VNTR - Venator Materials: Insolvency Seems Just Around The Corner

2023-03-19 02:52:39 ET

Summary

- Venator Materials booked a $228 million loss for Q4 2022 due to restructuring charges and weak demand for its products.

- The current portion of the debt has surpassed $1 billion and Venator anticipates the violation of certain debt covenants.

- The available borrowing capacity had shrunk to just $37 million as of February 17 and I think that insolvency is on the cards.

- The short borrow fee rate is just 3.92% but short selling seems dangerous due to high share price volatility and limited hedging options.

Introduction

I've written three articles on SA about UK-based titanium dioxide producer Venator Materials (VNTR). The latest of them was in December 2022 and in it I said that the company's Q4 financial results were likely to be even more underwhelming than the ones for Q3.

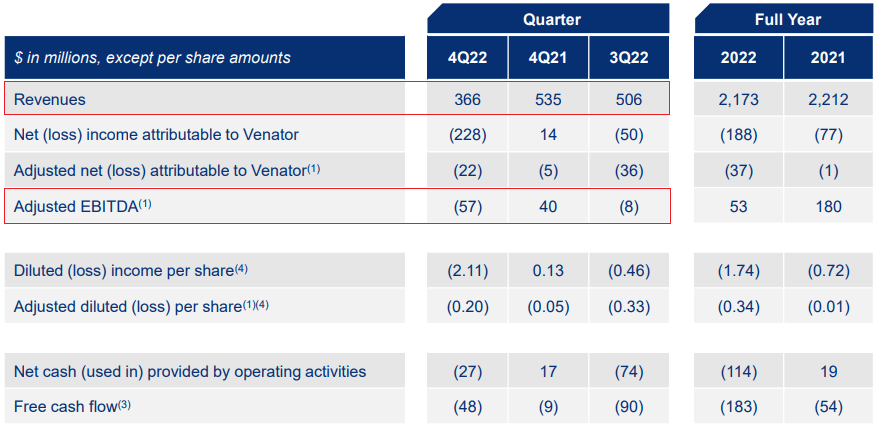

Well, it seems I was right as Venator booked a $228 million loss for Q4 due to restructuring charges and weak demand for its products. The future of the company looks grim as Q1 2023 adjusted EBITDA is expected to be even lower. In January, Czech private equity fund J&T MS 1 SICAV revealed that it had amassed a 14.3% stake and is pushing for board changes in a bid to improve the fortunes of the company. Well, I think that it's too little too late now as insolvency seems to be just around the corner. Let’s review.

Overview of the latest developments

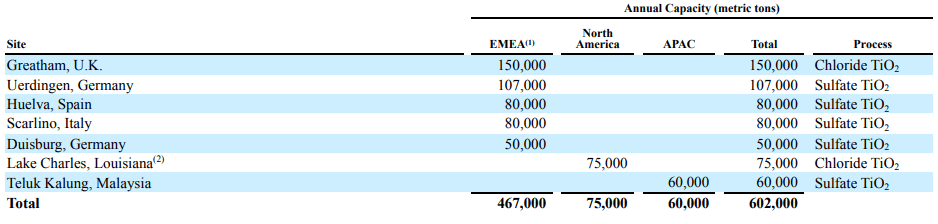

In case you haven't read any of my previous articles about Venator, here's a short description of the business. The company specializes in the production of titanium dioxide, functional additives, color pigments, and timber treatment products. Titanium dioxide is used mainly in products such as paints, sunscreen, and toothpaste and this business accounts for about two-thirds of Venator’s revenues. The company is focused on Europe, and it has 20 manufacturing facilities across nine countries with a total nameplate production capacity of around 937,000 metric tons per year. A total of seven of those are titanium dioxide manufacturing facilities and they have a nameplate production capacity of about 602,000 metric tons per year, putting Venator among the four largest global titanium dioxide producers in the world.

{kind=link}

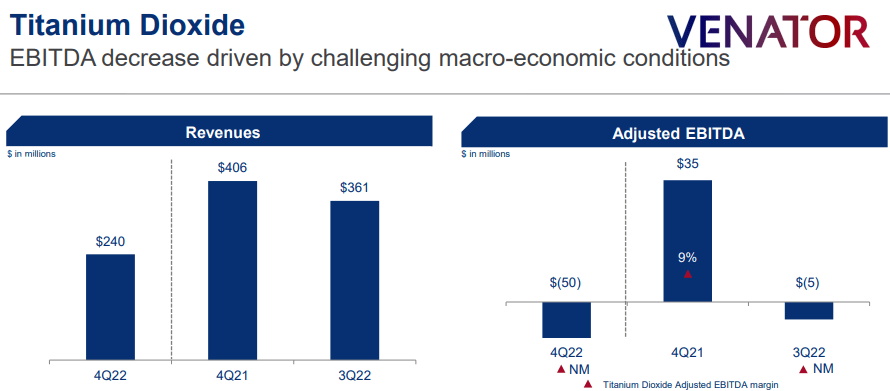

Turning our attention to the Q4 2022 financial results, net revenues slumped by 31.6% year on year to just $366 million and adjusted EBITDA was negative $57 million. The main reason behind the deterioration of the results was a 28% decline in volumes in the titanium dioxide segment due to customer destocking as well as low levels of demand.

{kind=link}

{kind=link}

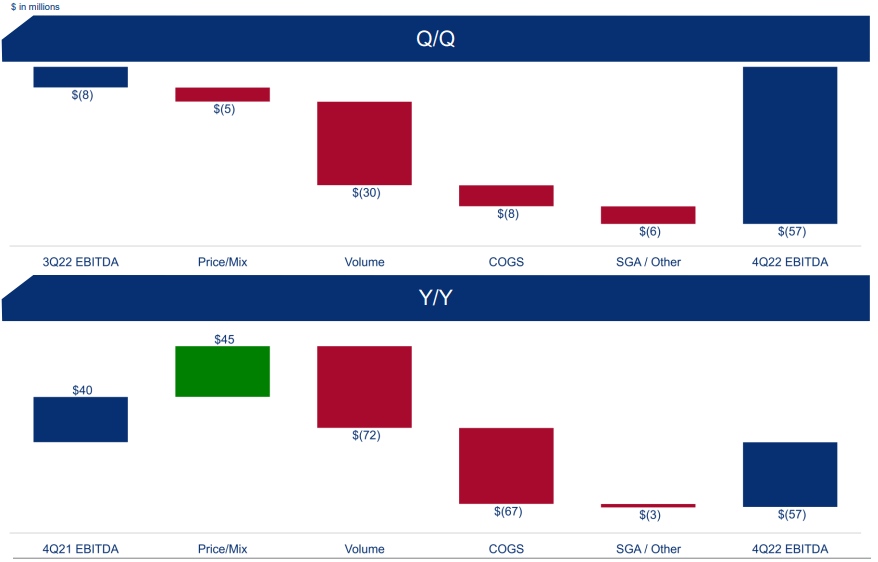

Operating margins were also put under pressure by high raw material and energy costs, especially in Europe. Looking at the numbers, the company was unable to pass on cost increases to its customers, with the cost of goods sold rising by $67 million year on year.

{kind=link}

Venator revealed that sales volumes for its titanium dioxide segment were beginning to recover in Q1 2023 (see slide 5 here ) but I’m concerned that some of the production facilities are experiencing significant operating challenges. The Duisburg plant was shut down in Q4 and while Venator plans to restart it in the future, the company revealed in its 2022 annual report that it does not believe it is economically viable to continue titanium dioxide production there longer term due to low margins (see page 52 here ). In addition, the Scarlino facility is operating at one-third of its nameplate capacity due to limited gypsum storage capacity, which is negatively affecting margins. You see, this facility generates gypsum from the manufacturing process, which has been mainly landfilled on-site. If the company doesn’t receive approvals for additional gypsum storage capacity soon, it may have to close the facility as its gypsum storage capacity is running out. It’s possible that the Scarlino facility shuts down in the second quarter of 2023.

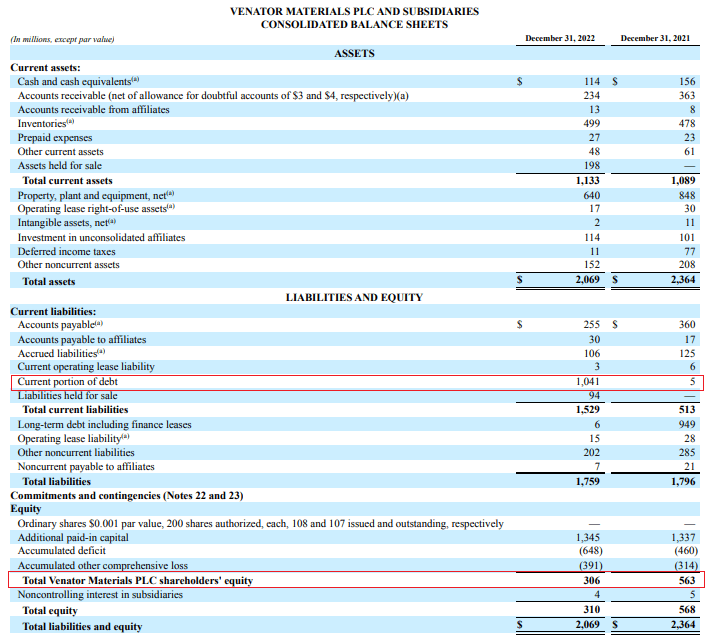

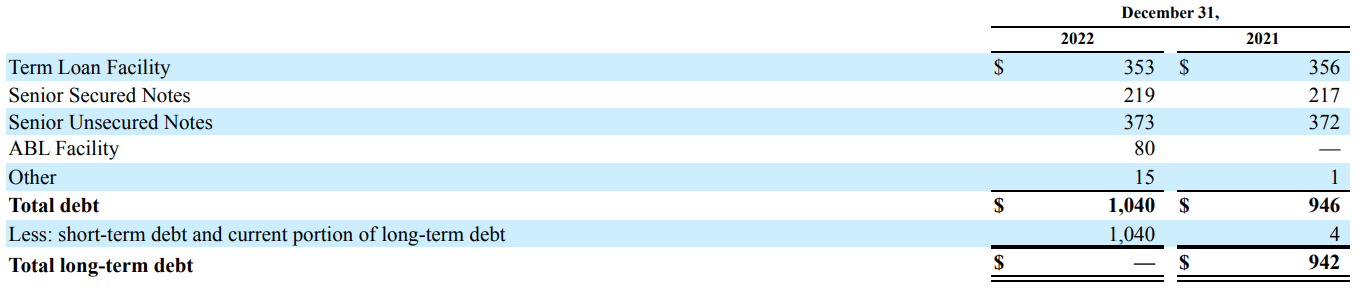

Turning our attention to the balance sheet, the situation looks grim as the current portion of the debt has surpassed $1 billion while shareholders' equity slumped to $306 million in Q4. The main reason behind the latter was $121 million in impairment and restructuring charges during the quarter. In November, the company inked an agreement for the sale of its iron oxide business at an enterprise value of $140 million and it had to write down the carrying value of the assets to the fair value less cost to sell.

{kind=link}

Looking at the debt situation, Venator seems to be on the brink of insolvency as it revealed in its annual report that it anticipates the violation of certain debt covenants in its Term Loan Facility and ABL Facility, specifically the issuance of an unqualified audit opinion to the lenders under these two facilities. This would give the right to these lenders to accelerate the repayment of the outstanding borrowings under the facilities (see page 112 here ).

{kind=link}

In addition, the available borrowing capacity had shrunk to just $37 million as of February 17. Considering Venator, revealed during its Q4 2022 earnings call that EBITDA for Q1 2023 was expected to be meaningfully lower compared to the previous quarter due to the higher cost of goods sold and lower average selling prices, you have a recipe for disaster. In my view, the most likely scenario for Venator in the near future is insolvency.

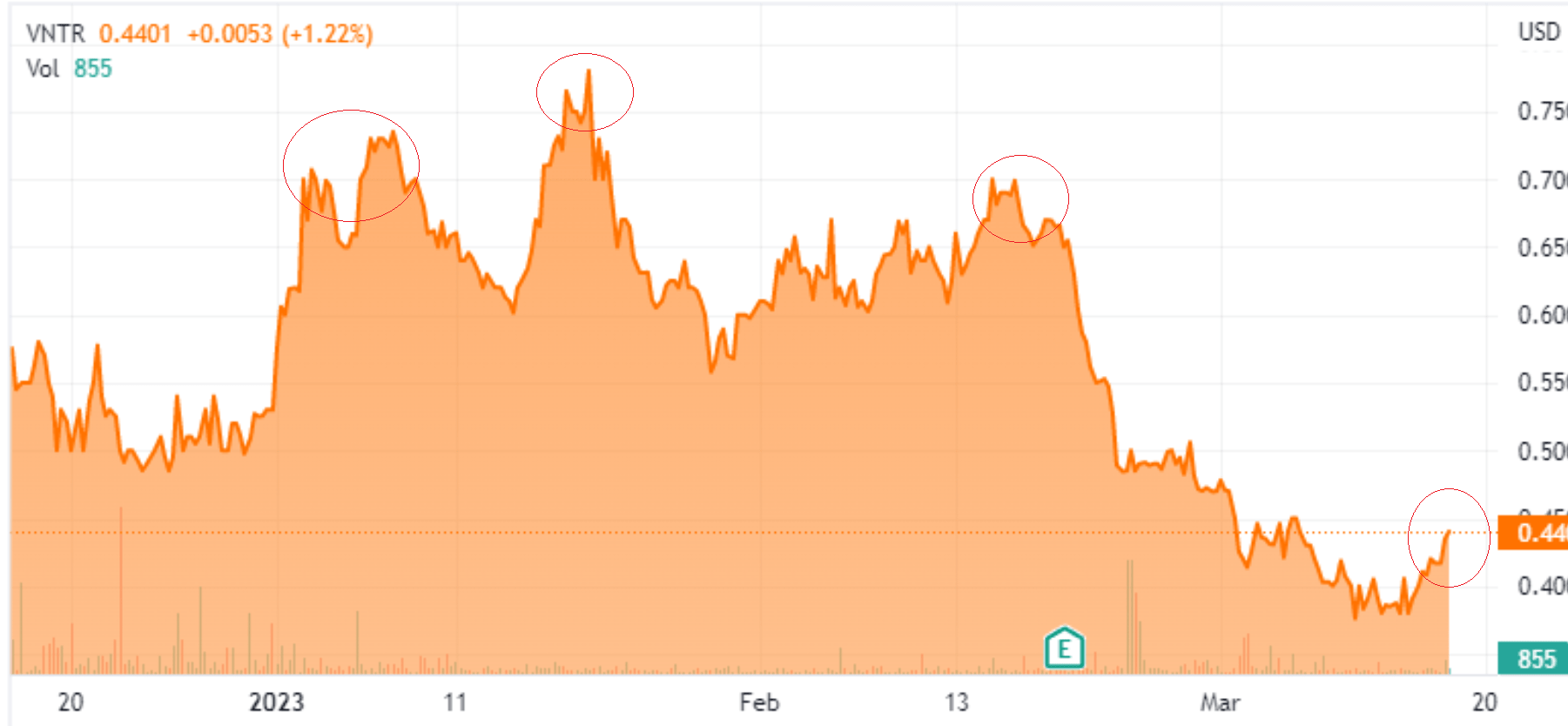

So, how do you play this? Well, short selling seems like a viable idea as data from Fintel shows the short borrow fee rate is just 3.92% as of the time of writing. However, the market valuation of Venator has dropped below $50 million and there has been significant share price volatility over the past few weeks due to low trading volumes.

{kind=link}

In addition, the lowest available strike price for call options is $2.50 which makes hedging ineffective. It could be best for risk-averse investors to avoid VNTR stock.

Investor takeaway

Venator has been struggling from a financial standpoint since it was listed in 2017 and it seems that the Russian invasion of Ukraine was the final nail in the coffin as high energy costs in Europe accelerated its demise. The company was already being pressured by Chinese competitors before the war as they have access to lower energy costs, and I think that it’s on the brink of becoming insolvent. That being said, short selling seems dangerous due to high share price volatility and limited hedging options. In my view, risk-averse investors should avoid Venator.

For further details see:

Venator Materials: Insolvency Seems Just Around The Corner