VRA - Vera Bradley: On The Mend

2023-11-09 14:58:48 ET

Summary

- The stock of Vera Bradley, a women's fashion retailer, has delivered remarkable returns of 125% since the new CEO took over roughly a year ago.

- We pick out some of the major improvements seen in the business and examine what could stick and what may ease.

- Valuations look fair and the stock may be close to hitting a crucial pivot point.

Introduction

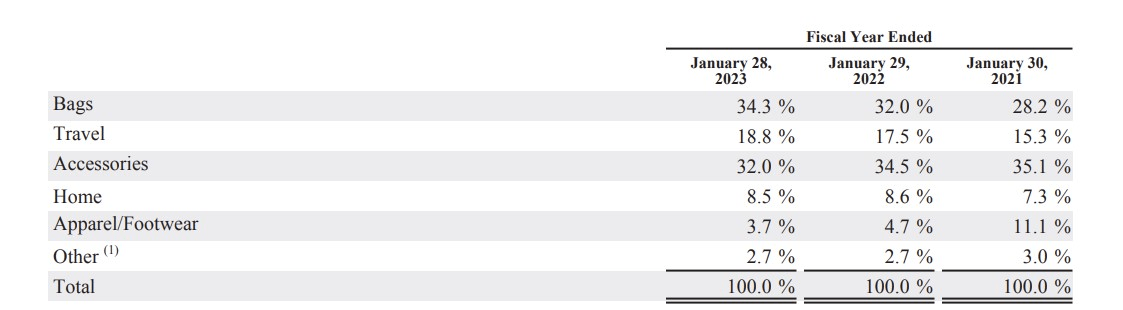

Vera Bradley, Inc. ( VRA ) is a micro-cap American-based retailer that primarily dabbles in the women’s fashion landscape. Previously, the bulk of its sales mix consisted of accessories, but recently, the sale of bags has taken precedence.

{kind=link}

Annual Report 2022

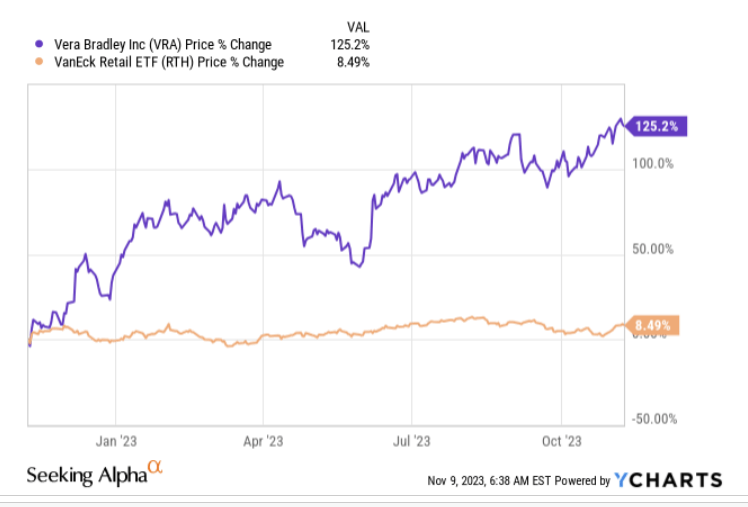

VRA saw a changing of the guard at the very top around a year ago, and since then the stock has fared exceedingly well, delivering returns of 125%, whilst also trouncing the VanEck Vectors Retail ETF ( RTH ) by a huge margin.

{kind=link}

YCharts

Could the momentum continue? Well, here’s what we think about the business and the stock of VRA.

Convalescing Well

VRA has faced plenty of difficulties in the past, but a lot of metrics are now trending in the right direction under the guidance of the new management team (they even appointed a new CFO in May- Michael Schwindle with three decades of experience in the retail space alone).

With a number of store closures carried out last year, it was always going to be a tough ask to expect ample YoY growth so soon, but the cadence of revenue declines appears to be slowing. After declining by -4% YoY in Q1, the revenue growth decline in Q2 only came in -2%, and it's quite possible that we could end up with flattish revenue growth by the end of this year.

Management has guided to a FY range of $490-$500m , but consensus has already locked in a figure that is on par with the upper end of this range. This would put it in line with last year’s revenue. The company is putting in place certain new strategies that could help drive traffic and boost the average order size and don’t be surprised to see the benefits of this flow through in Q4.

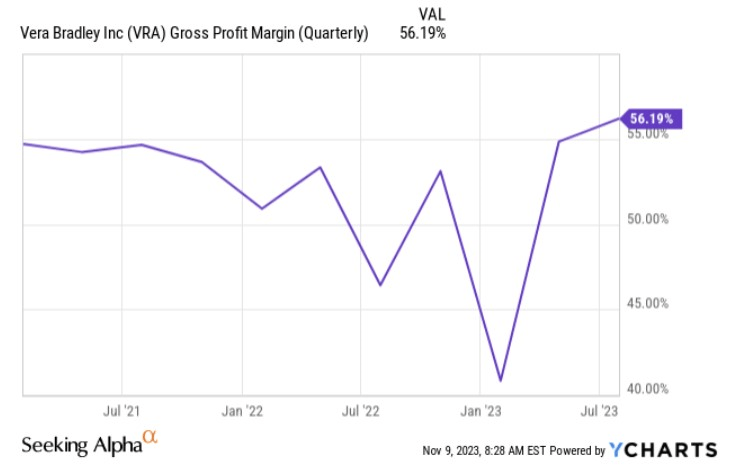

One metric that appears to be rather strong at the moment is the gross margin which recently rose by 470bps YoY and hit 3-year highs. Some of the YoY impact could be attributed to an inordinately weak base effect, but the company is still getting solid benefits through lower freight costs and better sell-throughs.

Now looking ahead, you would think some of the GM momentum may ebb, as VRA promotion activity will likely step up with the onset of the holiday season. In fact, for the FY management expects gross margins to come in at a slightly lower cadence of 53-53.8%, but note that even those levels would represent an impressive YoY improvement of 260-340bps.

{kind=link}

YCharts

Further below the line, improvements will also be seen on the SG&A front, as the company has been reworking its expense structure. The goal is to bring through $12m of cost reductions this year, and this should see the SG&A expense run rate come below last year’s figure of $245m.

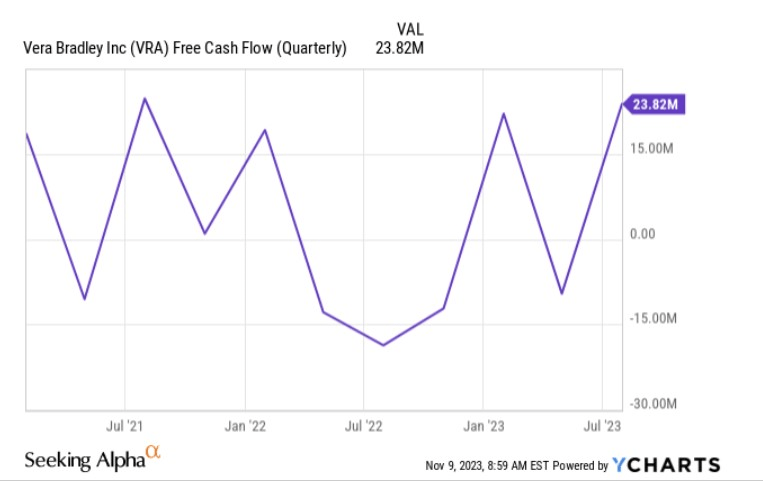

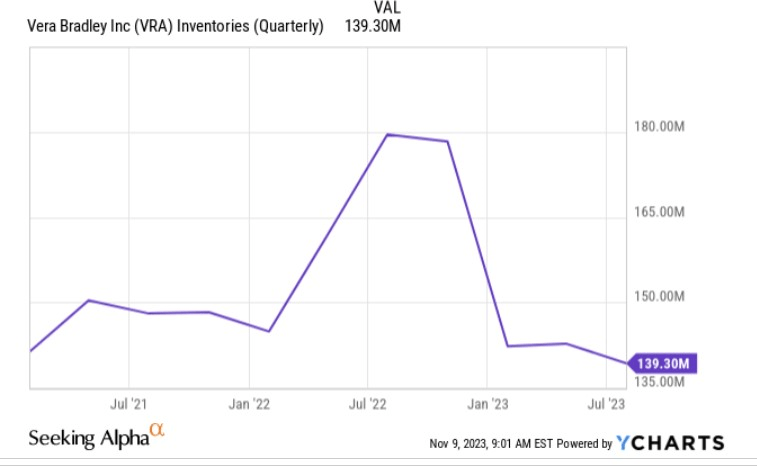

If there’s one key area where we think there still is some question marks, it’s the FCF metric, as this has been quite wobbly for multiple quarters now.

{kind=link}

YCharts

In three out of the past four quarters, inventory drawdowns have proven to be a very useful source of operating cash inflow, but now with the holiday season upon us, we don’t think VRA will be best placed to reduce its inventory position even further, and this may prompt the FCF to slip back into negative territory yet again.

{kind=link}

YCharts

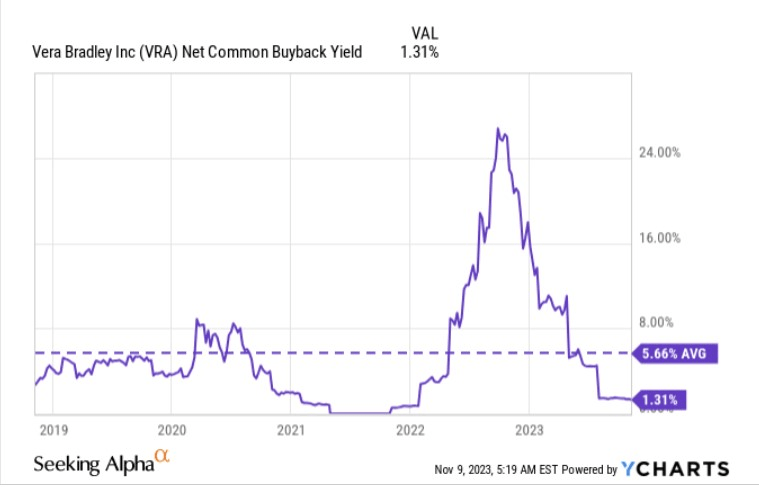

Sustained FCF generation will be key if one is to see a meaningful pick-up in the share buyback activities of VRA. Note that in recent quarters, Vera has barely indulged in any buybacks, so much so its current shareholder yield is around 430bps lower than its historical average. What’s key is that its current $50m share buyback program (which was initiated in December 2021) will come to an end by December 2024, and so far, VRA has executed only 48% of that plan.

{kind=link}

YCharts

One other admirable facet of VRA is that it doesn’t have any traditional financial debt on its balance sheet (although it does have $66m of capital leases), and even though it has a $75m ABL facility, it wouldn’t seem right to tap that to beef up the buybacks.

Closing Thoughts- Valuation and Technical Considerations

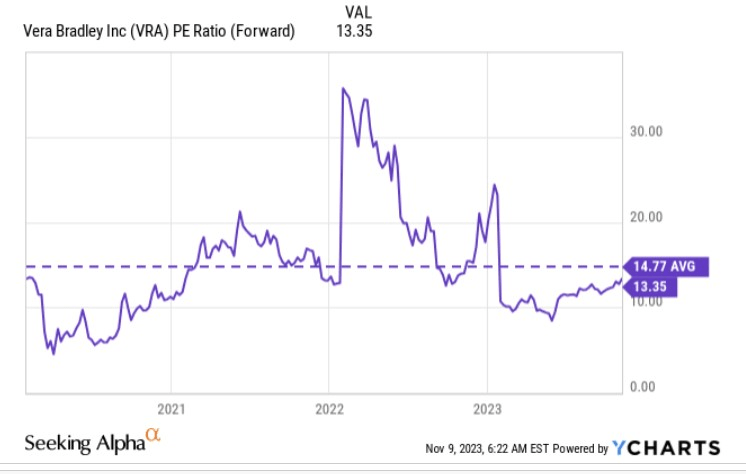

VRA’s valuation quotient looked very attractive in the middle of this year, but now we’re not overly swayed by it. On a forward P/E basis, the stock now trades at 13.4x P/E, only a 10% discount to its long-term average.

{kind=link}

YCharts

Besides, if one tracks consensus EPS estimates through the next two years, it looks like this is a business that could deliver earnings CAGR of 13%. So 13x P/E for 13% earnings translates to a PEG of 1x and that feels about fair.

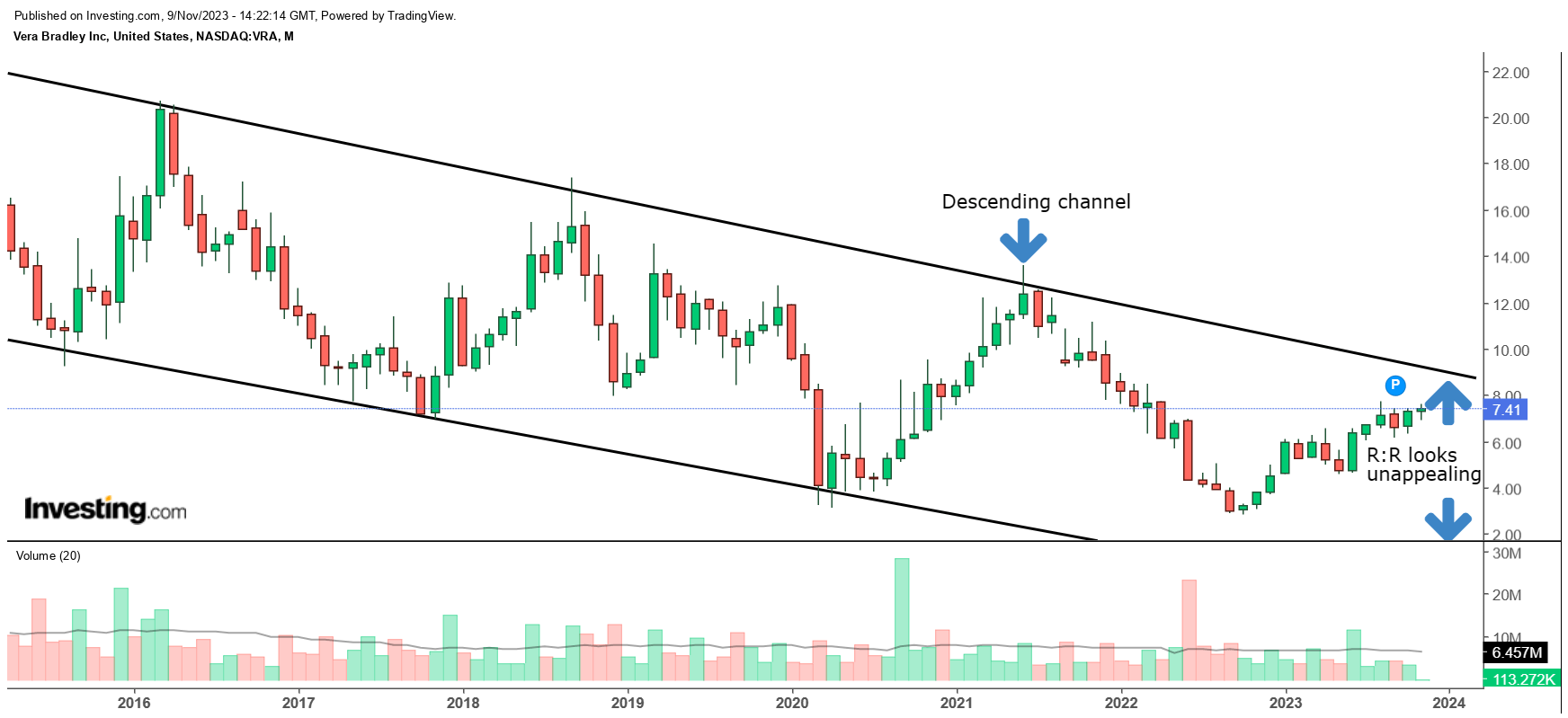

Then if we view VRA’s long-term price imprints it's clear that over the last 7-8 years this is a stock that has moved around within a certain descending channel. Making tactical bets around the boundaries of this channel has so far worked really well, and given that the price is not too far from hitting the upper boundary of the channel, we wouldn’t be too keen on kickstarting a long position here. It’s also worth noting that after months of dormant insider activity, the CEO chose to exercise and sell some of her stake at the start of this month.

{kind=link}

Investing

To conclude, VRA is a HOLD here.

For further details see:

Vera Bradley: On The Mend