BXSL - Venture Debt Opportunity Yielding 13% To 14% For Your Portfolio: Hercules Or TriplePoint?

2023-06-29 12:05:03 ET

Summary

- This article compares HTGC and TPVG, currently paying dividend yields of 13% to 14%, supported by debt and equity investments in venture capital (VC)-backed technology and high-growth companies.

- We compare the credit quality of their portfolios to identify which one will likely outperform.

- I currently own one of these BDCs due to its relatively safer portfolio and have provided a list of positive and negative considerations.

- Please see the end of this article for charts comparing various credit metrics, including the amount of "watch list" investments and the potential impact on NAV, non-accrual investments, and changes in NAV per share for one, three, and five years.

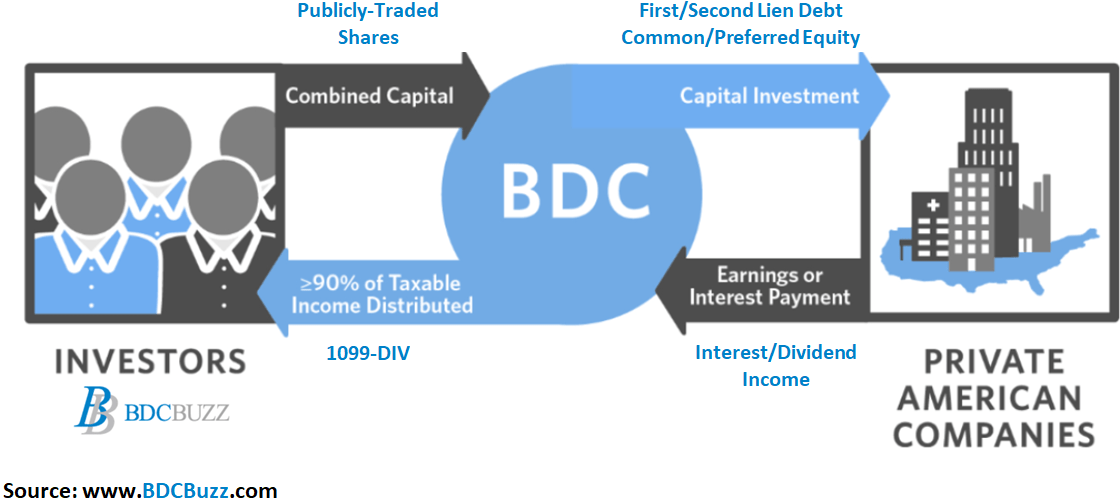

Quick Introduction To Business Development Companies

Business development companies ("BDCs") invest shareholder capital in privately-owned, small- and medium-sized U.S. companies generating income from secured loans and capital gains from equity positions, much like venture capital or private equity funds. Anyone can invest in BDCs as they're public companies traded on major stock exchanges. Also, many BDCs have investment grade ("IG") bonds/notes for lower-risk investors building a balanced 60/40 portfolio (composed of 60% to 70% stocks/equities and 30% to 40% bonds or other fixed-income offerings).

{kind=link}

The two biggest mistakes that I see new BDC investors make are:

- Not understanding why BDCs trade at different prices and thinking that price-to-NAV is the only measure to find a "good deal."

- Focusing on historical dividend coverage instead of projected dividend coverage which is heavily reliant on portfolio credit quality.

Please see the end of this article for a quick discussion of how BDCs are valued and charts comparing various credit metrics including the amount of "watch list" investments and the potential impact on NAV, non-accrual investments, and changes in NAV per share for one, three, and five years.

This article compares portfolio credit quality for Hercules Capital ( HTGC ) and TriplePoint Venture Growth ( TPVG ) which provide capital to venture capital-backed technology and high-growth companies and currently have among the highest dividend yields at 13% to 15%, as shown below. It should be noted that Trinity Capital ( TRIN ) is another BDC with a similar focus which I will be discussing next month.

{kind=link}

HTGC is the leading and largest specialty finance company focused on providing senior secured venture growth loans to high-growth, innovative venture capital-backed companies in a broad variety of technology, life sciences and sustainable and renewable technology industries. Since inception (December 2003), Hercules has committed more than $17 billion to over 600 companies and is the lender of choice for entrepreneurs and venture capital firms seeking growth capital financing.

Source: HTGC Website

TPVG is focused on providing customized debt financing with warrants and direct equity investments to venture growth stage companies in technology and other high growth industries backed by a select group of venture capital firms. The Company's sponsor, TriplePoint Capital, is a Sand Hill Road-based global investment platform which provides customized debt financing, leasing, direct equity investments and other complementary solutions to venture capital-backed companies in technology and other high growth industries at every stage of their development with unparalleled levels of creativity, flexibility and service.

Source: TPVG Website

These BDCs should continue to benefit from tightened lending policies and potentially increased banking regulations, which will likely include stronger capital and liquidity standards for certain banks. BDCs have a distinct advantage over banks in that they have "permanent equity capital" and are not subject to "runs on the bank," which could lead to the forced liquidation of undervalued assets. TPVG management discussed on the recent earnings call:

Given the unprecedented developments at both Silicon Valley Bank and Signature Bank last quarter and extending right into this quarter at First Republic Bank, there are significant and lasting impacts from these events and we expect these developments will continue to have a monumental effect on our market. From a market perspective, it is turning into a major game changer that is significantly and potentially permanently altered the competitive landscape for venture lending, translating into what we believe are increased in growing opportunities for the overall TriplePoint Capital platform to capitalize over the long term, including a very promising long-term outlook for TPVG. In terms of enter lending given this emerging post-SVB environment, bank appetites have changed and we have witnessed considerable tightening. This is a highly specialized business and venture lending has significant barriers to entry. Based on conversations with our venture capital partners, portfolio companies, and active prospects that are in the pipeline now more than ever, they recognize the importance of separating the commercial bank and the lending relationship as well as it's becoming more conscious of the hidden cost limitations and the associated drawbacks of bank lending."

The recent instability in the banking sector is likely to have a considerable effect on BDCs, resulting in continued improvement in yields on new investments and a wider range of investment opportunities. As a result, BDCs can continue to be very selective in their new investment choices. Last month, TPVG management mentioned the more lender-friendly environment with better terms, including stronger covenants (safer investments) and higher overall yields taken into account with the best-case projections:

The departure of SVB has also resulted in increased deal flow and has contributed to our building TriplePoint platform, which also includes providing newer replacement loans previously received from banks. At the platform level, we have a number of high quality lending opportunities to companies backed by our select venture partners where we are or will be replacing a major market participant, who is no longer active or as active and where we're becoming the new source for lending. The pipeline is continuing to build as these are not overnight situations and will continue to be part of our portfolio growth and build out over the next few quarters and well into the future years. Some of these companies are seeking financing for opportunistic acquisitions or previously equity only companies, which are continuing to turn towards debt and layering in as part of their go forward plans. Venture growth stage companies that raised equity over the last year or so at attractive valuations continue to turn towards venture debt given the valuation sensitive markets. And finally, the longer timelines for public listings and the need for additional runway between equity rounds have been serving as another driver."

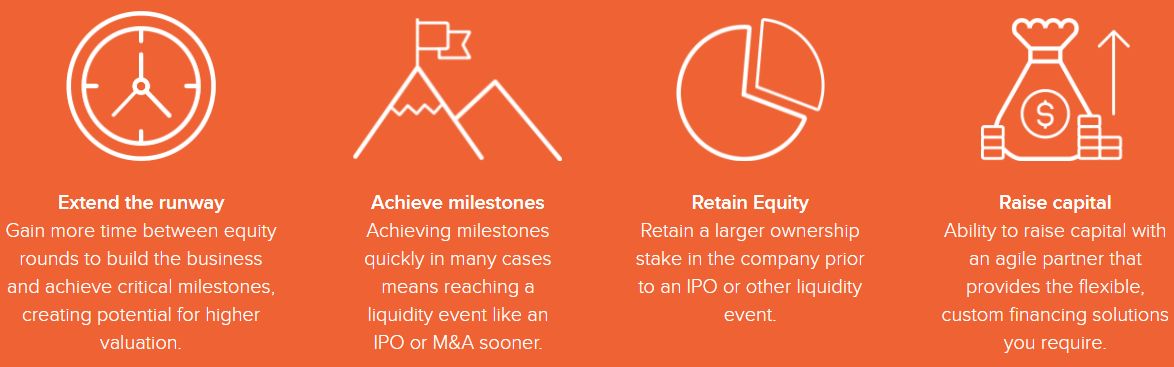

Why Would Venture-Backed Companies Use Venture Debt?

- Less dilutive than new VC round

- Lengthens time before next equity round

- Provides negotiating leverage for higher valuations

- Leverages returns for equity investors

{kind=link}

This article is a follow-up to " Buy The Dip And Position For Higher Rates With Hercules Capital " which suggested buying the dip as the company "will likely rebound, providing excellent returns" partially due to being "well positioned for higher interest rates that could drive additional dividend increases."

Did you buy it?

{kind=link}

Earlier this month, we discussed FS KKR Capital ( FSK ), PennantPark Investment ( PNNT ), Monroe Capital ( MRCC ), Goldman Sachs BDC ( GSBD ), and Prospect Capital ( PSEC ) in the following articles:

- Better High-Yield Buy: FS KKR Or Prospect Capital?

- Safer 12% Yield: Goldman Sachs BDC Or Monroe Capital

- PennantPark: Big Win From Dominion/Fox Settlement

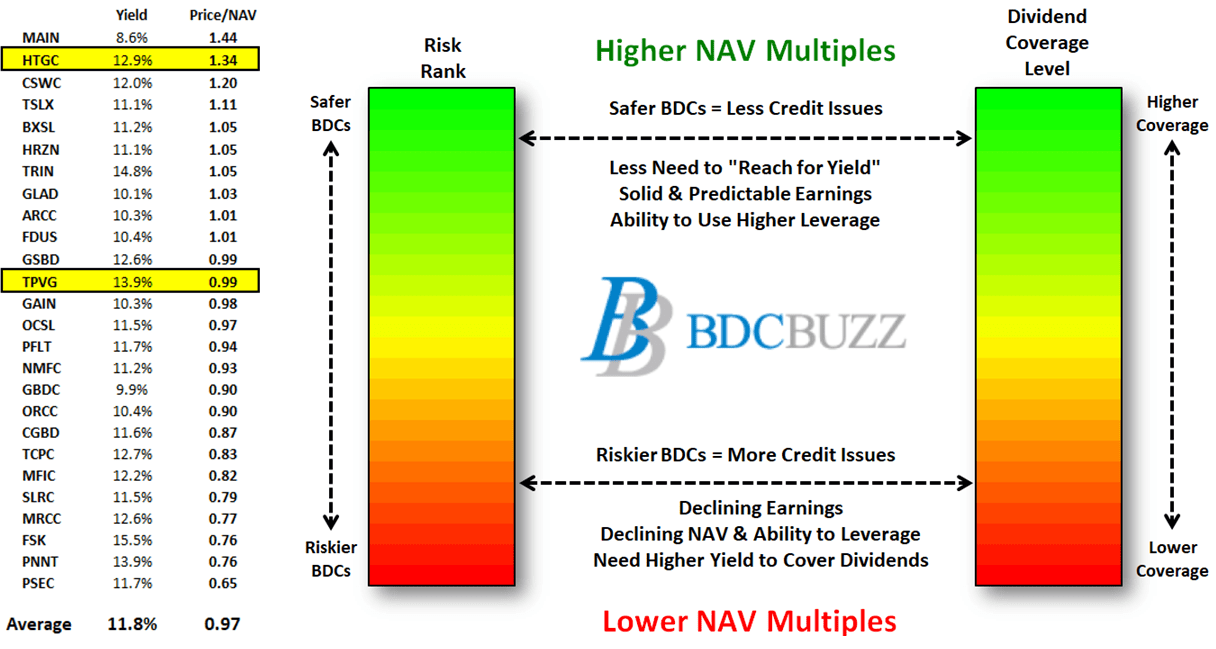

The following table shows the current dividend yield and price-to-NAV for each BDC. It's important to note that the dividend yield takes into account special and supplemental dividends including $0.32 per share for HTGC which was announced in February 2023 .

BDC Buzz

Comparing Portfolio Credit Quality

Author's Note: The following information was provided to subscribers of Sustainable Dividends along with a constantly updated full risk profile and rankings for HTGC and TPVG .

Hercules Capital

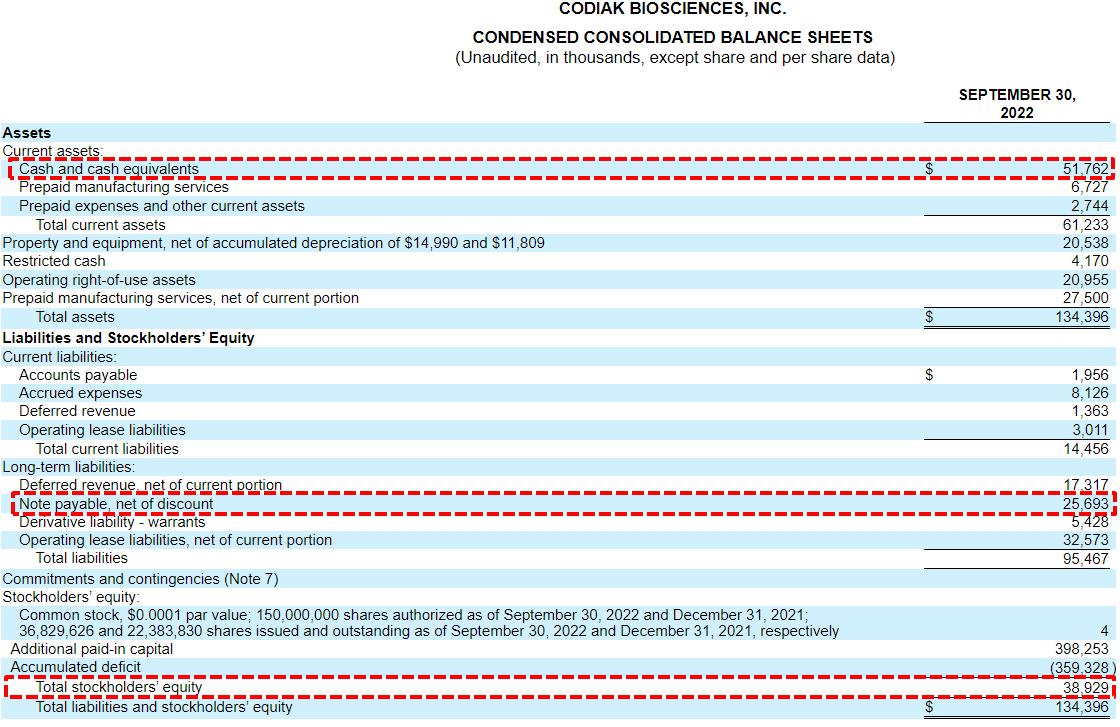

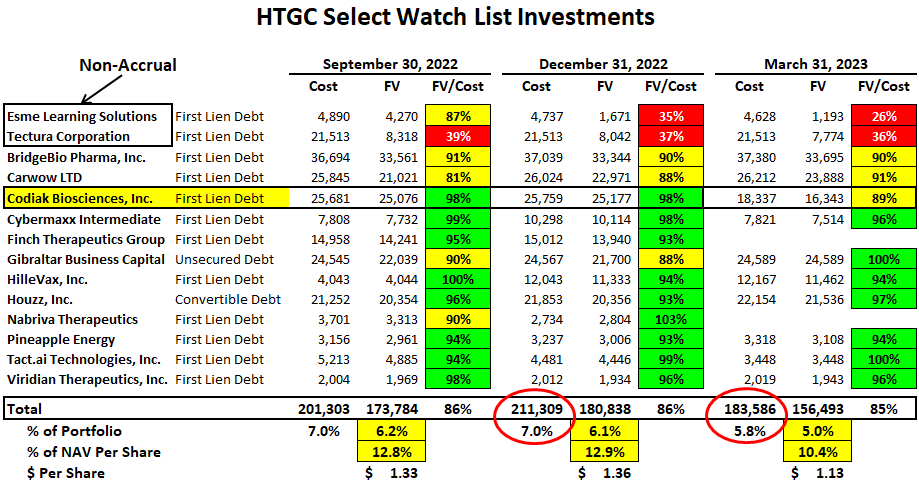

During Q1 2023, HTGC's non-accruals decreased from 0.1% to 0.0% of the portfolio fair value due to removing a portion of its investment in Tectura Corp . As mentioned in previous weekly updates, Codiak Biosciences filed for bankruptcy, but management is expecting a full recovery:

Q. "One of your portfolio companies, Codiak BioSciences filed for bankruptcy in late March, which is out there publicly. So just curious on what type of recovery you might expect there. Just looking at their balance sheet, they had a little over $50 million of cash as the third quarter and that compared to your $25 million loan, which looks to be about a $17.5 million principal now. So unclear what their cash burn has been since the third quarter just given disclosures. But curious if you're confident on a full recovery there based on their cash position or anything else worth pointing out?"

A. "As you pointed out, we do have one company out of about 120 debt positions that did file for bankruptcy at the end of Q1. Bankruptcy for us as a senior secured first lien creditor does not mean that we are going to have a loss on that position. When the company filed, we had $25 million of principal outstanding. Subsequent to the filing, we have worked cooperatively and constructively with the company, with the advisers and with the investors. We have already received $10 million of cash pay downs. So that $25 million principal loan has been reduced to $15 million. The company remains 100% current through the May 1 date on all payments of principal and interest to Hercules. The company has a vast pool of assets that they are currently looking to monetize, obviously, in consultation with Hercules and their advisers. And while there are no guarantees in any of these situations, we feel very good about the ultimate recovery of that position. I would also say that for us, what we just said is not just words. We have a very long track record of being able to be able to navigate through challenging workouts and bankruptcy situations. If you look at the last several workouts and bankruptcies that we, as an organization, have had, we've had very strong recoveries, and we're not seeing anything with respect to Codiak specifically that we believe will lead to a different outcome."

The following is from Codiak's agreement with HTGC and is typical of the protections for many BDCs with first-lien positions:

The Amended Term Loan Facility remains secured by a lien on substantially all of the Company's assets, other than the Company's intellectual property. The Company has agreed not to pledge or grant a security interest on the Company's intellectual property to any third party. The Amended Term Loan Facility also contains customary covenants and representations, including a liquidity covenant, whereby the Company is obligated to maintain, in an account covered by Hercules' account control agreement, an amount equal to the lesser of: 110% of the amount of the Company's obligations under the Amended Term Loan Facility, and the Company's then-existing cash and cash equivalents, financial reporting covenant and limitations on dividends, indebtedness, collateral, investments, distributions, transfers, mergers or acquisitions, taxes, corporate changes, deposit accounts, and subsidiaries. The events of default under the Amended Loan Agreement include, without limitation, and subject to customary grace periods, the following: any failure by the Company to make any payments of principal or interest under the Amended Loan Agreement, any breach or default in the performance of any covenant under the Amended Loan Agreement, the occurrence of a material adverse effect, any making of false or misleading representations or warranties in any material respect, the Company's insolvency or bankruptcy, certain attachments or judgments on the assets of the Company, or the occurrence of any material default under certain agreements or obligations of the Company's involving indebtedness. If an event of default occurs, Hercules is entitled to take enforcement action, including acceleration of amounts due under the Amended Loan Agreement."

As shown below, Codiak had over $50 million in cash as of Sept. 30, 2022, (the last available SEC filing). Please note that HTGC does not have an equity position in Codiak.

{kind=link}

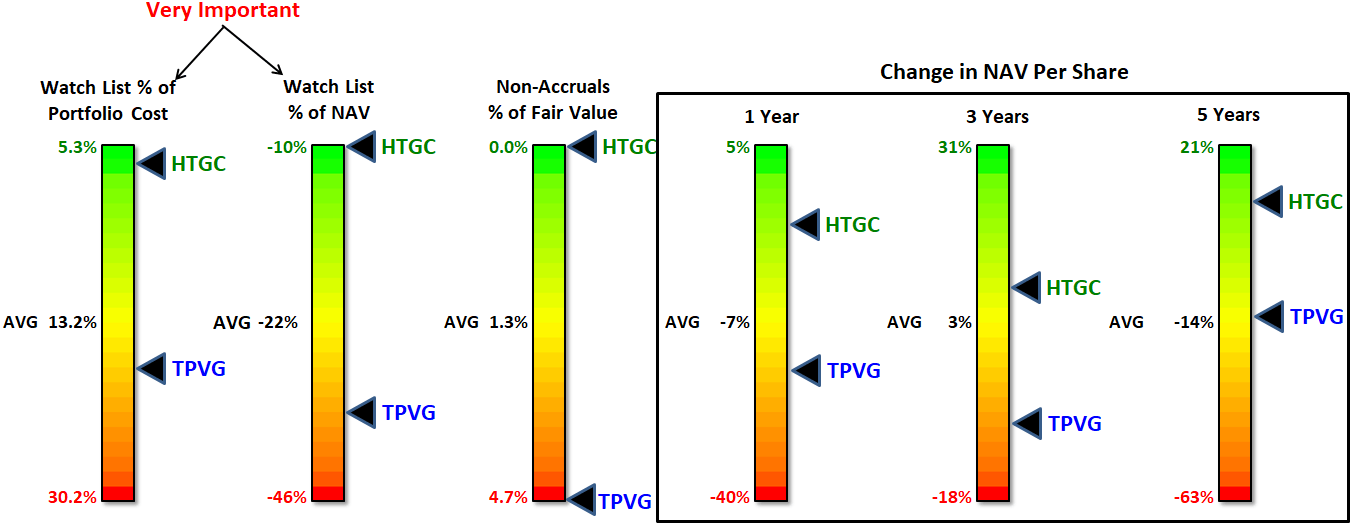

As shown below, the amount of investments on "watch list" recently declined from 7.0% to 5.8% of the portfolio at cost (5.0% of the portfolio fair value), which is much lower than most BDCs (as shown in the comparison charts):

{kind=link}

TriplePoint Venture Growth

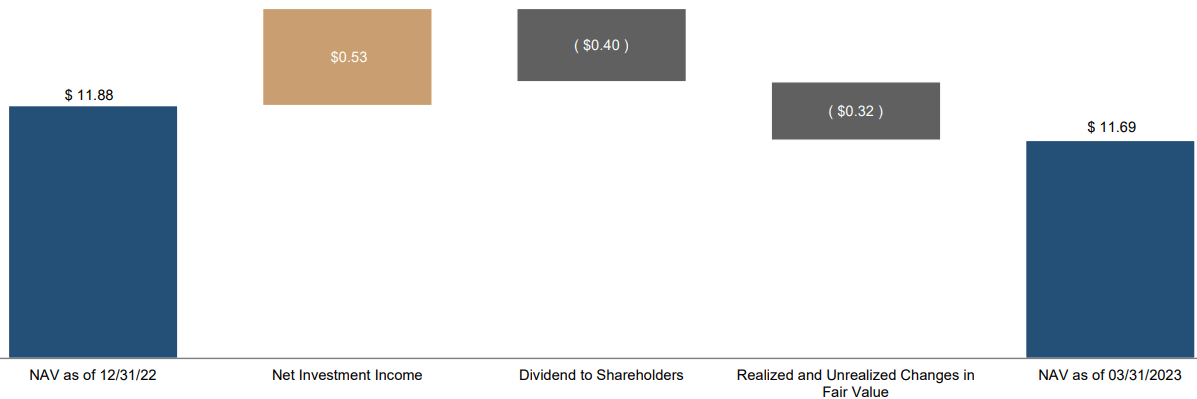

During Q1 2023, TPVG's net asset value ("NAV") per share declined by $0.19 or 1.6% (from $11.88 to $11.69) mostly due to its watch list investments in Hi.Q, Inc. (Health IQ) and VanMoof that contributed around $7 million or $0.20 per share of depreciation during the quarter, partially offset by over-earning the dividend. Other markdowns included some of its equity positions especially Capsule Corporation and Merama Inc.

{kind=link}

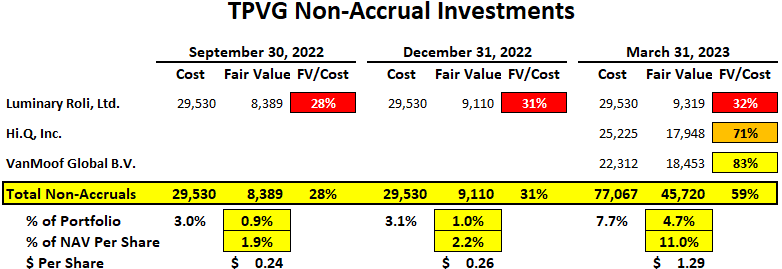

Non-accruals increased from 1.0% to 4.7% of the portfolio fair value due to adding its watch list investments in Hi.Q, Inc. (Health IQ) and VanMoof .

"During the quarter VanMoof an e-bike company with a principal balance of $23 million and Health IQ, an insured tech company with a principal balance of $25 million, which were both previously rated 3, were downgraded to Category 4 as they continue to navigate through challenges in their sectors and businesses as well as developments in their strategic financing processes."

{kind=link}

As discussed in the previous report, its investment in Hi.Q, Inc. (Health IQ) was among the larger markdowns during Q4 2022 likely due to a proposed class action suit alleging that the company made telemarketing calls offering health insurance to consumers in violation of the Telephone Consumer Protection Act, as ruled by a federal court.

Subsequent to quarter end, Hey Favor (The Pill Club), Underground Enterprises , and RenoRun filed for bankruptcy protection and will likely be added to non-accrual in Q2 2023.

Q. "Is it safe to say that RenoRun, Underground and Hey Favor will all go on non-accrual in the second quarter ?"

A. "Unless something happens more immediate that would be a fair assumption. "

These investments also were discussed on the recent call and management is expecting a high or full recovery on most of its watch list investments due to "the underlying inventory as well as other potential asset sales, including the entire enterprise and IP."

Hey Favor, also known as Pill Club, an online pharmacy with the principle balance of $20 million filed for Chapter 11 bankruptcy protection with the intent to continue operations and potentially reorganize as a standalone enterprise or sell to another company. This is an ongoing situation and we expect more developments to occur in the near term that could result in substantial or full recovery of our loan."

"Underground enterprises and the e-commerce retail with principle balance of $6 million was downgraded from Category 2 to Category 3 and has filed for Chapter 7 bankruptcy protection. We provided an inventory based financing facility to the company and look to recovery on our loan from the underlying inventory as well as other potential asset sales, including the entire enterprise and IP."

Q. "You have zero investments right now in the red category, but as you mentioned, three companies filed for bankruptcy since quarter end . And you mentioned some comments on recovery for those investments, but can you dig a little deeper into that as to what types of recovery - what types of recovery you might expect on those investments on either a percentage or dollar basis, and then your confidence there?"

A. "Yes, again, obviously these are ongoing situations and so it's hard to give full information just because they continue to develop. But I would say, as we said in our prepared remarks, I mean, I think, we generally are confident for or believe to see full or complete recovery , assuming facts and circumstances as of today in developments that we expect to occur ."

Q. "I'm curious to hear your thoughts on investment like The Pill Club. I mean, there's been articles out there that talk about the bankruptcy and a huge decline in revenue as well as huge legal fees in that business. Now, I can't see - I don't see it's financial, so I don't know if they're sitting on a bunch of cash or something like that or your loan is over collateralized, but something like that. But I guess what gives you the confidence to mark that investment where it is as well as there's other loans in the portfolio that are in bankruptcy or in the process of bankruptcy that you guys have marked pretty close to par. What in either the pill - The Pill Clubs specifically or any other investments that are going through this period, it gives you the confidence kind of mark on where you are despite sort of these fundamental deterioration and the…

A. "So I have to remember that they're easier paths to - if you wanted to shut down a company that you don't necessarily go through the bankruptcy process. So from our perspective in collaboration with the company's investors to select these C funds, you look at when there's value there's interest in those assets, there's value in those assets and you look at what's the best path to free-up those assets to either reemerge or to sell to other parties. So I would say there's a playbook in managing stress credit situations, and it's a function of our assessment of underlying value and our playbooks with our teams. And so, so I would say the - and then as you look to the method by which you look to recovery as you said, right there are various assets these companies have. In certain cases when we're doing inventory financing, we're secured not only by a formula based financing for that inventory, so we're not financing 100%, generally it's a discount . So we're secured by that underlying inventory, plus we have the enterprise too. So as you look to recovery its great, the underlying asset that we financed and then the value of the business, the intellectual property whatever it may be. When you look to as again, other scenarios, right? There's a liquidity, there's cash and so again you look through the benefit of liquidation process is an orderly way to unlock those assets to the senior creditors . And then again, I'd say more broadly, when you look to acquirers out there in this environment, they generally want things clean and free. So again, I think a bankruptcy process and for companies themselves, right, there's a way when there's strong, solid fundamentals of these businesses, but they may have unsecured claims or creditors. And so going through the Chapter 11 process in general is a way to again, cleanse, clean up, restructure secured debt and then come back and again give it another shot or sell to other companies. So again I think that, it's our team's assessment of the playbook, the path and the underlying assets. And in collaboration with our companies, we determine the course of action and that's how we look to set our fair values based on assessment of the probabilities, and the likelihoods and the values of those assets."

Q. "In relation to Hey Favor and rolling back to Medly Health, in both cases there were some form of management fraud that contributed to the situation. And it looks to me like they came out of the same underwriting pod. I mean, is there a flaw in your underwriting process that you failed to pick up on the situation that they existed in Hey Favor and Medly Health?"

A. "Absolutely not. Again, we stand by our underwriting and our track record, again as you look we've had 170 obligors or borrowers at TPVG we've had credit losses in roughly 10 to 11. Our loss rates are 3% of commitments, 2% of funding, so I would say the data speaks for itself that our underwriting and our track record over the long-term works. And so I'd say that's first answer. I would say, again we're not suggesting at both companies where they're fraud, I think Medly, it's again in the public - in the filings not suggesting fraud at Hey Favor, and again, I think all are unique circumstances and situations."

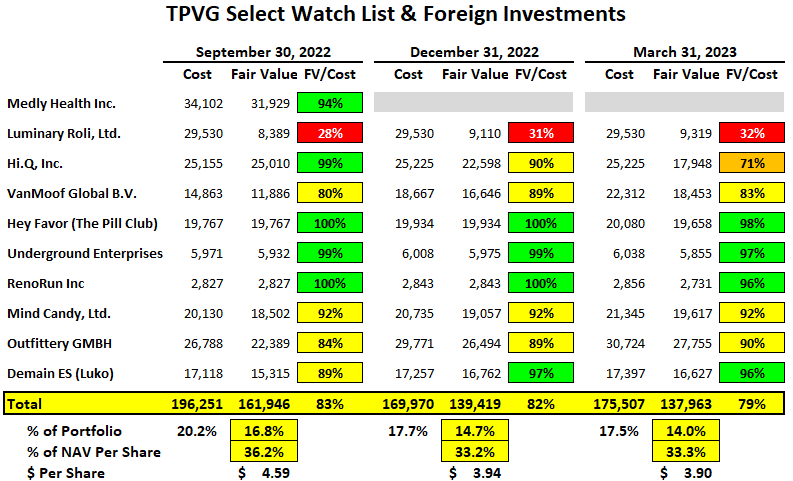

As discussed in previous updates, I sold my position in TPVG in December 2022, mostly related to having a higher amount of investments considered watch list. After taking into account the recent markdowns, the amount of watch list investments remains almost 14% of the portfolio fair value and around 33% of NAV, which is much higher than most BDCs (as shown earlier).

Demain (Luko) is an insurtech company that was recently downgraded from Category 2 to Category 3 (mentioned later) due to delays in its strategic financing process.

One of my primary concerns is growth capital loans to Mind Candy, which has been continuously extended/amended, pushing its maturity date out which is now Sept. 30, 2023, (for the largest loans). Also, Mind Candy is 100% payment-in-kind ("PIK") interest income which is not paid in cash, so I will continue to watch closely, as this investment accounts for $0.55 per share of NAV .

Also, Outfittery is 100%PIK interest income, but the total amount of PIK remains lower than historical levels currently at 6.5% of total interest income (previously 10% to 11%).

Some of these investments are companies based in foreign countries, so a portion of the previous markdowns were related to a stronger dollar. There's a good chance for a reversal of previous unrealized losses as the dollar weakens, resulting in a positive impact on NAV per share over the coming quarters. Also, the company will likely over-earn the dividend as shown in the base and best-case projections supporting NAV reflation.

{kind=link}

It should be noted that around 20% of its growth capital loans as of March 31, 2023, are with borrowers that have other facilities in a senior position to TPVG. We have classified this portion of the portfolio as "second lien."

SEC Filing: "Growth capital loans in which the borrower held a term loan facility, with or without an accompanying revolving loan, in priority to our senior lien represent 20.4% and 21.4% of our debt investments at fair value as of March 31, 2023 and December 31, 2022, respectively."

BDC Valuations and Comparing Watch Lists

Author's Note: The following information was provided to subscribers of Sustainable Dividends along with updated target prices and suggested limit orders (for making purchases) for HTGC and TPVG .

There are very specific reasons for the prices that BDCs trade driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). BDCs with higher-quality credit platforms and management typically have higher-quality portfolios and investors pay higher prices. This drives higher multiples to NAV and lower yields.

{kind=link}

The charts below compare the various credit metrics for HTGC and TPVG including the amount of watch list investments and the potential impact to NAV, non-accrual investments, and changes in NAV per share for one, three, and five years.

{kind=link}

{kind=link}

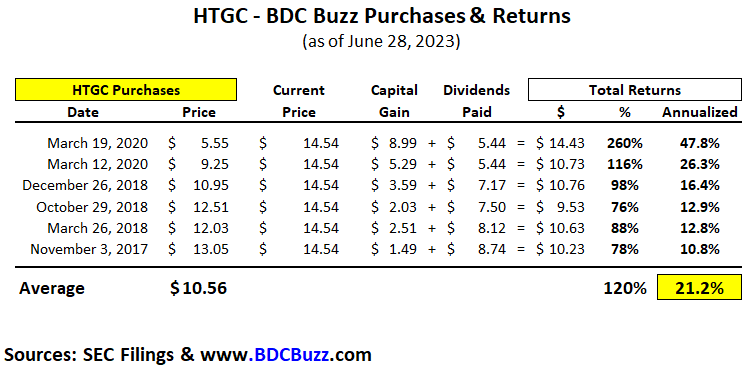

Clearly, HTGC is the winner which is why I own the stock. I have not purchased shares recently because I'm building my smaller positions for a balanced portfolio and will discuss my other positions in upcoming articles.

The following table shows my average annualized returns from my previous HTGC purchases, currently averaging around 21% but continuing to head higher, as the market rebounds. The "Annualized" return shown does not use a simple average but shows the actual compounding of annual returns. This is the true return each year.

{kind=link}

The following are many of the positive considerations for HTGC, some of which are discussed in this article:

- 71% of portfolio companies have at least 12 months of liquidity, 41% have 18 months or more, and 18% have six to 12 months

- Increased its regular quarterly dividend by 95% from $0.20 (in 2010) to $0.39 per share

- Upcoming prepayment-related income (likely including Provention Bio and Oak Street Health ) potentially driving an earnings beat in Q2 2023

- Recent and continued new investments at higher yields with pending commitments of $510 million

- Increased benefit/returns from the RIA/Hercules Adviser with dividends starting Q3 2023

- Average historical but higher projected dividend coverage

- Paying supplemental/special over the last 6 years (consecutively over the last 11 quarters)

- Undistributed taxable income ("UTI") of $0.96 per share to support additional dividends

- Continues to leverage its internally managed cost structure

- Recent instability in the banking sector and venture equity slowdown will drive continued improvement in yields on new investments and a wider range of investment opportunities

- Lower-than-average leverage mostly due to its ATM equity program

- Lower expense ratio mostly related to its internally managed cost structure

- SBIC license provides an incremental source of long-term, low-cost capital

- Excellent "Asset Coverage" and "Interest Expense Coverage" ratios for fixed-income investors of its notes/bonds

- Investment grade ratings: Moody's (Baa3), Fitch (BBB-), DBRS (BBB), KBRA (BBB+)

- Strong balance sheet supported by mostly unsecured longer-term, lower fixed-rate borrowing with only $150 million due in 2024 ($1.7 billion total outstanding)

- Relatively lower amounts of non-cash/PIK interest income

- The portfolio is 93% first and second-lien secured debt

- NAV per share has increased by 11.3% over the last 5 years (much better than most)

- Net realized losses of only $5 million or around $0.03 per share over the last 10 years (much better than most)

- Only 0.0% of portfolio investments at fair value on non-accruals status

- Very low amount of watch list investments that remain under 6% of the portfolio (at cost)

- Management focused on ROE with the ability to earn higher returns through investing in VC-backed tech companies providing NAV per share growth and realized gains

The following are many of the negative considerations for HTGC, some of which are discussed in this article:

- Codiak Biosciences filed for bankruptcy, but management is expecting a full recovery

- 11% of portfolio companies have 6 months or less of liquidity

- Net realized losses of $28 million or $0.20 per share over the last 3 years

- Slightly lower-than-average dividend coverage over the last 4 quarters partially due to previous dividend increases

- Publicly traded equity positions typically result in higher NAV volatility

For further details see:

Venture Debt Opportunity Yielding 13% To 14% For Your Portfolio: Hercules Or TriplePoint?