VLO - Valero Energy: A Buy The Fundamentals Are Strong And Balance Sheet Has Been Rebuilt

2023-03-09 03:57:59 ET

Summary

- Valero's core business remains strong. Demand for diesel and fuel products remain high and there are significantly supply constraints in the refining industry in the US and aboard.

- Management has done a good job with the balance sheet, this company has the flexibility now to increase the dividend and initiate significant share buybacks.

- The stock looks cheap using several metrics.

Sometimes the best investments are in the most forgotten sectors. One of the hardest industries during the pandemic was the refining business. Covid forced most companies in the refining business to take on significant debt to survive, and operators in this industry have faced some tough times.

Today, the situation is much more optimistic, the fundamentals of the refining industry are strong.

One leading refiner that is positioned very well today is Valero Energy ( VLO ). Valero faced adversity like most companies in this industry over the last seven years, but the company's core business and balance sheet are in very good shape now.

Valero Energy has had a huge run over the last decade; VLO stock is up 222.64% during that period, while the S&P 500 is up 154.75% in that same timeframe. The refining business got hit predictably hard during Covid. Few industries were more impacted by the pandemic and Covid related government shutdowns than the travel business, and most refiners such as Valero were forced to take on significant debt over the last several years to survive.

Today, Valero Energy is a buy. The fundamentals of the refining business are strong, energy prices and crack spreads are expected to remain at elevated levels for some time. Valero's management team has also done a good job of managing capital, this group has focused on paying off debt in the short-term so the company has more leverage for buybacks and dividend increases over the long-term.

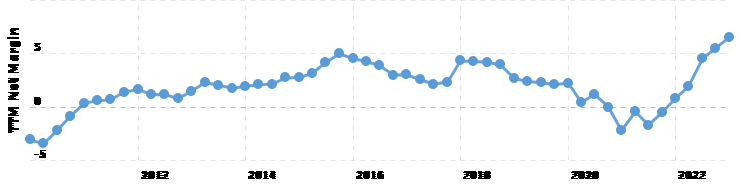

Valero's net margins are currently the highest this company has seen in a decade, and analysts expect crack spreads to remain strong in the refining business.

{kind=link}

{kind=link}

Valero's net margin is currently at 6.54%, which is the highest this company has seen in a decade. Valero's average net margin over the last decade has been just 3%. The crack spread today is nearly $27 a barrel, far higher than the historical average of $10.50 a barrel. While this margin has come down from the high of $35, analysts and traders expect this number to stay elevated for a long time because of several reasons.

Global inventories of multiple oil and gas products, such as diesel and jet fuel, remain very low. Many of the supply constraints that are impacting the energy industry are also likely to remain. The Russia-Ukraine conflict should continue for some time, Asia opening up should lead to growth rates accelerating in the back half of the year, and travel rates are also expected to increase as travel restrictions are eased and more people come back to work. The airline industry expected travel rates to return to pre-pandemic rates of a half a percent of GDP next year.

Most refineries also ran at near full capacity all of next year, and many of these operates will need significant downtime this year for maintenance. There was also significant underinvestment in the energy and refining industry from 2016 to 2020 because of how low oil prices remained for most of that time period. The crack spread future rate for May contracts of this year is nearly $29 a barrel.

Valero has also done a very good job of managing the company's balance sheet during both good and bad times, and this operator's emphasis on paying down and restructuring the significant debt the company took on during Covid should give them a lot of flexibility moving forward. Valero was forced to issue some bonds at 8.75% during the pandemic to survive, and the company took on $4 billion in debt in 2020 alone.

Today, the company's cost of capital is much lower. Management over the last year has been able to issue 4 percent 30-year senior bonds at T+200. Valero paid off $1.3 billion in debt in 2021 alone, and the company has further reduced debt levels by $4 billion since the second half of 2021. Valero's long-term debt levels have fallen from $14.5 billion during the height of the pandemic, to nearly $10.57 billion today, the refiner has also refinanced short term debt at lower rates with longer-term bonds. Valero now has a very strong balance sheet with $4.86 billion in cash on hand.

This is why this refiner looks undervalued today using several different metrics. Valero isn't likely to see another record year like the company had in 2022 anytime soon, but that is already priced into the stock. Valero currently trades at nearly 6x forward earnings estimates, and .33x forward sales estimates. The industry average is 8.82x forward earnings estimates, and 1.91x forward sales projections. Even though analysts are projecting Valero's earnings will fall nearly 15% from the current record levels, to $16.42 a share in 2024, analysts have also consistently underestimated Valero's earnings, and the market has already priced this likely fall in the company's earnings into the stock. This refiner has easily beaten earnings expectations in each of the company's last four quarters earnings reports, and revisions for next year's earnings continue to rise.

The refining industry got hit hard during Covid, and Valero was forced to take on significant additional debt during the pandemic to survive, but today the company is in a very strong position. Management has done a good job of focusing on reducing the company debt that was issued at high rates in 2020, and this refiner now has a lot of flexibility moving forward. While the refining industry isn't often the most talking, Valero should be able to continue to consistently outperform the S&P 500 and most of the broader indexes.

For further details see:

Valero Energy: A Buy, The Fundamentals Are Strong And Balance Sheet Has Been Rebuilt