VLYPP - Valley National Bancorp: Why I Sold The Series A Preferred Shares

2023-06-09 06:50:02 ET

Summary

- Valley National Bancorp's first quarter earnings showed a reversing trend in net income, despite interest income more than double that of the previous year's first quarter.

- Over $30 billion of the bank's $48 billion loan portfolio is tied up in commercial real estate, with 84% of the commercial real estate portfolio not owner-occupied.

- The bank's high loan-to-deposit ratio and exposure to low interest commercial real estate loans led me to sell their holdings, citing concerns over concentrated risks.

Valley National Bancorp (VLY) has seen its shares beat down by the regional banking crisis. Like many other regional banks, I took a flyer on the bank's Series A 6.25% preferred shares (VLYPP) when they sold off as well. After reviewing the bank's first quarter financials, I believe there was too much risk staying with the bank's 8.5% yielding preferred shares and I opted to sell.

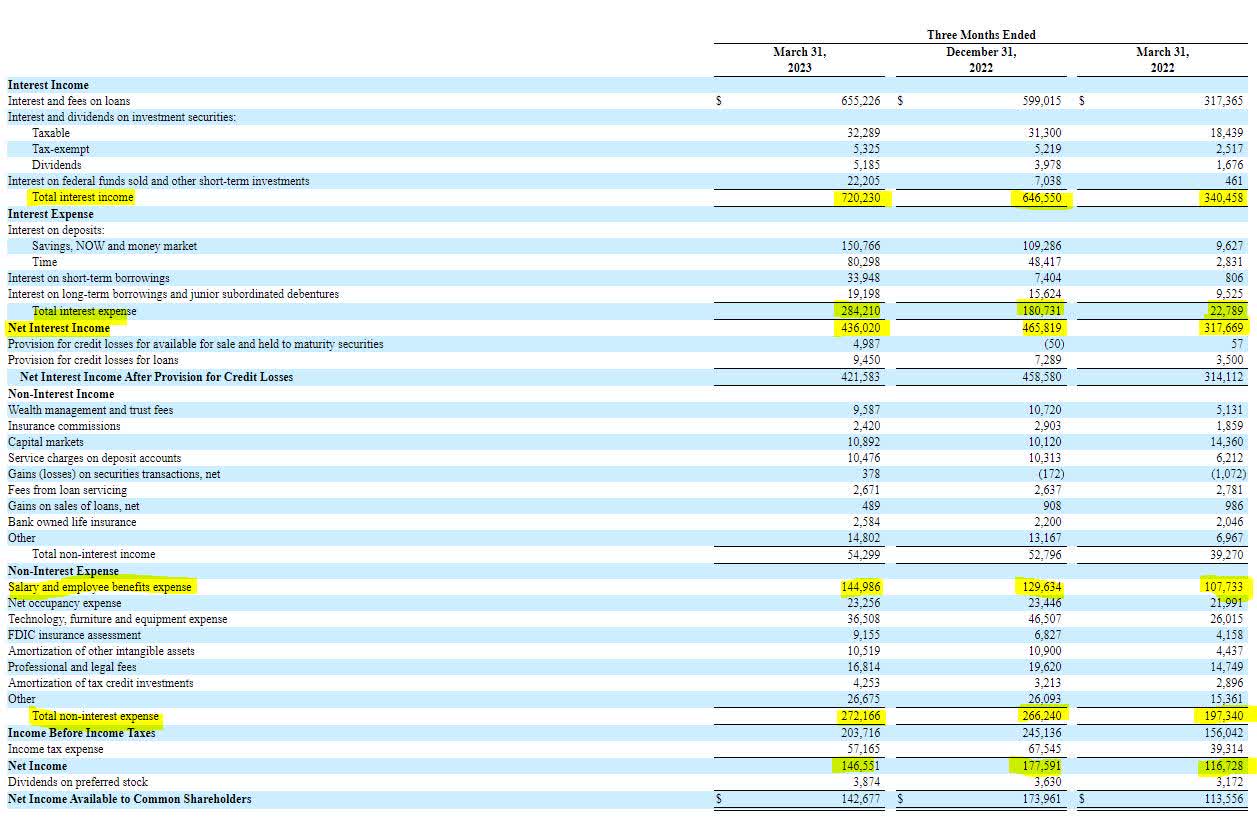

Valley National's first quarter earnings showed a reversing trend in net income. Interest income was more than double what it was in the previous year's first quarter, and despite a large increase in interest expense ($104 million quarter to quarter), net interest income finished the quarter nearly $120 million higher than the first quarter of 2022, but both net interest income and net income slipped by $30 million compared to the fourth quarter, but net income covered preferred share dividends more than 30 to 1.

{kind=link}

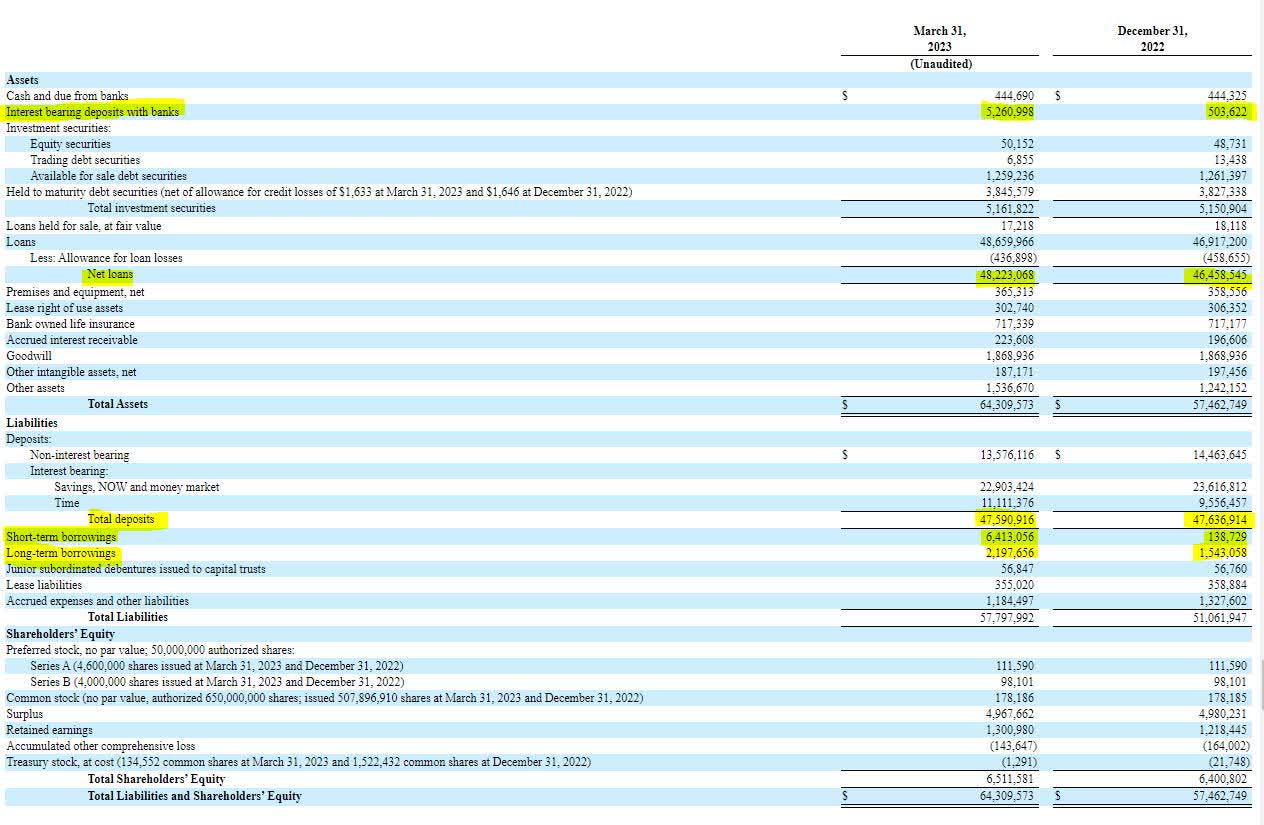

Valley National's balance sheet shows how serious the bank handled the regional banking crisis in March. The bank increased short term borrowing by more than $6 billion and long-term borrowing by $600 million. Most of the borrowings ended up in cash, which went from under $1 billion in December to $5.7 billion at the end of the quarter. Loan activity increased by nearly $2 billion despite deposits remaining flat. Essentially, out of the nearly $7 billion in new borrowing by Valley National, $5 billion went to cash and $2 billion went to loans.

{kind=link}

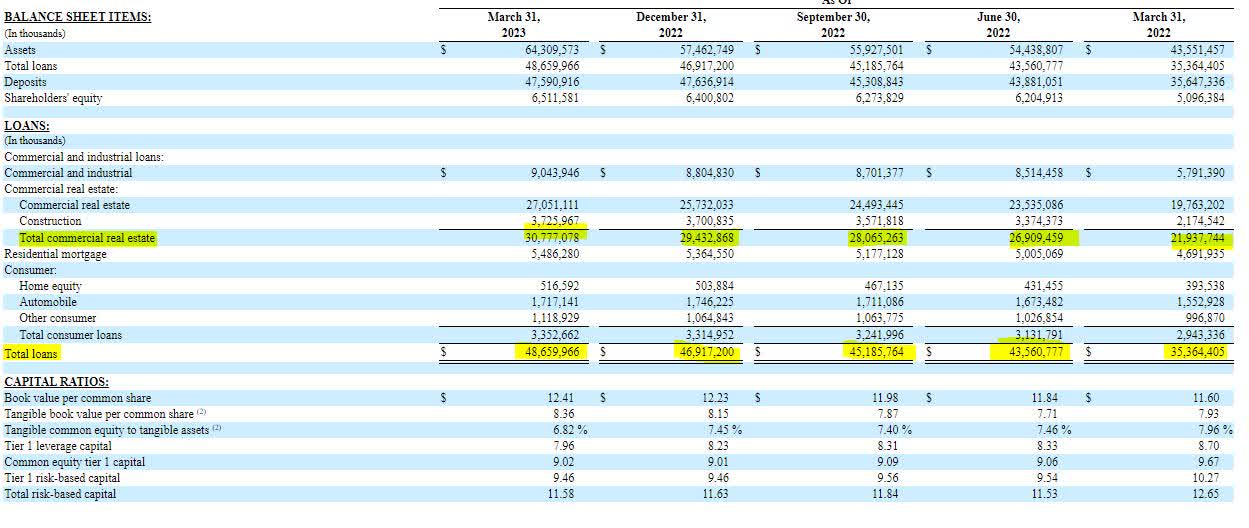

Where I begin to get concerned about Valley National Bancorp is when I dig deeper into the numbers. Over $30 billion of the bank's $48 billion loan portfolio is tied up in commercial real estate. Commercial real estate loans have been receiving a lot of press lately for being problematic. Valley National is quick to point out that within their CRE portfolio, there is diversification between industries and uses, but 84% of the commercial real estate portfolio is not owner occupied, making it easier for the owner to walk away from any underwater loans.

Earnings Presentation

{kind=link}

Another concern I have is the yield on the loan portfolio, currently at 5.48%. While new loan originations have doubled in yield, the volume of new loans is declining. This means the bank is bogged down with lower interest rate loans that would be hard to sell if they needed emergency liquidity. Additionally, by having a heavy exposure to commercial real estate, many of the low interest rate loans made in 2020 and 2021 will be resetting at market rates, creating the higher probability of defaults.

Earnings Presentation

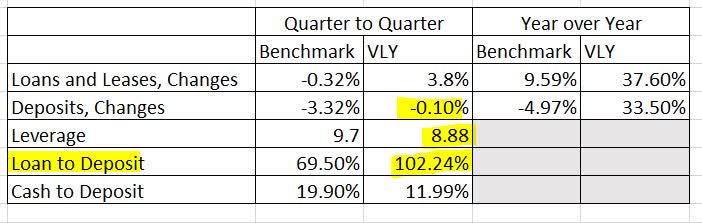

Even if Valley National had higher loan demand, I'm not sure they would be able to underwrite many more new loans. The bank's 102% loan to deposit ratio is at the top end of the industry, and essentially means that any new lending done by the bank will have to be funded by non-depositor borrowing. While Valley National's leverage is below the industry average, there's still not enough cushion to protect the balance sheet from any earnings fallout related to its loans.

{kind=link}

Valley National's exposure to low interest commercial real estate loans and its high loan to deposit ratio were enough for me to sell my holdings. There are several other regional banks offering comparable yield preferred shares that have a lower loan to deposit ratio or a more diversified lending portfolio. Valley National Bancorp's risks are too concentrated for my liking.

For further details see:

Valley National Bancorp: Why I Sold The Series A Preferred Shares