VLO - Valero Energy Is Benefiting From A Strong Oil Refining Market

2023-04-12 04:54:30 ET

Summary

- Crack spreads remain elevated, benefiting VLO.

- Longer term, the company is working on projects to lower its cost structure and improve margins.

- VLO stock looks fairly valued at current levels.

Valero ( VLO ) is riding a strong oil refining environment, but the stock looks fairly valued around current levels.

Company Profile

VLO is a global refiner that operates in the U.S., Canada, and U.K. Its refineries process a variety of sour and sweet crude, as well as other feedstocks, and produce things such as transportation fuels, low-sulfur fuel oil, heating oil, aromatics, and asphalt.

Overall, the company operates 15 refineries. Thirteen of the refineries are in the U.S. with seven in Texas, two in California, two in Louisiana, one in Oklahoma, and one in Tennessee. It also owns one in Quebec, Canada and one on Wales. Combined the refineries have throughput capacity of approximately 3.2 million BPD.

VLO also owns crude oil pipelines, product pipelines, terminals, tanks, marine docks, truck rack bays, and other assets that support the transport of its refined products. The majority of its products are sold through unbranded channels, but it also sells to independent dealers and distributors that operate under the Valero and other owned brand names.

The company also owns 12 ethanol plants with production capacity of 1.6 billion gallons per year. They also produce co-products such as livestock feed and inedible corn oil. Through its DGD joint venture, it also operates two renewable diesel plants.

Opportunities & Risks

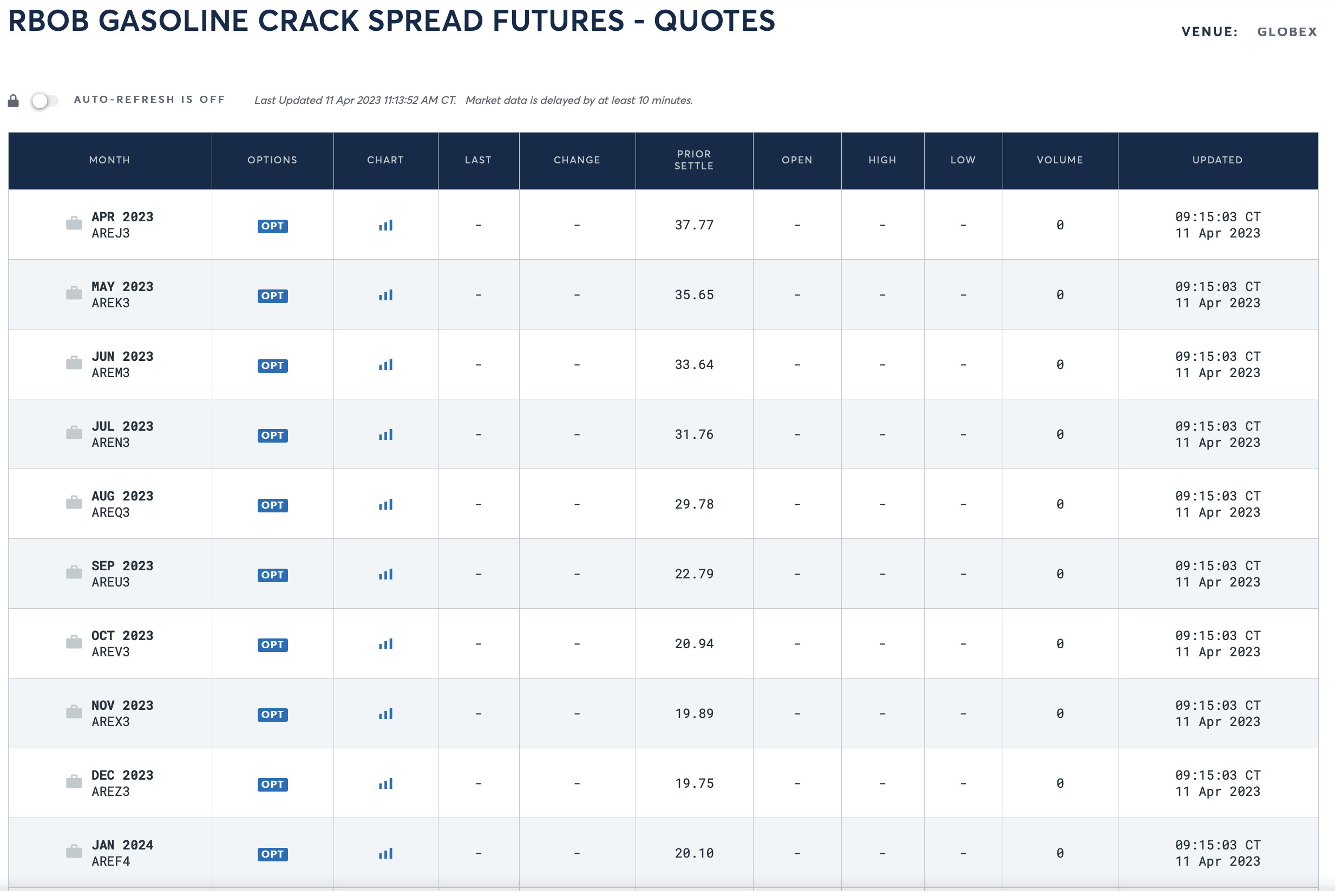

Similar to fellow downstream operator Marathon Petroleum ( MPC ), which I wrote about last month , crack spreads are the biggest driver of VLO’s business. As I noted in that article, in simplest terms, the crack spread is the difference between crude prices and refined product prices. Refiners such as VLO and MPC, meanwhile, have been enjoying very robust crack spreads over the past year.

The historical crack spread is around $10.50 , while today the spread in just under $38 . That’s higher than the $35 when I looked at them a few weeks ago, and futures have also risen during that time, indicating a still solid market.

{kind=link}

Of course, as noted when I looked at MPC, crack spreads really widened at points in 2022. Part of that stemmed from the increased demand for gasoline and other fuels coming out of the pandemic, combined with the release of crude from the U.S. Strategic Petroleum Reserve, creating a huge demand for that crude to be turned into fuel. As a result, VLO’s Refining segment’s operating income went from $1.9 billion in 2021 to $15.8 billion in 2022.

{kind=link}

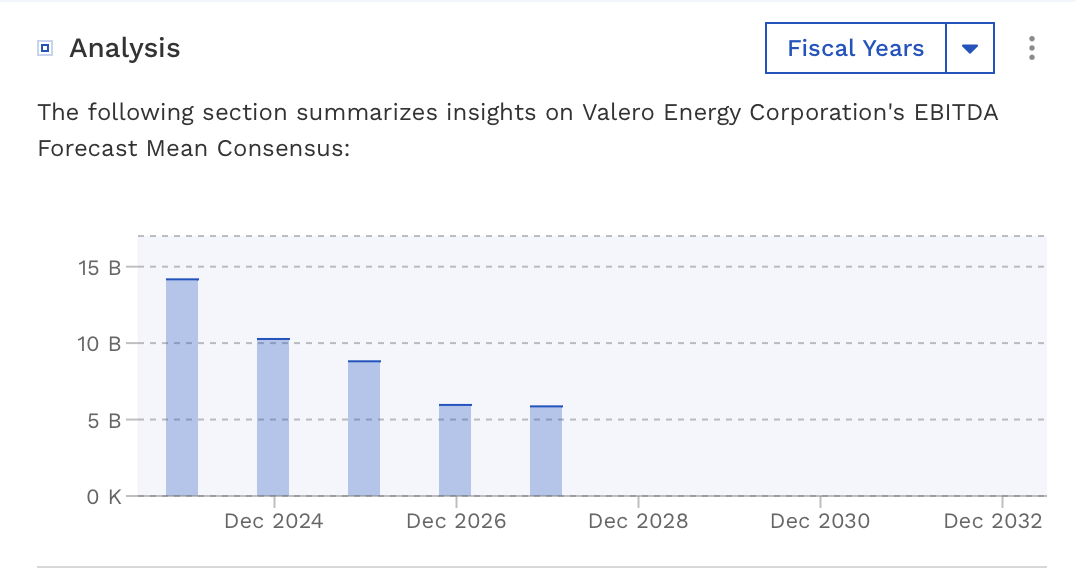

Not surprisingly, VLO will not keep these outsized gains year in and year out. EBITDA is forecast to go from $18.3 billion in 2023 to a projected $14.2 billion this year and analysts are expecting EBITDA to trend lower in later years.

{kind=link}

Discussing refining margins of its Q4 call, CEO Joseph Gorder said:

"As we saw during most of 2022, refining margins were supported by low product inventories, which resulted from the significant permanent global refinery shutdowns and the continued recovery in product demand. Our refining system also benefited from heavily discounted sour crude oils and fuel oils. These discounts were driven by increased sour crude oil supply, high freight rates and the impact from the IMO 2020 regulation for lower sulfur marine fuels. Also, high natural gas prices in Europe incentivized European refiners to process sweet crude oils in lieu of sour crude oils, adding further pressure on sour crude oils. …

“Looking ahead, we expect low product inventories and continued increase in product demand to support margins, particularly for U.S. coastal refiners that have crude oil supply and natural gas advantages relative to global refineries. And we continue to see large discounts for heavy sour crude oils and fuel oils that we can process in our system. The startup of the Port Arthur Coker is also expected to have a significant earnings contribution in the back half of 2023, supported by wide sour crude oil differentials and strong diesel margins.”

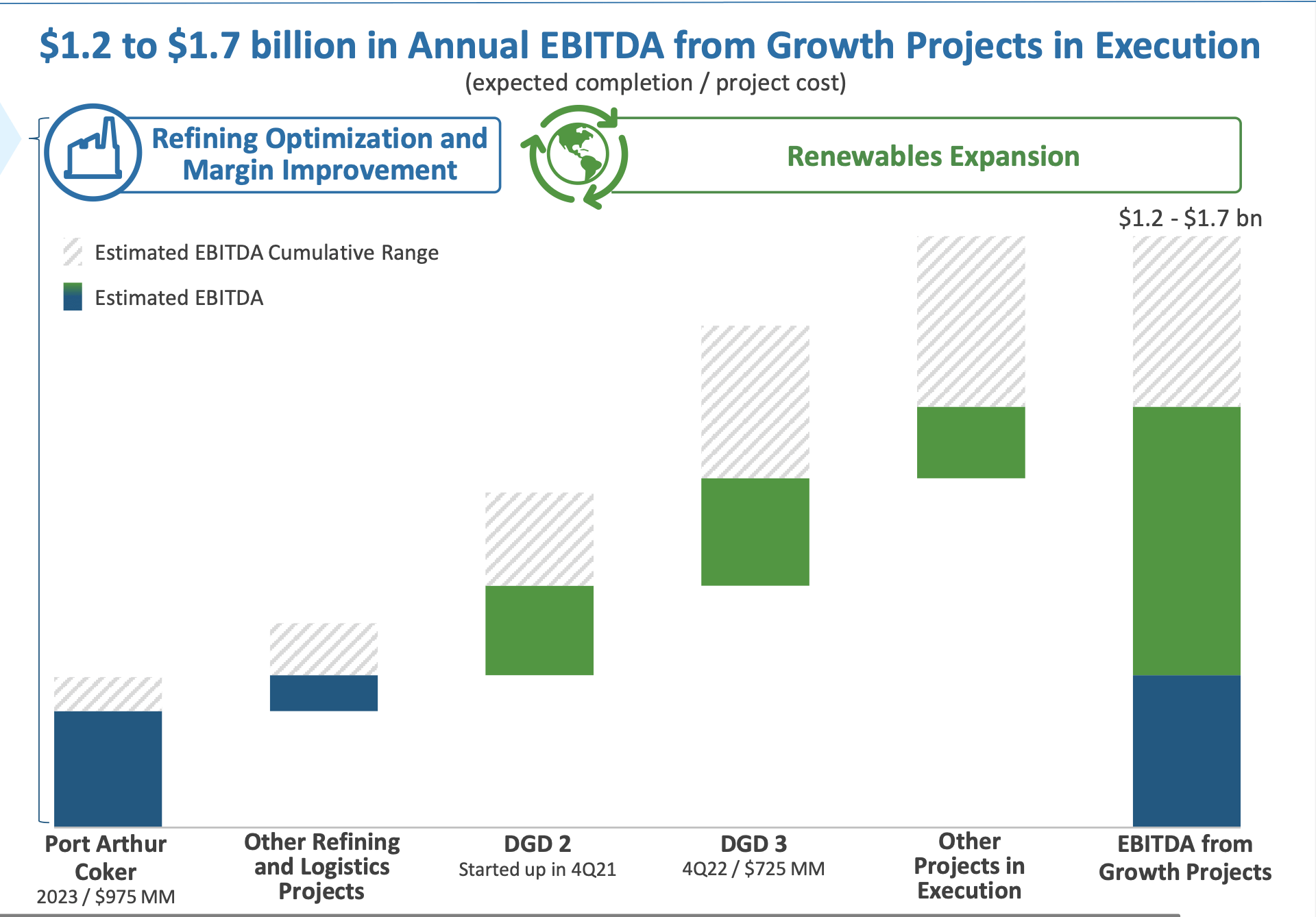

Outside of refining margins, VLO is trying to execute growth projects that will lower its cost structure and improve margins. A lot of smaller projects are being done within its logistics segments, where it is expanding its pipeline capacity and creating better connectivity. It is also investing in its Renewable Diesel segment, where its new DGD Port Arthur renewable diesel plant went into service in November.

VLO’s big project for 2023, though, is its Port Arthur Coker project. The project is expected to be completed in Q2 and will allow the refinery to increase throughput capacity and give it the ability to process incremental volumes of sour crude oils and residual feedstocks, as well has help improve turnaround efficiencies. The project is estimated to contribute $420 million in annual EBITDA based on 2018 prices and $325 million at mid-cycle prices.

The company is also working on carbon capture opportunities within its Ethanol segment. Its BlackRock and Navigators carbon sequestration project is expected to begin start-up activities in late 2024.

{kind=link}

Similar to MPC, VLO also took advantage of its strong earnings to buy back stock in 2022, but not nearly as aggressively. It bought back about $4 billion in stock, reducing its share count by about 8% compared to a 22% reduction by MPC. VLO also reduced its debt by $4 billion since the second half of 2021. It debt-to-capitalization ratio was about 21% at year-end, down from the pandemic high of 40% at the end of March 2021.

Valuation

VLO trades at a 4.1x EV/EBITDA multiple based on the 2023 EBITDA consensus of $14.17 billion. Based off of the 2024 EBITDA consensus of $10.27 billion, it trades at around 5.7x.

It trades at 6x forward EPS, with analysts forecasting 2023 EPS of $23.32.

It’s projected to see revenue fall -10% in 2023.

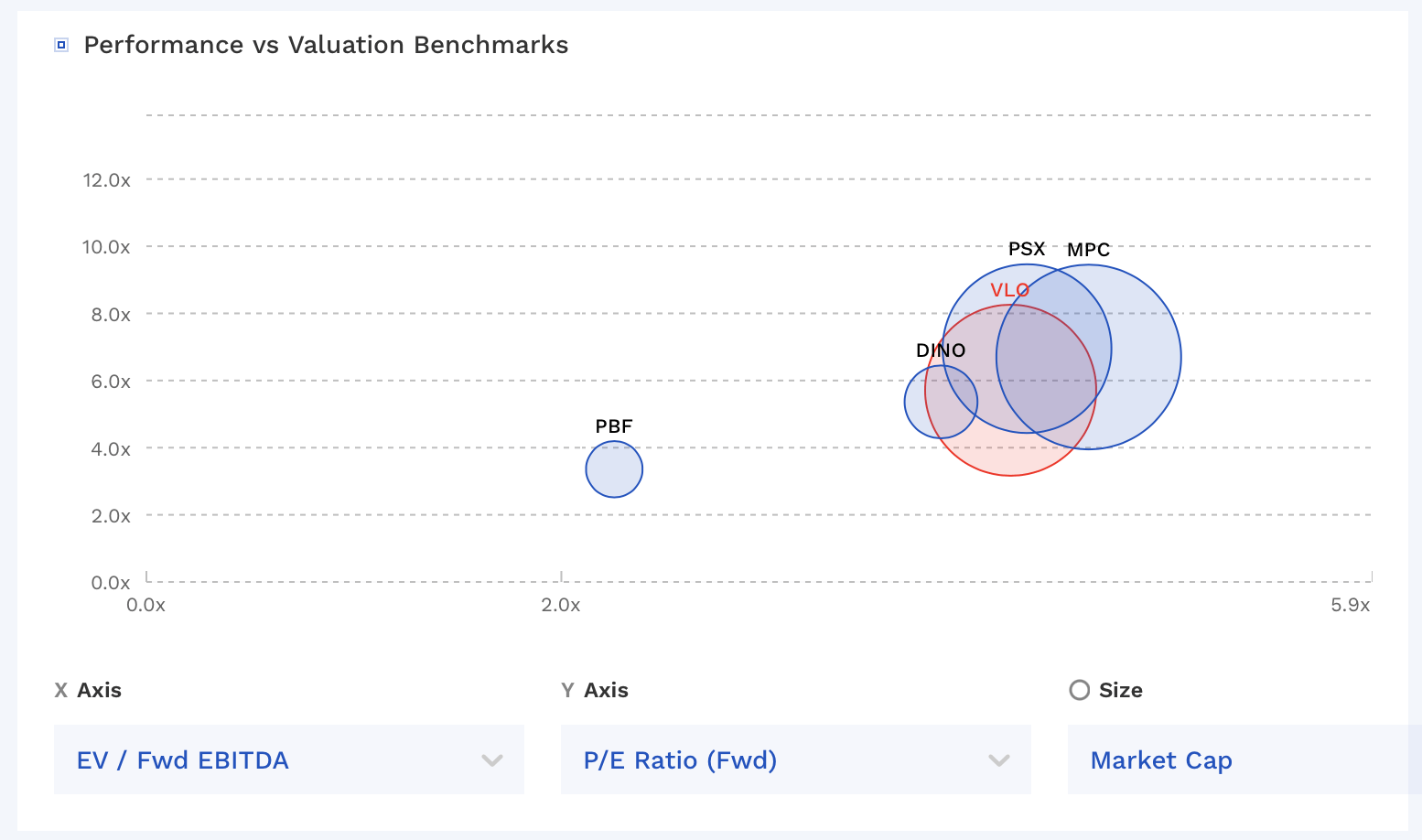

VLO’s stock generally trades in line with other refiners.

{kind=link}

Conclusion

VLO and other refiners look cheap because crack spreads have widened to well above historical norms. More normalized EBITDA after growth projects for VLO is likely closer to $6-7 billion. On that basis, it’s trading around 8-10x normalized EBITDA.

VLO probably has the best position in the Gulf Coast, with over half its U.S. capacity in this advantaged market. The Gulf provides access to various end markets given its infrastructure, as well as more access to cheap natural gas (its uses a significant amount of natural gas to help run its refineries) and skilled labor.

That said, I prefer MPC a little more over VLO given its stake in MPLX ( MPLX ). VLO has its own midstream assets within the company, but not to the extent of MPLX. I rate both stocks a “Hold” and think they should do well the longer the market remains strong for oil refiners.

For further details see:

Valero Energy Is Benefiting From A Strong Oil Refining Market