VVV - Valvoline: Dilemma Between Growth And Value

2023-04-18 05:20:17 ET

Summary

- Valvoline's Q1 performance is seen as a favorable outlook for the company's financial prospects, driven by a blend of pricing modifications, premiumization, and a boost in non-oil change revenue.

- However, its overvaluation relative to competitors based on financial metrics, such as P/E Non-GAAP and PEG Non-GAAP ratios, P/S ratio, and high EV ratios, is noted as a potential concern.

- Valvoline's subpar performance in meeting internal goals, potential inflationary pressures, and a competitive environment are also noted as potential risks to profitability.

Thesis

I believe that Valvoline Inc. (VVV) stands at a crossroads, with investors seeking to understand the company's potential for growth and value creation. Therefore, my article delves into the bull and bear cases for Valvoline, examining the company's strategic moves, financial performance, and market position to potentially help investors make a well-informed decision about the prospects and risks associated with the company's stock.

{kind=link}

Valvoline's Bull Case

Valvoline remains confident it can meet its long-term objective of 55% franchises even with its current franchise mix at 53%, by expanding into 100 company-operated stores while simultaneously speeding franchise growth. In my estimation, such an innovative plan should enable Valvoline to broaden its business ventures while protecting profitability.

Valvoline Strengthens Its Footprint

Moreover, the encouraging discourse with prospective franchisees bodes well for the future enlargement of Valvoline's commercial sphere. As contemporary inflationary forces alter the landscape for independent Quick Lube operators, Valvoline stands to reap the rewards of this development in both the realms of acquisition and franchise recruitment.

In addition, the notable enhancement of Valvoline's non-oil change revenue penetration merits recognition, as does the firm's conviction in its operational performance and the robustness of consumer and customer tendencies. This further substantiates the solidity and resilience of Valvoline's business architecture, thereby offering investors a renewed sense of trust in the organization's capacity to yield long-term returns.

Refining Cost Efficiencies and Increasing ROI

Upon further examination, Valvoline's concentration on refining labor scheduling and procurement to bolster cost efficiencies represents a judicious approach to augmenting profitability. In my opinion, honing these pivotal aspects of the enterprise, the company is well-positioned to curtail operational expenses without compromising the caliber of services rendered to its clientele.

On the subject of advertising, Valvoline's robust returns on investment are also worth noting, as they fuel growth among both novel and established customers. From my viewpoint, as the business terrain grows ever more competitive, the importance of efficacious marketing cannot be overstated, and it is indeed encouraging to witness the fruits of Valvoline's labors.

Peering into the future, Valvoline's guidance range intimates a strong likelihood of delivering impressive earnings growth during the latter half of the year. Given that historical data suggests approximately 55% of full-year EBITDA is customarily generated within this timeframe, I can't help but view this as a propitious outlook.

Robust Sales, Strategic Divestment, Enhanced Focus

To my mind, Valvoline's robust Q1 performance presents a favorable outlook for the company's financial prospects. Sales growth has been driven by a judicious blend of pricing modifications, premiumization, and a boost in non-oil change revenue, attesting to the efficacy of the company's strategic approach.

Despite a dent in GAAP operating income owing to an anomalous key item concerning legacy tax assets, Valvoline finalized the divestment of its Global Products business in the early stages of calendar 2023. This shrewd maneuver positions the company to optimize its capital structure and channel resources more effectively, ultimately bolstering shareholder value. Upon further examination, the decision promises to sharpen Valvoline's focus on core competencies and streamline operations.

Moreover, the company's emphasis on propelling same-store sales via its tried-and-true model of swift, reliable, and dependable service , I believe, bodes well for future expansion. As Valvoline garners market share and fortifies customer loyalty, the firm stands to augment its revenue and profitability in the years ahead.

Peer Evaluation

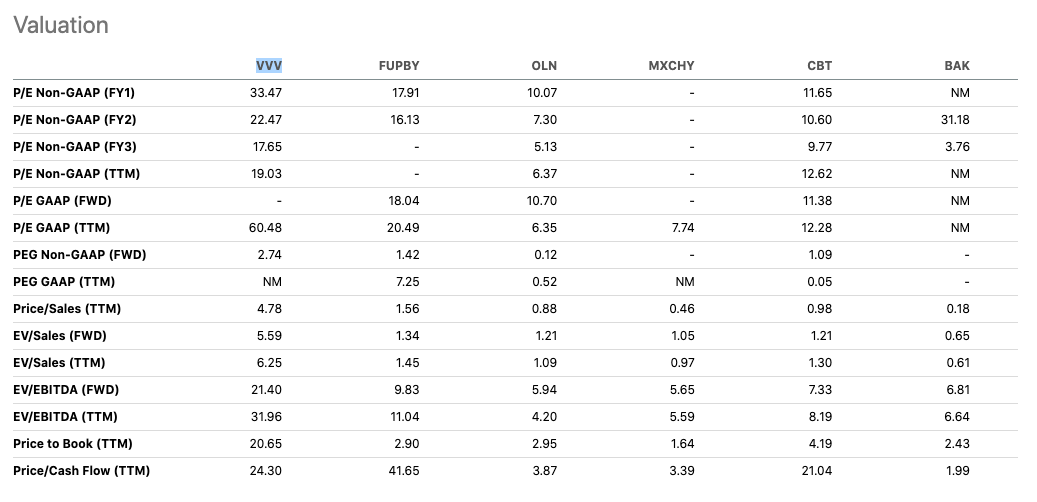

As far as I'm able to judge, Valvoline seems to be experiencing an outstripping valuation relative to competitors based on numerous variables.

{kind=link}

Primarily, VVV's P/E Non-GAAP (FY1) ratio sits at a lofty 33.47, considerably outpacing its counterparts. This implies that the market anticipates VVV to generate superior earnings growth relative to its competitors, a premise not necessarily corroborated by additional financial metrics. Furthermore, VVV's PEG Non-GAAP [FWD] ratio of 2.74 surpasses that of its peers as well. Given that a PEG ratio exceeding 1 typically denotes overvaluation, this may indicate that VVV's stock price lacks sufficient justification in terms of its earnings growth prospects.

{kind=link}

Additionally, VVV's Price-to-Sales (P/S) ratio of 4.78 surpasses all of its competitors and indicates that the stock price is significantly more expensive in relation to its profitability. Furthermore, VVV has high EV ratios across the board; namely, EV/Sales ((FWD)) at 5.59, EV/Sales ((TTM)) at 6.25, and EV/EBITDA ((FWD)) at 21.40 - further illustrating a significant overvaluation when it comes to sales or profits before interest payments and taxes are taken into account.

{kind=link}

Lastly, in terms of profitability metrics, I noticed that VVV trails some of its competitors. For instance, the company's EBIT margin of 13.87% and EBITDA margin of 19.56% lag behind those of some of its peers. It could be safe to assume that this diminished profitability could provide yet another rationale for the potential overvaluation of VVV's stock price.

Valvoline's Bear Case

Moving on to Valvoline's risks, the first thing that became clear to me is that the company has regrettably fallen short of its internal goal by a margin of 5%. This subpar performance is especially disconcerting amidst the prevailing economic backdrop, which might impede the company's ability to lure new franchisees and obstruct its ambitious plan to elevate its franchisee base to 55% by fiscal year 2027.

Valvoline Falls Short of Goals; Profits at Risk

Moreover, I am of the opinion that Valvoline's endeavors to counter inflation through pricing modifications and enticing franchisee incentives might not be sufficient to entirely neutralize cost pressures, potentially affecting profitability. Although the company has reaped substantial rewards from its advertising investments, it could face an uphill battle to generate substantial revenue growth in an intensely competitive environment. If left uncontrolled, escalating SG&A expenses might further dent profitability, while unforeseen disruptions in the supply chain or labor market could exacerbate the impact on margins and profits.

Therefore, despite a robust Q1 performance, with sales from continuing operations soaring by 17%, Valvoline's GAAP operating income from continuing operations was adversely affected by a considerable, nonrecurring key item linked to legacy tax assets. Furthermore, while the company envisions returning $1.6 billion to shareholders via share buybacks within 18 months after finalizing the sale of the Global Products division , from my point of view, there is no assurance that market conditions will accommodate such extensive share repurchases.

Valvoline Misses Q1 2023 EBITDA Expectations

Valvoline's Q1 2023 EBITDA modestly missed management's expectations due to the ramifications of inflation on the cost of goods and the heightened relative influence of company operations on overall margins. Although the company has instituted a central operations team devoted to enhancing efficiencies via process improvement and technology enablement, as far as I'm concerned, the efficacy of these measures in tempering inflation's impact on margins is yet to be determined.

Last but not least, from where I stand, the company's triumph hinges on bolstering same-store sales and supplementing units and incremental services. While there's no denying that Valvoline boasts an illustrious long-term history of promoting same-store sales performance and unit growth, there is no assurance that this upward trajectory will persist. Consequently, I think that the company's strategy to return the lion's share of proceeds from the Global Products division sale to shareholders through share buybacks may not constitute the most judicious allocation of funds, particularly if the company fails to accomplish its growth objectives.

Takeaway

I concluded that maintaining a status quo stance on the stock is advisable. The firm's Q1 performance undoubtedly warrants attention, as it boasts a commendable 17% surge in sales derived from ongoing operations. Yet, Valvoline's inability to achieve its internal objective—falling short by a 5% gap—is cause for concern. Additionally, the firm faces headwinds in the form of inflationary pressures , supply chain tumult, and a volatile labor market , all of which threaten to dent its profit margins. Consequently, I propose that investors adopt a cautious approach and maintain their current holdings in the stock.

For further details see:

Valvoline: Dilemma Between Growth And Value