VVV - Valvoline: Fiscal Health And Better Focus Are The Key (Rating Upgrade)

2023-12-06 00:40:17 ET

Summary

- Valvoline's transition to a pure-play retail business has resulted in strong financial performance and a healthy balance sheet.

- VVV's narrow focus on its core business and a healthy store network contribute to its competitive advantage.

- The key to future growth lies in well-calibrated expansion of the store network and monitoring same-store sales and operating margins.

In an article we published a year ago in Aug 2022, we expressed our optimism on the deal between Valvoline (VVV) and Aramco (ARMCO) in which the former agreed to sell its Global Products (Lubricants) business in order to focus on growing its more competitive Retail Services business. Post-transaction, the company had its first year as a pure-play retail business, within an industry that is characterised as non-discretionary with relatively less volatile revenues/margins due to service-based business model. We are obviously not disappointed with the short-term outcome and believe the company should be able to deliver decent performance in the long term as well.

Nov 2023 - Investor Presentation

{kind=link}

Although there was an across-the-table decline in margins that should be considered in the context of the broader inflationary macro-environment. The net income and EPS have grown substantially on the back of higher revenues with the latter supported even further by the share buyback. The repurchase program was executed successfully with US$212 million still remaining (market cap US$4.66 billion).

Strong Fiscal Position

The company has a very healthy balance sheet as evidenced by the following:

- Sizable cash & equivalents that provide them the ability to maintain or even increase capex. The company is forecasting approx. US$185-$215 million in capital expenditures for the next fiscal year, to be funded primarily from the operating cash flows.

- The transition to a pure-play service-based model means the working capital requirements could be lower and better controlled with long-term supply agreements on the product side with Aramco.

- The net debt position is very comfortable at US$1.31 billion, with 96% of the long-term debt not due before 3 years.

- The company used part of the sale proceeds to redeem the short to medium-term loan notes maturing in 2024-25 with some of those at the higher end of rates the company is paying on its debt.

- Due to the interest rate swap agreements in place, approx. 82% of the company's outstanding borrowings had fixed rates , with the remainder bearing variable interest rates.

- The company currently has additional capacity to borrow US$472 million which should bring additional dry powder to fund the growth if needed.

Long-term Debt Breakdown (Latest 10-K Filing) Debt Maturity Waterfall (Latest 10-K Filing)

{kind=link}

{kind=link}

Narrower Landscape, Better Focus

The company is aiming for 3,500-plus stores with a target to lower capital requirements through accelerated franchise growth. Now their strategic and business landscape is a lot narrower one may expect a better focus on the core business growth. Their ecosystem includes automotive dealerships, automotive repair and maintenance centers, along with regional and independent quick lube operators. The retail stores compete for consumers and franchisees with other major franchised brands such as Jiffy Lube, Grease Monkey, Take 5 Oil Change, Express Oil Change, and Mr. Lube in Canada. The competition with other franchisors in automotive services and across other industries is based on "the expected return on investment and the value propositions offered to franchisees".

A Healthy Store Network is the Competitive Advantage

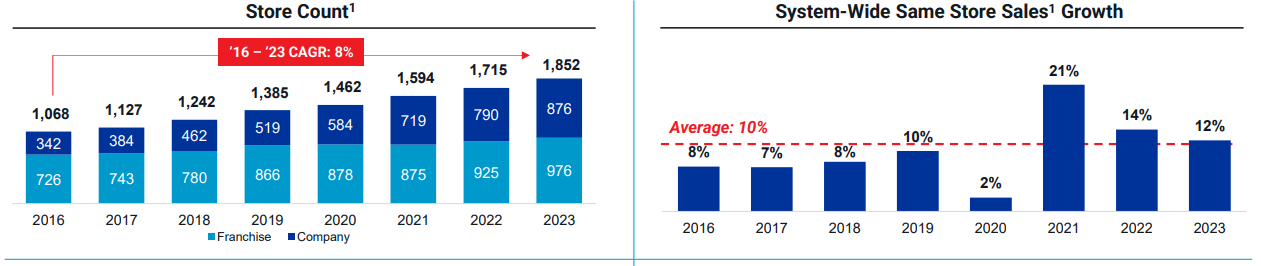

Logically, one would look for the growth or sustainability of the same-store sales to understand if they would able to command better pricing, in addition to the growth in revenues due to a higher number of stores. In that context, the fiscal year 2023 was the 17th consecutive year of positive same-store sales growth, which is quite impressive for a company with +1000 stores across the USA and Canada.

Store Network (Latest 10-K Filing)

{kind=link}

The network increased by 30% over the last five years with over 50% franchised, lowering the risk on the fixed assets side. Despite the average 8% p.a. growth in store count since 2016, the company has reported an average 10% p.a. growth in same-store sales.

Nov 2023 - Investor Presentation Nov 2023 - Investor Presentation Nov 2023 - Investor Presentation

{kind=link}

The trend in volumetric growth continued during fiscal year 2023, and the company is even more ambitious about its target for the year 2027 with 250 net new store additions per year. This should help grow the revenues and add to the bottom line at hopefully similar or better multiples the stock is currently trading at, although the actual net new store additions might be lower due to any potential recessionary headwinds in the coming years.

Quarterly Net New Stores Addition (Nov 2023 - Investor Presentation) Targeted Net New Stores Additions (Nov 2023 - Investor Presentation)

Calculated Growth is the Key

The key upside in this business should come through a well-calibrated growth in the number of stores because the expansion for the sake of it won't bring additional returns for the shareholders. For this reason, the key metric to monitor in the long run is the trend in same-store sales and operating margins. Any persistent idiosyncratic decline in these two measures would be the canary in the coal mine for the long-term business prospects and subsequently the stock price.

One thing we would like to be cautious about though, is any sizable potential acquisitions by the company using debt (or even operating cashflows), which would go against our investment thesis (fiscal health, improved strategic focus). We would like to re-evaluate the business prospects if the management decides to pursue inorganic growth through such business acquisitions.

To conclude, the stock could be considered a good buy at current levels, however, it may not be a bad idea to wait and accumulate at lower levels because of the long-term investment thesis.

For further details see:

Valvoline: Fiscal Health And Better Focus Are The Key (Rating Upgrade)