VREX - Varex Imaging: Capital Productivity A Mitigating Factor Despite Recent Rally

2023-06-23 14:51:16 ET

Summary

- Varex Imaging Corporation has experienced a 15% increase in market price in the last 6 months, breaking out of a long-term downtrend.

- The company's growth percentages indicate a well-diversified revenue stream, but its ROIC has decreased from 20% in 2015 to 6.65% in the TTM.

- Current valuations are unsupported at 19x forward earnings, getting me to $15 per share in equity value.

- Net-net, rate hold.

Investment Summary

As we're around halfway through FY'23 it's been a pleasure to see some of the healthcare longs I've positioned against come into the money. I'm now extending the coverage universe in search of more selective opportunities. My searches, deep within the entrails of the global financial markets, led me to Varex Imaging Corporation ( VREX ), a name that's caught a 15% bid in the last 6-months.

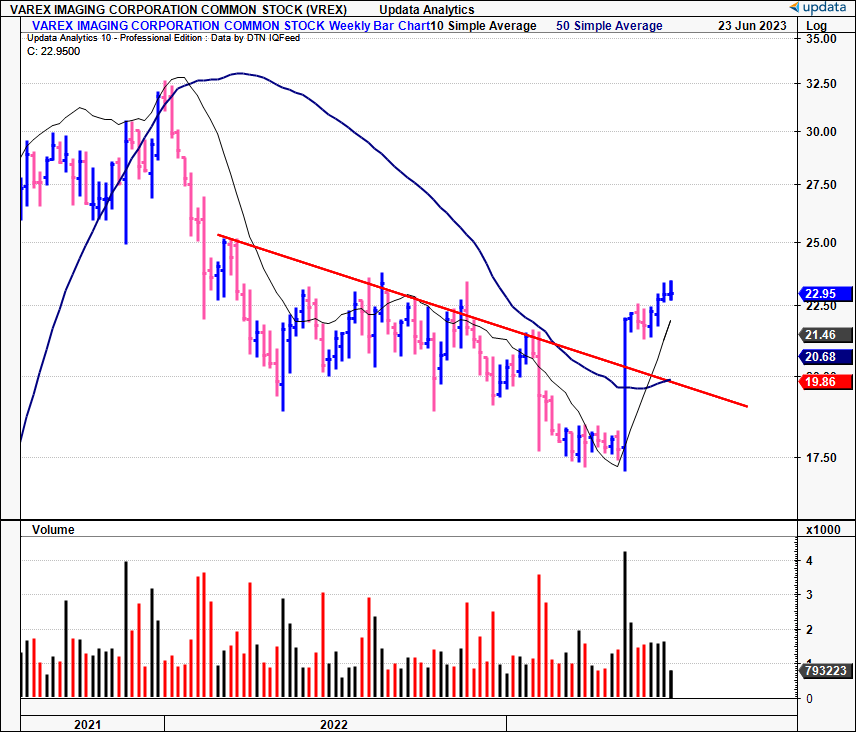

Analyzing the economic characteristics of VREX's business and the figures are unappealing in my view. However, the market has certainly revised its expectations on the company, evidenced by the sharp repricing described above. Further, the breakout is significant as it brings VREX out of an extensive long-term downtrend, and thus must be investigated further.

VREX is comparable to RadNet ( RDNT ), a company I am heavily bullish on and have recognized sturdy gains with in 2023. I would encourage you to check that publication out to make an accurate comparison between two competing names. See the latest RNDT publication here . Net-net, I rate VREX as a hold for now, looking to a price range of $15 per share.

Figure 1. VREX breakout from long-term downtrend.

{kind=link}

Critical facts to VREX investment debate

Peeling back the superficial layers to analyze all of the moving parts, my analysis points me to 3 coverage areas for VREX– 1) fundamental drivers, 2) sentiment factors, and 3) valuation. Detailed analysis of all components follows.

1. Fundamental drivers

Latest numbers

The company's latest numbers are telling of the revised expectations. It clipped Q2 FY'23 sales growth of 6% YoY and 11% sequentially. Underscoring this growth, the firm's medical segment was up 9% from Q4 and 2% YoY. Further, the industrial segment clipped a 19% sequential growth pattern and was up 22% YoY. On face value, the firm's growth percentages indicate a well-diversified revenue stream, effectively hedging the top-line to large sigma events going forward. You see this in the company's unimpacted revenue clip from 2019–'23.

Moving down the P&L, I'd note the following takeaways:

- The firm brought the revenue growth to 33% gross margin, which is tight. For example, the sector offers a median 55% gross, 42 points above the company. It pulled this to $30mm in adj. EBITDA.

- Whilst these are thin margins, one positive is the company's exposure to non-destructive inspection products ("NEPs") and photon counting detectors positions it well to capture a higher-margin over time in my opinion. For example, the global NEP market is poised for 8.7% CAGR into 2030, a high-growth segment. It's just up to the company to convert on this.

- It also exited Q2 with cash of $122mm, representing a $14mm increase from the prior quarter. Cash flows were improved by a $9mm inventory decrease as sales pulled through.

Looking ahead, management anticipates revenue growth of 3% to 5% over FY'22, calling for $902mm at the top-line in FY'23. This isn't exciting, and there's been no updates to earnings projections on this.

Unfavorable economic characteristics

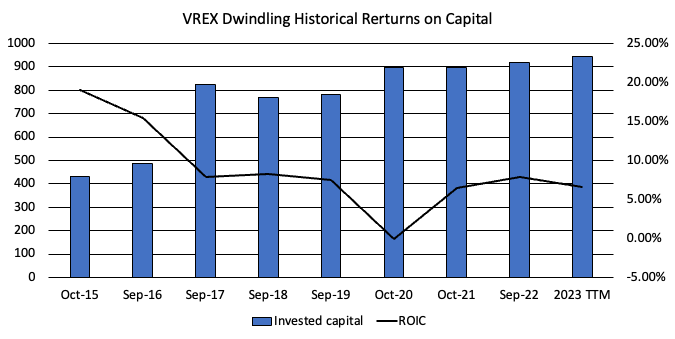

Since FY'15 VREX has delivered mixed results on the capital it has invested into operations. As potential investors in the business, we want to know exactly what profits VREX is producing on the capital it has at work, as, in this instance, capital produces the profits for the company. Hence, when I noticed the run-down in trailing ROIC from 20% in 2015 to just 6.65% in the TTM [Figure 2], I was surprised. It suggests the company has had a hard time in meeting its cost of capital, and certainly in meeting the market return on capital.

Figure 2.

{kind=link}

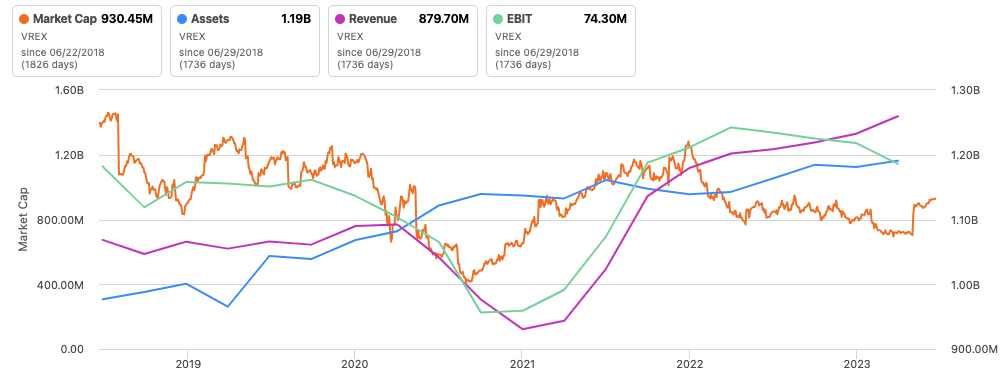

The relevance of this point is observed in Figure 3. It would appear the market is valuing VREX with a close relationship to sales and pre-tax earnings, more so than asset factors. This makes sense– the company allocates capital to generate additional sales and profits over time (the capital produces the profits remember). Hence, that VREX is producing less and less profitability on its capital, hasn't been conducive to its rating any higher. Notably, the uptick and sales from Q2 ––and the FY'23 projections–– may be one reason behind the recent rally. Thus, I am looking directly at the firm's pre-and-post-tax earnings growth scaled by its asset growth over the coming periods. For now, this data is supportive of a hold in my view.

Figure 3.

{kind=link}

2. Sentiment factors

The recent increase in VREX's market value can be attributed in large part to changes in investor sentiment, in my view. The importance of sentiment in driving stock prices higher cannot be overstated, and we can observe this phenomenon in 3 distinct ways here.

Firstly, we note a significant improvement in analyst ratings in the past 3 months, with sell-side analysts revising sales and earnings upwards 4 times. Consensus now forecasts a 4.5% growth rate for this year and the next, with anticipated revenue figures of $898mm and $940mm, respectively. These upward revisions reflect a growing bullish sentiment on The Street.

Secondly, options-generated data reveals that calls are heavily stacked at a strike price of $25 for both July and August expiries. This indicates a bullish outlook among investors with money at risk, betting on a rally to $25. Such informed opinions represent a notable factor in the ongoing debate over the company's future value.

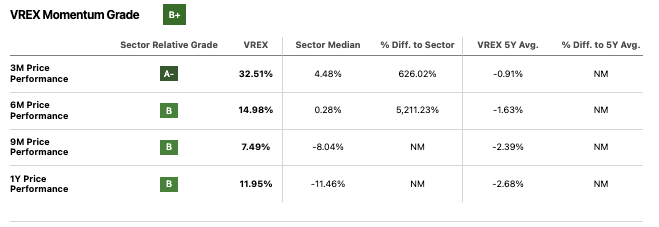

Finally, you will observe that momentum indicators are aligning well with the current sentiment. The stock is currently trading above all moving averages (10, 50, 100 and 200-day averages), surpassing key psychological levels. At the same time, the recent break has sent VREX above all previous time frames except for the 5-year mark. This price action suggests that investors are pricing in increasingly bullish expectations, further supporting a positive outlook for the stock.

Figure 4.

{kind=link}

3. Valuation

VREX trades at 19.7x forward earnings, and this is a shade below the sector's multiple of 20x, with the stock priced at 1.8x book value of equity. With the sharp rally from May–June, my question immediately is how much farther these multiples can extend.

Growth projections tell us a great deal on this as a decision rule– would you pay 19x forward, only for a PEG ratio of 85x? This implies a stagnant growth rate for an otherwise relatively unattractive valuation. Hence, using my investment criteria, there is no way I can pay this multiple without the growth factors to back it up. As an exercise, presuming no earnings growth moving forward, paying 19x forward, you'd get your payback in 19 years. Not attractive. My assumptions have the company to do $30mm at the bottom line. At 19x forward, this gets me to ~$15, about in line where the company was before the latest rally. This is supportive of a neutral view.

Appendix 1. VREX forward estimates

{kind=link}

In short

Collectively, there are positive points worthy of discussion for VREX. However, on closer inspection, there is a lack of torque feeding into the company's flywheel, meaning the latest buying rally in the company doesn't appear well supported on a fundamental basis. My numbers have the company to do $30mm in earnings this year and at the market's multiple of 19x forward this gets me to a value of $15/share, below the current market price. All the points raised here today, therefore, are supportive of a neutral viewpoint in my opinion. In that vein, I am rating the company a hold for now. I look forward to providing additional coverage.

For further details see:

Varex Imaging: Capital Productivity A Mitigating Factor, Despite Recent Rally