VSTA - Vasta Platform: Limited Upside Catalysts In The Near Term

2023-05-11 14:01:28 ET

Summary

- Vasta is the second-largest provider of K12 content in Brazil.

- I expect Vasta to grow revenues at a ?15% CAGR in the medium term.

- I currently have a hold rating on VSTA stock, given limited catalysts in the near term and growth likely being already reflected in the valuation.

Investment Thesis

I maintain a hold rating on Vasta Platform Limited ( VSTA ), which provides content, methodologies, and technology for private K12 schools in Brazil. Although the company operates in a large market with a current TAM of $37 billion as estimated by the company, I believe there are limited growth opportunities from here within an already penetrated market which is now reaching maturation levels. Despite the stock's decline over the past year, I believe the current valuation multiples are still high in the sector, which is why I currently recommend staying on the sidelines for now.

Company Description

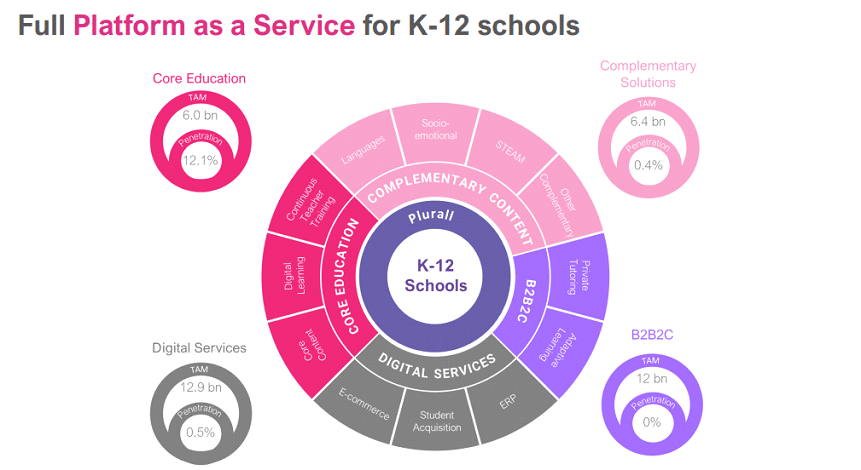

Vasta is the second largest provider of K12 content in Brazil, operating mostly under a B2B2C model. The company offers learning systems, traditional books, and digital services for the private K12 segment, serving 1.6m students and 4.5k schools. Content (91% of total revenues) is sold as traditional learning systems (78% of content), hybrid/PAR (15%), and spot (8%). Moreover, Vasta also offers digital services (9% of total revenues), consisting mostly of Livro Fácil, an e-commerce business focused on book sales.

{kind=link}

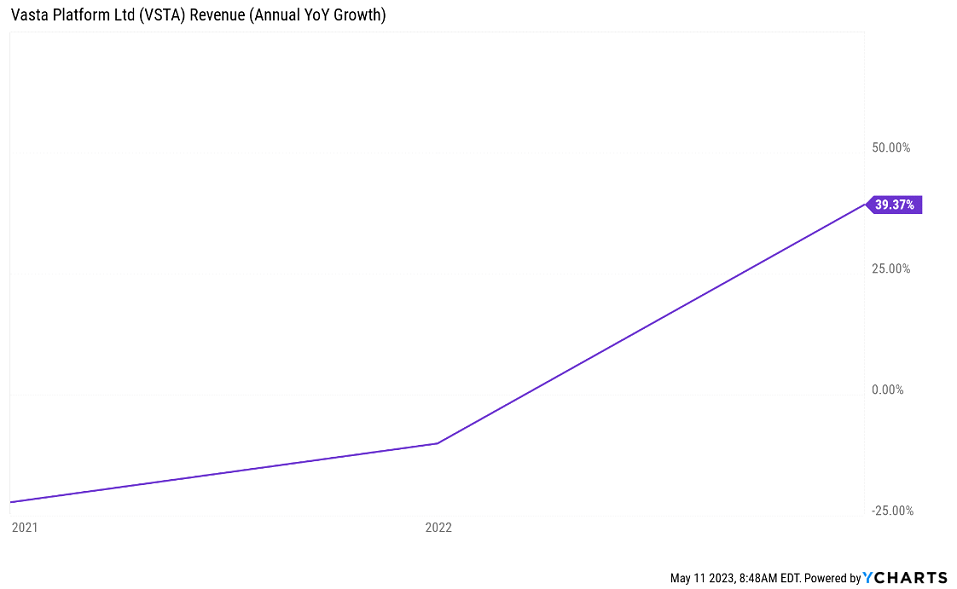

Revenue Trends: Solid Growth Trends Ahead

I expect Vasta to grow revenues at a ?15% CAGR in 2022-25E, supported by a 20% expansion pace in subscription revenues (in line with ACV growth ), which represent 88% of 2022 total revenues, while partially offset by a single-digit growth in non-subscription revenues, comprised of spot books, digital sales, and preparatory course tuition, mostly on the decline in spot book sales.

Vasta's revenue is affected by the timing of its deliveries to schools, which primarily occur in the 4th quarter of one year and the 1st quarter of the next. Revenue is recognized when schools obtain control over the materials. The 4th quarter results tend to reflect the growth in the number of students from one school year to the next, resulting in higher revenue in this quarter. Vasta's Digital Platform segment, which includes physical and e-commerce offerings, also experiences high demand during the back-to-school period from November to February of the following year. As a result, e-commerce revenue is concentrated mainly in the 1st and 4th quarters of the year.

VSTA annual revenue growth (Ycharts)

{kind=link}

Core Revenues Continue to Grow but Could Be Reaching Maturation Levels

The "core segment," which encompasses K12 mandatory curriculum content, has been the primary driver of Arco and Vasta's growth in absolute terms. However, the growth potential of this segment is expected to be limited due to factors such as a declining school-age population in Brazil, weak macro trends that hinder migration from public to private schools, and the high penetration rate of learning systems.

I expect the usage of learning systems to grow at a low single-digit rate, mostly as a result of learning systems gaining share over books, already making up 56% of the private market. While the private market itself could grow, it seems unlikely in the near term, given that the household income should remain under pressure, limiting migration of public-school students into private schools, which has nearly halted since 2014, and weak demographics for the school-age population.

Learning Systems Already Make Up a Large Amount of Private K12

There is a trend of growing penetration of learning systems, although I believe some schools will continue preferring to use traditional books; thus, it is unlikely that learning systems will ever reach 100% of all schools. There are several reasons behind the choice to adopt a learning system, including higher and more uniform quality provided to students. Nevertheless, price is sometimes also a reason: a study conducted by Oliver Wyman (hired by Arco) found that learning systems tend to be ~40% less costly to parents than traditional books. Moreover, retail is bypassed, and the school is able to earn a markup on the materials. On the other side, it is important to keep in mind that parents do not always buy traditional materials, which sometimes is not the case: parents might reuse books from older children, buy used books, or borrow.

Valuation

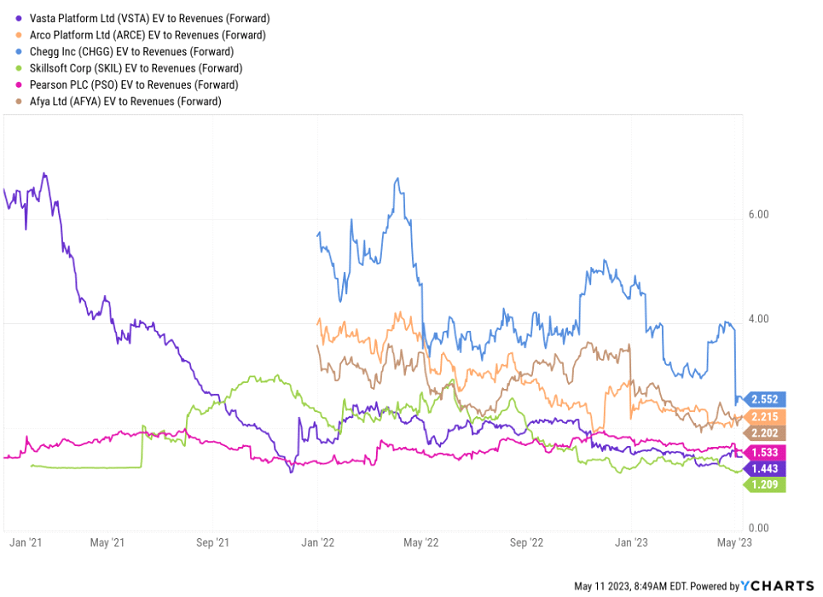

Vasta trades at a forward EV/Sales of 1.4x, at a significant discount to its historical valuation multiple. However, the depressed multiple is true for other companies in the sector as well, like, for example, Afya Limited ( AFYA ), a premium higher education name with strong and predictable earnings delivering solid growth rates, which trades at a significant discount at 2.1x EV/Sales.

The sector has faced relevant de-rating over the past couple of years, which I attribute mostly to a deterioration in the long-term growth potential of these companies, intensified by the weak performance of the companies during the COVID-19 crisis, with revenues coming short of guided ACV. Moreover, increasing yields have been putting pressure on growth stocks, also affecting the sector. I recommend a hold rating on the stock, given limited catalysts in the near term and growth being already reflected in the valuation.

Comparable Analysis of VSTA's Valuation Metric (Ycharts)

{kind=link}

Investors' Takeaway

The K12 education sector in Brazil still presents growth opportunities. The demand for core content is expected to increase as learning systems become more accepted and Vasta continues to gain market share. In addition, there should be higher adoption of supplemental content, leading to a revenue compound annual growth rate of about 15% for Vasta in the medium term. However, the companies in the K12 education sector in Brazil have experienced a significant decline in valuation over the past few years, mainly due to a reduction in the long-term growth potential of the companies in the sector. I believe there are limited catalysts in the near term for any upside re-rating of the stock, which is why I currently maintain a hold rating on the stock.

For further details see:

Vasta Platform: Limited Upside Catalysts In The Near Term