XLE - VDE: When The Recession Hits You Don't Want To Be Here

2023-06-19 13:17:04 ET

Summary

- The Vanguard Energy Index Fund ETF is expected to suffer due to the coming recession.

- VDE has a concentration issue, with nearly 40% of its AUM in Exxon Mobil and Chevron, which may affect its broad sector exposure.

- The coming recession, not accounted for in oil price forecasts, will likely lead to a decrease in oil consumption and lower prices, negatively impacting VDE.

Vanguard Energy Index Fund ETF (VDE) tracks the US energy sector. With AUM of about $7.3B, VDE has a 30-day SEC yield of 3.5%. It's no surprise that the energy sector is heavily correlated to the price of oil, and I think current oil forecasts are too high, and when oil consumption goes down due to the recession, VDE will suffer. Along with this, VDE has some concentration issues that concern me. I rate VDE a Sell.

Holdings

VDE holds 117 US energy stocks in order to track the broad market performance of the energy sector. This is far more than its peer, the most popular energy sector benchmark, XLE , which only holds 26 companies. These 117 companies are weighted by market cap but use the MSCI 25/50 method to avoid too much concentration. " No group entity exceeds 25% of the index weight, and the aggregate weight of issuers with over 5% weight in the index is capped at 50% of the portfolio."

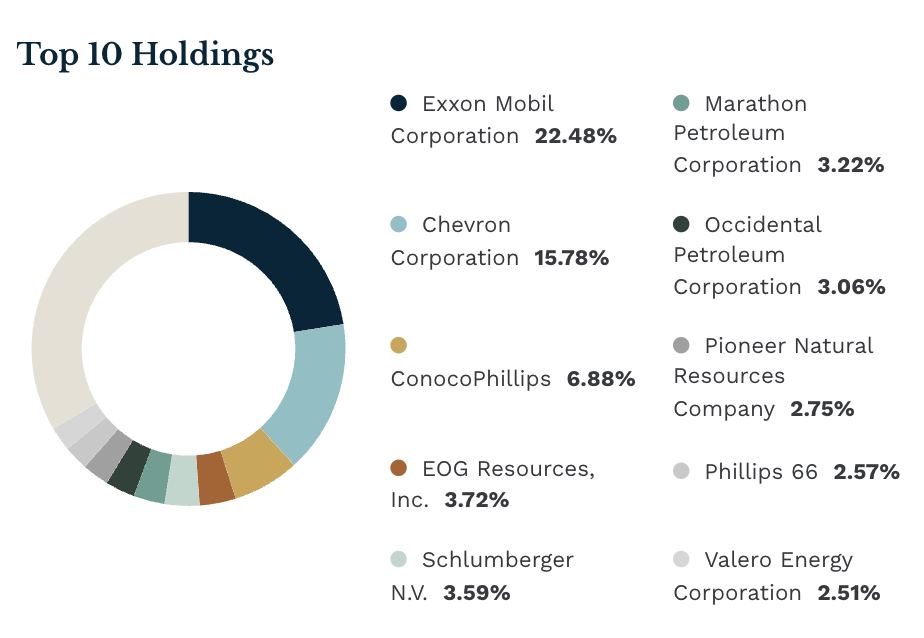

VDE's top 10 holdings make up about 67% of the ETF.

{kind=link}

Even with the MSCI 25/50 method being used, I still see a major concentration issue with Exxon Mobil ( XOM ) and Chevron ( CVX ). In my opinion, having nearly 40% of its AUM in 2 companies takes away from the broad sector exposure. This isn't just an issue with VDE, but with most energy sector benchmarks like XLE .

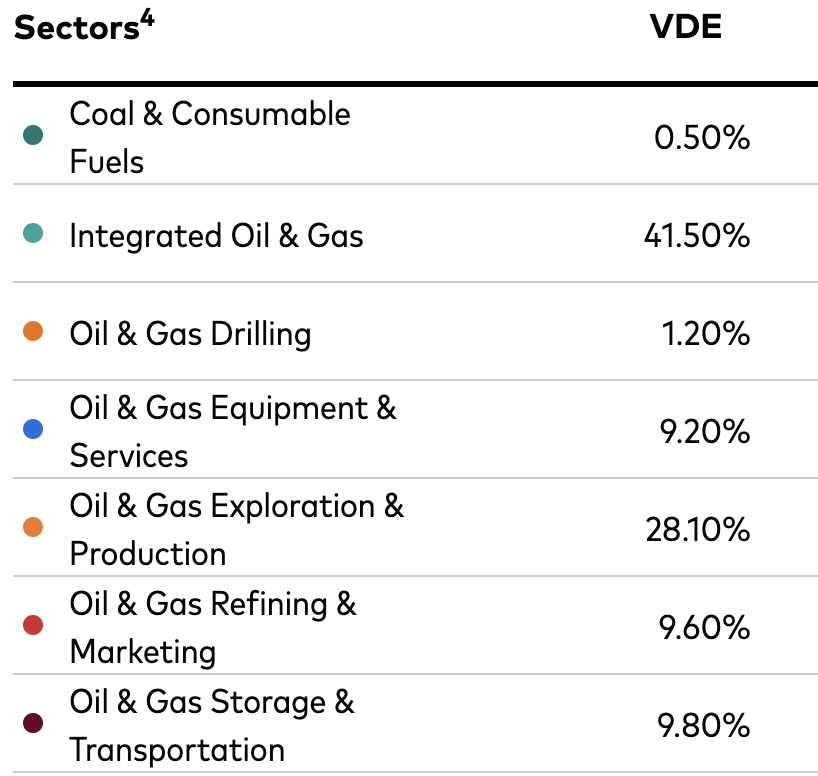

Within the energy sector, VDE has good diversification between upstream, midstream, and downstream companies.

VDE's holdings by service (vanguard.com)

{kind=link}

VDE and oil correlation

My argument for why I believe VDE will drop in price is based on my belief that oil prices will also fall in the next 12 months. Therefore, I will quickly show how VDE and oil prices relate. It's no surprise that VDE is highly correlated with oil. The chart below shows the correlation between 1-year total returns of VDE and [[USO]], a US oil fund.

Although it does stray from 1 (perfect correlation), there's no denying that they are closely correlated. The correlation sits around 1 most of the time, and if it falls, it quickly goes back to around 1. The current correlation is about 0.98.

Why I think oil forecasts are wrong

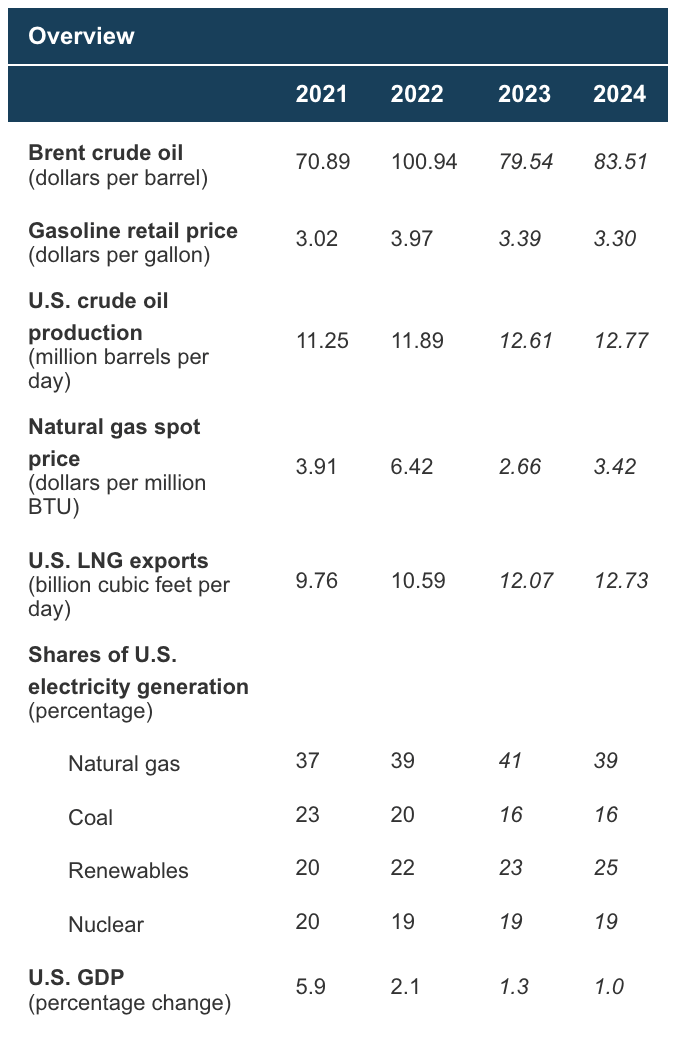

Most 2023 and 2024 oil forecasts have the price of Brent oil being higher than it currently is. These forecasts have one thing in common-they aren't predicting a recession. The EIA is currently predicting Brent prices in 2023 and 2024 to be $79.54 and $83.51 respectively.

{kind=link}

If you look down at the bottom of the chart above, you will see the EIA's GDP predictions. For 2024, they are predicting a 1% growth in GDP. I think this is an overestimate. There is a real chance that we will have negative GDP growth in 2024 because of the recession that I predict is on the horizon. The EIA is predicting Brent to rise from current levels and average $83.51 in 2024, but this prediction is based on predicted 1% GDP growth.

We see the same thing with Goldman Sachs' forecasts. They recently cut their 2023 oil forecast from $95 a barrel to $86. Although the forecast was cut, $86 is still well above the current Brent price of about $76 per barrel. But again, Goldman Sachs also doesn't forecast a recession within the next 12 months, sitting only a 25% chance .

If we enter a recession, consumption will fall, leading to cheaper oil. The coming recession isn't being taken into account with these forecasts. If they were, the forecast would be much lower.

The coming recession

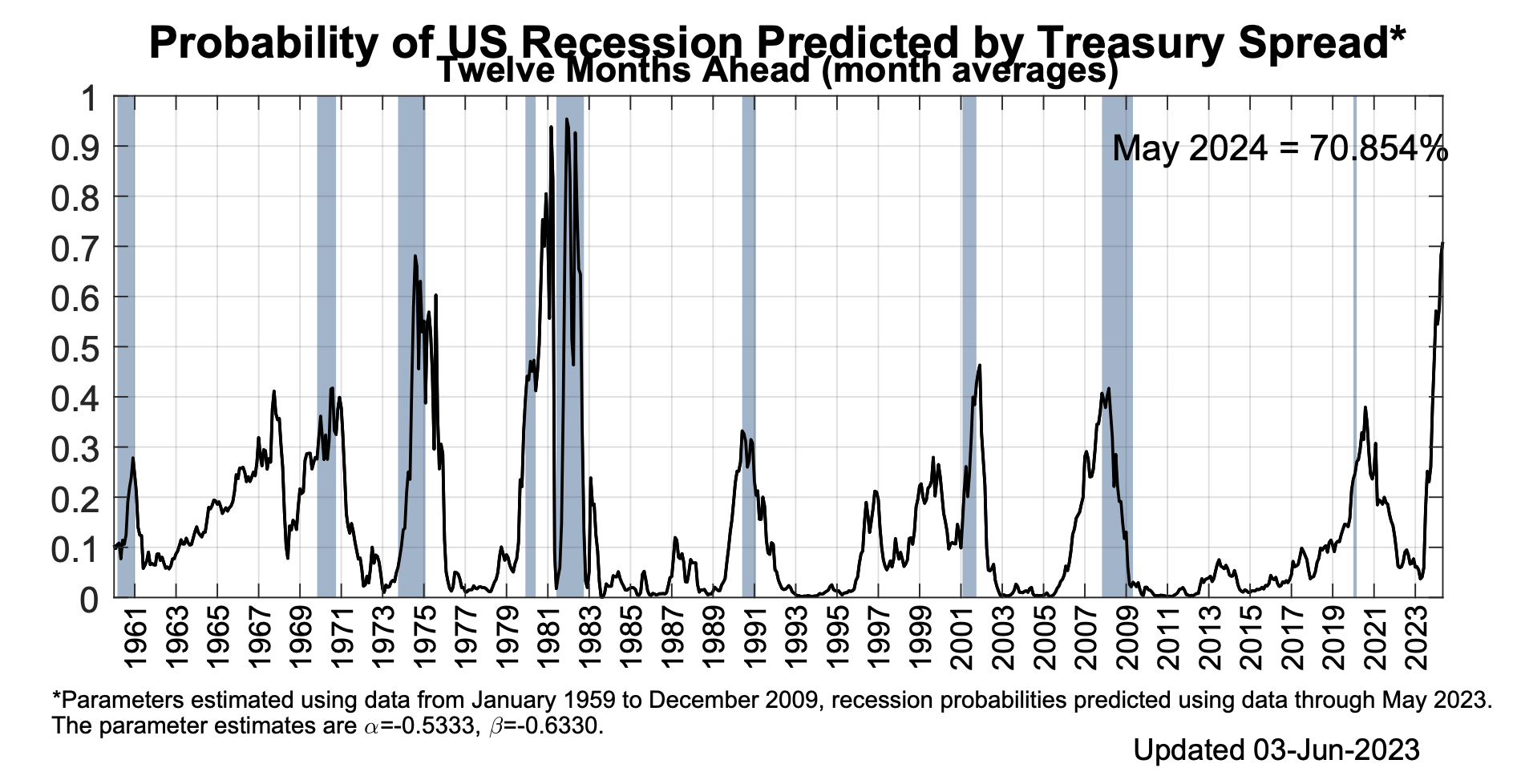

My thesis lies in the idea of a recession in the near future. Probably the best source to back up my claim is the New York Fed. The New York Fed model predicts a 71% chance of a recession in the next 12 months.

Recession chance (newyorkfed.org)

{kind=link}

As the chart above shows, this model has a pretty good track record of predicting a recession. With that being said, the likelihood of a recession in the next 12 months is at a level that hasn't been seen in over 4 decades.

Looking at Fed Chairman Powell's June rate hike pause announcement also tells us a lot. Although in June, we just had an encouraging CPI headline, the increase in core CPI hasn't budged in the last 3 months. The economy is still dealing with very sticky inflation, and the Fed seems determined to get it back down to the target rate. After the June pause, Powell said to expect 2 more rate hikes in 2023. This really shows the Fed's commitment to lowering inflation. He also said that it will be a couple of years before any rate cuts. These high-interest rates will ultimately lead to a recession, causing oil prices to fall.

Conclusion

VDE offers broad market exposure to the energy sector. However, with 2 companies making up nearly 40% of its AUM, I believe there is a concentration issue. Although there are many forecasts saying that the price of oil will rise, they don't take into account a recession that I believe is coming. Because of all this, I rate VDE a Sell.

For further details see:

VDE: When The Recession Hits, You Don't Want To Be Here