VGR - Vector Group: A Good Market Position And A Sustainable Dividend

2023-04-11 03:12:24 ET

Summary

- Vector’s market position with value brands has been a huge tailwind for their revenue growth.

- Vector’s management is acutely aware of leverage and manages the balance sheet well.

- The dividend at Vector is safe for the foreseeable future.

- Risks are nothing new in the tobacco industry and Vector has proven its ability to navigate them.

- VGR stock is a strong add to any dividend portfolio.

Vector Group (VGR), with a market cap of $1.92B, is a holding company in the consumer staples sector, operating both tobacco and real estate subsidiaries. In 2021, they spun-off Douglas Elliman, a large real estate brokerage. Today, their subsidiary New Valley has a collection of real estate investments while Liggett Vector Brands covers the tobacco portion of their operations. Liggett is differentiated from many other tobacco companies as they are focused on discount and value brands. They are currently the fourth largest US cigarette manufacturer with roughly 5.5% of the wholesale market.

Revenue

Over the last 10 years, Liggett has managed to increase their market share and unit volume in the tobacco segment, which makes them an outlier in comparison to other cigarette manufacturers. When examining the historical numbers at VGR, it is important to note that Douglas Elliman was spun off, so the drop in revenue was not attributable to poor operations. After the spin-off in 2021, VGR actually saw double-digit revenue growth from $1.2B to $1.44B in 2022.

They are proven operators and with questions swirling about the economy, there are likely tailwinds for the value brands that they operate in the tobacco space. Tobacco is of course under regulatory assault, but as long as it's around the prices will continue to climb. I really like the positioning of VGR's value brands at this time.

As I previously mentioned, Vector does still have a real estate subsidiary, but revenue was negligible at just $15.8mm in 2022. The tobacco segment is what will enable this company to pay dividends for many years.

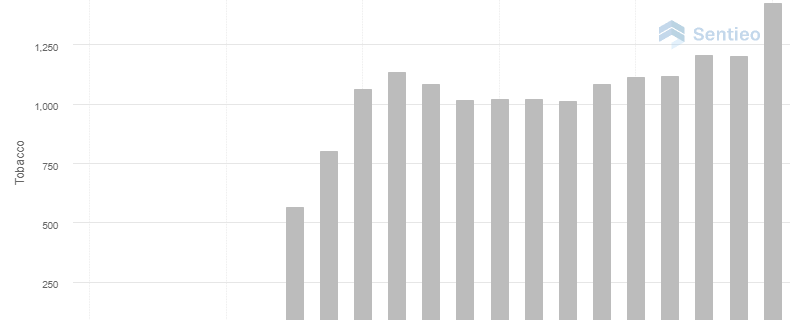

Here is a chart of the growth of VGR's cash cow tobacco segment, back to 2006:

{kind=link}

What's so astounding here is that even with strong regulatory and social pressures they've managed to keep it not just stable, but actually grow the segment! Now if that's not exciting, I don't know what is.

Valuation

Let’s keep in mind that the makeup of this business has changed in the last two years with the spin-off of Douglas Elliman. It would not be prudent to compare past multiples to current multiples, as the holding company now gets almost all of its revenue from the tobacco segment.

As of year end 2022, VGR stock is trading at 2.2x EV/Sales, this is well below its closest peers. British American Tobacco (BTI) trades at 3.72x, Altria Group (MO) trades at 4.93x and Philip Morris (PM) trades at 6.2x. The discrepancy in multiples can mostly be attributed to the operating margins at each company. Vector's TTM operating margins are 23%, while Philip Morris saw operating margins of nearly 40% and Altria was closer to 60%.

With the operating margins in mind it becomes clear why we have the differing valuations, so in my opinion I'd have to say its most likely fairly valued.

Debt

At the end of the day, the reason to own Vector is the dividend, so evaluating the balance sheet is extremely important. Vector does have a significant amount of total debt, $1.4B, and the net debt position is just under $1.2B. The vast majority of the debt is long-term, and after the spin-off of Douglas Elliman, interest coverage is a solid 3.1x so servicing it isn't a problem.

They do have a few high interest notes, 5% and 10% senior notes, due in 2029 and 2025, respectively. These high interest notes come with indentures that significantly restrict their ability to act (including paying dividends) if they cannot pay the interest. Now at this time I have no reason to believe they can't pay the interest, but this is a risk that you should be aware of. See their FY 2022 10-K Page 22 for their full disclosures around these notes.

Dividends

The real reason to own a tobacco stock is the for the dividend, and boy did VGR have a great dividend. Now in 2020 they had to cut it, after raising it nearly every year for 20 years. Given what happened in 2020 this makes sense.

Prior to that cut the payout ratio was unsustainably high. After the cut they're still yielding a fantastic 6.5%, and the payout ratio is much closer to what I'd consider sustainable. Preferably I'd want to see below 60% there, and it's still a bit over, but is better than before.

Considering they are still growing EPS, we do not fear that this dividend will be cut anytime soon. The cash flow situation at VGR is solid and management has made it clear that the dividend is a priority, paying out a large chunk of the free cash flow every year. This makes me comfortable in owning VGR for the dividend income.

It's worth noting that, prior to the cut in 2020, I wouldn't have been comfortable. The payout ratio was just too high, and it was apparent they were using funding other than earnings to help pay those dividends. Which takes us to the next section.

Shares Outstanding

The share float is one of the big things I like to look for in a bird's eye view of a company. A company that buys them back is returning value over time to its shareholders. A company that issues them needs the money for some reason. Given VGR's previously extraordinarily high dividend payout ratio I believe they were issuing them to help gain additional cash flow to pay the dividends to shareholders.

Shares outstanding has remained relatively flat ever since the Douglas Elliman spin-off was complete. There's always the risk in the future that they'll offer more shares, so this is something that the wise investor needs to keep on the lookout for. They did file offering paperwork in Sept 2022, but so far it doesn't look like they've issued a considerable amount of shares. At this time, being that the dividend was dropped to a sustainable level, I'm not concerned.

Risks

The tobacco industry, and more specifically cigarettes, are a melting ice cube. Taxes, regulation and fines, and non-tobacco nicotine alternatives all present challenges for VGR. With that being said, Vector has managed to navigate all of this for many years, and management is well aware of the risks. Now that Douglas Elliman is spun off, this is priced into the multiple. The ESG movement in general makes this name tough to own for many, that is why the dividend yield is fairly high.

Because of regulatory risk, just like its peer group, owning VGR comes with its own set of problems. The dividend focused investor would do well to have this as only a small part of their portfolio, and not lean heavily into the tobacco sector. At any time we can see new litigation and legislation on the horizon that can throw the company into turmoil.

Management

The current CEO, Howard Lorber, has managed New Valley and Vector, along with Douglas Elliman, since 1994. He has guided the company through tons of regulatory changes and through litigation related to the tobacco industry. You can sleep well at night knowing that a seasoned operator is at the helm of VGR.

Unfortunately there are very few employee reviews of this company on Glassdoor. I always love to see what employees say because of how often employee buy-in will make or break a company. In this case the employees seem to be middle of the road with a 3.6/5 star aggregate review, and 80% of them approving of the CEO.

Conclusion

Regulation and new non-tobacco nicotine products have completely disrupted cigarette manufacturers. Despite this, Vector Group has shown earnings growth and taken market share in the cigarette space over the past few years. The ESG movement and mandates at many institutional investors have also contributed to the beat down of tobacco stocks.

Taking this all into consideration, Vector has a healthy balance sheet and we do not see any short-term threat to their dividend. If you are looking to add a to your dividend income, Vector Group is a good place to start. The most important thing to note is that if you do own this stock for the dividend, you need to keep an eye on any regulatory changes and follow earnings closely. At the first sign of a threat to the dividend, it would be time to sell. But for now I'll give a buy rating for your dividend focused portfolio.

For further details see:

Vector Group: A Good Market Position And A Sustainable Dividend