8x multiple, we get a price target of $177. The current consensus price target is $145, a dollar below the current price.

My opinion is that the company will generate higher-than-expected earnings (including EBITDA and free cash flow) over the next few years. I do not expect supply to rebound as quickly as expected, and I'm also not a supporter of the thesis that quick EV adoption will significantly hurt demand.

If anything, emerging demand in markets like Asia and Africa will likely provide strong export demand growth for decades to come.

Having said that, I'm considering selling a bit of VLO.

- VLO's mid-term risk/reward has gotten unfavorable. The market has priced in new supply issues while economic growth has continued to decline.

- Some of my favorite investments have sold off quite a bit, which would allow me to rotate some cash from VLO to other investments.

- I'm also looking to de-risk my portfolio a bit, moving cash from volatile investments to less volatile investments.

This is not a call to get people to sell VLO. This is just my view on the mid-term risk/reward.

I believe that VLO has a very bright future, and if I decide to sell, I will be on the hunt to buy back at lower prices. That could be triggered by a further decline in economic growth, causing potential demand destruction to offset supply tailwinds.

Takeaway

Valero Energy has transformed from a struggling investment to a major success.

The refining industry, despite economic headwinds, is thriving due to supply-related factors. Recent geopolitical shifts, like Russia's temporary diesel export ban, emphasize this.

Valero's strategic growth and financial discipline bode well for investors. The company's prudent capital allocation strategy, boasting a sub-0.3x net leverage ratio, signifies a commitment to shareholder returns.

Nonetheless, given the current risk/reward and other investment opportunities, I'm considering selling a bit of Valero Energy Corporation to potentially buy it back at lower prices if I get the chance.

For further details see:

Valero: Despite Massive Strength, I'm Considering Selling (Rating Downgrade)