VLO - Valero Energy: Upgrading To Buy

2023-06-14 18:00:33 ET

Summary

- While VLO is at peak earnings, the company has been doing well buying back stock and increasing its dividend.

- Growth projects should help drive more normalized EBITDA growth once crack spreads return to more historical levels.

- Upgrading the stock to "Buy" after its recent pullback.

The stock of Valero Energy ( VLO ) is down over -17% since I initially placed a “Hold” rating on the stock. Let’s take a closer look to see if the stock is worth upgrading after the pullback.

Company Profile

As a quick reminder, VLO is a refiner with operations in the U.S., Canada, and U.K. It operates 15 refineries that process a variety of sweet and sour crude, as well as other feedstocks, to produce end products such as transportation fuels, low-sulfur fuel oil, heating oil. The company also owns 12 ethanol plants as well.

VLO also owns midstream assets that help support the transportation of crude and refined products, including crude oil pipelines, product pipelines, terminals, tanks, and marine docks. It sells the bulk of its refined products through unbranded channels, but it also has a network of independent dealers and distributors that operate under its own name.

Valero’s Performance and Crack Spreads

For refiners, the biggest driver of their operational performance tends to be crack spreads. In simplest terms, the crack spread is the difference between crude prices and refined product prices. They are a good estimate for refining margins, but they don’t take into account all the revenue from other produced products or the costs outside of crude.

Crack spreads widened to extraordinary levels at points in 2022, fueled by transportation fuel demand coming out of the pandemic, while the U.S. released crude from the U.S. Strategic Petroleum Reserve with the purpose of lowering crude prices, and ultimately prices at the pump.

However, all of that crude needed to be turned into fuel at refineries which caused crack spreads to blow out and be a huge boon to refiners. VLO was a huge beneficiary of these dynamics, seeing its Refining segment’s operating income surge from $1.9 billion in 2021 to $15.8 billion in 2022.

While VLO started to see a boost from crack spreads in Q1 of last year, they really widened in Q2, when the company reported refining operating income of $6.2 billion versus only $349 million in Q2 2021. While not as wide as Q2 2022, crack spreads have remained strong, helping VLO’s Refining segment generate $4.1 billion in operating income in Q1 versus $1.5 billion a year ago.

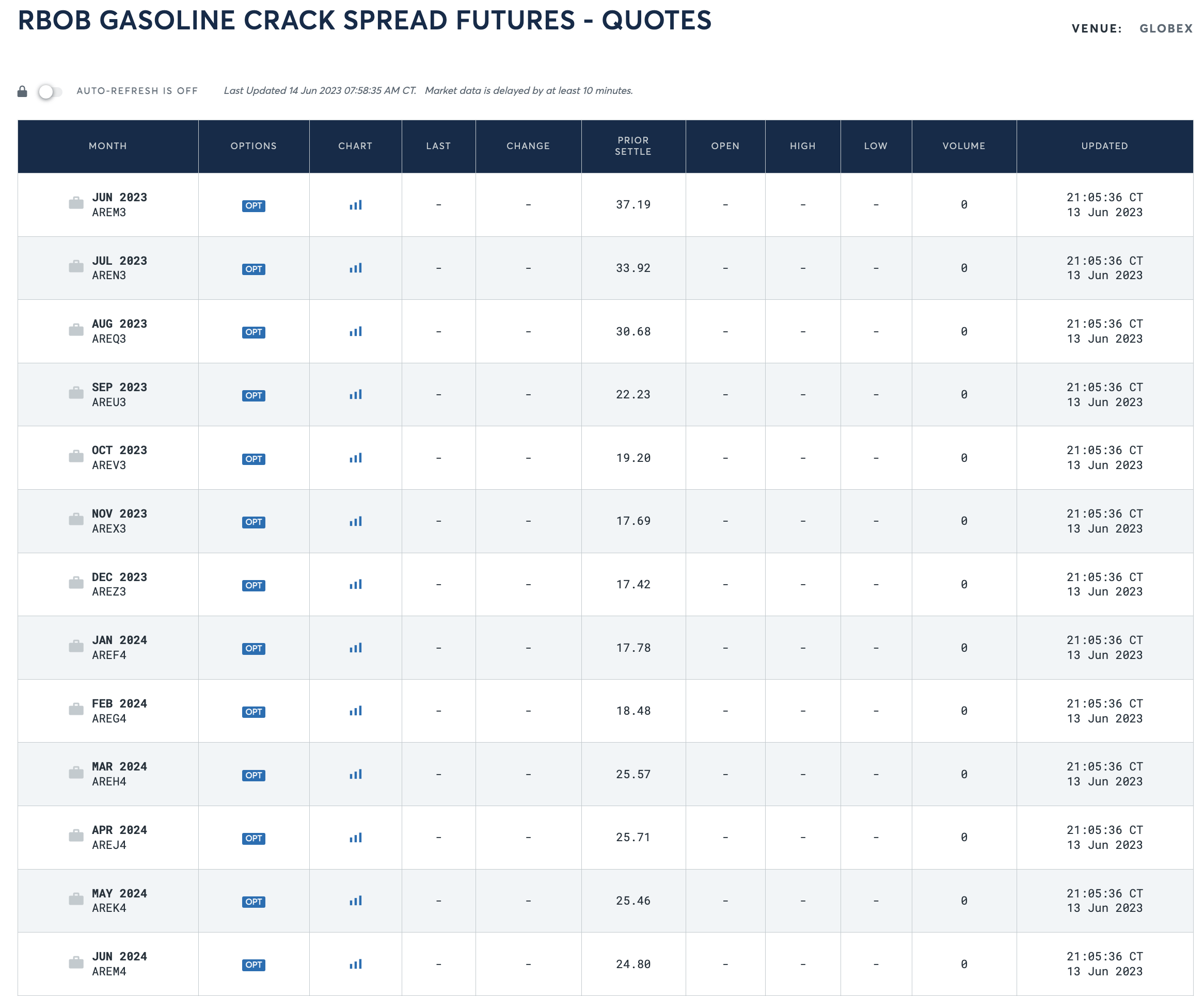

Crack spreads continue to remain strong, with June futures at a robust $37.19. That remains well above the historical crack spread of around $10.50 . Not surprisingly, these conditions are not going to last forever, and the crack spread for the rest of the year is expected to drift lower. There is some seasonality in the spreads, so looking at June 2024 futures, they are a third lower than June 2023 futures.

{kind=link}

Notably, every time I’ve looked at crack spreads for articles on refiners, the near-term months have moved higher. For example, June contracts were $33.64 when I looked at them in April, and today they are over 10% higher. However, autumn month contracts have drifted lower.

Outside of crack spreads, one of the other big themes with VLO is capital allocation. On that front, the company returned over $1.8 billion back to shareholders last quarter. It spent $1.5 billion to repurchase 11 million in shares in Q1. That reduced its shares outstanding by about 3%. Over the past year, the company has reduced its share count by about 8.5%, buying back $4.1 billion in stock at an average price of $124.76.

VLO also paid out a $1.02 quarterly dividend, increasing it from 98 cents. The stock currently yields around 3.6%. And it reduced its debt by $199 million to $9.0 billion. Net debt is $3.5 billion, as it has $5.5 billion in cash and equivalents.

VLO also is continuing with growth projects. It completed its Port Arthur Coker project in March, and started it up in April. The project is estimated to generate $420 million in annual EBITDA based on 2018 prices and $325 million at mid-cycle prices.

In its Renewable Diesel segment, meanwhile, it expects to build a $315 million sustainable aviation facility at Port Arthur, Texas with an expected completion date of 2025. VLO will pay for half the project. It is also looking at other low-carbon opportunities.

Both its Renewable Diesel and Ethanol segments had strong quarters. The Renewable Diesel saw a jump in operating income to $205 million, as it benefited from the ramp up of DGD Port Arthur, which went online in November. Meanwhile, the Ethanol segment saw operating income surge from $1 million a year ago to $39 million, as it averaged 138,000 gallons per day more in production versus last year.

While these segments are small compared to what VLO’s refining segment is currently generating in operating income, in a more normalized environment, they become much more important. Prior to the pandemic in Q1 2019 for example, VLO’s refining segment generated $479 million in operating income, which suddenly makes the $244 million in operating income from its other two segments not look so insignificant.

Notably, after the earnings report, VLO did announce that CEO Joseph Gorder will retire at the end of June after 9 years on the job. Lane Riggs, who had been serving as COO, will take over. I see little disruption coming from the change, as Riggs has been at his position for over 5 years and has held various leadership roles at the company before that.

Valuation

VLO trades at a 3.6x EV/EBITDA multiple based on the 2023 EBITDA consensus of $13.49 billion. Based off of the 2024 EBITDA consensus of $9.2 billion, it trades at around 5.3x.

It trades at about 5x forward EPS, with analysts forecasting 2023 EPS of $22.09.

It’s projected to see revenue fall -15% in 2023.

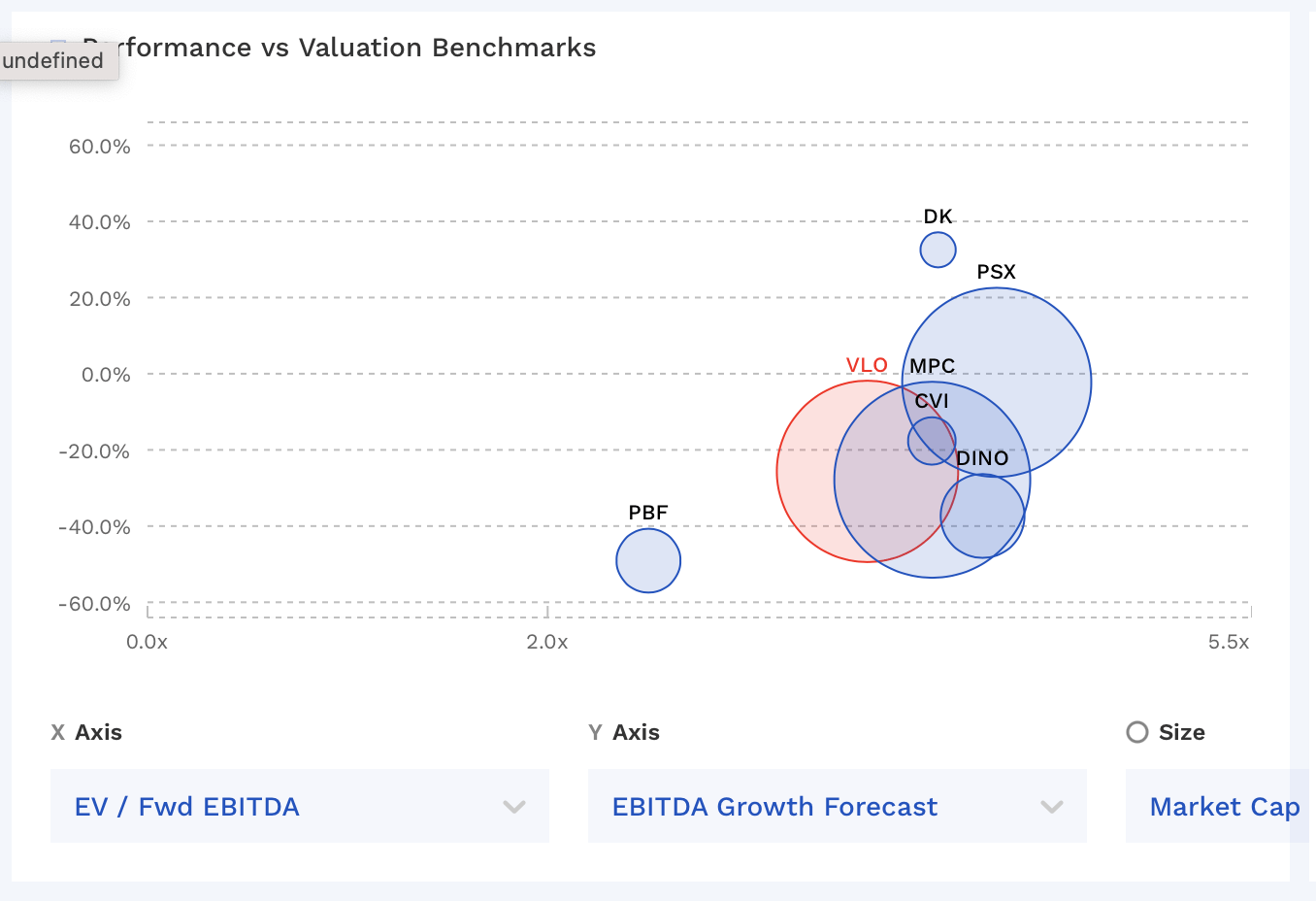

VLO’s stock generally trades in line with other refiners.

VLO Valuation Vs Peers (FinBox)

{kind=link}

As I noted in my original write-up, VLO and other refiners look cheap because crack spreads have widened to well above historical norms. More normalized EBITDA after growth projects for VLO is likely closer to $6-7 billion. On that basis, it’s trading around 7-8x normalized EBITDA. The longer that VLO is able to see outsized crack spreads, the more it will be able to buy back stock and lower net debt as well, which lowers the numerator in the EV/EBITDA equation.

Conclusion

While VLO will see its results trend lower as crack spreads normalize, its Port Arthur project, along with the progress in is Renewable Diesel and Ethanol segments will help with more normalized growth. Meanwhile, the company has done a nice job of balancing growth projects, share buybacks, and debt reduction during this period of outsized earnings. The longer crack spreads remain elevated, the more shares VLO will be able to buy back and the better its balance sheet will be positioned.

The last time I looked at VLO I said I thought the stock looked fairly valued with it trading around $136. To upgrade it to “Buy,” I like to see a 25% return potential. So it’s very close to “Buy” territory, which would be about $109. That said, given the opportunity, I’m going to upgrade the stock to “Buy” today.

For further details see:

Valero Energy: Upgrading To Buy