VVV - Valvoline: A Well-Oiled Machine

2023-09-19 11:15:29 ET

Summary

- Valvoline's history of same-store sales growth and high ROIC indicates that it is a high quality business.

- If the company is able to meet management's long-term growth and margin guidance, its stock looks undervalued.

- Given its past results and management's guidance, I am assigning the stock with a $45 price target and a buy rating.

- Risks include poor execution of the growth strategy due to Valvoline's executive incentive compensation philosophy, and terminal value risk due to the global shift to electric vehicles.

Valvoline Inc. ( VVV ) has been a solid business over time despite its stock not reflecting that quality since the company was separated from Ashland Inc. ( ASH ) in 2016. The business has also undergone some large changes recently with the sale of its Global Products segment and the departure of its long time CEO Sam Mitchell. What will these changes mean for the stock going forward? The management team is touting that the new look Valvoline will be a high growth, high margin, and high ROIC company due to its sole focus on its retail business. I am inclined to believe that this will be the case, and I think that the stock is at a favorable valuation to make that bet.

{kind=link}

The stock doesn’t look cheap at first glance, but a deeper look into the earnings power of the business paints a different picture. The company’s shareholder friendly capital allocation policy that culminated in a recent Dutch tender in which the company used a bit over $1 billion from the proceeds of the Global Products sale to repurchase 27 million shares, seems to show that Valvoline’s management team understands that the earnings power of the business is being overlooked by the market.

If Valvoline manages to meet its long term growth and margin guidance, the stock looks like it is quite undervalued. However, what makes the stock especially appealing at its current valuation is that, even if the company misses those expectations, the stock looks about fairly valued. This should provide a bit of a margin of safety for investors if things don’t go as planned for the business.

I am initiating coverage with a buy rating and a price target of $45 based on my estimate of Valvoline’s intrinsic value, and my estimate of FY2024 normalized cash earnings per share of $2.17 and a 20x multiple. This report will provide more detail on the reasoning for my price target along with an overview of the business and its past financial results.

Business Overview

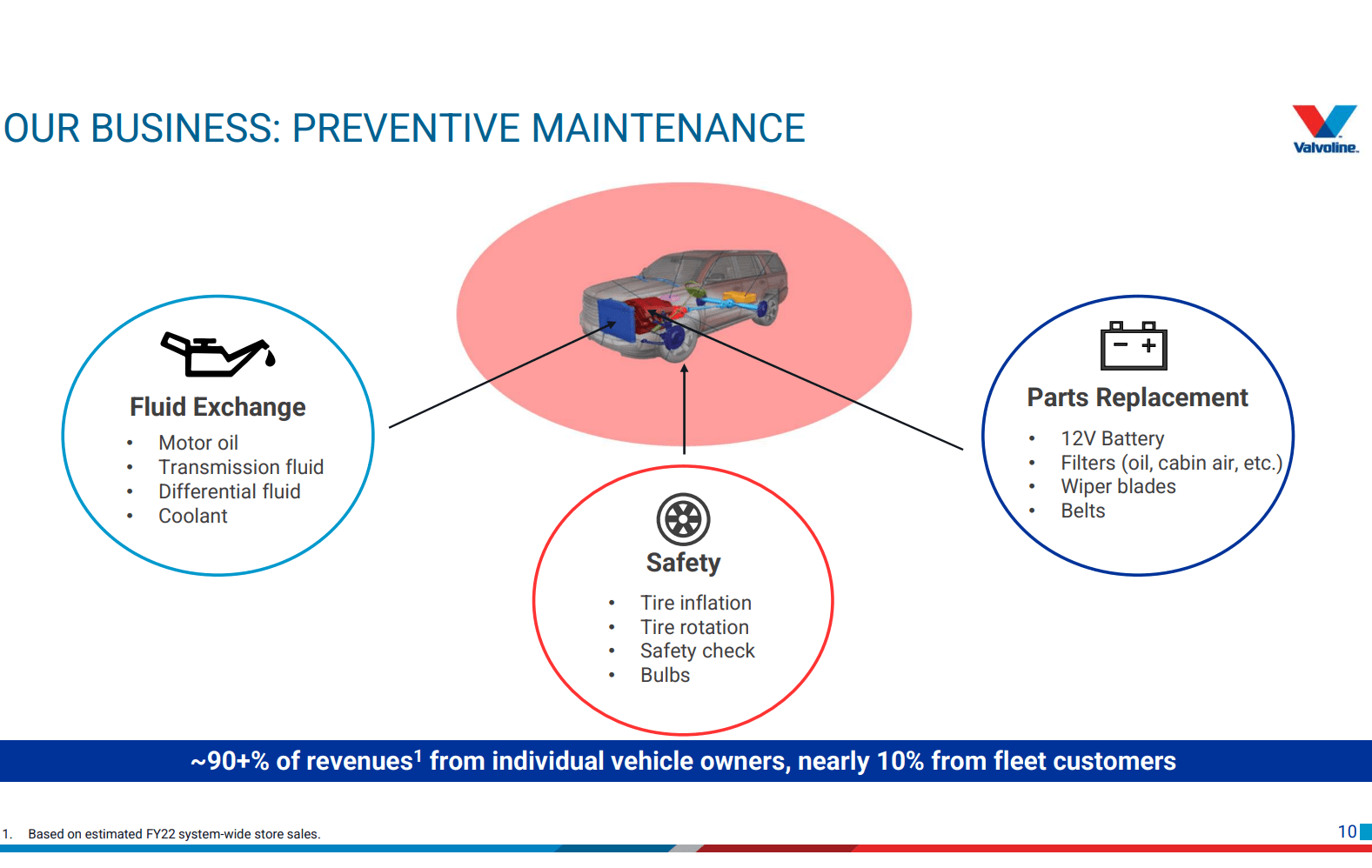

Valvoline went public in 2016 after it was spun off of Ashland. At that time, the business was organized into three segments: Core North America, Quick Lubes, and International. In the Core North America segment, Valvoline sold products to consumers for DIY automotive projects through auto retail outlets in North America. The Quick Lube segment encompassed its chain of company owned and franchised stores in which the company provided automotive services for its customers. In 2016 the company owned 330 of these stores and had 720 franchised stores. The International segment encompassed the sale of Valvoline’s products for international customers.

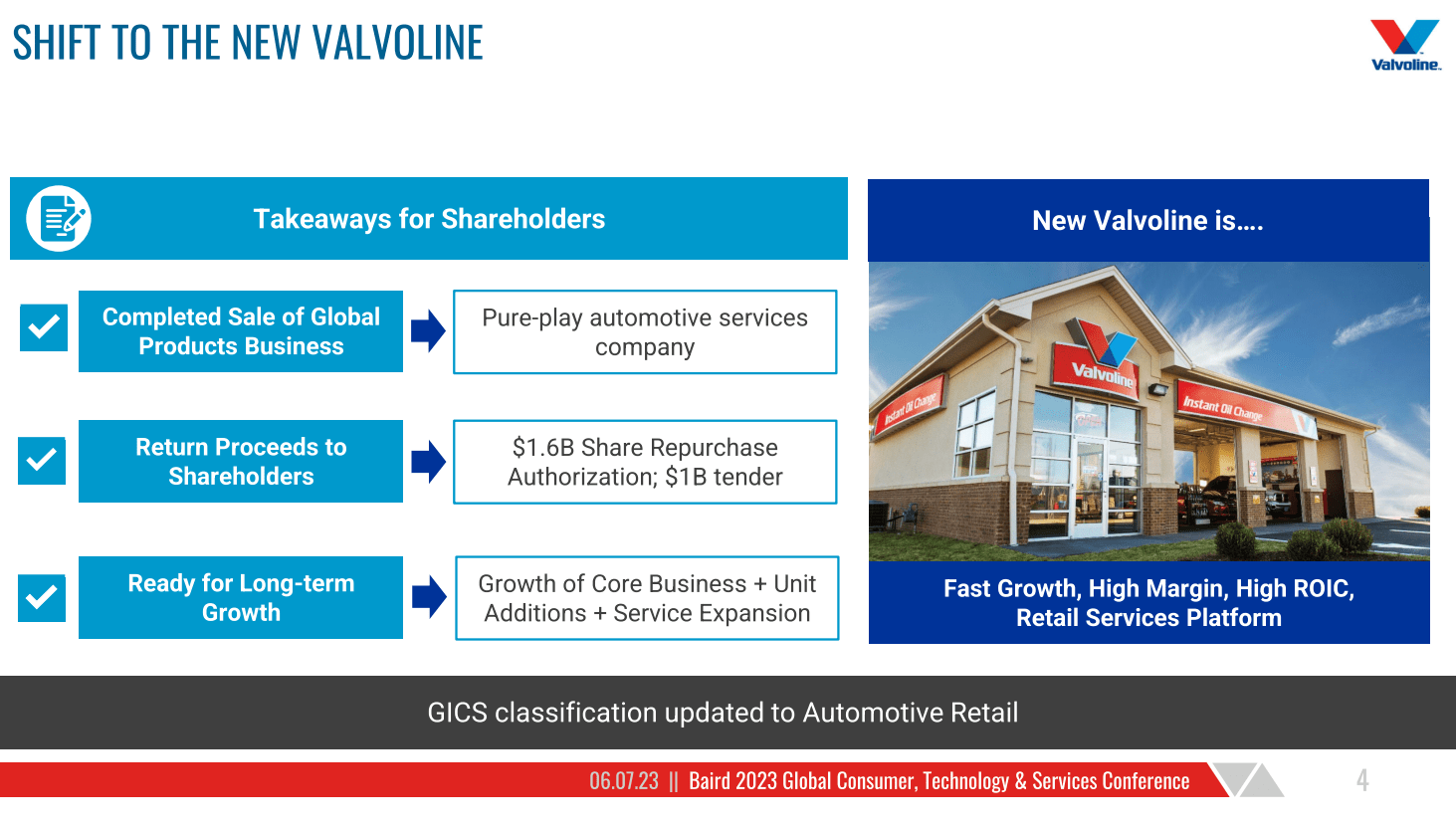

After the recent sale of the Global Products segment, which was the combined Core North America and International segments, the company became a pureplay automotive retail operator.

Valvoline Retail Segment Overview (Valvoline Presentation from Goldman Sachs Global Retailing Conference)

{kind=link}

Compared to 2016 when there were far more franchised stores than company owned stores, there is now more of an even split between the two. As of the end of Q3 2023, there were 1804 system-wide stores of which 950 were franchised and 854 were company owned. Valvoline management consistently reiterates that they don’t favor one over the other but rather think in terms of the total store count. The main differences between the two models is that company owned stores provide higher absolute revenue and EBITDA over time but lower ROIC, while franchised stores provide higher ROIC but lower revenue and EBITDA.

Compared to the current 1804 stores, management believes that at full capacity Valvoline can operate 3500 stores, leaving plenty of room for growth in the years ahead. This plan to aggressively pursue growth in its store count while maintaining high returns on invested capital did not change with the recent CEO change . Sam Mitchell, Valvoline’s CEO of the past 21 years, passed the baton to Lori Flees, a newer member of the Valvoline leadership team. While Lori is newer to Valvoline, she has many years of experience managing retail stores at Walmart so there should not be much disruption to what has been a well-oiled growth machine at Valvoline.

Past Financial Results

Valvoline’s financial history over the past decade contains information from the Global Products segment which isn’t relevant going forward. However, the company’s high returns on invested capital over that period indicates that it is a well-managed business.

In the following chart I created, invested capital is adjusted for held-for-sale assets and excess cash.

{kind=link}

ROIC has dropped in recent years due to a decline in earnings associated with the sale of the Global Products segment, combined with the fact that Valvoline has maintained some legacy assets on its balance sheet. As operating income grows faster than its asset base going forward, returns on invested capital will improve. This also means that returns on incrementally invested capital will be high in future years.

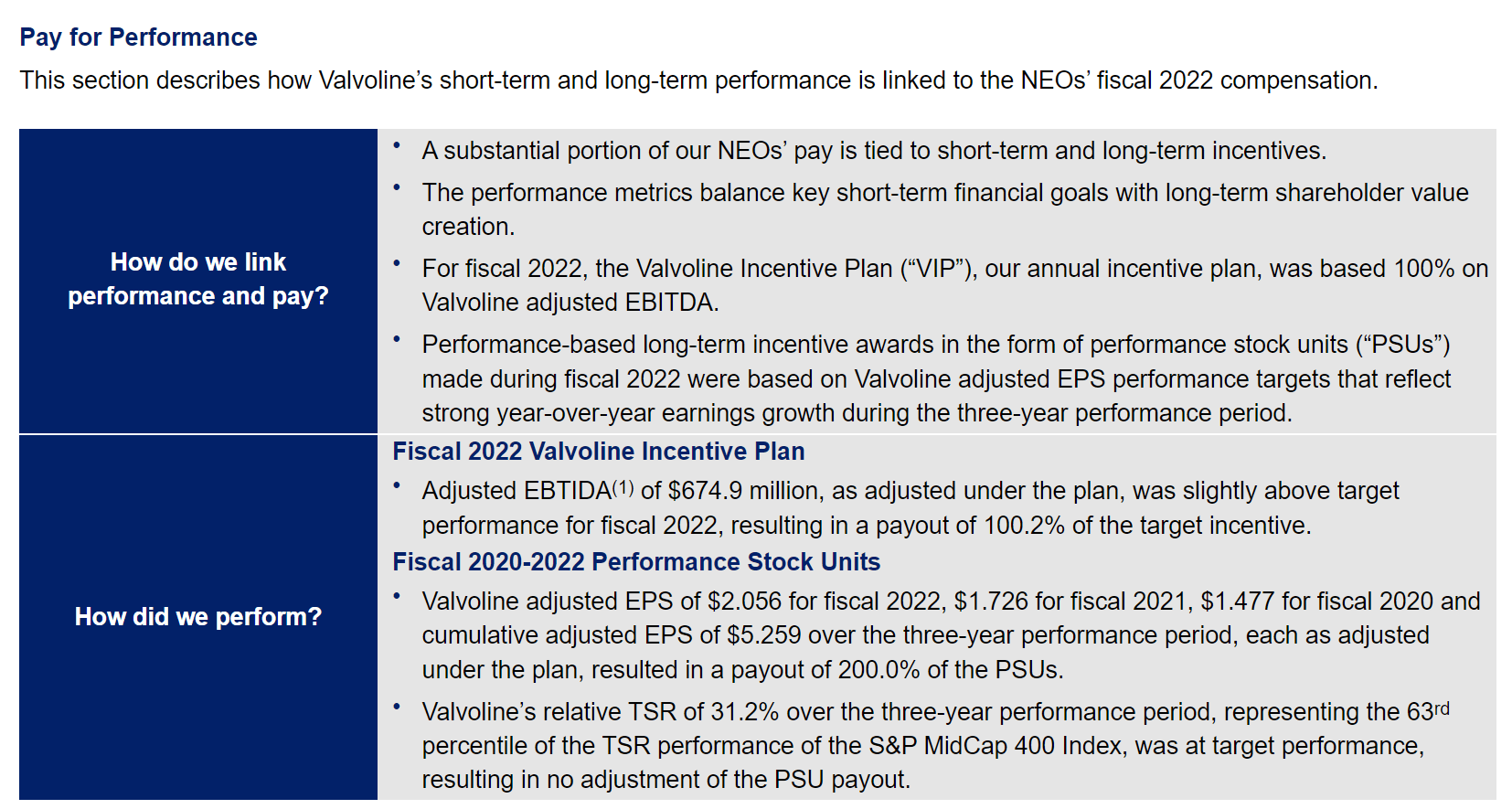

Management seems to place high importance on ROIC due to the many mentions of it in Valvoline’s IPO prospectus, in its investor presentations and in its earnings call. This would partially help explain why it's been so high but interestingly, management’s annual incentive compensation is not tied to ROIC in any way and is 100% based on adjusted EBITDA.

Valvoline Incentive Compensation Philosophy (Valvoline 2022 Proxy Statement)

{kind=link}

Coupled with the low insider ownership of the stock, this is a cause for concern as incentives often dictate actions over time. However, with its history of high ROIC along with the many mentions of it by the management team, I would bet that growth will not come at the expense of ROIC going forward.

Valvoline’s same store sales growth also indicates that the business is high quality. As of 2022, Valvoline has had 16 consecutive years of same-store sales growth as it continues to take share from other competitors in the fragmented automotive retail industry.

Valuation and Price Target

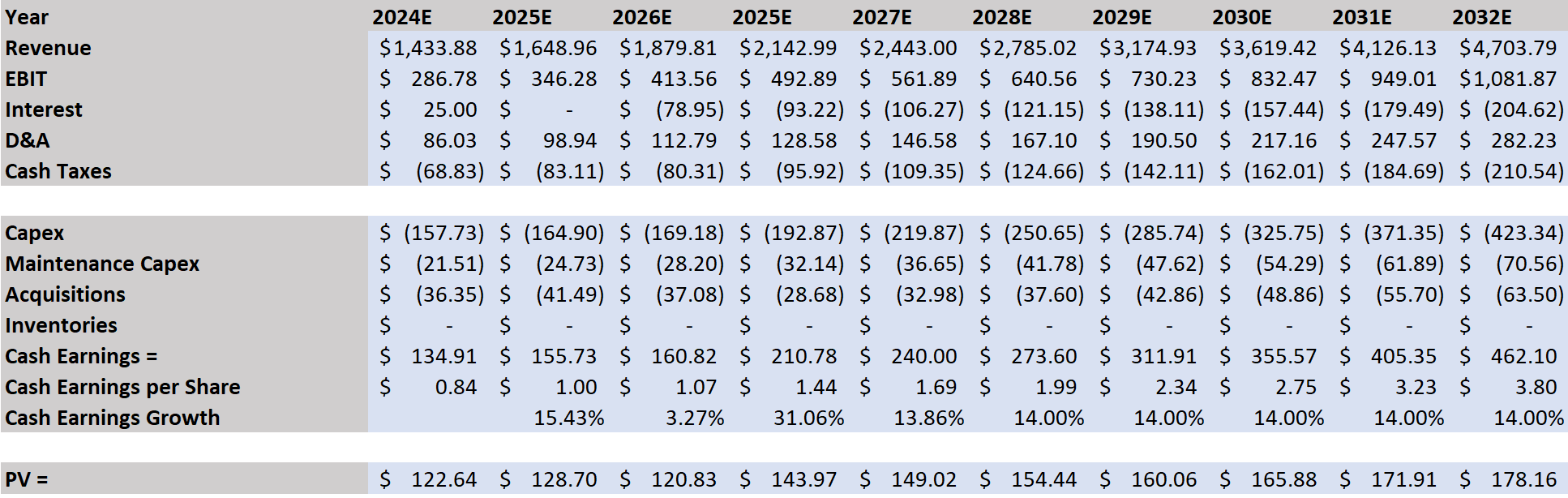

My estimate of Valvoline’s intrinsic value is based on management’s long-term guidance of a 14-16% revenue CAGR and 26-29% EBITDA margin. I am assuming:

- 16% revenue growth in 2023, 15% in 2024 and 14% thereafter

- Operating margin of 20% in 2023, 21% in 2024, 22% in 2025 and 23% thereafter

- Interest expense equal to 6.5% of net debt in 2023, 6% in 2024, and 5% thereafter

- 24% tax rate through 2032

- D&A equal to 6% of revenue from 2023 to 2032

- Capital expenditures equal to 11% of revenue in 2023, 10% of revenue in 2024 and 9% thereafter

- Cash spent on acquisitions equal to 5% of revenue in 2023, 4% of revenue in 2024, 3% of revenue in 2025, and 2% of revenue thereafter

- 10% WACC

- 2% terminal growth rate

{kind=link}

Valvoline DCF Continued (Created by Author)

All of these assumptions lead to an intrinsic value estimate of about $46 per share.

I am also estimating that Valvoline will trade for about $43 with a normalized cash earnings multiple approach. My definition of normalized cash earnings here is a measure of the total operating cash-earnings power of the business. This is similar to the estimate of cash earnings from my DCF above, but only takes into account maintenance capital expenditures and assumes no acquisitions are made. With this approach, I estimate that 2024 normalized cash earnings per share are $2.17 assuming that maintenance capital expenditures are equal to 1.5% of revenue. My $43 price target utilizes a 20x multiple with this estimate which is about the free cash flow multiple the stock has averaged over time.

Combining these two methods, I am assigning the stock with a buy rating and a $45 price target. This would provide investors with 40% upside from today’s price.

Risks

The primary risks stem from management’s execution of the aggressive growth strategy and general industry risks.

As I mentioned above, while management consistently mentions ROIC in presentations and calls, Valvoline’s executive incentive pay is 100% tied to adjusted EBITDA. If management eventually begins to make acquisitions and investments for the sole purpose of driving EBITDA higher without considering the price paid, shareholder returns will suffer.

There is also terminal value risk for automotive retailers like Valvoline. With a shift to electric vehicles, there may be less of a need for oil changes and less of a need for DIY automotive shops as EV consumers will have to go to specialized automotive repair shops or dealerships for repairs. If this shift occurs quickly, Valvoline shareholders will suffer as demand for the company’s services is negatively impacted. This is something Valvoline shareholders should keep an eye on going forward. I am personally in the camp that the EV transition will take longer than anticipated and its impacts will only be seen many decades from now.

Final Thoughts

The past financials of Valvoline’s retail segment indicate that it is a high quality and well-run business. If this continues and management is able to meet its long-term growth and margin guidance while maintaining high returns on invested capital, the stock should do well from here. With this in mind, I am assigning the stock with a buy rating and a $45 price target based on my estimate of Valvoline’s intrinsic value, and my estimate of the company’s FY2024 normalized cash earnings and a 20x multiple.

Risks include management execution that may suffer due to improper incentive compensation and terminal value risk as the electric vehicle transition unfolds. However, at the stock’s current price and valuation, I believe there is a margin of safety that will protect investors to a degree if these risks play out.

For further details see:

Valvoline: A Well-Oiled Machine