VEOEY - Veolia: Yet Another European Outperformer That Remains A Buy

Summary

- Investing in Europe has not been a bad idea for the past 6-8 months, even if the initial results were somewhat disheartening.

- However, we've seen a recovery in overall share prices that are likely to catapult these investments back into profitability over the longer period of time.

- Specifically, and in this article, I'm talking about the company Veolia - which is French, and in water/utilities.

- Let's provide a 2023 update for this business and the prospect of owning it.

Dear readers/followers,

Veolia ( VEOEY ) is the sort of company I believe you want to own long-term as a conservative investor. I'm certain that I do - and that's why I've owned a small position in the company for some time, which I added to back in august and October, bringing it to a current size of around 0.4% of my portfolio.

Its three service/business segments are necessary to everyday human life, which is one of the favorite qualities of investments that I make - and that's also why the company, despite being off its lows and despite being a positive investment from the view of my RoR since investing, is one I continue to put capital into at a slow pace.

Seeking Alpha Veolia Article (Seeking Alpha Veolia Article)

Updating on Veolia

Veolia is 170 years old and has during its history been part of conglomerates and other businesses. Its area of focus is typical government responsibilities, and the company is one of the only businesses I know of that works with hazardous waste on a global scale - and by global, I mean that it does exist on every single continent.

Veolia IR (Veolia IR)

This is also a market that's likely to grow, going forward, and one that's unlikely to see any sort of massive volatility in terms of its fundamentals. The company is "too good" for that to be the case. Despite being a company with a €20B+ market cap, it's still only a small portion of the global market for these services, because the market for them is so incredibly fragmented. In most areas, this is government and public responsibility.

This also means that the scaling potential for this business is nothing short of amazing, and Veolia isn't the only player that has seen this opportunity. Plenty of Chinese players are trying to enter the market, especially in Europe, in order to consolidate operations. Examples of such companies are EEW and Urbaser. Veolia is competing back, by actively M&A'ing and growing wherever possible in order to maintain its scaling advantages and growth.

On a high level, the company is Waste, Water , and Energy - all of these areas putting the company very much in the position of being a globally "necessary" company. Geographically speaking, the company is a legacy central European operator moving into emerging markets in the search for growth. The mature markets serve as a solid foundation for its expansion and growth.

In the mature areas, over 50% of its operations, the company wants to expand its asset-light service base to ensure its margins stay good, while in emerging markets the company seeks to expand its assets, to establish margins and operations.

The combination makes for an attractive proposal, at least if this in any way materializes. It provides the company with a good potential for growth. France is 30% of its operations, Europe is another 30%, with Asia and other geographies coming in at around 40% in the remainder - so it's still heavily France-centric, despite having managed to leave its home shores.

While Veolia does have GDP-specific cyclicality to its earnings, there are still baseline demands for the company's water, recycling and energy operations which really don't disappear. Furthermore, the utility-like segments have far more stability than those tied to GDP, such as hazardous waste.

Waste treatment income and pricing cycles are dependent on energy prices, which makes the company sensitive to energy pricing cycles, at least in the waste segment. This is not the case for Water, where pricing and sourcing conditions are more stable, and margins are more stable as well.

In most markets, it is the municipality that sets the price of water after deliberation by the elected members of the municipal council, taking into account the variations in various factors such as inflation, wages and any other external element.

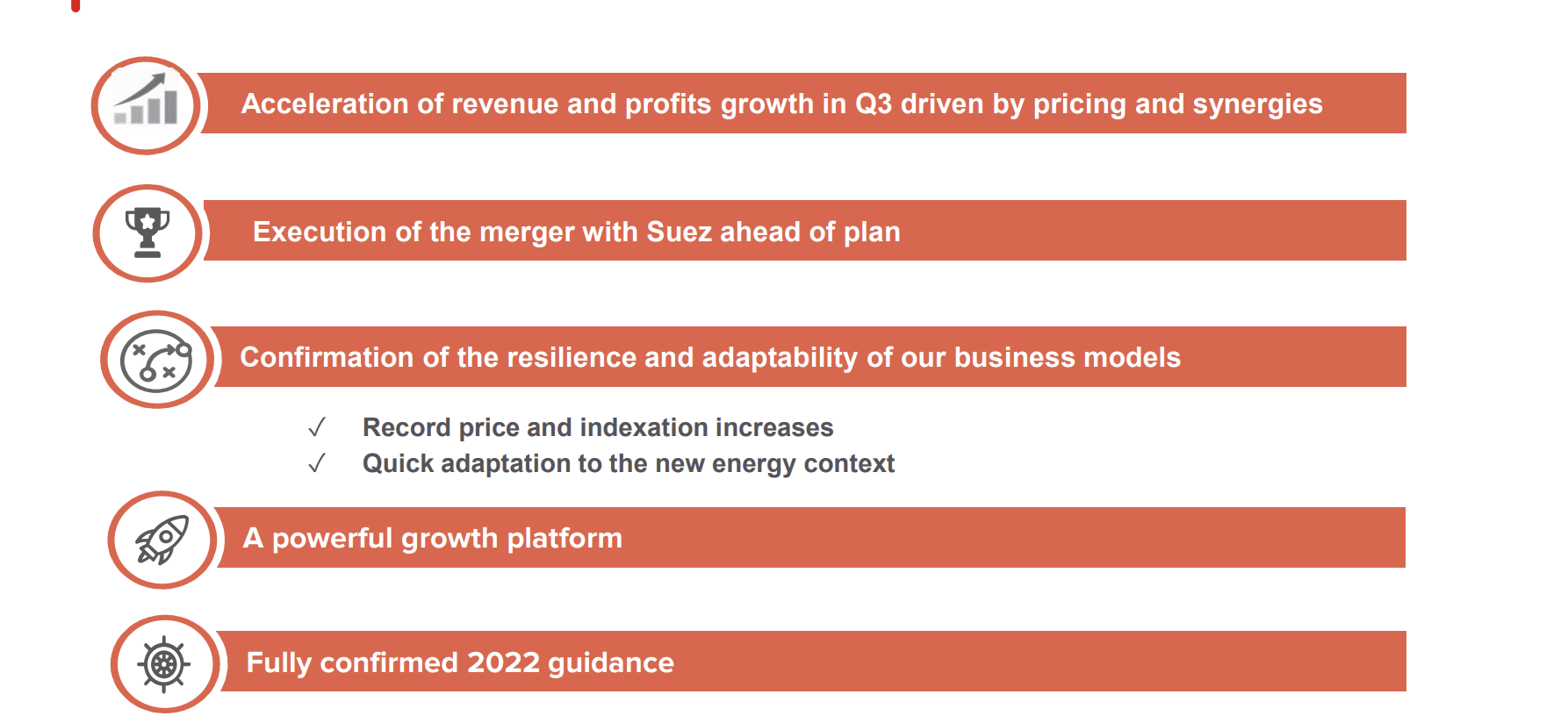

The results have been good. The latest set of results we have to look at are the 3Q22, and the company saw very impressive trends with revenues and profits both on the rise.

Revenue is up 13.7% YoY, and EBITDA is up almost 10% as well, with current pre-tax profit up almost 17% due to positive FX.

{kind=link}

Mergers ahead of schedule, good growth, resilience, and execution advantages - it's all good stuff coming in here. The company is also pushing pricing for its regulating bodies for its typical government services, and has managed higher indexations and record price increases for its services, with municipal water, waste, district heating, building energy services, and double-digit increases for Hazardous waste.

All in all, the companies and customers are seeing problematic pricing, but Veolia is enjoying its position and being able to offset most cost/inflation increases by pushing pricing here.

Also, we've more or less seen that Veolia is able to adapt its business model to meet the needs of a changing market. The ongoing energy crisis has reinforced the company's leadership in alternative, locally-sourced energy. The 2 company's main lines of business in energy are municipal and energy services and the company has already secured fuel not just for 2022, but for winter 2023 as well, as well for the beginning of 2024. Company activities in this segment are also, naturally, boosted by the high energy prices we are currently seeing.

Veolia is also seeking new opportunities in this segment.

{kind=link}

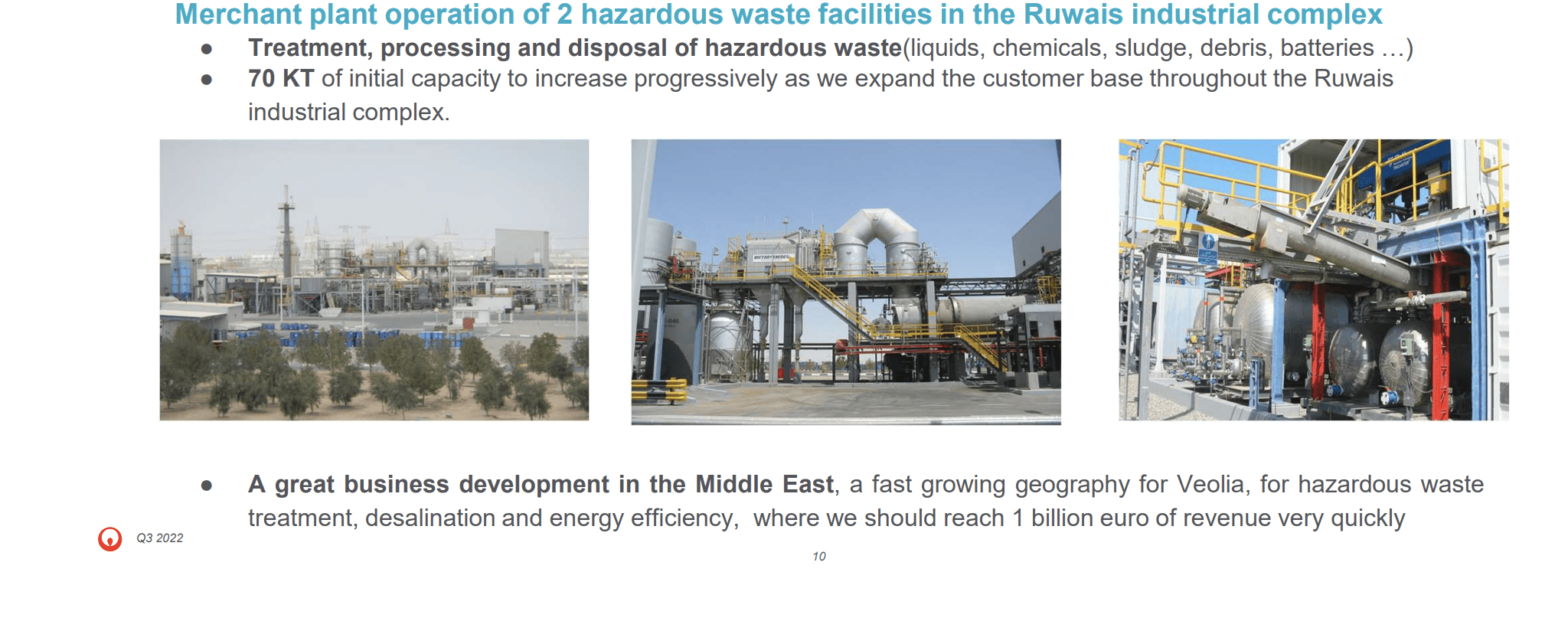

Additionally, the company is able to showcase some very excellent trends in waste collection, with new contracts and new business opportunities. For instance, hazardous waste management in Abu Dhabi is on the list here...

{kind=link}

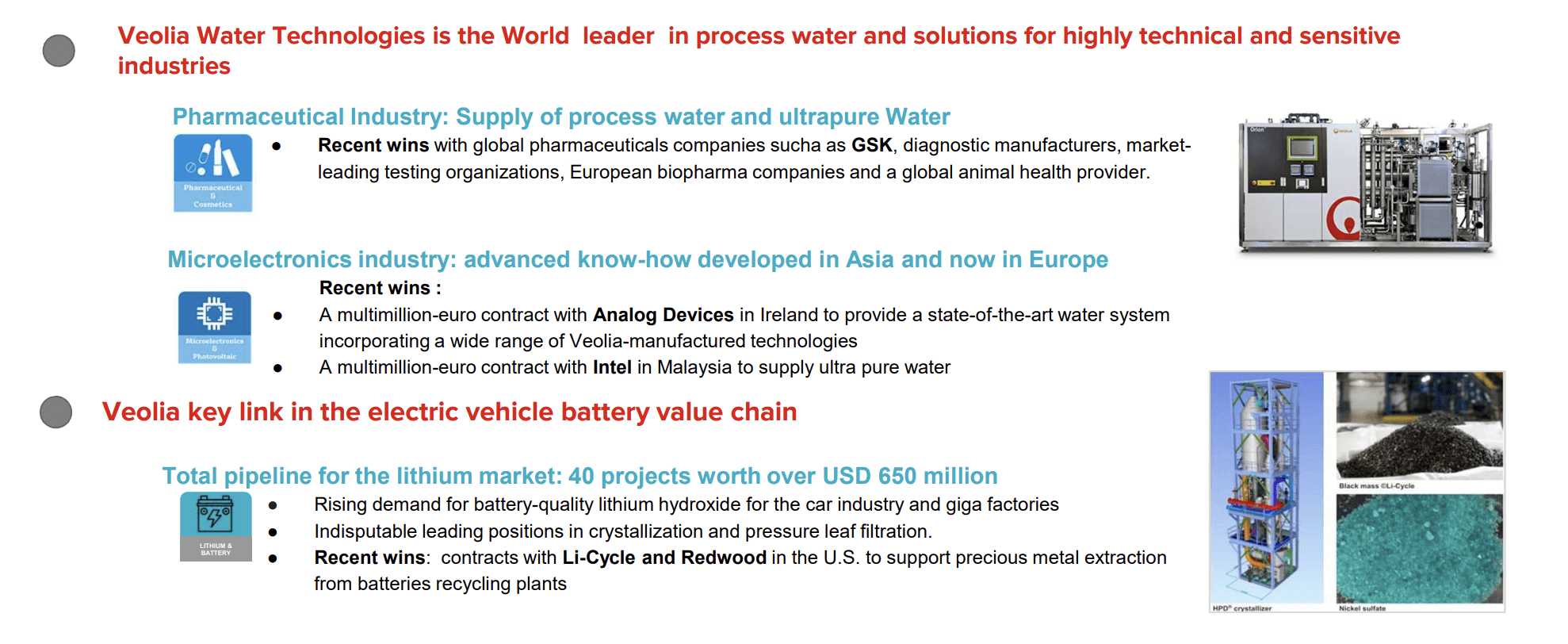

...and also, the company is increasing its water growth platform.

{kind=link}

The company has been able to deliver good cost discipline, and because it has been able to grow earnings, grow revenues, and deliver cost discipline and growth projects, this puts the company in a very good position to:

- Continue showcasing a very resilient sort of business, with a high efficiency

- Continue to deliver on accreditive and attractive mergers, like the Suez one, with €500M in cumulated synergies that are already ahead of schedule.

- Continue to work with a class-leading balance sheet and a sub-3x leverage post its divestment activities.

- Continue to grow in the next 2 years, fuelled by synergy, efficiency, and positives, regardless of how the macro goes.

- Continue to pay out an attractive 3-4% dividend, with the current dividend now confirmed for the coming year.

Because of this, I continue to call Veolia attractive as an investment here, and I go into the valuation section with this in mind.

The valuation for Veolia is convincing - it's time to move in deeper

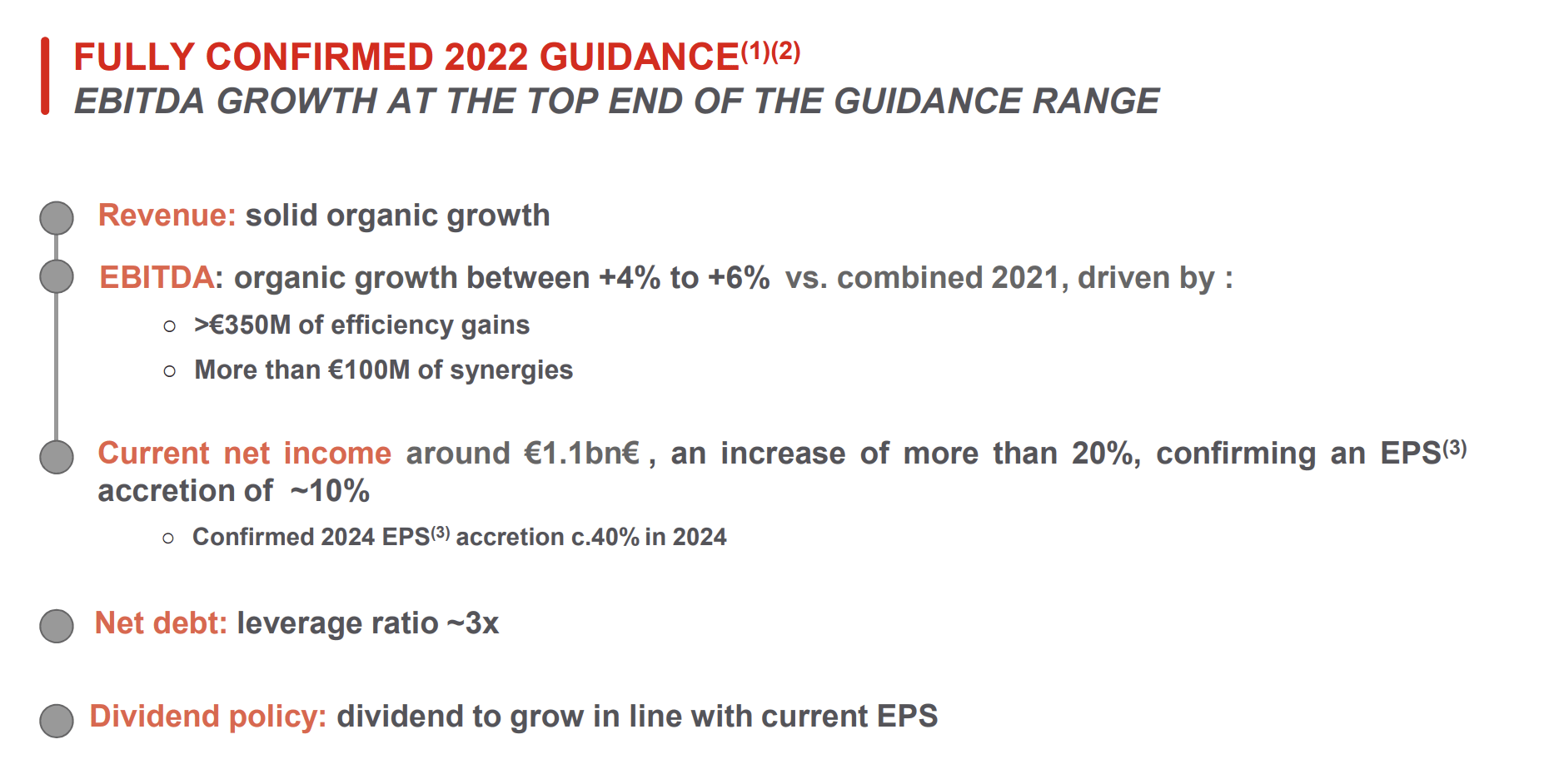

The company has delivered a Full-year guidance for this fiscal.

{kind=link}

And while the company does remain correlated to GDP, infrastructure expansion, and population growth, the company's fundamentals and strategies are so solid that I don't view these company risks as all that relevant to the long-term overall thesis here.

The company's one problem as I will say here, which also influences valuation, is its management. French companies are sometimes out of line with international ambitions - and this board has been slow on the uptake, instead for a long time being happy to let the company percolate in the single digits in a slow-moving national market. While this seems to be changing now, it's worth mentioning that German and French boards need watching to ensure they don't grow lax - and Veolia has been lax for some time. We need to keep an eye on this company's trends to make sure that things don't go out of bounds, and that the company continues to grow in line with expectations.

Veolia has an interesting valuation because even after a double-digit market outperformance, I would say that Veolia is still significantly undervalued here.

My own DCF work here, even with only a 2-3% EBITDA growth range and assuming as high a WACC as 8%, give us a ~€35 PT, which is down a bit from my last article, but I'm being conservative here to make sure that we're not straying too far from impacting the company's management and its somewhat weak historicals.

Remember, there aren't many relevant peers to the company. We could argue for American Water Works ( AWK ) and United Utilities ( OTCPK:UUGRY ). We also have Hera and FCC in Europe, as well as LYDEC, though this company doesn't have close to a comparable market cap.

Because of that, NAV, DCF, and historicals are the more interesting here, as I see it, and the more indicative of where the company could go in the long term. We of course also look at analysts overall, and where they compare in terms of PTs.

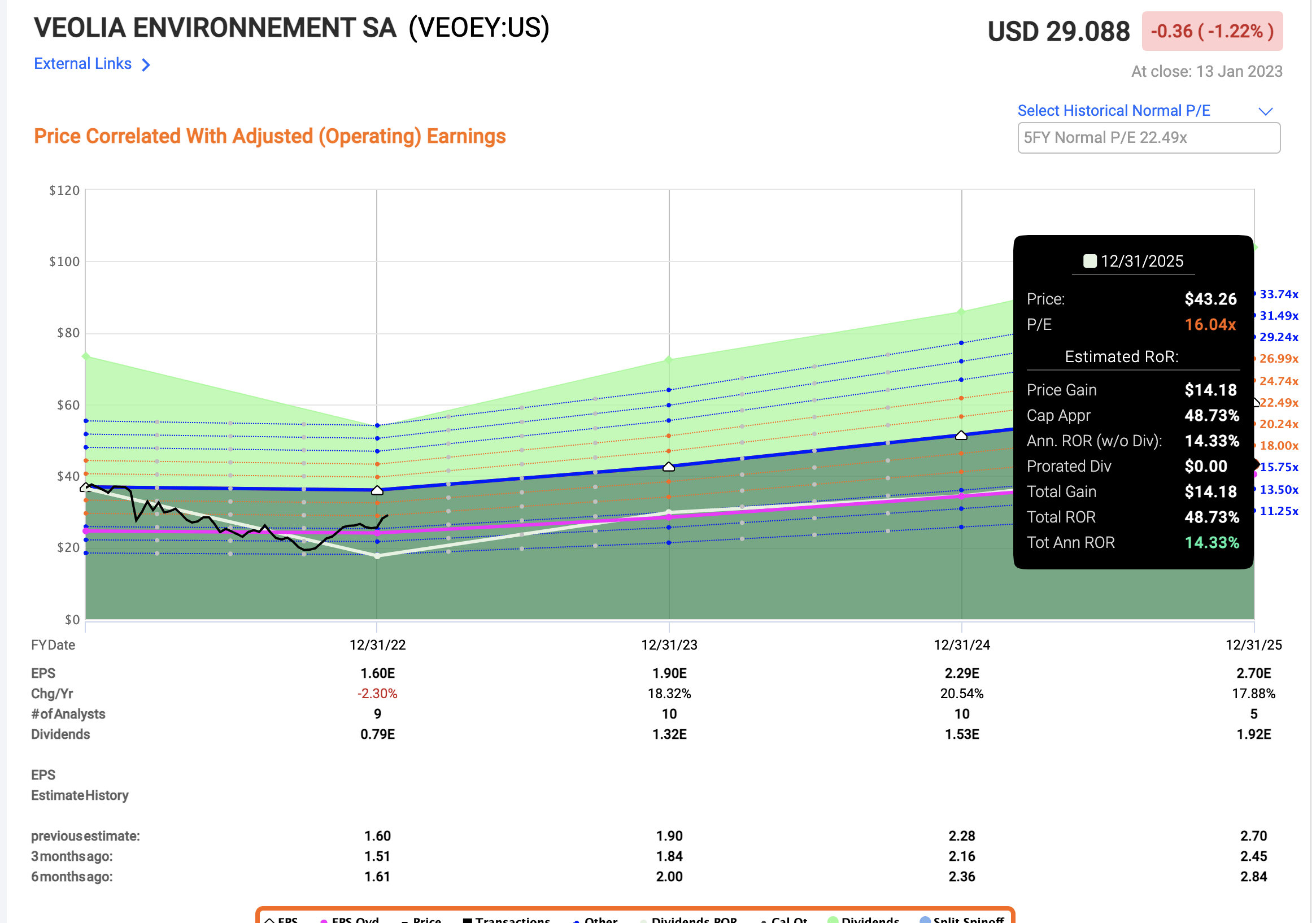

VIE trades on Euronext, and for the native ticker, we have a low of €21 per share and a high of €44 per share. 14 analysts follow the business, and 11 of them see an upside that's in the double digits here, coming to an average of €31/share.

I continue to believe that below €30/share, this company has utility-like safety and a massive, potential upside for conservative investors. There really isn't much to "dislike" about Veolia here, especially at this price.

My PT in my last article was €35/share, and while I impair this slightly to account for the higher costs of capital, costs of debt and overall costs of equity/expectations for returns, more than a €1 impairment down to €34/share is not something I'm willing to do.

Remember, the market is a violent and volatile place, in terms of ups and downs. It's my "job" as an analyst and a conservative investor to look past the noise - go past all of the "yelling", and try to find the sort of underlying truth here. As I see it, this is best done using math - historicals, forecasts, and facts.

We're no longer as cheap, but at $29 for the ADR, I believe we're still cheaper enough to interest you, given that the company is expected to grow at no less than 13-15% CAGR over the next 3 years.

Even conservatively at a range of 15-18x P/E, this implies an upside of no less than 14-15% annually, and as much as 20-30% in the case of full normalization, which would allow for triple-digit returns.

{kind=link}

Veolia remains conservatively BBB rated, and the dividend remains well-covered. All in all, I see a double-digit upside here for Veolia, and this leads me to my updated thesis for 2023.

Thesis for the common share

- Veolia is an attractive, undervalued utility-like company with recession-resistant sector exposure. While the company does have risks and potential downturns due to its correlations, the upside here is significant.

- The company has a solid set of 3Q22 results and is expecting results to still improve in the next couple of quarters. The company is still undervalued here - more than a double-digit upside isn't unlikely here.

- I view Veolia as a "BUY" here, and I give the company a PT of €34 - a downward adjustment of €1.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

This company fulfills every single one of my fundamental requirements - and is a "BUY" here.

For further details see:

Veolia: Yet Another European Outperformer That Remains A Buy