VNTR - Venator Materials: More Pain Ahead But Too Risky To Short

Summary

- The company closed Q3 2022 with an attributable net loss of $50 million as higher average selling prices couldn't compensate for weak demand in the titanium dioxide segment.

- Demand weakness continued into the fourth quarter in Europe and APAC, and Venator Materials is starting to see some softening in North America too.

- The company has started selling assets and has a cost-cutting plan in place, but significant stock dilution or bankruptcy in the next two years is starting to look likely.

- I think it could be best for risk-averse investors to avoid this stock.

Introduction

I've written about titanium dioxide producer Venator Materials (VNTR) two times on SA so far, the latest of which was in September. Back then, I said that energy prices in Europe were rising and that the company was likely to struggle to pass on further cost increases to its customers as titanium dioxide prices in China had been falling rapidly since July.

Well, the company closed Q3 2022 with an attributable net loss of $50 million and the balance sheet looks ugly even after two deals involving its color pigments division worth $191 million.

In my view, Q4 financial results are likely to be even more underwhelming than the ones for Q3, and liquidity is running out. The company could be heading either to significant stock dilution or bankruptcy in the next two years. Let's review.

Overview of the Q3 2022 financial results

In case you haven't read any of my previous articles about Venator Materials, here's a quick description of the business. The company is based in the UK and in 2017 it was separated from Huntsman Corp. (HUN), thus becoming public through a $454 million initial public offering ((IPO)). Its portfolio includes a total of 7 titanium dioxide production plants and 13 manufacturing and processing facilities focused on functional additives, color pigments, and timber treatment chemicals (these operations make up its performance additives segment). Venator Materials employs about 3,500 people and sells its products in over 110 countries worldwide. The titanium dioxide segment is focused on Europe and usually accounts for about three-quarters of revenues. Titanium dioxide is used primarily as a vivid colorant and across the EU, it's a popular ingredient in paints, plastics, paper, pharmaceuticals, sunscreen, and food products.

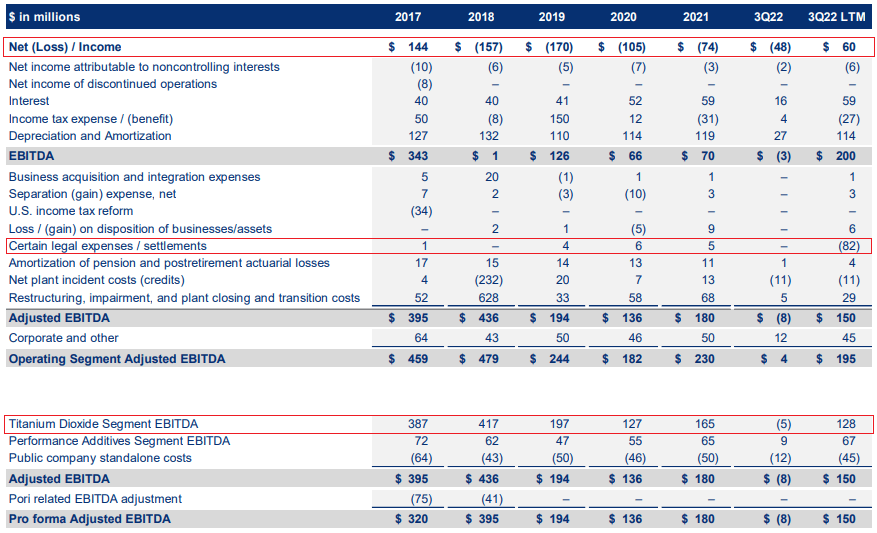

The issue here is that chemical companies are sensitive to energy prices and the war in Ukraine has put Venator Materials in a tough spot. The company was already being pressured by Chinese competitors before the war, finishing every year since 2018 with a net loss. The LTM result is positive, but this is mainly due to an $85 million settlement with Tronox (TROX). This lawsuit was over a break fee contained in an exclusivity agreement from July 2018 relating to Venator's merger with Cristal. As you can see from the table below, the titanium dioxide business is in serious trouble as its EBITDA slipped into the red in Q3 2022.

{kind=link}

In Q3, the average selling prices in the titanium dioxide segment increased by 19% year on year and 1% quarter on quarter in local currency but sales volumes slumped by 29% year on year and 25% quarter on quarter due to low demand, primarily in Europe and APAC. With COGS rising significantly due to higher energy, raw materials, and shipping expenses, EBITDA was minus $5 million. The performance additives segment fared better thanks to a 31% year on year increase in average selling prices, but this was not enough to offset the loss coming from the titanium dioxide business as sales volumes decreased by 8% year on year due to soft demand in Europe and APAC.

{kind=link}

With no end in sight for the war in Ukraine, energy prices in Europe are likely to remain high in the foreseeable future which puts the financial results of Venator Materials under severe pressure. In addition, the company said during its Q3 2022 earnings call that demand weakness continued into the fourth quarter in Europe and APAC and that it's starting to see some softening in North America as well. It seems that Q4 results are likely to be even more underwhelming. To counter this, Venator Materials is reducing its 2022 CAPEX by $20 million to $70 million and is implementing a $30 million cost reduction program that is expected to deliver $50 million of annualized savings by the end of 2024.

{kind=link}

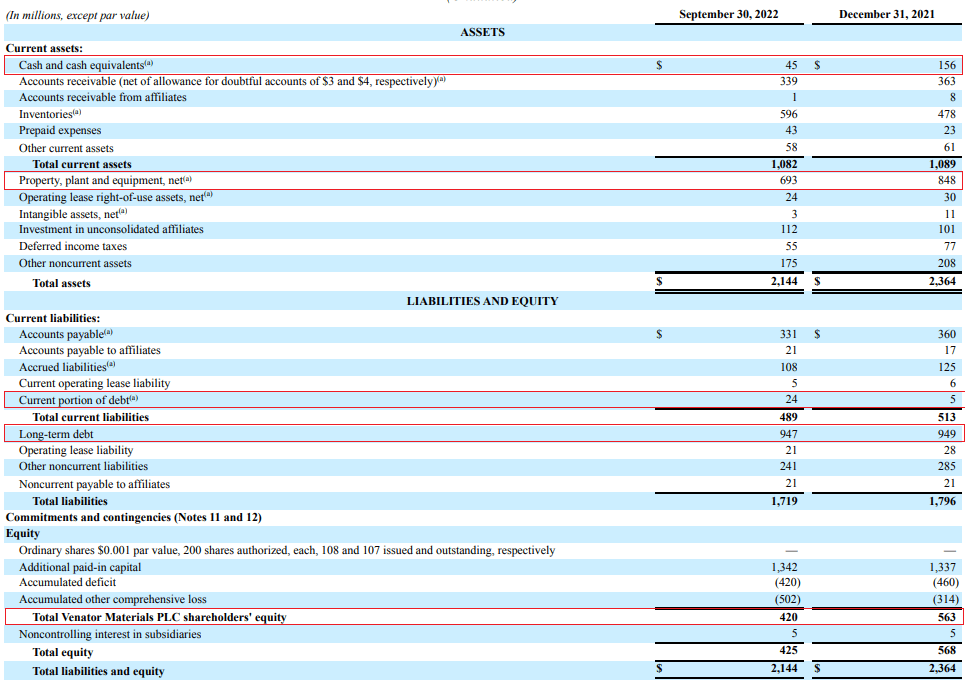

In addition, Venator Materials announced in October that it closed a $51.3 million sale-leaseback for its color pigments manufacturing facility in California. According to the Q3 financial report, the company received proceeds of $42 million, net of $9 million of taxes and other expenses (see page 9 here ). Just over a month later, Venator Materials revealed that it's selling its iron oxide business at an enterprise value of $140 million. This operation forms part of the performance additives segment and considering its average annual EBITDA in 2020 and 2021 adjusted for the impact of the sale-leaseback deal was $16 million, I think Venator Materials is getting a good price here. The deal should be closed at the end of March, but I think that the asset disposals are too small to help Venator Materials avoid major stock dilution or bankruptcy in the coming years. You see, net debt rose to $926 million in September, with a term loan facility in an aggregate principal amount of $375 million maturing in August 2024. While shareholders' equity was $420 million, I think it's likely that the company's business is worth much lower than its book value in this challenging market environment. For example, even the sales of the profitable iron oxide business and the California facility are expected to result in a pre-tax loss of $35 million to $45 million in Q4 (see page 9).

{kind=link}

So, how do you play this? Well, data from Fintel shows the short borrow fee rate is just 1.79% as of the time of writing but hedging is an issue as the lowest available strike price for call options is $2.50. And looking at the major risks for the bear case, short selling could be dangerous. First, the end of the war in Ukraine is likely to lead to a significant decrease in energy costs in Europe and this would provide a boost to the financial results of the company. Second, the share prices of microcap companies can sometimes increase for spurious and unknown reasons and Venator Materials has a market valuation of just $57 million as of the time of writing.

Investor takeaway

Venator Materials has been in dire straits from a financial standpoint for years now but the war in Ukraine and global macroeconomic headwinds have put its business under severe pressure. The company has started selling assets and has a cost-cutting plan in place, but I think these initiatives won't be enough to help it avoid significant stock dilution or bankruptcy in the next two years. It seems that Q4 could be more challenging than Q3 from a financial standpoint.

However, short selling seems too risky at the moment, and I think that the best course of action for investors is to avoid this stock. I probably won't write another article about Venator Materials unless there is a major change in the fundamentals of the business.

For further details see:

Venator Materials: More Pain Ahead But Too Risky To Short