VCLT - VCLT: Long Duration Investment-Grade Bonds Look Appealing

2023-07-26 03:07:53 ET

Summary

- VCLT is an exchange-traded fund that invests in investment-grade corporate bonds.

- The fund has a long duration of 13.2 years, which means that its price is sensitive to changes in interest rates.

- With most economists now predicting the July Fed hike to be the last one this cycle, the main risk factor for this fund is off the table.

- The fund's collateral contains mainly 'A' and 'Baa' industrial corporate bonds.

Thesis

The Vanguard Long-Term Corporate Bond Index Fund ETF Shares ( VCLT ) is an exchange traded fund focused on investment grade credit bonds. As per its literature, the fund:

- Seeks to track the performance of the Bloomberg U.S. 10+ Year Corporate Index.

- Provides for diversified exposure to the long-term investment-grade U.S. corporate bond market.

- Follows a passively managed, index-sampling approach.

- Provides current income with high credit quality.

The vehicle is entirely formed from investment grade corporate bonds, and targets the longer end of the curve with a 13.2 year duration. The fund is extremely granular, with over 2,700 individual names in the collateral. The main risk factor for this name is represented by rates, which have risen significantly in the past year.

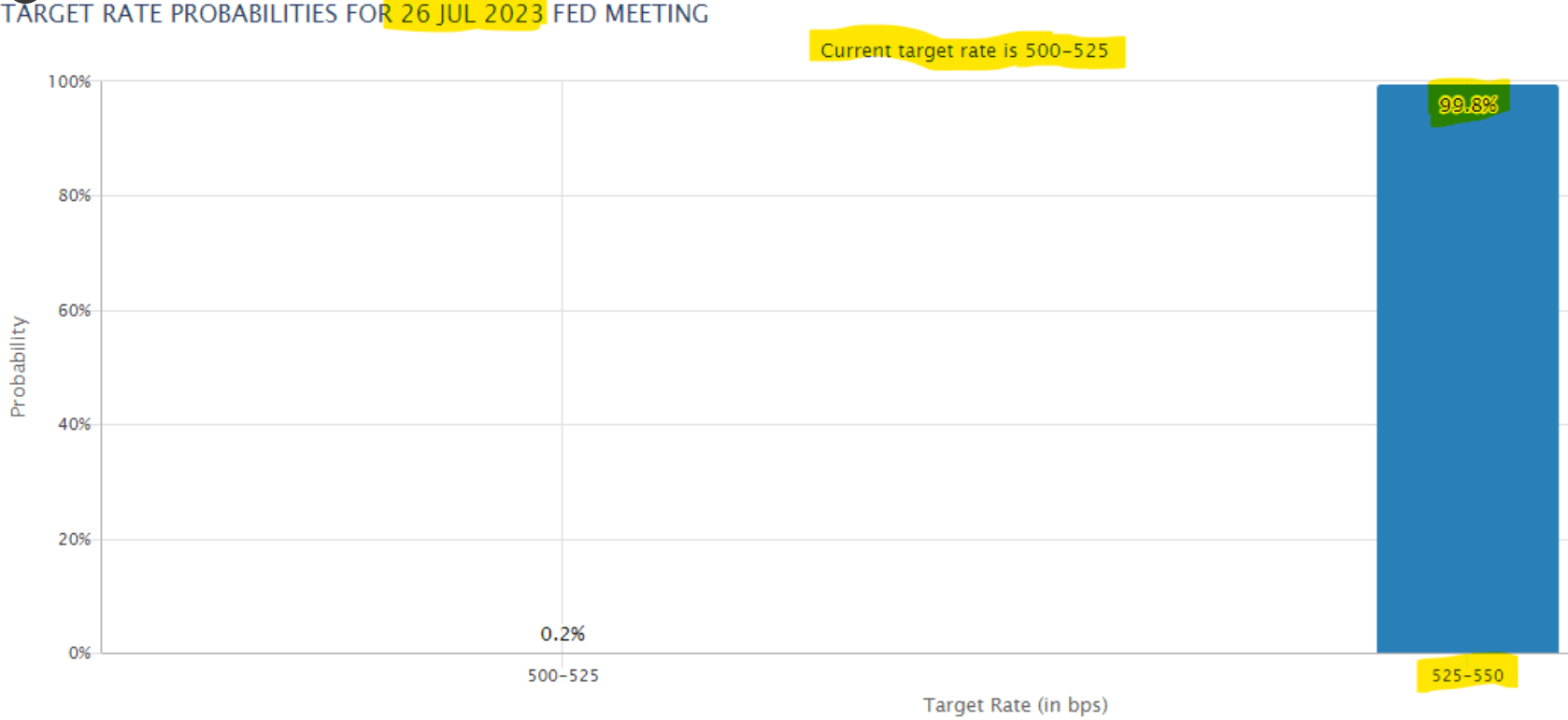

The next Fed meeting is set for the end of July, with the market priced for another rate hike:

Fed Hike Probability (Creative Planning)

{kind=link}

Most economists now predict this is the last Fed hike, which would mean there is no more downside risk coming from higher rates for this name. This fund is very similar to the much better known iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ), but LQD has a much lower duration of 8.4 years, which helped it experience a lower drawdown in 2022:

As per its literature, this fund is set to passively track the Bloomberg U.S. 10+ Year Corporate Index , which:

[...] measures the investment return of U.S. dollar denominated, investment-grade, fixed rate, taxable securities issued by industrial, utility, and financial companies with maturities greater than 10 years.

Via this build you are getting granularity and diversification, and are subject to rates risk and credit spread risk (rather than credit default). We discuss these factors further in the 'Risk Factors' section.

Analytics

- AUM: $6.2 billion

- Sharpe Ratio: -0.48 (3Y)

- Std. Deviation: 14.6 (3Y)

- Yield: 5.48%

- Premium/Discount to NAV: N/A

- Z-Stat: N/A

- Leverage Ratio: 0%

- Composition: Fixed Income - IG Corporate Bonds (Long Duration)

- Duration: 13.2 yrs

- Expense Ratio: 0.04%

Holdings

The fund is entirely composed of investment grade assets:

Ratings (Fund Fact Sheet)

We can observe from the above parsing that the buckets which have the highest representation here are the 'A' and 'Baa' buckets, which are on the lower rungs of the investment grade spectrum. This translates into a higher sensitivity to credit spread widenings rather than actual defaults.

The only pocket of the investment grade bond market that suffered actual defaults this year was represented by regional banks. That sector is now 'fixed' so to speak via the new Fed facility and the robust results recently reported.

From an industry standpoint the largest exposure here is to 'Industrials':

Sectors (Fund Fact Sheet)

The fund has a long duration and an even longer weighted average maturity:

Duration (Fund Fact Sheet)

As a reminder, an investor should focus on duration as a risk factor since it measures the entire cash-flow sensitivity of an asset, whereas maturity just references a point in time when the principal goes to zero:

Duration and maturity are both interest rate risk measures that are not interchangeable. The key differences between duration and maturity are: Duration measures the bond's sensitivity to interest rate changes, while maturity is the time until the bond's principal is repaid.

Performance

The fund experienced a deep drawdown in 2022, as risk free rates rose almost 400 bps for its main risk sensitive bucket, namely the 10-year point:

The above 10-year price chart does a nice job of highlighting what this fund actually does - in a normalized interest rate environment the price is fairly stable, with investors clipping the yield. When rates move down significantly (as they did in 2020/2021), the fund has significant capital gains given its long duration.

Expect more of the same for the future. With the fund yielding 5.4% now, expect significant capital gains as rates move down (roughly 10% gain for every 100 bps of rates decreases in the 10-year bucket).

Risk Factors

As discussed above in the 'Thesis' section, the main risk factor here is represented by rates. The fund had a significant drawdown in 2022 as rates rose. Just like the majority of the economists, we expect the July hike to be the last one this cycle. That would put a lid on losses from higher rates.

The second risk factor here is represented by credit spreads. We assign a very low probability of default to the underlying collateral due to its granularity and rating. Granular portfolios, even when experiencing a couple of defaults, are able to overcome them via the dividend yield. For example, if a name defaults, but it represents only 0.15% of a fund, then its impact is very low. We are more concerned over a temporary widening in credit spreads on the back of a market risk-off event. This type of event could bring a -7% drawdown here.

Conclusion

VCLT is an exchange traded fund. The vehicle holds long dated investment grade corporate bonds, and has experienced a large drawdown in 2022 on the back of higher rates. With most economists now predicting the July Fed hike to be the last one this cycle, the main risk factor for this fund is off the table. The ETF is set to track the Bloomberg U.S. 10+ Year Corporate Index , and has a very granular build, overweight 'A' and 'Baa' credits.

The fund does not really run default risk given its collateral, but is subject to credit spread risk (i.e. widening of the spread to treasuries for investment grade bonds). With the ICE BofA US Corporate Index Option-Adjusted Spread at 125 bps now, we can see this widen to 170 bps as in October 2022. Any such widening would represent a -7% drawdown.

Long term, the forward curve is implying lower rates next year, which will have an outsized positive impact on this long duration fund. We like the risk/reward here, and would start dollar cost averaging into this name, with a 12% plus total return target for the next year.

For further details see:

VCLT: Long Duration Investment-Grade Bonds Look Appealing