VLYPP - Valley National Bancorp: Highly Undervalued But Be Careful

2023-05-11 00:30:33 ET

Summary

- The P/B of this one is extremely low, yet it does not have an excessively speculative securities portfolio.

- Deposit beta has exceeded loan beta and momentum is likely to continue.

- The liabilities of this bank inspire confidence because of the stickiness of deposits. Only 31% are uninsured.

Valley National Bancorp ( VLY ) is going through an extremely complex period like all regional banks. The recent bank failures are hitting the stock prices of all small- to medium-sized banks indiscriminately, which is why Valley National Bancorp is performing -38% YTD. But is this slump justified? Let's see it together by analyzing the latest quarterly report .

How solid is this bank?

{kind=link}

Valley National Bancorp Q1 2023

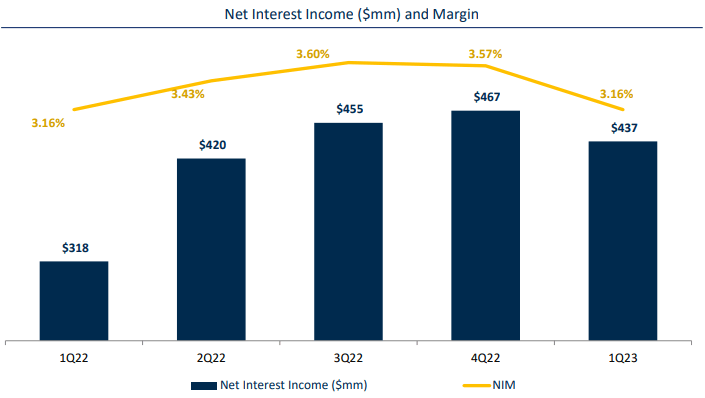

Net interest income achieved an improvement of $119 million over Q1 2022 but fell $30 million from the previous quarter due to a lower margin. But why is the net interest margin shrinking? There are two aspects to consider.

The first is technical, since the bank is preferring to keep liquidity high: thus not reinvesting it, until a normalization of deposit flows occurs. The last few months have been worrisome for the soundness of regional banks, and so Valley National Bancorp has chosen to reduce its profits in return to offset an unforeseen demand for deposit repayments. I find this a reasonable choice.

The second concerns the increasing burden of interest to be paid to finance activities. As everyone knows, the primary activity of banks is to obtain liquidity through deposits in order to invest them at a higher interest rate (typically also with a longer maturity), but at the point when deposits have to guarantee a higher interest, it becomes complex for the bank to keep the net interest margin stable. In the case of Valley National Bancorp this phenomenon is becoming increasingly evident for two reasons:

- The first is that their customers tend to be very liquid and especially savvy about where to deposit their cash. So, the bank is noticing a continuous rotation from non-interest-bearing accounts to interest bearing accounts.

- The second is that the inverted yield curve is hurting the bank's ability to attract new customers. Why should I deposit my cash at Valley National Bancorp and get 1-2% when the 3-month bond yield offers me 5.20%?

As Mike Hagedorn ((CFO)) also explained, such high short-term interest rates do not help bank funding, and only when the yield curve returns with a positive slope the problem will be solved:

The inverted curve is causing increased deposit competition, especially on the short end of the curve, and also we're competing against government securities with our clients as well. Some of the more savvy ones are moving into treasuries. The good news on that side is they're still staying within the Valley family to do that. So in a different interest rate environment, we expect some of those deposits or those securities to rotate back into deposits.

But how serious is the situation? Currently not so much in my opinion.

{kind=link}

Valley National Bancorp Q1 2023

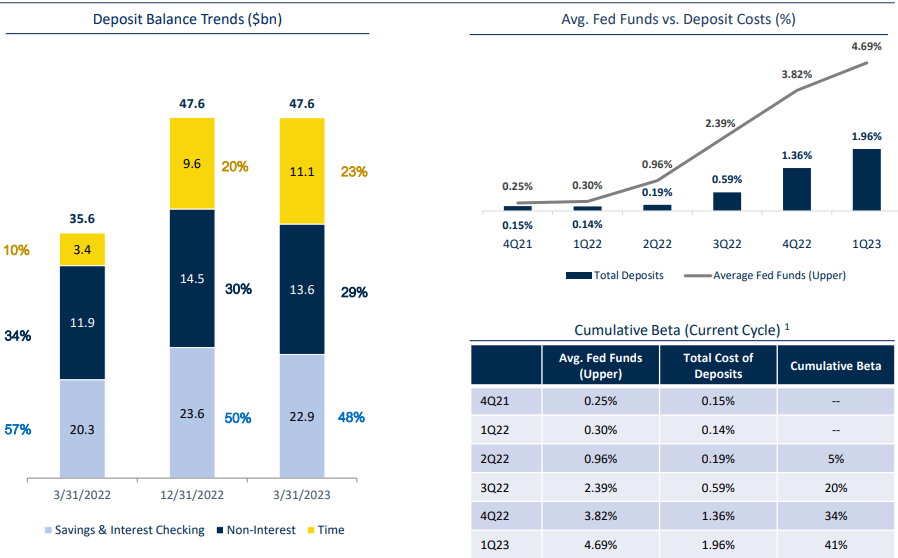

Deposits are up from Q1 2022 and unchanged from the previous quarter. Of course, as already anticipated, non-interest bearing deposits are taking a gradually lower weight on total deposits, but still, the total cost of deposits is not that high, 1.96%. Moreover, total deposits account for 82% of total liabilities and equity.

{kind=link}

Valley National Bancorp Q1 2023

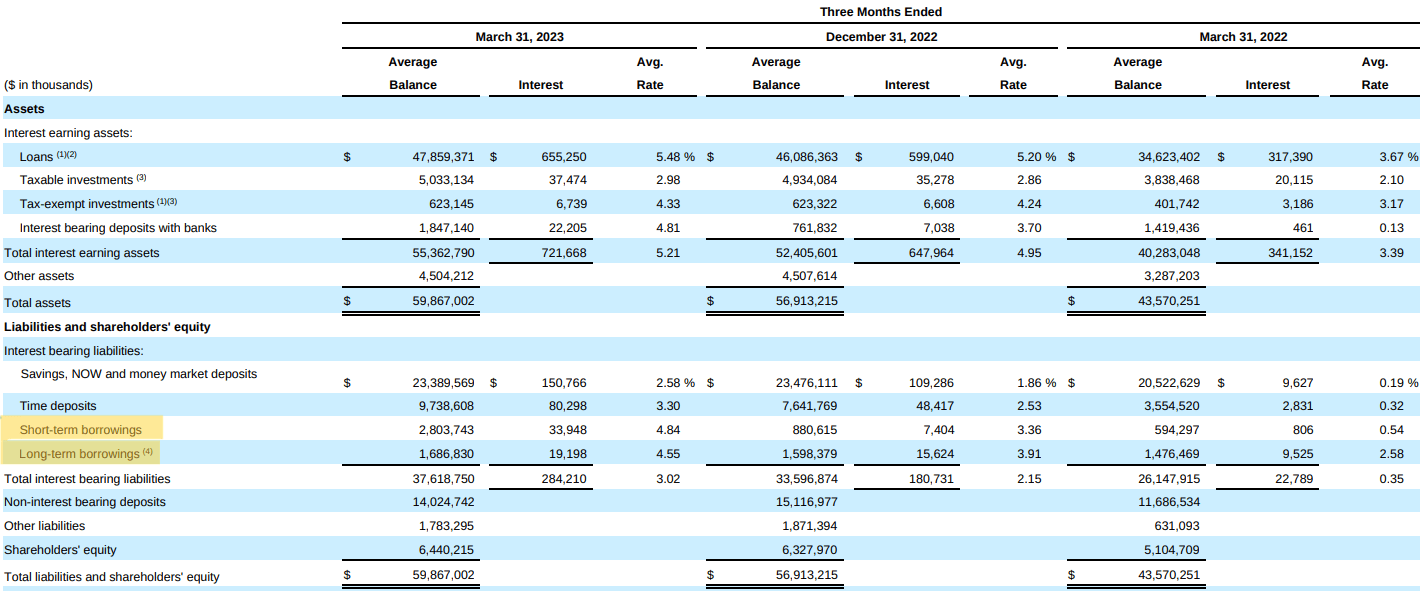

As can be seen from this table, short-term and long-term borrowings have minimal weight compared to deposits, however, it should be pointed out their average interest rate is far higher than the latter. Respectively, 4.84% and 4.55%. But why did Valley National Bancorp borrow money if it has enough deposits? It did so simply as a precautionary measure because of the series of bank failures in March 2023, and much of the short-term borrowing has already been repaid. Here are the CFO's words on the matter:

At the peak during that time (March 9-March 31), it was in excess of $6 billion. And as we sit today, our cash and cash equivalents at the Federal Reserve or any other cash balance is at $1.5 billion. So it is remarkably come down. And just to be clear about this, this was done specifically for an abundance of caution given the environment that existed post March 9.

So, as of now, short-term borrowings are not a problem given their small impact on total liabilities, even though they have a high interest rate. What is more, it is wrong to believe that from now on Valley National Bancorp has to pay 5% interest for every dollar that flows into liabilities since the Fed Funds Rate is at 5-5.25%. On this issue, Ira Robbins ((CEO)) during the conference call was clear:

I think it's probably incorrect to think every incremental dollar of funding cost comes in here at 5%. During the quarter, we raised over $600 million, what I would deem as core funding, non-specific broker and the cost of that was a blended 2.50%.

Let us now proceed to perhaps the most important aspect regarding deposits: how many are insured and how many are uninsured? In the current historical environment, having too many uninsured deposits is practically a death sentence, and Silicon Valley Bank and First Republic know something about this.

Valley National Bancorp Q1 2023

As for Valley National Bancorp, the situation is markedly different from the failed banks: only 31% of deposits are uninsured. Moreover, as shown in the figure, the bank would still be able to cope with a sudden repayment demand for uninsured deposits.

In addition, the bank revealed some statistics that improve its position in terms of deposit stickiness:

- Average Account Size (Commercial & Consumer) is $58,000.

- Average Customer Relationship with Valley is 10+ years.

- ~80% of customers with Valley for 5 years or more.

In light of these considerations, liabilities do not currently show serious signs of weakness. However, attention must be paid to how the situation will develop.

Valley National Bancorp Q1 2023

The deposit beta is increasing, which means that the bank is increasingly forced to adjust the interest rates offered on deposits to the short-term benchmark rates. Now the Fed Funds Rate is at 5 to 5.25%, so it is virtually certain that as early as next quarter we will see deposits that will be more expensive. The question is, when will the deposit beta go back down? According to Ira Robbins as long as the yield curve is inverted there is little that can be done:

Most of our competition today isn't peer banks that are sitting around the corner. Most of the competition sits in the treasury today based on where they are. So that deposit beta is going to stay elevated, I believe, as long as we're in this inverted curve. But once we get back to sort of a normalized curve in a normalized environment, I think the deposit betas will really come back down.

The Fed is not planning to cut rates this year, so I expect deposit beta to increase.

{kind=link}

Valley National Bancorp Q1 2023

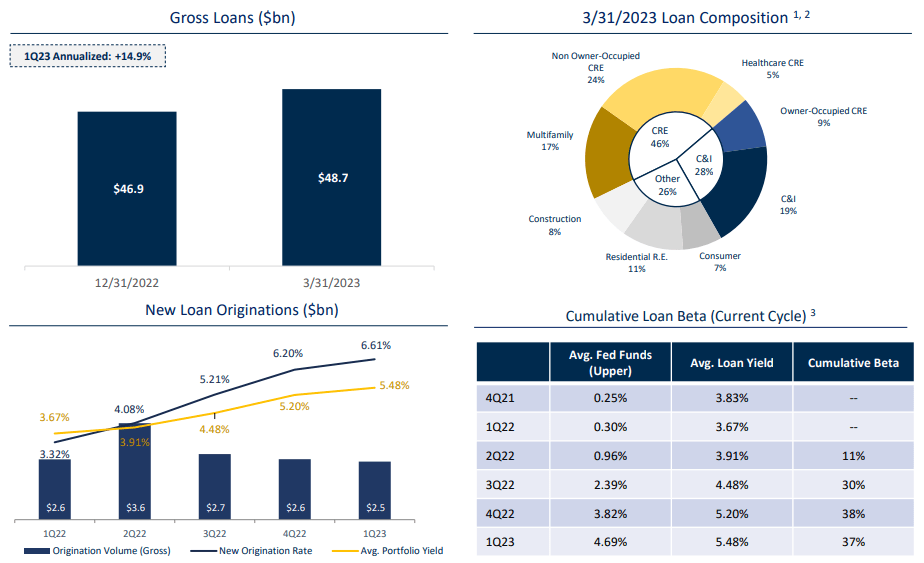

Anyway, the problem is not high deposit beta, but whether deposit beta increases more than loan beta. As long as the bank can lend at interest rates that rise more than deposit interest, the problem is not there. The point, however, is that this is not happening. The loan beta in Q1 2023 was 37%, while the deposit beta was 41%; after years, the latter is higher.

This means that the bank is adjusting passive interest rates more quickly to the Fed Funds Rate than active interest rates. In short, it all adds up, and that is why the net interest margin fell this quarter.

In this picture, however, there is another interesting aspect to comment on: new loan originations.

Compared to the previous quarter, new loans were made at a fairly similar interest rate thanks to a declining loan beta, yet this was not enough to stimulate demand for new loans. The result has been depressed for three quarters and does not seem to be improving. Households and businesses are increasingly reluctant to borrow at current rates, so they prefer to wait until the cost of money comes down.

But there's more: even Valley National Bancorp is more careful about who it lends money to, and is unwilling to give discounts for customers in a precarious financial situation.

We're a very conservative underwriting standards to begin with, but we look to tighten, especially in certain buckets of our portfolio. So we consistently do that throughout every cycle.

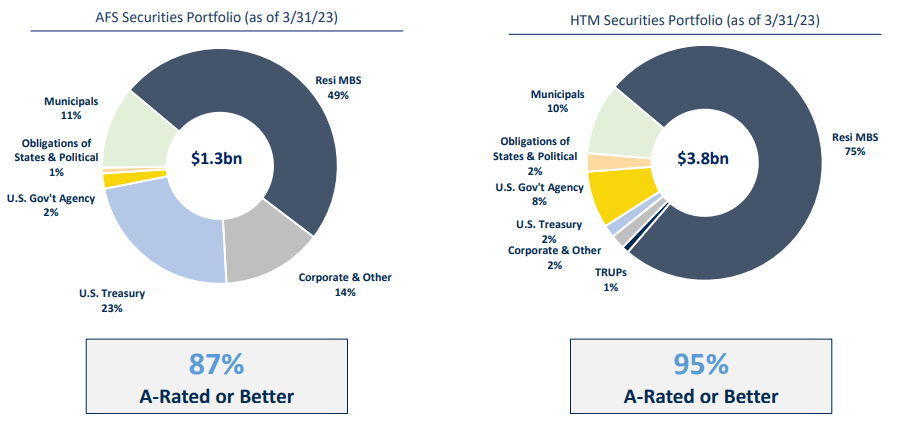

As a final aspect, I want to highlight market risk. As you are aware, many banks are facing a difficult time as rising interest rates have caused huge unrealized losses on their HTM securities. Is this also the case for Valley National Bancorp? Definitely not.

{kind=link}

Valley National Bancorp Q1 2023

The securities portfolio accounts for a modest 8% of total assets and is mostly composed of high quality securities. In short, with $3.80 billion in HTM Securities, I personally would not be very concerned about any unrealized loss. It is a very small share compared to the total assets.

To give you an idea of how low this number is, for Silicon Valley Bank it was 55%.

Final Thoughts

Personally, I find that this bank is going through a difficult time, but then again it is the entire banking industry that is suffering. In any case, based on the current data, I rate this bank positively. The deposit stickiness is good, the net interest income has improved from last year, and the securities portfolio is marginally weighted so there is no risk of incurring large unrealized losses. The area of most concern is how deposit beta will evolve: we know it will increase but not by how much.

{kind=link}

Valley National Bancorp Q1 2023

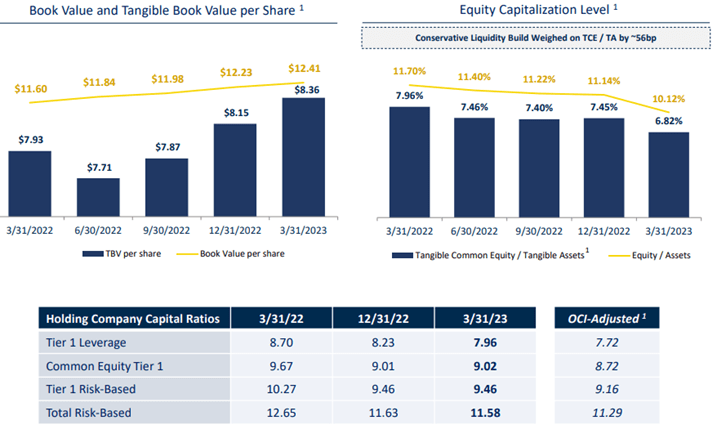

On paper, Valley National Bancorp looks like a bargain, as it fully meets the capital requirements of Basel III and its book value per share continues to grow despite its plummeting price. The current P/B is 0.58x , well below the last 10-year average of 1.16x. Multiplying the latter figure by the current book value per share ($12.41) the fair value of Valley National is $14.39, so it is now highly undervalued. Wanting to be more conservative, multiplying by the tangible book value per share the fair value would be $9.69, still higher than the current price.

Investing now in this bank after such a collapse could prove to be a bargain, but I personally prefer to avoid it, as there is still too much uncertainty about the macroeconomic environment. We have seen how regional banks can find themselves in trouble at any moment, even without having any particular weaknesses. First Republic was only guilty of having too many uninsured deposits, but otherwise it was a very good bank. I recommend reading my recent articles if you are interested in its failure.

In the case of Valley National Bancorp this risk does not exist, but I do not feel confident enough to say that this is the bottom. I am well aware that it is impossible to have perfect timing and buy at the bottom, the point is that I would not be surprised if the stock goes down much further. To invest in a regional bank I need a huge margin of safety, which is not there at the moment.

For further details see:

Valley National Bancorp: Highly Undervalued But Be Careful