VLOWY - Vallourec: Remains A Buy Despite Reaching 52-Week Highs

2023-12-26 01:03:30 ET

Summary

- Vallourec had a seesaw 2023 with negative oil and gas macro counteracting positive fundamental news but will end the year close to its 52-week highs.

- The international demand for oil country tubular goods remains strong while there are signs that North America has bottomed.

- Vallourec increased its guidance several times during the year and is now projecting debt-free status and generous cash returns as of 2025.

- You still have time to front-run the shareholder returns as they don't yet appear fully priced in.

Investment thesis

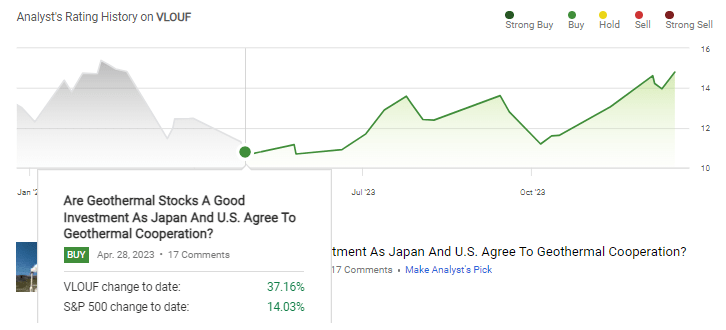

Vallourec S.A. (VLOUF) is a provider of premium tubulars for oil and gas and industrial applications. VLOUF has done quite well since I previously wrote about it back in April:

{kind=link}

However, the share price appreciation doesn't have much to do with Vallourec's long-term new energies promise (specifically, geothermal) I highlighted before but is simply driven by its bread-and-butter oil and gas business.

The resilience of the oil and gas capex cycle in international markets while North America appears to have finally bottomed have led to new sales orders and upward guidance revisions. This has started trickling down to the stock price, as analysts now expect Vallourec to be nearly debt free by 2025 and initiate a sizable dividend.

While Vallourec is trading close to its 52-week highs, which may cause some to conclude the opportunity is gone, I think the recent momentum is just the start of the re-rating process. VLOUF is on track to become a cash cow by 2025 and the market will likely front-run the news during 2024.

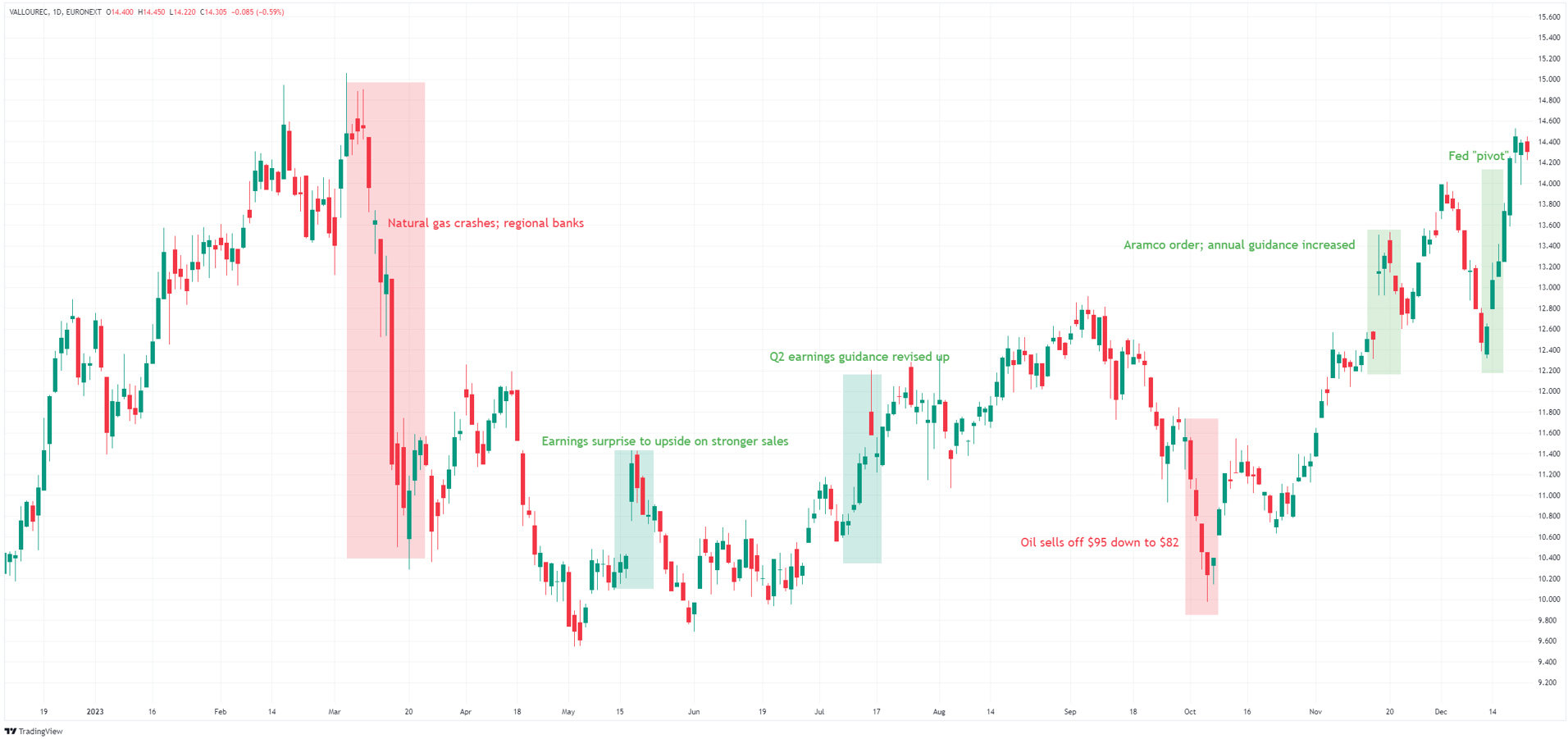

A year of positive surprises

Vallourec will end 2023 close to the February highs, so at first glance it may appear not much progress was made. However, in my view, the selloffs were mostly macro driven and didn't have much to do with the business; on the other hand, the fundamental news usually pushed the stock up:

{kind=link}

There were a couple of guidance increases from management along the way, and a major highlight were the additional orders Vallourec scored with Saudi Aramco:

These orders total more than 300m dollars and supplement Vallourec's recent successes in the region. They cover the supply of proprietary steel grade casing and tubing for high-pressure environments, threaded with premium VAM connections. These orders are incremental to the volumes to be delivered under the company's 10-year long-term agreement with Aramco.

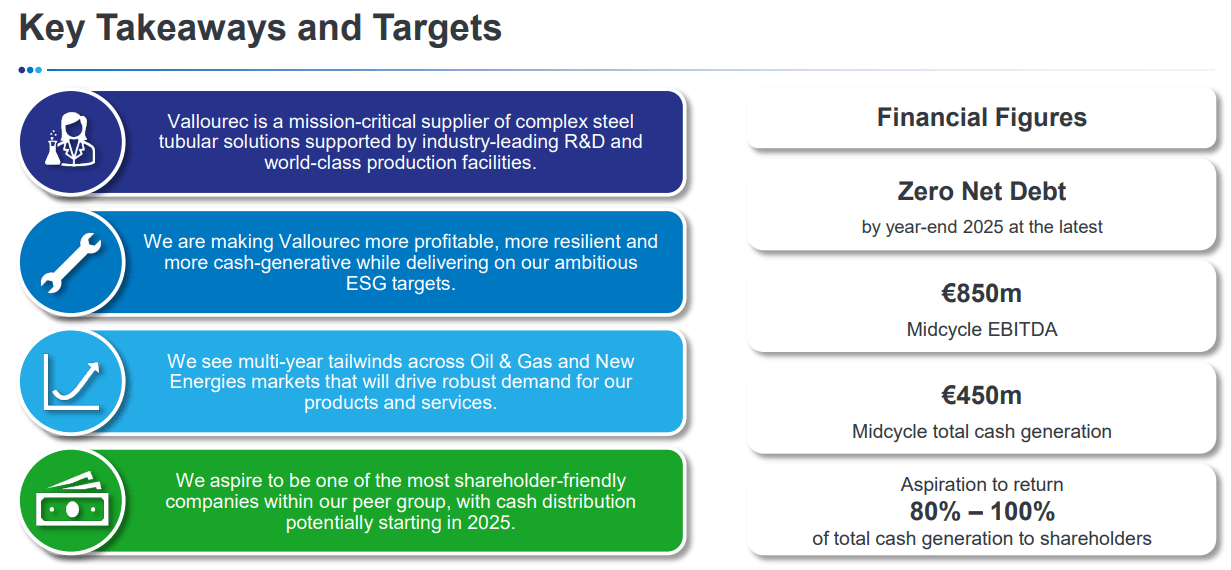

The company now expects to be debt-free by 2025 and initiate a cash return program to the shareholders that will target 80-100% of free cash flow:

{kind=link}

Assuming the midpoint of the targeted distribution range, this implies close to 10% yield on enterprise value.

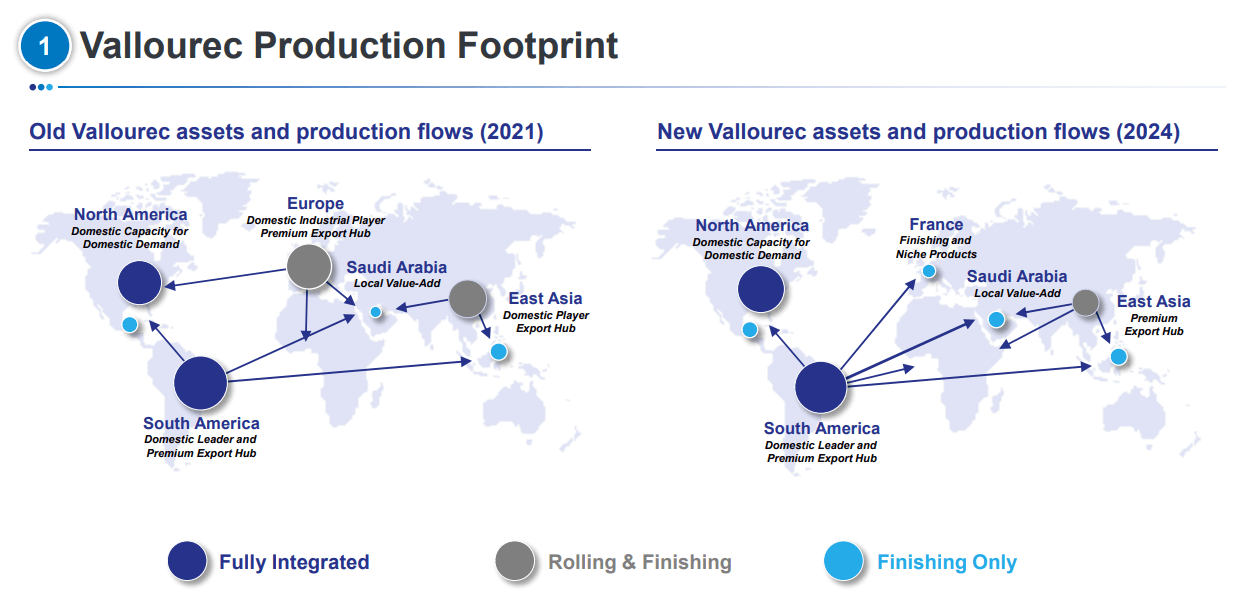

In the meanwhile, Vallourec has also been executing on its restructuring efforts, which saw production shifted from the high-cost France and Germany to Brazil:

{kind=link}

With the rising energy costs in Europe, this makes sense and Vallourec appears to be basically leaving just some finishing activity in France plus, of course, the R&D.

The good news this year also included a rating upgrade by S&P from BB- to BB and Vallourec's 2026 debt appears to be trading at slight premium to par.

The demand from oil and gas is strong

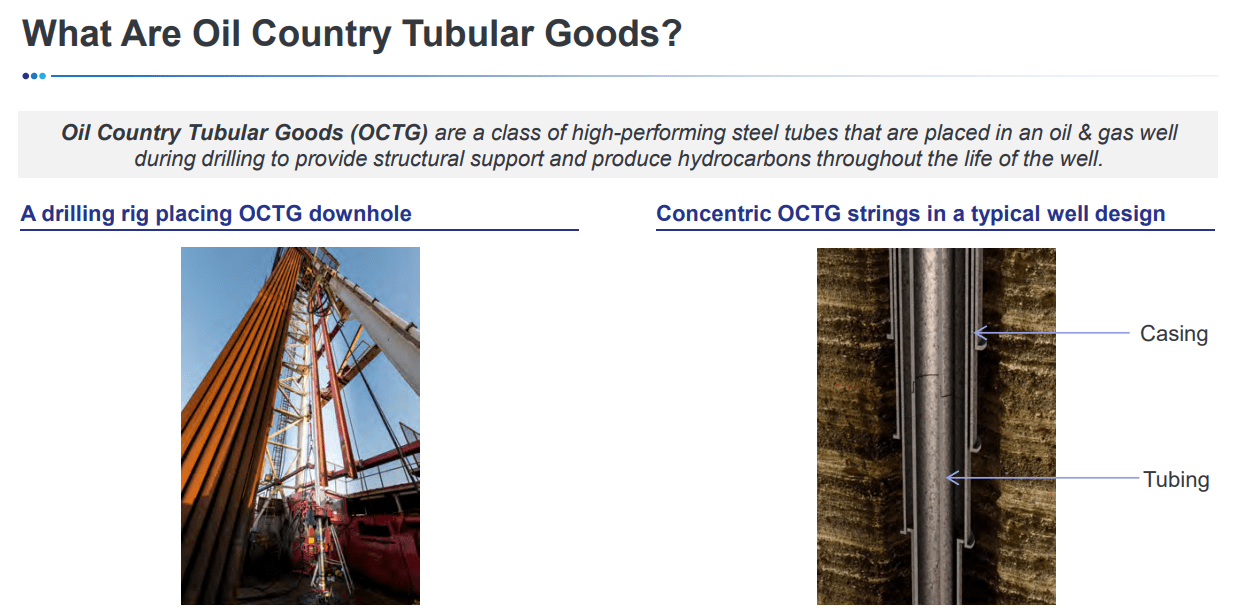

I have written before about Vallourec's potential in the geothermal space, and the company's steel tubular goods also have applications to offshore wind and other renewables. However, for the time being the main product remain the so-called oil country tubular goods (also OCTG), or special pipe used in drilling oil and gas wells:

{kind=link}

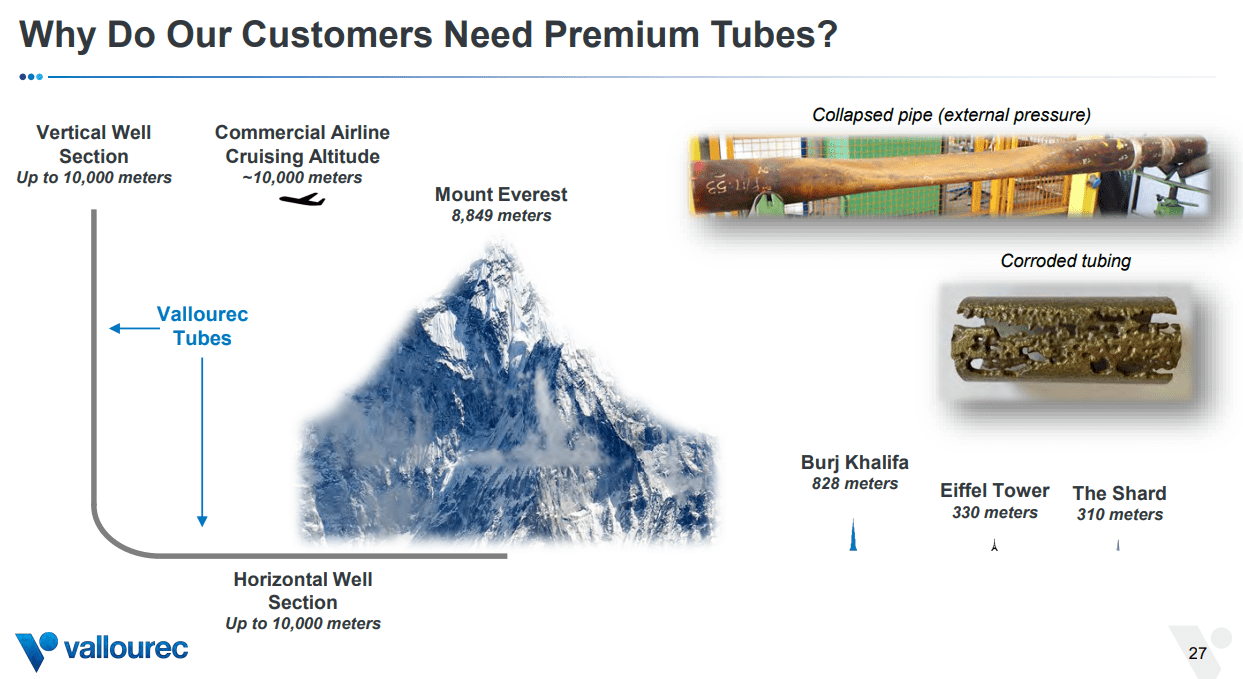

The manufacturing quality is of utmost importance given the application:

{kind=link}

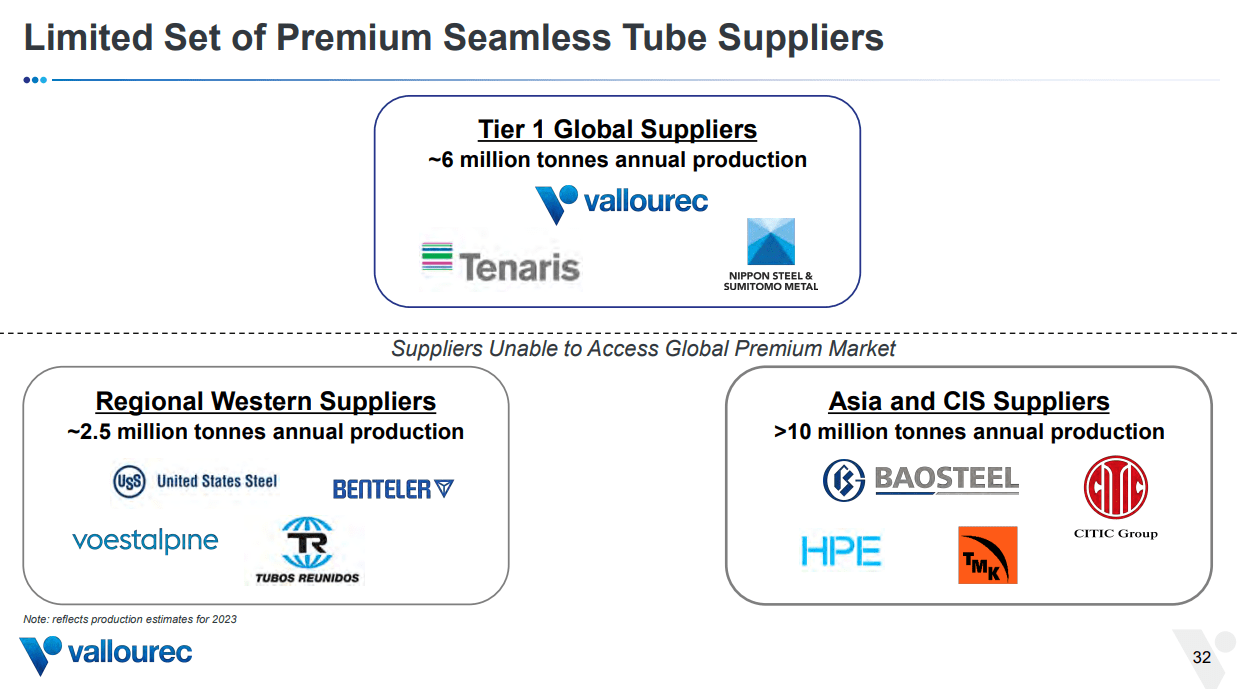

Considering the effort and time it takes to attain the requisite manufacturing excellence, VLOUF has only a handful of competitors, including Tenaris (TS) and the recently acquired United States Steel (X):

{kind=link}

In theory, weak oil and gas prices mean less OCTG demand, but, as I have pointed out multiple times in my oilfield services coverage, the capex cycle in international markets has been very resilient. This been emphasized by industry bellwethers like SLB (SLB) and many others.

VLOUF is no exception, and management commented regarding international markets during the last earnings call :

Onshore and offshore drilling activity have remained stable at healthy levels for the past several months. In addition, there remains positive tailwinds in offshore markets driven by global deep water projects and robust shallow water activity in the Middle East. Offshore developments tend to demand higher-end tubes, so continued growth in this market will be positive for Tier 1 players like Vallourec.

Much of the international capex is driven by national oil companies like Aramco or Petrobras (PBR), which are both VLOUF customers. These players are fulfilling long-term production growth mandates and care less about oil prices in the short term, which is why the OCTG orders remain steady.

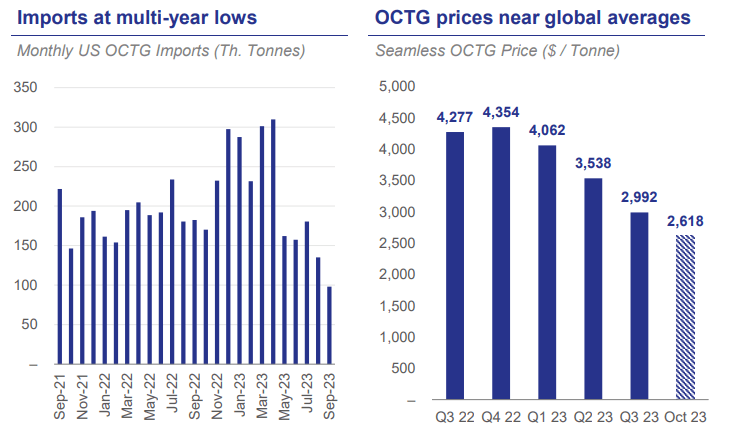

In contrast, North America, where VLOUF and others faced weakness in 2023, is much more responsive to demand and the weak oil and gas prices pushed US OCTG imports to multiyear lows, which has also impacted pricing:

{kind=link}

However, Vallourec's management believes North America has already seen the bottom:

We agree with the market consensus that there will be a recovery in drilling activity from here, given supportive oil and gas prices and favorable customer drilling economics. Following exceptionally high OCTG imports in the fourth quarter of 2022 and first quarter 2023, imports have now fallen to multiyear lows, extending the trend observed through the summer. Domestic shipments also fell in the third quarter. Distributor inventories have been declining steadily for several months now.

Recent reporting from the US Department of Commerce suggests that October 2023 imports of OGTC already saw a large increase of 123% from the prior month of September, although year-on-year the imported volumes were still down 19%.

Valuation and risks

A report from Société Générale published just before the Q3 earnings came up with a EUR 25 target, which implies significant upside to the current EUR 14 price. Although SG's target is based on a DCF model, it isn't hard to rationalize it with a simpler multiples approach.

Assuming management's EUR 850 million mid-cycle EBITDA (which, by the way, is lower than professional analysts' 2024-5 projections of EUR 1.0-1.1 billion), a 6.5x multiple implies a EUR 5.5 billion enterprise value. If you do the math, this is 70% upside for the equity, or EUR 24 per share, close to the SG target.

On the risk side, I don't think fundamentally too much will happen. S&P doesn't issue easily BB ratings to mid-cap oilfield manufacturing companies. However, the association with the oil and gas industry means that any macro-driven selloff will likely continue to impact VLOUF.

Bottom line

Historically, Vallourec may have not had the best track record in generating shareholder value, but lately the company has been making good moves and is on target to become a cash cow by 2025. The stock price doesn't fully reflect this yet, so I expect more repricing in 2024 as the market front runs the commencement of the cash returns.

For further details see:

Vallourec: Remains A Buy Despite Reaching 52-Week Highs