TSM - Valuing The SMH ETF Using Micron's Earnings

2023-03-30 12:36:08 ET

Summary

- Micron's latest quarter earnings report provides us with a prelude as to what can happen in the semiconductor industry.

- To make my point, I use VanEck's SMH together with the fact that memory and processors are intricately linked due to their use in electronic devices as components.

- There are certainly generative AI-related prospects as I elaborate upon, not only for Nvidia but also for Intel, Micron, and AMD.

- While recession risks have now increased, tech may constitute a beacon of hope, with one of the reasons being that the Fed may have to be less aggressive in tightening monetary policy.

- Another reason is that SMH's positives outweigh the negatives, but investors are cautioned that volatility should reign.

Micron's ( MU ) second-quarter (Q2) financial results of fiscal 2023 were bad as it missed both revenue and earnings estimates, but, one has to remember that market conditions are challenging. However, its CEO stated that customer inventories are improving and anticipates a gradual improvement in the demand-supply equation.

Using the VanEck Semiconductor ETF ( SMH ), my objective with this thesis is to assess whether this optimism is justified and can reverberate across the semiconductor industry. For this matter, not only Micron reports earnings before other SMH's holdings, but its memories are intricately linked to Intel or Nvidia's ( NVDA ) chips when it comes to manufacturing electronic equipment as this thesis will elaborate upon.

Looking at the price action, investors will note that Micron's stock has weighed on the ETF's share price as the memory and storage areas of the semiconductor industry faced their worst downturn in the last 13 years.

To start with I show that Micron is not alone in showing optimism.

Micron's Memory Linked to Other SMH Holdings

Some will remember that at the time of publishing its annual results in January and despite the slumping memory market, which forms the bulk of its chip business, Samsung ( SSNLF ) chose to maintain its investments in semiconductors in 2023.

Coming from the Korean electronics giant, which is also the world's number one in semiconductor production, this is indeed positive. Noteworthily, SMH's holdings do not include Samsung and only 4.22% of its overall weight is dedicated to Micron as pictured below.

SMH Top Holdings (www.vaneck.com)

However, memory chips cannot be consumed by electronic equipment manufacturers on a stand-alone basis, be it for making PC, servers, automobiles, or any other devices.

Instead, the memory is just one of the components used together with processors, and others to fabricate printed circuit boards. Of course, there is a difference between their degree of utilization which depends on the type of equipment being manufactured and the automation level the designers want to achieve. For example, a toaster makes use of basic control chips compared to advanced processors and memory chips for an intelligent robotic vacuum cleaner, not to mention electric vehicles which in addition to the energy savings aspect incorporate communication devices from the likes of Broadcom ( AVGO ).

Coming back to Micron, the sluggishness forced it to reduce production capacity, in order not to see a further increase in inventory, but according to the CEO, this may have peaked in Q2, as measured by the Days of Inventory Outstanding. He even went on to affirm that the company was close to sequential revenue growth, but without precisely indicating when. If this was to happen the third quarter would be the first quarter of growth since the March 2022 quarter.

Now, for this purpose, it can rely on the competitiveness of its products which can also be attractive from the efficiency viewpoint. Here, I have in mind the 1-beta DRAM memory chips used in smartphones which bring 35% more capacity and 15% improvement in power efficiency over the previous generation. Now, smartphones also need miniature but powerful processors designed by the likes of Qualcomm ( QCOM ).

However, the device market should continue to regress in 2023, namely by 4% after cratering by 11% in 2022 according to data by Gartner. The research firm also states that the PC market will decline by about 5%, but that inventory levels will normalize in H2-2023. This gives some credence to the statement by Micron's CEO that "PC inventories are meaningfully better".

Still, as per the deep blue chart below, after slumping steeply from the middle of last year, Micron's quarterly sales have deteriorated less rapidly in its latest reporting quarter.

In comparison, SMH's other holdings have been impacted to a lesser degree and could produce positive surprises, as, according to some Wall Street analysts, after a deeper-than-expected downturn, recovery may be approaching.

Based on this optimism, stocks posted gains of up to 7.85% on March 29 as pictured below.

The Worst May Be Over and Opportunities in AI

Pursuing on a positive note, the data center market should continue to grow by 10% per year till 2030 according to data by McKinsey . This prediction made on January 17 does not include generative AI which has seen renewed interest following the advent of the stable version of ChatGPT by Open AI in March and has been adopted by Microsoft ( MSFT ) for its Bing search engine.

In this respect, compared to a server used for processing normal IT loads, one used for AI requires eight times the DRAM capacity as well as three times the amount of NAND.

In this respect, Micron has developed the higher density DDR5 which is required by both Intel's ( INTC ) Sapphire Rapids and made by Advanced Micro Devices ( AMD ) Genoa processors in servers which allows applications to run faster. Therefore, with more interest in AI, not necessarily the recent Generative flavor, but the more traditional ones like Analytics AI and Recommendation AI, there should be more sales of processor and memory chips, with opportunities possibly materializing in H2-2023 or later.

Furthermore, in graphics, the company's 16-gigabit G6X has recently been launched by Nvidia in its RTX 4070 Ti card, with demand expected to be stronger in H2-2023. Now, Nvidia is not only a graphics card supplier but also a key stakeholder in graphics processing units or GPUs with its Ampere Tensor Core A100, which is the foundation for Microsoft Azure intelligence infrastructure used by OpenAI.

Looking deeper, in addition to Nvidia, SMH's other holdings could also benefit. In this respect, for a Generative AI tool like ChatGPT, in addition to the training part where GPUs are used, there is the inference part where Intel's GPU can be used. For this matter, Intel has the Hanana Gaudi 2 running inference faster than the A100 by 20%. Now, with generative AI costing millions of dollars to run, the cost factor becomes important, and, going forward, it is unlikely for big companies which want to implement their own private generative AI (in order not to have their data in the public domain) to do so by choosing a mix of suppliers, all forming part of SMH's ecosystem.

Continuing with a dose of realism, these are uncertain times thereby warranting an assessment of the risks.

Uncertainty impacting Chip Equipment Makers

Now, after a period of oversupply has impacted the demand-supply equation, there is normally a cut in CapEx throughout the semiconductor industry, as in 2013 . This time, with the exception of Samsung, SK Hynix, Kioxia, and Micron all reduced investments. Thus, for fiscal 2023, the U.S. company will reduce investment, by more than 40% compared to fiscal 2022, out of which WFE or Wafer Fab Equipment used to manufacture chips would be axed by 50%. While this augurs well for Micron's cost optimization efforts over the short term, it also implies fewer purchases from semiconductor equipment manufacturers like Lam Research ( LRCX ), ASML Holding N.V. ( ASML ), Applied Materials ( AMAT ), and KLA Corp. ( KLAC ).

I further confirm this negative outlook from data by semi.org which expects fab equipment spending for 2023 to decline by 22% YoY before rising again next year. Factors that explain this are a reduction in demand namely for consumer and mobile devices, recessionary concerns as well as constraints in selling certain equipment permitting the production of advanced nodes to China.

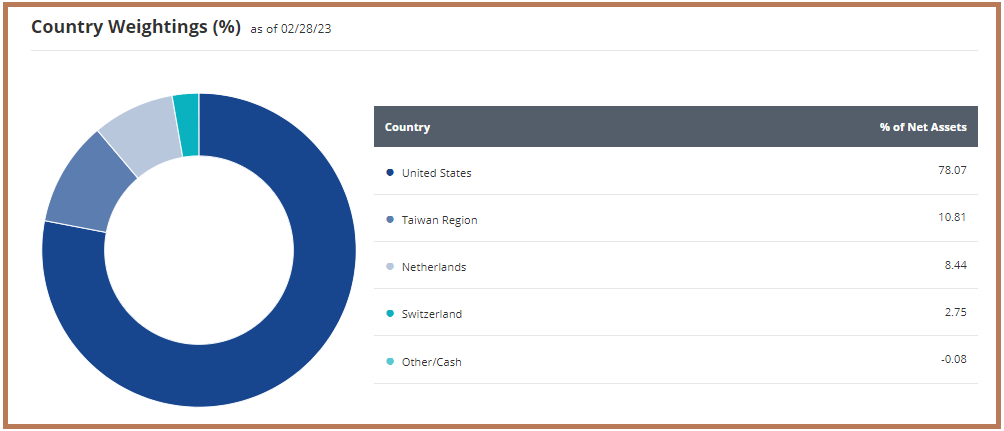

Now, while none of SMH's holdings operate in China, they certainly do business with that country, and issues around Taiwan can fuel geopolitical tensions with the United States.

Country Weightings (www.vaneck.com)

{kind=link}

As SMH's second-largest holding, Taiwan Semiconductor ( TSM ), it does not manufacture chips for Micron which has its own plants, and as shown by the above revenue chart, has not suffered from a slump. One of the reasons for this is its huge backlog, but, aligned with Gartner's estimates that overall chip revenue will regress by 3.6% in 2023 (compared to 1.1% growth in 2022), it announced that it would lower spending during fourth-quarter results in January. However, any AI-related pickup in server demand would certainly be beneficial to the stock as a contract manufacturer of chips designed by U.S. companies.

Conclusion

The prospects are certainly here, but, it would be foolish to ignore that recession risks have gone up now that cracks have started to appear along the liquidity front as interest rates have gone up resulting in the devaluation of the long-term treasuries banks hold as part of their assets. To stop these cracks from turning into structural damage to the economy, the Federal Reserve may have to tighten monetary policy at a less aggressive pace as it fights inflation. Now, lower rates imply cheaper borrowing costs which are good for tech to drive their revenue growth and above-average valuations.

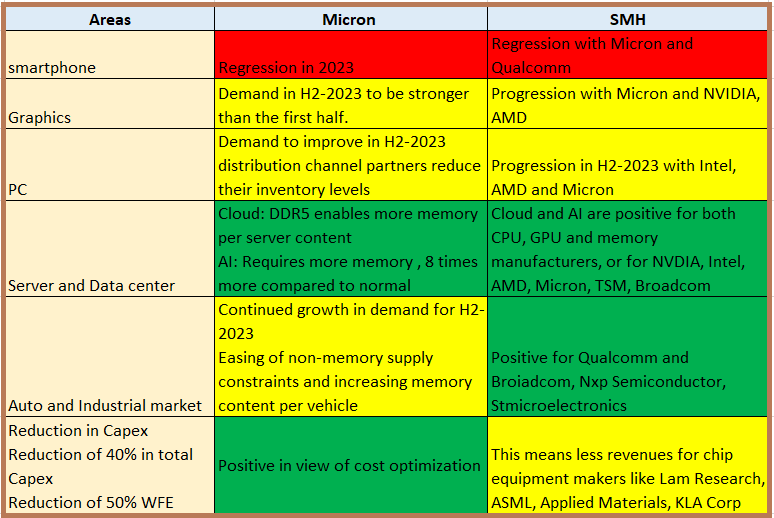

In this case, in a world where more cyclical names and consumer discretionary suffer, tech can appear as a beacon of hope, but, coming back to basics, in this case demand-supply, bear in mind that most of the demand for Micron should come only in the H2-2023 as illustrated in the table below.

Table showing how different areas impact Micron, and SMH, prepared with data from (www.seekingalpha.com)

{kind=link}

Also, with some areas like PC and smartphones still to reach bottom, DRAM and NAND sales will take time to pick up, signifying that if you are looking for a sustained stock price rebound, you probably need to hold Micron for another six months. Also, since the company had to " reduce the price to remain competitive", it does not have the pricing power to increment revenues in a stagflation environment.

On the other hand, for SMH, its approximate 25% combined exposure to TSMC and Nvidia is certainly positive, as it helps offset 17% of the ETF's weight dedicated to chip equipment makers (shaded in yellow in the table above). There are also AI-related opportunities. Thus, I have a buy rating, and after being down by nearly 10% as per the introductory chart, it could climb to the $274 (261 x 1.05) level based on its share price of $261 appreciating by just 5%. It charges fees of 0.35%, but, with only 25 holdings , the ETF carries high concentration risks, implying volatility.

For further details see:

Valuing The SMH ETF Using Micron's Earnings