MSGS - Valuing The Pieces Of Madison Square Garden Entertainment Before Its Upcoming Spinoff

Summary

- Madison Square Garden Entertainment is being split into two pieces via spinoff in an attempt to unlock shareholder value.

- I examine the various components of MSGE and attempt to assign a value to each ahead of the spinoff.

- I take a look at the Dolan family's influence on the path of their various companies.

- I finish with an assessment of what I expect each stock to be worth post-spin and how I'm playing the upcoming spin-off.

What's happening?

Madison Square Garden Entertainment ( MSGE ) is being split into two. The new MSGE and Madison Square Garden Sphere (SPHR). This is being done as a tax-free spin-out of the new MSGE from the old MSGE. The old MSGE will then be renamed to SPHR.

I think this is a particularly interesting transaction since the current iteration of MSGE is complicated, with several assets I'd be interested in owning. Madison Square Garden, the upcoming sphere, and the Tao hospitality group are all compelling one-of-a-kind assets.

The simplification of the equity structure could be a catalyst to realize value. Even if the current valuation doesn't look compelling stocks sometimes have price dislocations post-spin-off so doing our homework now can help us know if a bargain is available later.

The logic behind the MSGE spin-out

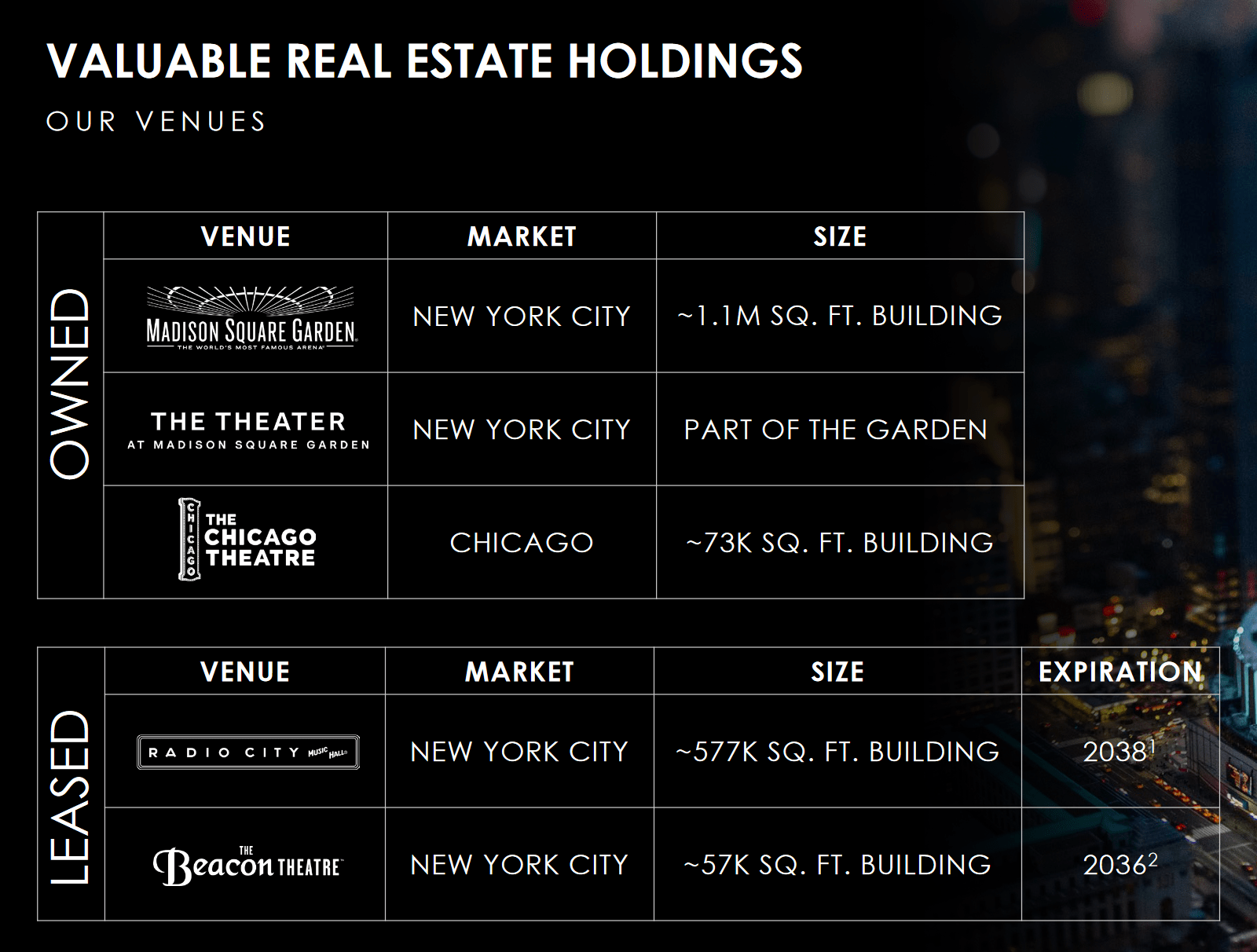

MSGE is being spun off as the "good" company. It contains the assets most investors seem to like. It contains Madison Square Garden along with MSGE's other owned and leased entertainment venues. The hope is that by spinning out these easy-to-understand assets investors will be willing to apply an infrastructure like multiple to them.

{kind=link}

This is appealing since instead of having to do a sum of the parts analysis investors can do a cash flow analysis slap a multiple on it and be done with it. So since that is the goal let's try it out. Find below my simple cash flow breakdown along with an explanation. This is based on fiscal 2023 guidance that was provided in MSGE's recent investor presentation on the spinoff and the company's S-10 on the same subject. MSGE fiscal year ends in June so we are currently halfway through. I'd expect this means management's recent guidance is fairly accurate. All numbers are in millions of dollars.

| cash operating income |

| 150 |

| The midpoint of management's guidance. This is cash flow from operations less interest, taxes, one-time expenses, and working capital changes |

| maintenance capex |

| 19 |

| Average of last 3 years of capex for the entertainment division (2020, 2021, 2022) |

| cash flow to debt |

| 131 |

| Cash operating income less maintenance capex |

| interest expenses |

| 61 |

| $675 million in debt at a 9% interest rate |

| taxes |

| 0 |

| Per guidance, MSGE won't be a meaningful taxpayer until 2027 |

| free cash flow to equity |

| 70 |

| Cash flow to debt less interest and tax payments |

| share based comp |

| 20 |

| Per management's guidance |

| owner's earnings |

| 50 |

| Free cash flow to equity less share-based comp |

From here I applied a 6% growth rate to cash operating income, maintenance, capex, and share-based comp. Between 2019 and 2023 cash operating income grew at a 15% CAGR but I don't feel comfortable giving them that kind of credit going forward. I also made the company have to start paying taxes in year 4 per management's guidance.

MSGE discounted cash flow analysis (Author's work)

{kind=link}

If you don't like discounted cash flow analysis you can slap a 20 multiple on 50 million in owner's earnings and come up with a pretty similar valuation. I believe MSGE equity is worth $900-1000M .

Dealing with a large debt burden

MSGE comes burdened with 675 million in debt. The company's indication seems to be that its main objective post-spin will be to deleverage the balance sheet. This seems wise since interest payments are currently eating up a larger percentage of its cash flows.

The debt is floating rate. The exact interest rates are a bit complicated but I believe it can be simplified down to being about SOFR plus 3.5% currently. The choice to go with a 100% floating rate interest seems quite stupid to me. Maybe it's just hindsight bias, but the loan began in June 2022 interest rates should have been top of mind. In addition none of MSGE's cash flows benefit from rising rates so borrowing entirely at a floating rate creates a mismatch.

I'd also note that the crown jewel of the stock Madison Square Garden itself is not encumbered by the loan. This means theoretically all the other theaters are supporting these loan payments, which makes them look very over-levered. Although I'm not sure how much this matters in practice.

Share-based comp

After breaking down the owner's earnings I was surprised by how much of the free cash flow is being eaten by share-based compensation in 2023. 2023 is not an outlier either, the entertainment division has had share-based compensation expenses over $40M in the each of the last three years. When you are only going to be making about 70 million in free cash flow to equity giving management 20 million in share-based comp just seems greedy.

It feels especially bad when you consider that a lot of the comp is going to James Dolan and his family. The Dolan family already owns over 13% of the economic interest in MSGE. It's not clear why they need to grant so much additional equity in the business to themselves. The Dolan family also controls more than 50% of the voting power in MSGE via special voting shares. Effectively they are the ones deciding how much to pay themselves.

Do MSG spins unlock value?

Over the past few years, Madison Square Garden Sports ( MSGS ) was spun out of MSGE. Then Madison Square Garden Networks ( MSGN ) was merged with MSGE. Now MSGE is being split in two. Separating MSGE from everything else.

Especially concerning in all of this is the merger of MSGN into MSGE. This was done despite protests from many minority shareholders and resulted in a lawsuit . On a recent earnings call management admitted to the merger being motivated by funding the development of the sphere.

we acquired MSG Networks last year. And since that time, that transaction has provided a number of important benefits for us, including significant cash flow, which we've directed towards our Sphere initiative.

I think it's fair to question if these equity spinoffs do anything. The Dolan family still controls all of the MSG companies with their super-voting shares. They've demonstrated they will do what they believe is best for the overall Dolan empire, not any individual equity.

Breaking down Sphere Co

SPHR co will consist of 3 different units: Tao hospitality group, MSG networks, and the MSG sphere itself. These 3 assets don't make a lot of sense together. When the spinoff was originally announced in April MSG networks were going to stay with MSGE. The pitch was that MSGE would contain legacy businesses with stable cash flows while Sphere co would contain "growth" assets. They subsequently decided to add MSG networks to Sphere co and reportedly are looking to sell Tao.

From what I can tell the only thing that ties all three of these assets together is that investors don't seem to like them. MSG networks are viewed as being in terminal decline, the sphere is seen as an inefficient use of shareholder money, and investors struggle to understand the normalized earning power of the Tao group.

So once again we are left doing a sum of the parts valuation.

Evaluating Tao

Tao is reportedly for sale with an asking price of over $500M. The group has been able to operate with full venue capacity for the last twelve months. Although they have struggled with controlling costs, which has affected their profitability. Overall it seems like the last twelve months should give a decent look at what we can expect on a look-forward basis.

| cash operating income |

| 57 |

| Trailing twelve months' cash flow from operations less interest, taxes, one-time expenses, and working capital changes |

| maintenance capex |

| 23 |

| Trailing twelve months capex |

| cashflow to debt |

| 34 |

| Cash operating income less maintenance capex |

| interest expenses |

| 6 |

| 83 million in debt at a 7.2% interest rate |

| taxes |

| 5 |

| Cash operating income less D&A and interest expenses times 21% |

| free cash flow to equity |

| 22 |

| Cash flow to debt less interest and tax payments |

| share based comp |

| 8 |

| Trailing twelve months share-based comp |

| owner's earnings |

| 14 |

| Free cash flow to equity less share-based comp |

It's hard to know how much these owner earnings are worth because this has historically been a fairly unstable business. But it has several strong brands with a demonstrated track record of being able to invest more capital. Tao has slightly over $83M in debt. So to get to the reported asking price of $500M someone would be willing to pay over $400M for the equity. I'd guess that equity is worth somewhere between $200M and $400M. That's a big range but I don't think we have enough data about what this looks like under normal operation to give a more accurate answer. MSGE owns 67% of TAO so let's just say their equity stake is worth $130M-$260M .

Evaluating MSG Networks

A regional sports network MSG Networks is a business that is seen as being in terminal decline. They are attempting to pivot from making money on the cable bundle to a paid streaming app. Here is my look at normalized owner's earnings, all numbers are rounded to millions of dollars.

| cash operating income |

| 158 |

| Trailing twelve months' cash flow from operations less interest, taxes, one-time expenses, and working capital changes |

| maintenance capex |

| 6 |

| Trailing twelve months capex |

| cashflow to debt |

| 153 |

| Cash operating income less maintenance capex |

| interest expenses |

| 68 |

| $973M at a 7% interest rate |

| taxes |

| 16 |

| Cash operating income less D&A and interest expenses times 21% |

| free cash flow to equity |

| 69 |

| Cash flow to debt less interest and tax payments |

| share based comp |

| 9 |

| Trailing twelve months share-based comp |

| owner's earnings |

| 60 |

| Free cash flow to equity less share-based comp |

Once again this business is being hurt by a large debt burden that is all floating rate. The cash this business is generating is declining and due to the large and increasing interest charges, we are seeing negative leverage. The debt will also need to be re-financed in 2024 which may be challenging given the deteriorating financial performance. From Fiscal 2018-2022, cash operating income was cut by 45%. If this rate of decline continues the business will be generating no owner's earnings within 5 years unless interest rates drop substantially. I'm even being kind to their earning power here since I'm using a TTM number, I should be reducing this by some expected decline percentage.

I applied an expected decline of 11% to cash operating income, maintenance capex, D&A, and share-based comp to calculate the following DCF. Note I assigned no value to any years beyond year 5 since per this model only minimal cash flow will be generated thereafter.

Discount cash flow analysis of MSGN (Author's work)

This model is once again overly simple and a change in interest rates or the success of a DTC business could make this look quite different. But I feel it's about right. I assign the MSGN equity a value of $150M .

Evaluating the sphere itself

Calling the Sphere a debacle is probably an understatement. Originally projected to cost $1.2B and forecasted to open end of 2020 it is being delivered almost 3 years late and over a billion dollars over budget. The head of the project was recently let go .

When asked about returns on this investment management has deflected. The fact that management has not been willing to give any concrete numbers for profitability this close to launch doesn't bode well in my opinion. Some leaks have surfaced giving us some clues about potential revenues, but we are still left with a lot of guesswork.

- The Sphere is projected to attract 3-4 million customers for made-for-the-sphere movie experiences in the first year. Assuming $30 a customer on ticket sales and concessions this is $90-120M in revenue from movies.

- They expect to host 40-80 concerts a year. With 17500 seats I guess they make 2 Million in revenue per concert although much of this will go to the artist. That is $80-160M in revenue.

- Finally naming rights and advertising, they are reportedly seeking $50M million in naming rights for the sphere. They should also have opportunities for smaller advertising deals on the huge sphere display screen. Let's say this brings in $25-75M in revenue.

That brings us to $195M-$355M in revenue. MSGE converts revenue to cash flow from operations at a high teen rate of 17-18%. The sphere's cash flow mix looks to be similar to MSGE. This leaves $33M-$64M in cash flow from operations from the sphere.

For a project that is costing over $2.2B and has taken almost 5 years to complete this would be a disastrous outcome. I'm entirely open to the idea I'm missing something here but until management provides more clear guidance on what they are expecting profitability wise I'm forced to model based on rumors.

The sphere carries $275M in debt at a floating rate. At current interest rates will the debt cost is around 10%. If we assume the high end of my estimate after subtracting interest payments we are left with around $30M in owner's earnings. If we assume a 20 times multiple, we are left with an equity value of $600M for the sphere.

Putting it all together

We have the following value estimates for equity based on cash flows.

| MSG Entertainment |

| $900-1000M |

| MSG Networks |

| $130M-$260M |

| Tao entertainment |

| $150M |

| MSG sphere |

| $600M |

This gives us a total equity value of $1,780M-$2,010M. Given the current market cap of $2,120M, I find the company to be fully valued to slightly overvalued.

The company does have almost $400M on the balance sheet in cash. By my calculations, this will all be needed either to complete the sphere or as working capital in the various businesses. It also has some equity investments on the balance sheet in the form of ownership in DraftKings ( DKNG ) and Townsquare ( TSQ ).

There are a lot of variances here. As mentioned throughout the article current MSGE has $18B in floating rate debt on the balance sheet if interest rates drop things could look better. There are a lot of unknowns about the future profitability of MSG networks and the sphere. If the sphere ends up being utilized at a higher rate than current rumors or if MSG network can stop its decline things will look more interesting.

In terms of stocks post spin:

- MSGE is fairly straightforward, I'd assign it a fair value market cap of $900M-$1000M .

- SPHR will continue to own 1/3 of MSGE post-spin-off. So I'd expect SPHR to be worth somewhere around a market cap of $1.1B-1.4B .

How I'm playing the spin

For now, I'm not going to take any stake in the equity. But I'll be watching the components post-spin. I wouldn't mind owning one or both of these if they trade at a large discount to my current estimate. If management provides updates and guidance on how they expect the sphere to perform I could also update my valuation to reflect the additional insight.

In particular, I think any bad news related to the sphere could cause a large sell-off in SPHR. It's pretty clear investors already do not like the sphere and it has been plagued by bad news from the outset.

The fact that SPHR will own 33% of MSGE may also cause some overhang on MSGE. Management has indicated that SPHR may sell its MSGE block to provide liquidity if needed. If liquidity is not needed it may be available in an exchange offer.

For further details see:

Valuing The Pieces Of Madison Square Garden Entertainment Before Its Upcoming Spinoff