VEON - VEON: Looking Over The Deal

Summary

- VEON's stock has been hit hard this year due to its exposure to the Russian and Ukrainian telecom markets.

- Despite this, the company has shown resilience and its valuation is deeply discounted.

- The potential catalyst for the stock to rise in the upcoming quarters could be the recent announcement of a deal to sell its Russian assets.

Shares of VEON ( VEON ) have experienced a disastrous year, with a decline of over 70%. This is despite the fact that the stock, traded on the Nasdaq, actually saw an increase of nearly 80% in the past two months.

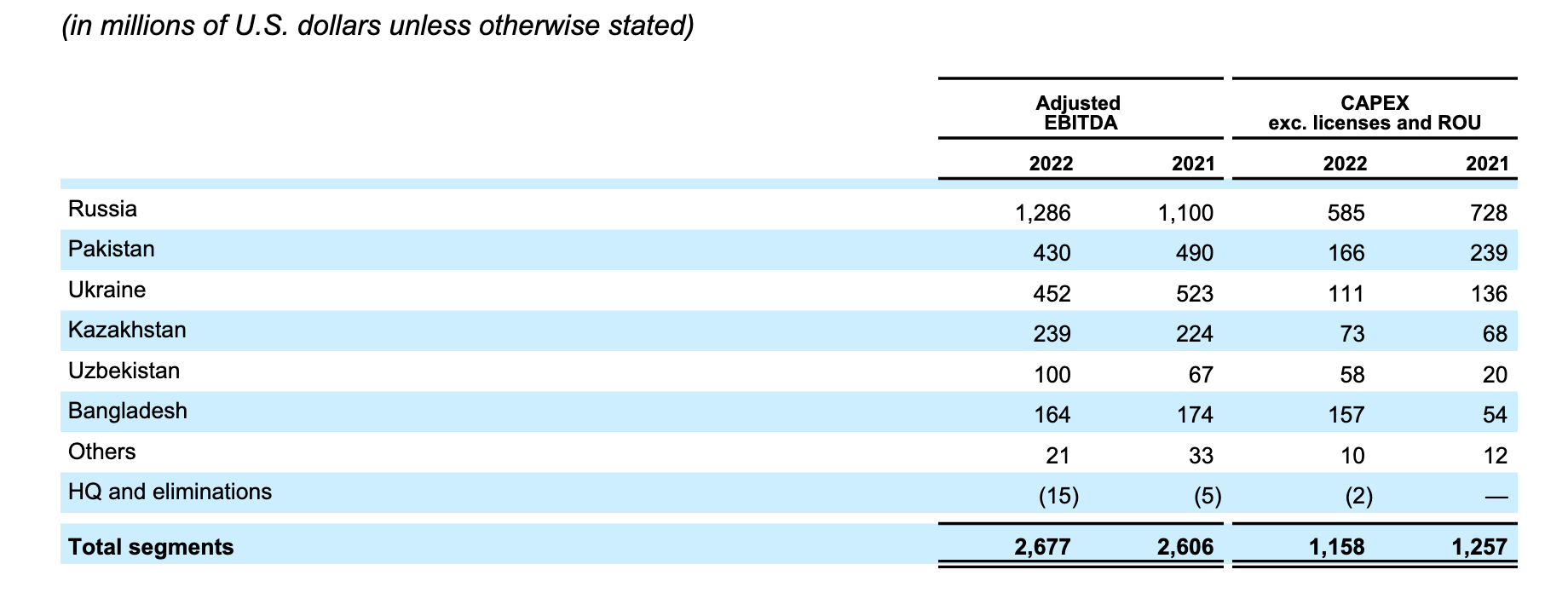

Surprisingly, VEON's business has proven to be quite robust so far: in the first nine months of 2022, for example, reported revenue and EBITDA increased by 3%. However, it should be no secret that the main reason for VEON's weak performance in 2022 is geopolitical, not economic. VEON is a telecommunications holding company that conducts a large part of its operations in Russia (through its subsidiary VimpelCom) and Ukraine (through Kyivstar): we are talking about more than 60% of the company's EBITDA. In the first nine months of the year, however, VEON's business was not significantly affected by the conflict: Kyivstar's revenue decreased by 3% year-on-year and EBITDA by 13%, with the devaluation of the Ukrainian currency playing an important role. The Russian business reported a 7% increase in revenue and a 17% increase in EBITDA, driven by the strength of the Russian ruble. Many risks and uncertainties remain as the company is obviously still in the midst of a major geopolitical confrontation, but at the same time there are also reasons for hope, with the announced sale of VimpelCom, which we will discuss in more detail, probably being the most important. Considering that the stock is still heavily oversold (price/EBITDA ratio of about 0.3 and EV/EBITDA < 3 at the time I am writing this), I am not sure that the valuation can be considered fair at this point, and that is the reason why I have placed a reasonable bet on this name (important disclosure: I bought the Amsterdam-listed shares, not the ADRs, which carry some additional risk).

A (too) vague deal

Some weeks ago we learned that VEON had reached an agreement to sell its Russian operations. This news, which had been the subject of many rumors in the preceding weeks and was then finally announced, caused VEON shares (especially ADRs) to rise by double digits, from a very low level at which they were previously trading. Although the announcement was welcomed by the market as it clearly addresses some regulatory concerns, the terms of the deal are not crystal clear, or at least they need to be interpreted. So let us try to look at them in more detail. First of all, it says that VimpelCom will be sold to some high-ranking managers in the group: this is an important point to understand. Indeed, the managers of VimpelCom are not poor, but they certainly do not have enough personal funds to buy out the company, i.e. the total amount of RUB 130 billion (about $2 billion) cannot come from them.

So, what is happening here? If we read the official explanations carefully, we can notice some important things: first of all, the proceeds aren't paid in cash.

It's expected that the entire consideration will be paid primarily by VimpelCom assuming and retiring certain debt of VEON Holdings B.V., thereby substantially reducing the burden on VEON's balance sheet.

Second, the deal implies a much higher valuation of Vimpelcom EV (370 VS 130 billion rubles): so what does this mean? Well, the simplest explanation is that VEON's so-called "Russian assets" are packaged into one company, which will then of course be deconsolidated, eliminating the associated liabilities as well. These obviously amount to 370-130=240 billion rubles. Consequently, VEON's net debt (see figure below) will also decrease by up to 370 billion rubles.

Company's Presentation

Well, 370 billion rubles currently correspond to $5.25 billion, while at the time of publication of the last VEON report they amounted to more than $6 billion. However, the reported figures should also be updated (reduced) due to the recent devaluation of the ruble. Overall, we can expect both gross net debt and net debt after leases to halve.

However, the company's EBITDA will also suffer a similar haircut: the current gearing ratio of around 1.8 net debt/EBITDA will thus remain unchanged after the acquisition. What will definitely change, of course, is the debt/equity ratio.

{kind=link}

It is worth noting that the level of Net Debt/EBITDA is somewhat correlated with the real assets a company owns: investors tend to accept much higher ratios when liabilities can be covered by assets (REITs, for example, usually cover their debt by two or three times, so investors in REITs even accept a net debt of more than 5 ). This confirms the correctness of the potential VEON deal as conceived. In summary, VEON is currently very cheap: its forward price to FCF, for example, is less than 3. Indeed, the company also faces high regulatory risk, which could be significantly reduced if it manages to sell its Russian assets.

However, profits will be cut in half next year if the deal goes through as expected. So management is trading a better risk profile (from a financial and regulatory perspective) for its profitability, which could make sense in the current environment.

Bottom Line

VEON's share price plunged 70% in 2022 as geopolitical unrest made uncertainty about the company's operations unbearable. From an operational perspective, however, the company has held up quite well, and the opportunity announced a month ago to sell its Russian assets on relatively favorable terms has helped dispel some skepticism about its future.

However, the risks remain high, even if the deal goes through as expected (which cannot be taken for granted). Refinancing the company's debt is probably the most critical issue, as interest rates are gradually rising everywhere. The geopolitical and regulatory confrontation isn't going to ease anytime soon, and it's also worth noting that the stock may be delisted from Nasdaq as it trades below the $1 threshold, although admittedly this issue can be smoothly resolved with a reverse split. All in all, the company is currently a speculative buy, and conservative investors probably need more clarity before considering the purchase.

For further details see:

VEON: Looking Over The Deal