VB - VB: Small Caps Are A Buy In My View

2023-10-11 17:16:14 ET

Summary

- I evaluate the Vanguard Small-Cap Index Fund ETF as an investment at the current market price.

- I believe small-caps can benefit from continued US economic growth, a stronger US currency, and a favorable labor market.

- Small-cap stocks have performed well in 2023, but have been overshadowed by the rise of large-cap stocks. This could change going forward.

Main Thesis & Background

The purpose of this article is to evaluate the Vanguard Small-Cap Index Fund ETF ( VB ) as an investment at the current market price. This fund's objective is "to track the performance of the CRSP US Small Cap Index, which measures the investment return of small-capitalization stocks".

This is my first comprehensive review of VB, although I have written about small-cap exposure as part of some of my macro-reviews in months past. As we push closer to 2024, I continue to see a more favorable backdrop for small-cap exposure which is why I have decided to amplify this messaging in a stand-alone article. For perspective, small caps, as measured by VB, have actually performed reasonably well in 2023. However, those gains have been dwarfed by the rise of their large-cap peers:

YTD Performance (Google Finance)

{kind=link}

Given this divergence, I wanted to examine the small-cap theme more closely to see if I was missing something. After review, I am more convinced that there is value here and that the market may be missing it. This leads me to a "buy" rating on small-cap ETFs, such as VB, and I will explain why in more detail below.

The Discount Is Wide

One of the primary drivers of my bullish rating at the moment is valuation. This may seem odd, given that equities have had a positive year and don't exactly look "cheap" here in the US - no matter what sector you are considering. But this is all about relative value, and small-caps definitely have that.

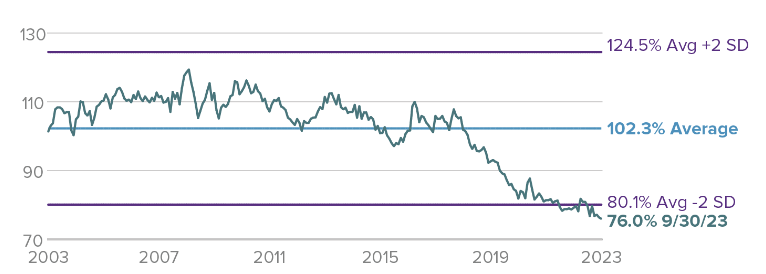

To illustrate, consider the gap in valuation is not only low in isolation, it is close to the biggest discount to large caps on record for the past twenty years:

Enterprise Value/Earnings Before Interest and Taxes (TTM) (FactSet)

{kind=link}

What this is showing is that by a common valuation measure (enterprise value over earnings before interest and taxes), small-caps look under-valued. This doesn't always translate to market gains (or out-performance). So we have to consider this is just one attribute out of many. But given the uptick in volatility we are currently seeing in the market, finding sources of relative value gives me definitive support.

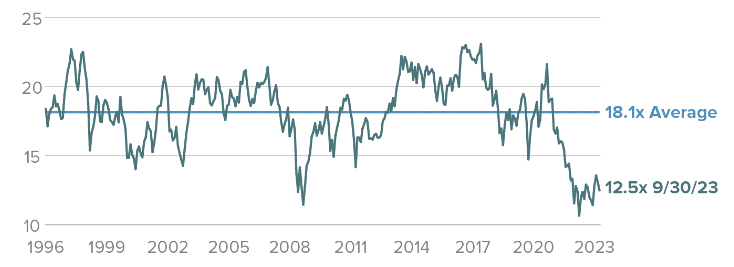

Expanding on this point, small-caps do have a low absolute P/E relative to their own history as well. This perhaps excites me even more than the comparison outside this sector because it shows investors are disproportionately fleeing this area relative to their own trading history:

Small-Cap Index (Current P/E) (S&P Global)

{kind=link}

The conclusion I draw here is that small caps look attractive from a valuation perspective. This is both in response to how they are trading compared to their own history, as well as the discount between them and larger firms. While not a guarantee of positive results going forward, it certainly represents a reasonable time to gamble on it, in my opinion.

Diversification Either Way

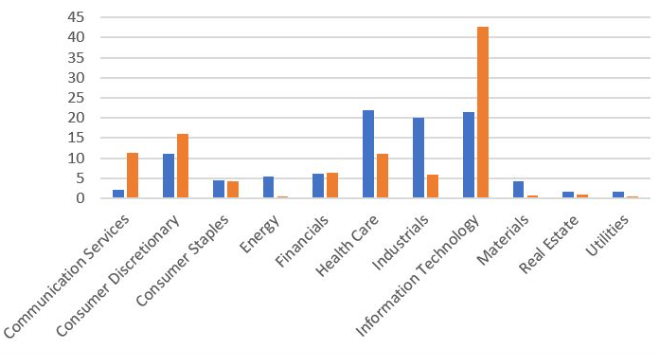

Another aspect of small-caps that I like in most times - not just now - is the potential for diversifying a portfolio. I would surmise many readers are like myself: heavily exposed to the S&P 500 and therefore, by extension, large-cap US Tech stocks. This is not inherently "bad" because these types of companies tend to deliver strong returns over time. But it does present concentration risk, so I am always looking for ways to proactively even out my holdings.

Sector Exposure (Orange Bar: Large-Caps; Blue Bar: Small-Caps (Vanguard)

{kind=link}

We can see that this extends to VB, whose sector holdings match the broader small-cap index benchmark fairly closely:

VB's Sector Breakdown (Vanguard)

Again, whether this is attractive or not is subjective. It depends on your individual outlook for these areas, as well as what other exposure you already have. While I personally see merit to diversifying in this fashion, I recognize it may not be for everyone. Deciding to add small caps to one's portfolio should not be taken lightly. Smaller companies may have more inherent risk, and the diversification element may not be as beneficial if one is already properly diversified in other ways.

Stronger Dollar Helps US, Domestic Focus

My next thought considers currency implications. In particular, small-caps can benefit from the strength in the US dollar in a disproportionate way to their larger peers. This is because larger companies are more apt to generate revenues and profits overseas - on average. If applicable, those foreign sales can be worth less when converted to a rising dollar. Small-caps, by contrast, are more geared towards the domestic (U.S.) economy because they are more likely to sell products within their own borders. This helps to insulate them from the loss of competitiveness of a stronger dollar, all other things being equal.

So why does this matter now? Because the USD has seen renewed strength as the market comes to terms with the Fed's "higher for longer" mantra. Compared to other developed market currencies, such as the Euro, the USD has seen appreciation in the short term:

{kind=link}

The takeaway for me is that the USD's rise is not equally felt across sectors or company sizes inherently, but based on whether or not those companies sell their goods and services domestically or internationally. On average, small-caps are going to benefit more from a rising dollar, but that assumes two things: all other attributes are equal (and they often aren't) and that those small-caps do actually generate mostly domestic profits.

I bring this up because while I like VB as a way to play this idea, readers could get more specific and drill down to a handful of small-cap companies that generate most (or all) of their profits in the US. In this way, they may outperform an index fund like VB. But I personally favor ETFs and diversification, so this is the right fit for me.

Should We Wait?

My final topic for discussion concerns timing. In this respect, I am referring to the timing of whether or not it makes sense to buy VB (or other small-cap stocks) now . As I'm sure my followers know, I have published multiple articles on why reason for caution exists, and this was before the flare-up in the Middle East. So far the market has shrugged off the violence, but that may not always be the case - especially as the conflict escalates. So it is important that each individual considers their own unique outlook and risk tolerance.

Expanding on that, I wouldn't fault anyone for being a bit weary of building on a more pro-growth investment idea like small caps. There are risks to this buy thesis - I won't pretend there aren't any. Chief among these risks is domestic growth. The US has been facing a wall of worry over a recession for a couple of years now, and it has yet to materialize. For this reason, I don't recommend holding off until a recession hits (or a recovery begins), but I will note that others may feel differently.

I won't pretend to suggest I know exactly when the US will face an actual recession, but I do know that history tells us recessions are generally not kind to small-caps. They tend to under-perform their larger peers by a wide margin in those environments:

Relative Performance (Bloomberg)

By contrast, small-caps will perform wildly better in the year coming out of a recession. During that recovery phase gains are very strong - and are (on average) much higher than what large companies deliver in terms of share price moves. So, in this vein, an argument could certainly be made to wait for the worst to occur here, and then dive in aggressively.

The problem with this is that we could be waiting a while. The US economy and labor market have both proved resilient. That could change, and the change could be quick. I am not denying that or suggesting a recession is a long way off. But the point is that I don't know - and neither does anyone else. So I can see the merit to owning small-cap exposure through VB, and then looking to build on it if my timing was off and a recession hits. A domestic slowdown could hurt VB, but I would see a mitigated reaction given how underpriced the underlying sector is right now.

Bottom line

VB offers investors exposure to a host of smaller companies, and that has piqued my interest. It offers potential for growth if the US economy continues to expand, there are diversification benefits, and domestic-oriented firms should see a boost from a stronger US dollar. Further, while the share prices have not moved substantially higher in 2023, the underlying companies are healthy enough to be pumping up their dividends in a meaningful way:

| June & September Distributions (2022) |

| June & September Distributions (2023) |

| YOY Growth |

| $1.25/share |

| $1.49/share |

| 19% |

Source: Vanguard

I am not suggesting VB as a "yield play", but a growing dividend stream is something I prefer both as a "Dividend Seeker" and also as someone that recognizes it is healthy firms that grow their dividends, not struggling ones.

For all these reasons, I am considering building a position in VB in my portfolio going forward. I would suggest to my followers that they consider this thesis going forward.

For further details see:

VB: Small Caps Are A Buy In My View