VBF - VBF: Moving From Buy To Hold (Neutral) After A +19% Return

Summary

- The Invesco Bond Fund is a fixed income closed end fund.

- The CEF focuses on investment grade corporate bonds.

- After assigning it a Buy rating in October, the fund is up more than 19%.

- We feel the current market rally in rates and spreads is overstretched and it is prudent to take some risk off the table here.

- This article covers CEFs and related analytics.

Thesis

The Invesco Bond Fund ( VBF ) is a fixed income closed end fund. The vehicle has income as its primary objective, and holds investment grade U.S. debt. We have covered this CEF before here , where we assigned it a Buy rating. The fund is up more than 19% on a total return basis since our rating:

Performance (Author)

Our article was posted at the end of October, hence a 19% total return from an unleveraged investment grade bond fund is quite impressive. Let us have a more detailed look at what drove that performance, and more importantly, what a retail investor should do now if it bought the name.

The main drivers in the CEF's performance have been:

- A) Discount to NAV, and

- B) Market Factors (rates and credit spreads).

On the discount to NAV side, the fund moved from an approximately -7% discount to net asset value to a flat share price versus underlying NAV. That is a fairly substantial move in a short amount of time, and now moves the CEF towards the top range for its historic discount. Ultimately, since the fund does not employ any leverage, we do not expect this name to trade at a premium. The all-in yields are too low and tightly positioned for an asset manager to really bring substantial alpha to such a vehicle.

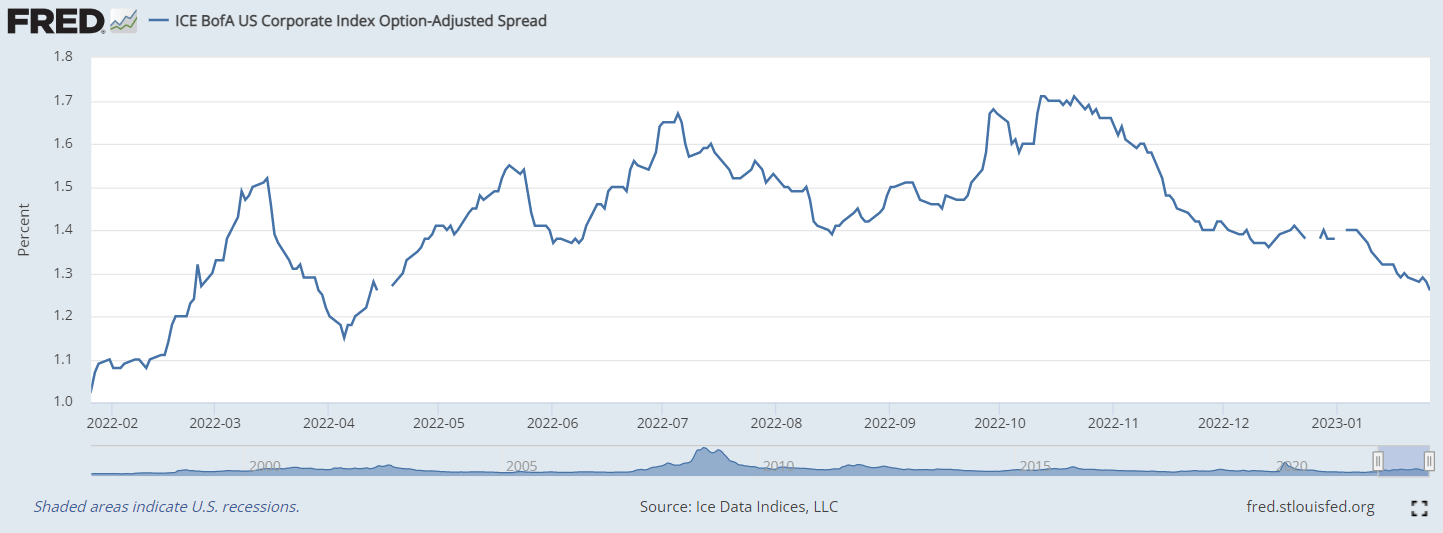

On the Market Factors side, rates have moved lower and credit spreads have tightened, pushing prices higher on investment grade paper. The narrative has now shifted to a 'soft landing' scenario, where the Fed is about to end its hiking cycle and will actually cut rates later this year. The market is now pricing this in (erroneously in our opinion), with rates lower and credit spreads tighter:

{kind=link}

We can see from the graph above, courtesy of the Fed, how investment grade corporate bond spreads have now tightened to levels not seen since the beginning of 2022. Spreads peaked at 1.7% in late October, and have now re-traced to 1.26%.

A fellow Seeking Alpha contributor, namely @Logan Kane , just published a very nice piece on this topic that singularly describes this 'priced for perfection' state. We do not think the trepidations in the wider market are done for, and we feel inflation is going to be sticker than prior considerations. With a very substantial run-up in total returns in just three months, we are now moving to Hold / Neutral on this name presently.

Analytics

AUM: $0.190 billion.

Sharpe Ratio: -0.03 (5Y).

Std. Deviation: 8.1 (5Y).

Yield: 4.5%.

Premium/Discount to NAV: -1%.

Z-Stat: 2.

Leverage Ratio: 0%

Performance

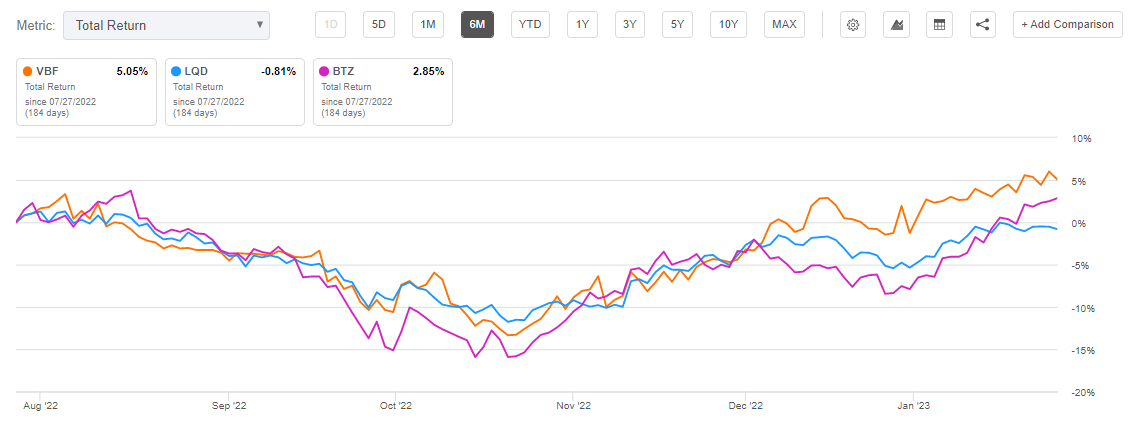

We can see how the CEF has fared compared to some of its peers:

{kind=link}

After bottoming out in late October, all three investment vehicles are up, with VBF outperforming. VBF is the CEF version of the iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ), but it has managed to outperform the ETF by more than 5% points in the past six months. Most of that move is due to the discount narrowing.

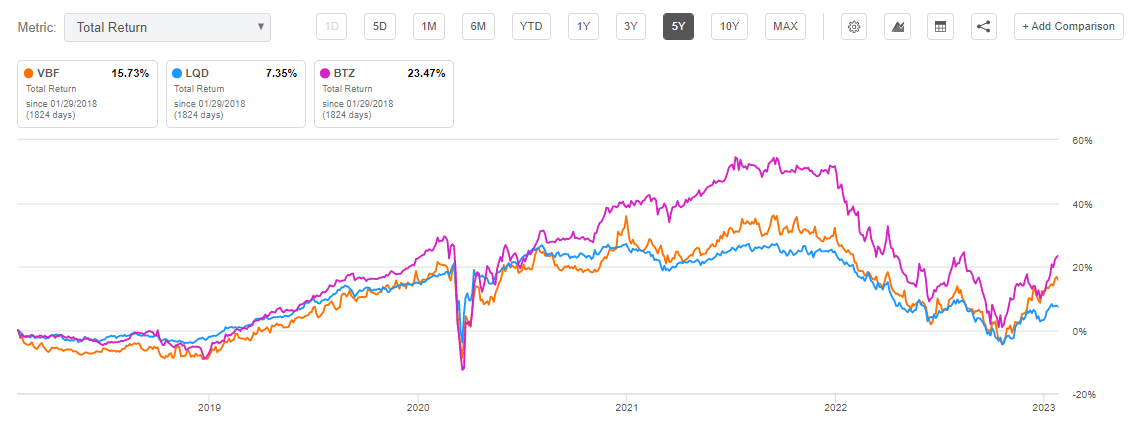

On a longer time-frame, the leveraged version of the investment grade bond exposure take, namely BTZ, outperforms:

{kind=link}

However, leverage magnifies both positive and negative returns, and we have seen the fund post a very negative 1-year total return since rates have risen. To note that on the contemplated 5-year period VBF outperforms LQD.

Premium / Discount to NAV

The fund's discount to NAV has narrowed substantially:

We can see the CEF having moved from a -7% discount to NAV to almost flat to net asset value. That is a fairly significant move, and at the top of its historic range. We can see that 0% has acted as resistance historically, and we expect that to re-occur.

Conclusion

VBF is an investment grade bond closed end fund. The vehicle does not have any leverage, but has historically outperformed LQD. We assigned the CEF a Buy rating in October, and the vehicle is now up more than 19% on a total return basis. The fund is now trading flat to its net asset value, at the top of its historic range. Given the CEF has no leverage, we do not see this name moving to a premium to NAV on a consistent basis. With credit spreads tighter and rates lower, the market risk factors have also bumped up the fund's performance. We do not feel the bear market is over, and we do not see the Fed pivoting this year by cutting rates. The market has now priced a 'soft landing' goldilocks scenario which will fail to materialize. With a very substantial run-up in total returns in just three months, we are now moving to Hold / Neutral on this name.

For further details see:

VBF: Moving From Buy To Hold (Neutral) After A +19% Return