IQV - Veeva Systems: Its Strong Moat Might Extend To The SMB Sector

2023-09-21 17:32:46 ET

Summary

- Veeva Systems is executing well its migration plan from Salesforce to Veeva Vault CRM, positioning itself for double-digit revenue growth.

- Better than expected Q2 2023 results with revenue of $590.2 million and GAAP net income increasing 23%.

- Veeva's strategy to target the SMB sector is proving successful, attracting new clients with its high-quality software and integrated collection of products.

- We rate the stock as a buy.

We rate Veeva Systems (VEEV) as a buy as the company is executing well its migration plan from Salesforce (CRM) to Veeva Vault CRM while developing future growth avenues that might help the company secure double-digit revenue growth for the next few years. In our last article in December 2022: Veeva Systems: The stock is not expensive ; we've identified that the small and mid-size biotech companies ((SMB)) segment was a sector where the company needed to work hard to develop a moat as strong as that of the big pharma industry, so we were more conservative in rating the stock as a hold given the saturation in the big pharmaceutical sector and the difficulties associated with growing in the SMB sector. The strong competition from IQVIA (IQV) and the not-so-well-known name of Veeva in the SMB sector were two of the most important obstacles for the company to gain a name in the segment. Nevertheless, Veeva is taking interesting steps to be successful in the SMB sector, as we will discuss in the article, which has made us change our view about its future.

Better than expected Q2 2023 results

The results in the second quarter of 2023 were better than expected, as revenue achieved $590.2 million, increasing 10% Q2 YoY, whereas GAAP net income increased 23% in the same period. Non-GAAP adjusted net income reached $1.21 per share, up from $1.03 per share in Q2 YoY, as analysts, on average, were expecting adjusted net income of $1.15 per share and revenues of about $583 million.

Long-term growth opportunities are still there

Migration to Vault CRM from Salesforce is going well

We should remember that Veeva has a contract to use Salesforce's platform that ends in September 2025 and a five-year winding-down period during which Veeva might continue using the Salesforce platform combined with some of Veeva's solutions for its customers. Nevertheless, during this five-year period, there will be limitations on the additional subscriptions Veeva can sell to its existing clients.

During the first half of 2023, Veeva was working on the migration of its clients from the Salesforce platform to Veeva Vault CRM as expected, but CEO Peter Gassner expected early adopters for its Vault CRM in 2024 in the call for the Q1 2023 results. Nevertheless, in the call for the Q2 2023 results, Gassner said that Vault CRM had already gained its first client.

It was supposed that the early adopters would be Veeva's current clients that are under the Salesforce platform right now; nevertheless, an entirely new client is adopting Veeva Vault CRM, which indicates that the management is taking solid decisions to prevent disruptions in the middle of a migration process while attracting new clients to its own CRM platform. That reveals the excellence of the management's execution since a normal scenario would have been a more difficult migration process from one platform to another without attracting any new clients to the new platform.

On the other hand, under the contract with Salesforce, Veeva is not allowed to operate in certain sectors, such as the medical device industry or products for non-drug departments of pharmaceutical and biotechnology companies. However, once the migration to Veeva Vault CRM is completed in 2025, Veeva will have the chance to get into those new sectors gradually, which are not only comprised of big companies but also of SMBs.

Veeva's approach to targeting the SMB sector

Veeva's strategy to keep developing business with each client is critical to understanding its future growth opportunities not only in the big pharmaceutical sector but also in the SMB sector, as mentioned in the last call by Peter Gassner :

One of our special things is this multi-product company approach, our operating model that allows us to do that. So, excellence in an area like clinical or quality or safety, but because we have a lot of autonomy in those areas, we can go deep in those areas and provide the full suite of things, not just the surface level. So, if we look actually in clinical, there's not been a company that has attempted to do the full broad suite of clinical applications such as Veeva is trying. Nobody has attempted that before, let alone succeeded at it. So, it is absolutely our strategy to go in each area with autonomy, deep in each area with excellent applications, the main ones that people need, and then have things aligned across areas on a common set of values.

We know that Veeva has a rock-solid position among the big pharmaceutical companies in the industry, offering a collection of software in different areas while building more and more new applications in those areas, and that's how Veeva has solidified its position over the years in the pharmaceutical industry.

For example, Veeva started its suit for clinical data in 2013, offering the Veeva eTMF, a unique software that manages documents in real time and substantially improves supervision. Then, in 2017 , Veeva launched its Vault CTMS to manage the end-to-end clinical trials. That's how the company keeps developing more high-quality software based on the cloud around one specific area, going more deeply into that area, and generating more stickiness toward its products.

The SMB sector is well known for being more sensible in macro headwinds, as they face higher restrictions on funding, so they face difficulties supporting their clinical trials to expand their operations under those scenarios. Nevertheless, the SMB sector is finding that Veeva's products are outstanding, giving them so much value in different areas.

As of the first half of 2023, Veeva has attracted 11 SMBs in Q1 and 8 more in Q2, despite the fact that it's way more difficult to play in that sector with more competition there like that of IQVIA. The reason behind this is the high-quality software offered by Veeva, which truly contributes to adding value to clients, making the work easier for the users.

To illustrate the higher efficiency of Veeva's products that are attracting the SMB sector, Peter Gassner mentioned in the last call for the Q2 2023 results an interesting example of a study amendment. Using the competitor's products, one would need to change the design of the study, unloading and reloading the data while the clinical research site cannot be operated at that time. Conversely, Veeva offers a newer architecture whose tooling enables clients to build their studies, defining them substantially faster; instead of taking 8 weeks, Veeva's software can reduce that time to only 4 weeks.

In addition, the competitor's software requires much custom programming that is expensive and also requires specialized skills, whereas Veeva's products do not require those skills as the software, due to the way they were designed, requires much less custom programming.

Another interesting factor that is helping Veeva penetrate its products in the SMB sector is the value generated through the integration of its different software. For instance, Veeva has a great clinical trial management system and a great EDC system; the client does not need to use both, but if it uses both, these different systems work even better through the integration. Another example is that Veeva's ePRO system and its RSTM system work well if the customer does not have the Veeva EDC; none the less, integrating the three systems offers an even better value for the client.

There are different providers of those systems, but any of them can offer a complete and fully integrated collection of software to develop different areas, and that's what makes Veeva a very hard player to compete with in the SMB sector. Once a company from the SMB sector buys one software from Veeva, it realizes that it's even better to have an integrated collection of software for a specific area and then to start buying other Veeva's products to work in other areas. The integration of the different softwares and how deep those softwares are in each area are what is giving support to Veeva in the SMB sector, adding to the fact that it is way better for a client to have one supplier that covers software for all the critical areas rather than several suppliers covering those areas.

One interesting point to highlight is the price of the services since IQVIA's more affordable price tag is more appealing to the SMB sector; for example, for full access to produce, version, and host all material within the platform, a VEEVA certification costs $10–15,000 per year for teams, while IQVIA is just $3,000. It's interesting that with such a meaningful difference in prices, Veeva is advancing well in the SMB sector, and apparently, the new clients are discovering that the value received is way higher than the price paid.

Veeva's business model is stronger than IQVIA's

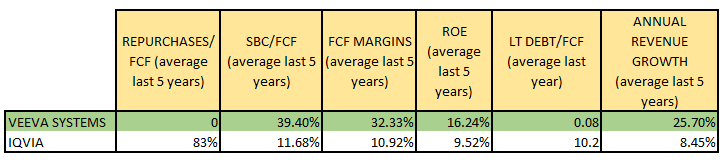

There are several smaller competitors in the SMB sector, but IQVIA is the competitor with a similar size to Veeva that, at first glance, might represent a threat to its market position. However, just looking into certain critical metrics, we could see that Veeva is way better managed to support its future growth than IQVIA:

{kind=link}

In the table above, we can see that IQVIA has allocated an important percentage of its free cash flow ((FCF)) to make repurchases in the last 5 years. Nevertheless, repurchases are not always something positive for shareholders, particularly if the company needs those resources to keep reinvesting in its own business to strengthen its market position within the sector. You can read our article, Intel: The Patient Investor Might Benefit, where you will find a similar problem with Intel (INTC), which was undergoing huge share buybacks for years, whereas Taiwan Semiconductor (TSM) was doing the opposite.

The result of this is that Veeva has a strong advantage as the company is using all its FCF to reinvest in its own business, generating more innovation, and going deeply into different areas, which is critical to being successful in the SMB sector. Also, Veeva's very low long-term debt combined with its very good FCF margins indicate that the company is using its own resources to finance its projects to launch very good and innovative products at higher prices than those of the competition while being truly appreciated by the market.

Conversely, looking into the column of the LT Debt/FCF, we may see that IQVIA is holding a very high long-term debt, which is clear result for using all its money generated in share buybacks. In other words, if the company is using most of its FCF for share buybacks, it will need to get other sources of funding to support its future growth, either through acquisitions or reinvestment in its own business. In this particular case, IQVIA decided to get into more debt.

Now, the problem is that IQVIA might be subject to more debt restrictions through covenants and interest rate hikes, affecting its bottom line and weakening its financial support for future long-term growth. In addition, IQVIA's lower FCF margins and lower ROE than those of Veeva indicate that the company is not executing adequately since offering cheaper products does not mean that demand will rise as a result, particularly if the market, in general, perceives that the value generated by those products is lower than the price asked for them. The latter might be inferred by the lower revenue growth of the company compared to Veeva's.

Last but not least, IQVIA not only has allocated most of its FCF for share buybacks, but also its stock-based compensation ((SBC)) over FCF is way lower than that of Veeva, which might be seen as a sign that IQVIA is a more shareholder-oriented company than Veeva. However, we believe that would be a mistaken interpretation since a real shareholder-oriented company would also show way better ROE and FCF margins combined with low long-term debt. As such, share buybacks and low SBC/FCF are not good enough indicators by themselves to determine if the company is shareholder-oriented.

Looking into these simple metrics, we may see that Veeva has a more sustainable business model with more money to reinvest in its business than IQVIA, generating better returns and FCF margins as a result of its higher revenue growth, which comes from its culture, organization, and way of executing its operations.

Valuation

According to Seeking Alpha , Veeva appears to be expensive in every metric; however, we need to consider that all these metrics are compared with companies that belong to the healthcare industry, but the great majority of them are outside the very niche segment of Veeva, so we will need to use another method to calculate the intrinsic value of the company.

{kind=link}

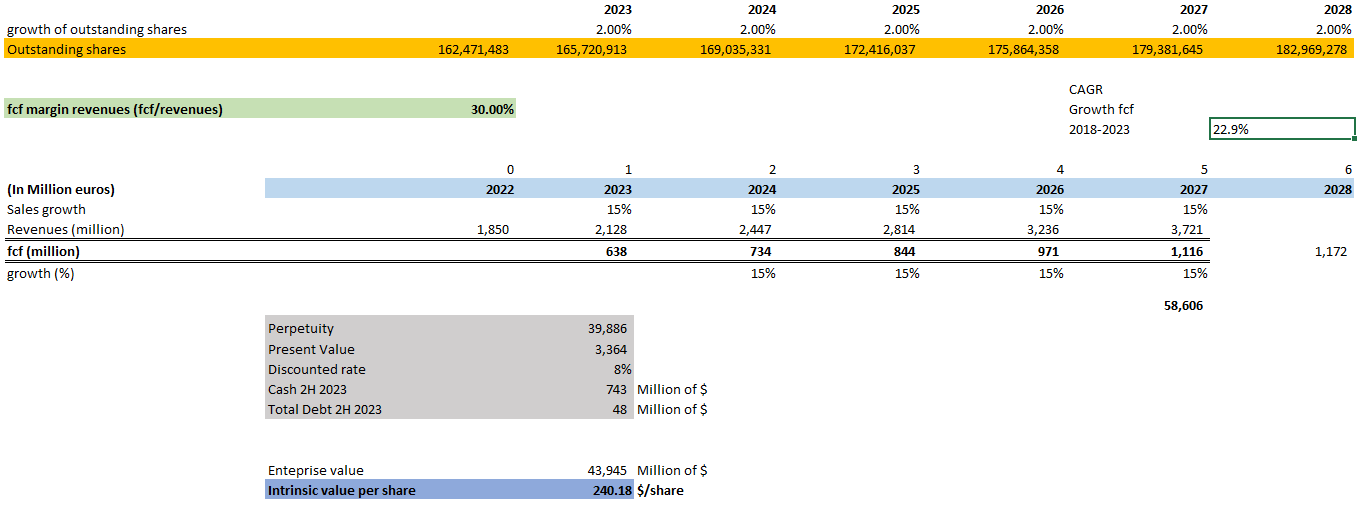

We will use the discounted cash flow ((DCF)) method, so we will need to make certain assumptions aligned with the management's expectations:

Assumptions

- Outstanding shares: 165,720,483 (growing at 2% annual as a result of SBCs)

- FCF margins: 30% (average of the last 10 years)

- Revenue growth: 15% annual (aligned with what the management said in the last call and confirming its target of $2.8 billion in revenues for 2025).

- Cash as of July 2023: $743 million

- Debt as of July 2023: $48 million

- Discounted rate: 8%

- FCF growth in perpetuity: 6% annual (CAGR FCF growth from 2018 to 2023: 22.9%)

{kind=link}

To find the perpetuity, we used the formula:

Perpetuity = FCF 2027/(discounted rate - g)

where g = FCF growth in perpetuity, which was assumed to be 6% annual

With perpetuity, we calculate the present value of all the FCFs beyond 2027. Then, we calculate the enterprise value using the following:

Enterprise Value = Present Value of FCF (from 2023 to 2027) + Perpetuity + Cash + Total Debt

Finally, the intrinsic value is calculated by taking the enterprise value and dividing it by the outstanding number of shares. In this way, we could get $240 per share under the assumptions presented.

Now, we can build a sensitivity analysis to see how our results might change when some assumptions are modified:

Author

If Veeva keeps working to keep its strong FCF margins of around 30% while delivering a FCF growth of more than 6% annually into perpetuity, the price could reach a range between $240 and $364 per share in the long term. Those are feasible results, as the company generated an average of 37% of FCF margins in the last 5 years and achieved a FCF growth of 22.9% CAGR in the last 5 years.

Risks

The SBC of the company is growing faster than its cash flow from operations; this has the effect of increasing the outstanding number of shares by 2% on average year over year. We've incorporated this factor of dilution in the intrinsic value calculation. If that rate grows faster than 2% in the next few years, our calculation of the intrinsic value would be overestimated. However, this rate has been decelerating clearly in the last five years: 0.06% in 2023, 0.93% in 2022, 1.58% in 2021, 1.37% in 2020, 1.39% in 2019, and 5.33% in 2018. So, apparently, Peter Gassner is well aware of the dilution related to stock-based compensations to attract better professionals to the company, so this rate is being reduced year over year, and that's good news.

If the revenue growth falls to unexpected levels in the next few years as a result of different factors such as a recession scenario, competitors becoming stronger than Veeva, etc., our intrinsic value would be lower than our estimations. We cannot take for granted anything about the future, but at least we can play with probabilities, knowing how good the management's execution is. In this way, we could estimate that under Peter Gassner's leadership, Veeva has a very good chance to succeed in the next few years, just following its current innovative culture and its very good capital allocation.

Finally, Veeva has been in the process of litigation with IQVIA since 2017 due to assertions of infringing intellectual property rights by Veeva. There are counterclaims and countersuits from Veeva that might significantly reduce any claim or suit from IQVIA. There has been nothing new since our last article in December 2022 related to this matter. However, in July 2023 , the Federal Trade Commission ((FTC)) blocked an important deal from IQVIA to prevent a monopoly in the digital pharma ad market. This blocking is not related to the problem with Veeva about the intellectual property, but it certainly does not play in IQVIA's favor to win its case against Veeva.

We'll need to follow up on this litigation since it's unclear when the final results will be, but we expect that whatever the result, it will not materially affect Veeva's growth prospects.

Final thoughts

Veeva Systems is a very interesting company that deserves to be on your radar. The company serves a very specialized sector with high barriers to entry. In my opinion, these high barriers are shaped by the way the company operates, offering a wide range of high-quality software that covers several critical areas within the pharmaceutical industry.

The relatively higher PER might deter some investors from looking into this company, but most likely, it might be justified given its strong position in a very niche sector within the pharmaceutical industry and the high-quality management's execution to deliver future value. In this sense, Veeva can take advantage of the SMB sector as it offers increased complexity, delivers excellent and innovative products, focuses on customer success, which is critical in shaping its competitive advantages in the SMB sector, and strengthens its reference selling, which means that early adopters are the best advocates for Veeva's products and software.

We should follow up on the migration process toward the Veeva Vault CRM from the Salesforce platform, as even though Veeva has not mentioned so much about the growth opportunities that this could bring, given its good relationship with Salesforce, there would be growth avenues in different industries that might support Veeva's long-term growth once this contractual relationship with Salesforce ends in 2025.

For further details see:

Veeva Systems: Its Strong Moat Might Extend To The SMB Sector