VRA - Vera Bradley: Financials Are Improving But Risks Remain

2023-08-07 07:57:49 ET

Summary

- Vera Bradley's revenue increased by 4.2% YoY, while operating loss (% of revenue) decreased to 6.8%.

- An increase in guidance for 2023 supported the company's quotes.

- After the growth of quotes, my recommendation is hold, as I see more risks than additional growth catalysts.

Introduction

Vera Bradley (VRA) shares have risen 44% YTD. Despite the fact that the company's shares are still relatively cheaply priced by multiples, I don't think this is the best time to go long.

Investment thesis

While the company has been able to show improvement in operating and financial performance, I currently have a hold recommendation for the company's stock. First, I don't expect to see a quick recovery in discretionary consumer spending if inflation falls in the second half of the year because consumers will continue to face higher daily spending. Secondly, in accordance with guidance for 2023 (calendar), the company continues to expect relatively low revenue growth rates (from -2% to +2%), which, in my opinion, may limit the company's ability to increase operating margin in view of the absence of the effect of leverage, since part of the operating expenses (rent, salary) are fixed. In addition, the stock has risen strongly since the beginning of the year and reflects the company's guidance for 2023, which I consider to be quite ambitious and optimistic, which in my opinion will not be easily beaten.

Company overview

Vera Bradley designs, manufactures and sells bags, luggage and accessories for women. The main business segments are VB Direct (62% of revenue), VB Indirect (16% of revenue) and Pura Vida (21% of revenue). The VB Direct segment includes 48 full-line stores and 80 factory outlet stores, and the VB Indirect segment includes 1,700 partner stores. The Pura Vida brand targets girls aged 18 to 24. The company operates in the US market.

1Q 2024 (fiscal) Earnings Review

At the end of the quarter , the company's revenue decreased by 4.2% YoY due to a decrease in comparable sales by 3.3% YoY. We see the largest declines in the VB Indirect and VB direct segments, where revenue decreased by 9% YoY and 4% YoY, respectively, while the Pura Vida segment increased by 1.2% YoY.

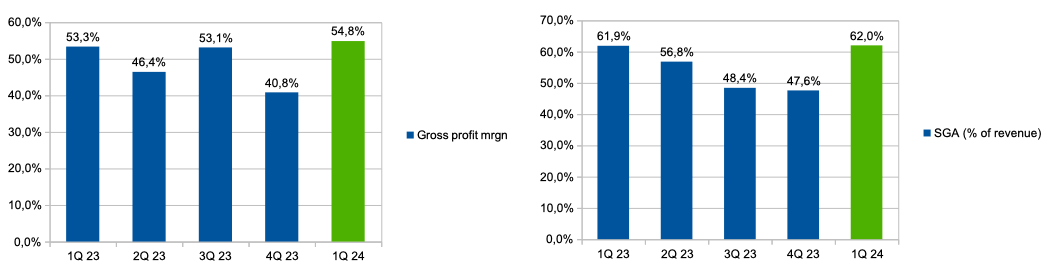

Gross profit margin increased from 53.3% in Q1 2023 (fiscal) to 54.8% in Q1 2024 (fiscal) due to lower freight costs. SGA spending (% of revenue) slightly increased from 61.9% in Q1 2023 (fiscal) to 62% in Q1 2024 (fiscal). You can see the details in the chart below.

Margin trends (Company's information)

{kind=link}

Thus, operating loss (% of revenue) decreased from 8.4% in Q1 2023 (fiscal) to 6.8% in Q1 2024 (fiscal). You can see the details in the chart below.

Op. loss (consolidated) (Company's information)

If we look at operating income by segment, we can see that the biggest contributor was the VB Direct segment, where operating income increased from 8.9% in 1Q 2023 (fiscal) to 12.5% ??in 1Q 2024 (fiscal). ) and the Pura Vida segment, where operating income increased from 5.3% in 1Q 2023 (fiscal) to 7.8% in 1Q 2024 (fiscal), while in the VB Indirect segment we see a decline from 32.3 % in Q1 2023 (fiscal) to 30.6% in Q1 2024 (fiscal). You can see the details in the chart below.

Op. income by segment (Company's information)

{kind=link}

I would like to point out that the company has published strong guidance for 2024 (fiscal) . Thus, management expects revenue to be $490-$510 million, which implies a decline/growth of -2% - 2% YoY. In addition, the company expects gross profit margin to improve by 120-240 basis points to 52.8% - 53.8% due to lower freight costs and increased operating efficiency. I note that the company publishes guidance based on Non-GAAP.

My expectations

At the moment, I like the fact that the company continues to focus not on increasing the number of stores, but on improving operational efficiency. In addition, the updated guidance indeed, in my opinion, reflects the company's strategy, however, in my personal opinion, the current positive forecasts contain a number of risks, while the quotes have already responded strongly to the increase in EPS forecasts.

Firstly, I am confused by the fact that comparable sales continue to be in the negative zone due to a decrease in traffic, which is not compensated by an increase in the average check due to the ability to pass on higher inflation to the end consumer.

Secondly, most of the company's expenses such as salaries, rent and production are fixed. On the one hand, I like that the company is talking about cost-cutting initiatives, on the other hand, in an environment of low revenue growth, I believe it will not be easy to achieve a leverage effect that can support operating margins.

Risks

Margin: reduced economies of scale can lead to deleverage, which can have a negative impact on operating profitability. In addition, an unfavorable change in the product mix and increased marketing costs due to increased competition can also put pressure on margins.

Macro (general risk): a decrease in real income may lead to a reduction in consumer spending in the discretionary segment, and, consequently, a decrease in revenue growth rates.

Drivers

Pura Vida: in line with management comments, the company plans to provide a new store opening plan in the Pura Vida segment by the end of 2023, which could result in both higher revenue and improved operating margins.

Revenue: efficient marketing spend could have a positive impact on store traffic dynamics, which could boost revenue in the VB Direct and Pura Vida segments in the coming quarters.

Valuation

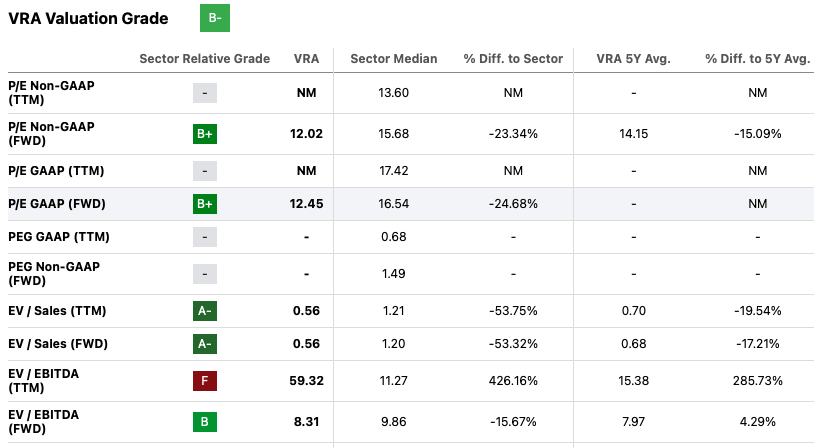

Currently Valuation Grade is B-. Under P/E ((FWD)) and EV/EBITDA ((FWD)) multiples, the company trades at 12x and 8.3x, respectively, implying a discount to the sector median of around 23% and 16%, respectively. On the one hand, I still find the current valuation attractive, but on the other hand, I believe that it is not worth making a purchase decision based only on a relatively low valuation. First, in my personal opinion, the company's valuation deserves a discount due to low revenue growth, low capitalization and operating loss. Secondly, I see additional risks after EPS upward revisions after the company provided ambitious guidance for 2024 (fiscal) year. So, if the company reports worse than expected, then we can see a correction in share prices.

{kind=link}

Conclusion

On the one hand, I like how the company was able to demonstrate an improvement in operating margins, especially in the Pura Vida segment, however, on the other hand, in my personal opinion, the current level of quotes is based on the company's ambitious guidance, where I see more risks than opportunities, so now my recommendation is hold. I will continue to monitor the company's financials and will gladly change my recommendation if I see sustained changes in the company's financials in the coming quarters.

For further details see:

Vera Bradley: Financials Are Improving, But Risks Remain