VEOEY - Veolia: An Outperforming European Utility

2023-12-15 11:45:37 ET

Summary

- Veolia is a French water and waste management company that has outperformed the US utility sector and NextEra Energy.

- Veolia's top line is reliable and protected from rising costs and inflation due to long-term contracts with major municipalities.

- The company's latest results showed significant YoY growth in organic revenues and exceeded growth guidance for the year.

Dear readers,

Veolia ( VEOEF ) is a French-based global water and waste management company which I've covered a number of times already, most recently in early October here . I issued a BUY rating at EUR 27 per share, because the stock was trading at a reasonable P/E of 14.6x, promising solid upside to my EUR 35-40 price target. Since then, the stock price increased to EUR 30 per share, returning about 10%.

I've been quite bullish on many European utilities all year. In addition to Veolia, I have mostly focused on Enel ( ENLAY ) which is an Italian-based electricity company. Both of these represent high-dividend conservative plays and notably have significantly outperformed the U.S. utility sector ( XLU ) as well as one of the largest producers of electricity in the U.S. - NextEra Energy ( NEE ).

I know Veolia's business quite intimately from my private equity days, having led a major transaction with one of the company's many subsidiaries. With that I can tell you that their top line is incredibly reliable and well protected from rising costs and inflation. This is because in many cases, Veolia has long-term 10-year plus contracts with major municipalities and is able to increase prices relatively freely in an inflationary environment with 70% of revenue indexed to inflation. Moreover, Veolia forms infrastructure that is absolutely necessary for a functioning society.

On the other hand, their margins are quite slim - EBITDA margin of 15% and net profit margin of under 5%, which can make the bottom line quite volatile, especially considering that Veolia is leveraged at roughly 3x EBITDA.

Note: I refer to Veolia's EUR-denominated native shares, ticker symbol VIE, traded on the Paris stock exchange. There are ADRs available, but I'm not familiar with them, so make sure to do your own research.

Latest available results

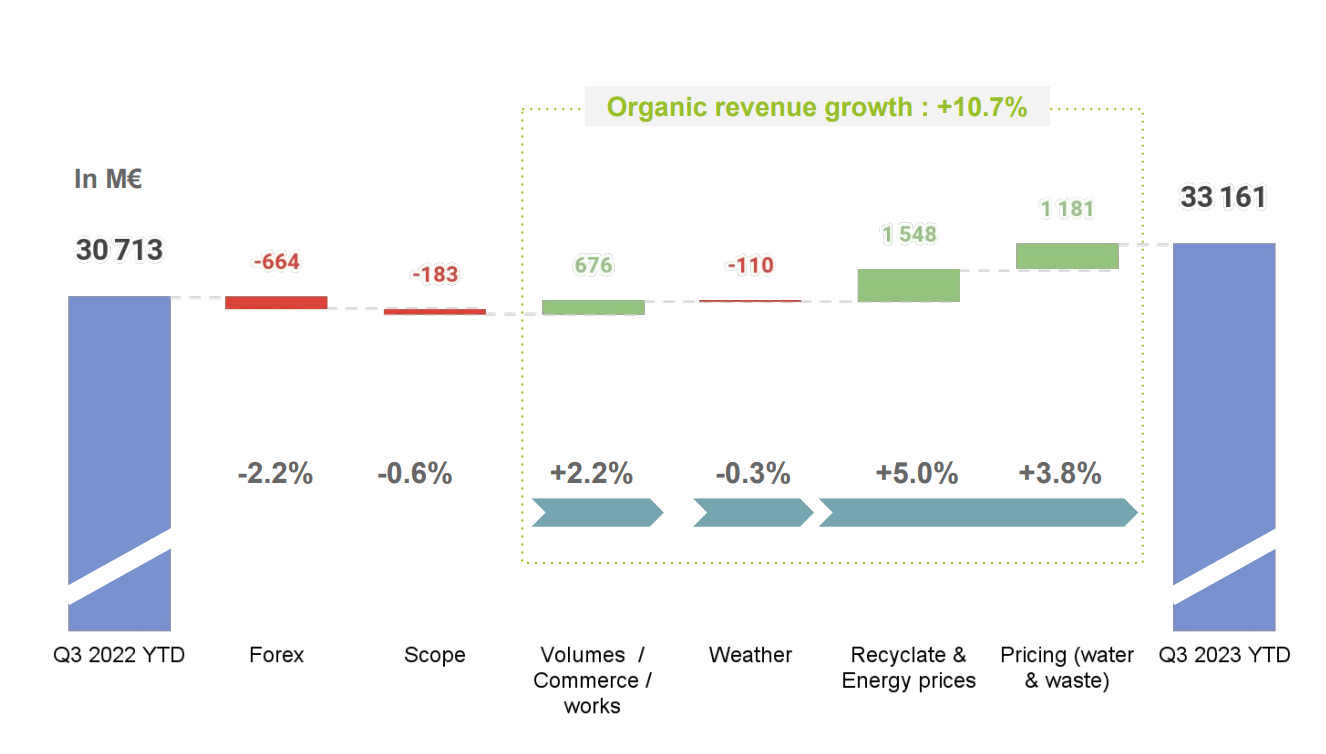

Q3 2023 results were released about a month ago and showed significant 10.7% YoY growth in organic revenues, driven by higher volumes (+2.2%), higher energy prices (+5%), and higher water prices (+3.8%).

{kind=link}

Veolia IR

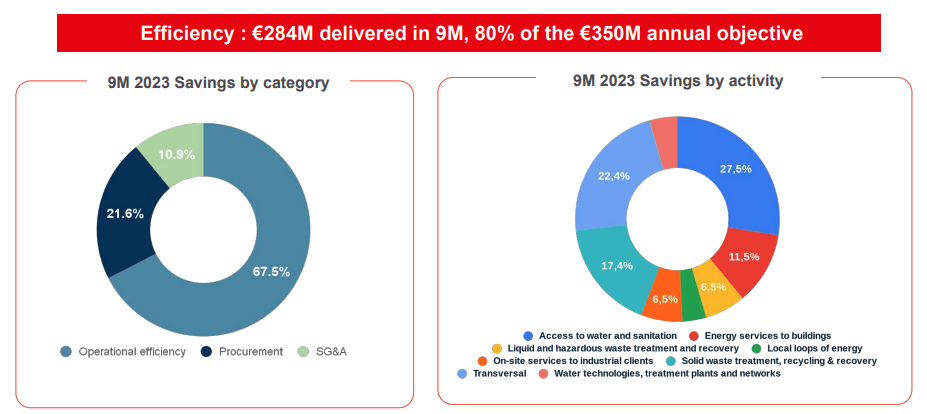

EBITDA increased by 7.7% which is above the top-end of the 5-7% growth guidance for this year. During the first nine months of the year, EBITDA growth continued to be driven by strong (and faster than expected) synergies of EUR131 Million realized from the Suez merger and $284 delivered in (mainly operational) efficiencies.

{kind=link}

Veolia IR

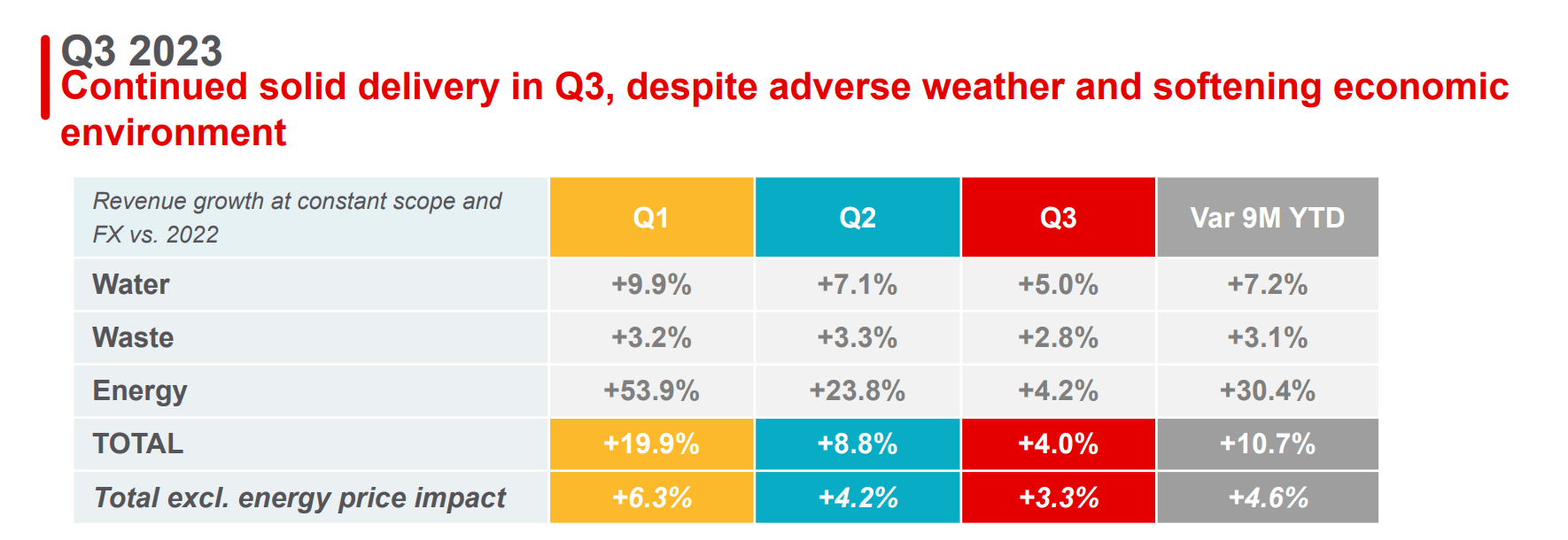

Recall that Veolia operates in three key segments - water, waste and energy.

The water segment is the largest, representing about 40% of all revenues, and is quite stable. Revenue growth in the water segment has slowed since the beginning of the year, but remains in line with targets at 7.2% YoY, driven by tariff indexation in all geographies (+4.3%) and higher overall volumes (+3.4%).

The waste segment is almost as large, with revenues of just under 40%. Most notably, it includes the very profitable toxic/hazardous waste segment, which is the only one of its kind in the world. The waste division has posted slower 3.1% YoY growth due to a drop in recycled materials prices, which offset two thirds of additional revenue from higher prices.

Finally, the energy segment is the smallest, but also the most volatile due to the nature of energy and heat prices. Year-to-date, the segment has seen revenues increase by 30.4%, largely attributable to steep heat price increases in Central Europe.

{kind=link}

Veolia IR

Veolia is well on track to hit its full year net income target of EUR1.3 Billion (EUR 1.85 per share), up 14% from last year.

Financials

Reducing leverage has been a key focus since the Suez acquisition, and Veolia is on track to reducing their net debt to 2.9x EBITDA by the end of the year.

This is a BBB rated business with a strong EUR 6 Billion cash position on its balance sheet. As a result, there will be no new debt issuance needed to fund Veolia's aggressive CAPEX.

Moreover, with 80% of fixed-rate debt, the sizeable cash position acts as an anchor for interest expense, because while the cost of debt increases gradually, interest earned on the cash balance adjusts to high interest rates immediately.

Veolia IR

With a stable interest expense, one of the main risks to Veolia's bottom line remains the volatile nature of energy prices. Veolia does a good job of hedging in the near-term with about half of next year's exposure hedged, but with a sub-5% profit margin, earnings per share are going to be inherently volatile.

Valuation

Veolia paid an EUR 1.12 per share dividend this year, a dividend yield of about 3.85%. And going forward, management has confirmed that the dividend will grow in line with EPS. My expectation is that the dividend will grow by high-single digits and could reach EUR 1.30 per share by 2025, a yield on cost of 4.3%.

Native shares trade at EUR 30 per share or a P/E of 16x. I've previously discussed why I see 18x earnings as justified. With double-digit consensus EPS growth, my price target for Veolia remains at EUR 40 per share. Over time, I expect the main catalyst that gets us to these rates to be a drop in interest rates and yields. Consequently, beyond energy price volatility, one of the biggest risks that Veolia faces is that interest rates will stay high for a long period of time. But with the ECB much more dovish than the Fed, and even the Fed now taking their foot off the pedal, the risk seems small at the moment.

Though it's worth mentioning that the consensus miss ratio is very high at >50% and my personal expectation is that EPS will grow by high-single digits over the next two years as (1) Veolia realizes the rest of expected synergies from the Suez deal worth about EUR 220 Million, (2) revenues increase by 4-5% per year as a result of inflation driven indexation, and (3) net interest expense stays relatively stable thanks to a large cash position and high interest rate hedging with relatively low near-term maturities.

FAST Graphs

I fully expect Veolia to provide stability in a portfolio via an almost 4% yield and solid upside of up to 30% over the next three years or so as the rest of synergies from the Suez deal get realized, aggressive CAPEX spending translates into additional profits and the company re-rates to a higher multiple when interest rates decline.

For further details see:

Veolia: An Outperforming European Utility