VCYT - Veracyte: Testing Numbers Stretching Higher But Valuations Uncertain

2023-08-17 09:00:00 ET

Summary

- Veracyte posted Q2 FY'23 earnings with continued growth in revenues and cash collections.

- The company's Decipher acquisition has shown positive results, with an increase in testing volumes.

- Despite potential investment value, uncertainties remain on the stock's ability to sell above its resistance level of ~$30/share.

- Net-net, reiterate hold.

Investment briefing

Veracyte (VCYT) posted Q2 FY'23 earnings last week with continued growth at the top line and excellent uptick in cash collections. I'd encourage you to read my last publication, where I performed a deep dive on each of the company's core offerings, in addition to a dive on the prostate cancer diagnostics and treatment markets. VCYT's Decipher acquisition has begun to bear fruit, evidenced by the rate of testing volumes over the last 12-18 months.

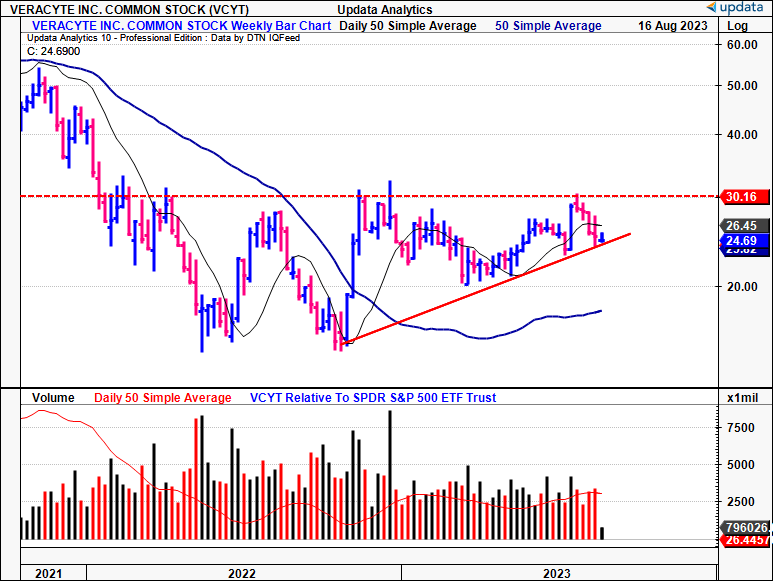

Despite the facets of potential investment value, these are balanced by uncertainties on the prospect of its selling above the band it has caught since 2022. As seen in Figure 1, it is wedging up to previous highs, but the $30 level appears to be a major level of resistance for the equity stock. This analysis will break down the economics driving VCYT's market returns and closely examine the financial and intangible results driving these numbers. Net-net, I continue to rate VCYT a hold on valuation grounds.

Figure 1.

{kind=link}

Q2 FY'23 earnings insights - in tandem with historical run rate

1. Top-line disaggregation

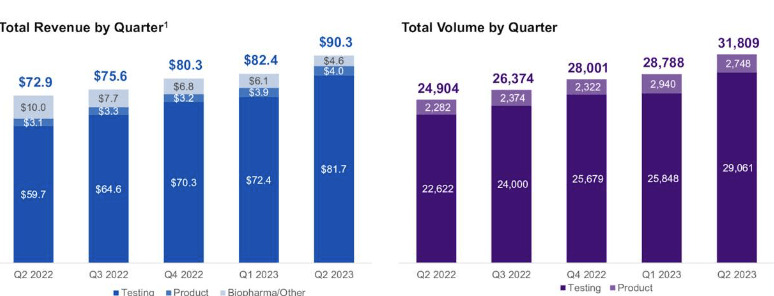

Starting with its latest numbers first, VCYT booked $90.3 mm in quarterly revenues, up 24% YoY. Critically, total volumes came to ~31,800 tests, a YoY increase of 28% from last year. It also booked ~$4mm in product revenue and another $4.5mm in biopharma (and other) revenues.

Overall testing volumes were 29,000 for the quarter. The volume mix comprised ~13,000 Afirma tests and around 15,000 Decipher Prostate tests. It was noted in the last publication that VCYT has made considerable efforts to enhance the test experience in its Afirma segment for both providers and patients. This drive bore fruit, as >70 new accounts were onboard this quarter.

In addition:

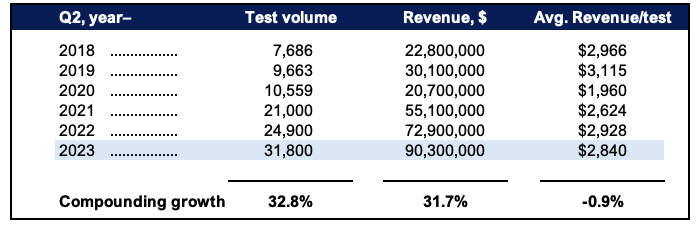

- The firm's volume and revenue growth as recorded at Q2 from 2018-'23 are noted below. Total quarterly volumes and total revenues are shown. Note, the overall volume and avg. revenue/test will be slightly off total testing volume due to gaps in utilization, and the fact VCYT books the income at the delivery of the test results.

- For example, Q2 revenue from quarterly testing reached $81.7mm, up 37% YoY. Decipher Prostate and Afirma volumes underscored the growth. The total testing volume amassed c.29,000 tests, on an average selling price ("ASP") of $2,800 per test. This figure was bolstered by roughly $2mm attributed to out-of-period collections. Extracting this, the testing ASP stood at >$2,700.

- From Q2'18-'23, VCYT has compounded volume and turnover at ~32% each; thus, last quarter's numbers were roughly in-line with these rates. The path over the last 12 months is shown with more granularity in Figure 3.

Figure 2.

{kind=link}

Figure 3.

{kind=link}

By the same token, its Decipher Prostate testing division showed considerable upside last period. For a deep dive on the Decipher test, and the underlying Prostate Disease treatment market economics, see the last VCYT publication. But basically, the segment is combined from the Decipher prostate biopsy ("DPB") and Decipher radical prostatectomy ("DRP") diagnostics to identify prostate cancer. VCYT bought the Decipher business in FY21' for $600mm, and it already is bearing fruit to the investment tree.

Despite its modest sales team of ~45 in the headcount, it exhibited impressive productivity in my opinion. The company reported conducting around 15,000 Decipher Prostate tests during the quarter, marking a 50% YoY expansion in volume when compared to the 10,000 tests carried out last year. This equates to the average rep hitting 333 tests vs. 222 on a comparable basis last year, an increase of 111 tests per rep.

2. Cash collections driving FY'23 guidance raise

The pace of sales growth on costs saw it produce $16.7mm in OCF for the quarter, a record for the company. The cash flow bridge from Q2 last year to the last period is observed below. Excluding maintenance charges, most of the change comes from cash receipts on inventories, reduction in receivables and cash inflows from payables-true cash inflows. This saw it run from an outflow of $0.4mm last year to the c.$17mm mentioned.

That VCYT realized these inflows is critical in my view. It's all well and good to continuously book testing revenues forward. But less meaningful if these fail to convert to cash on the settlement of the test accounts. These are good economics leading into H2 FY'23.

Figure 4.

Sources: BIG Insights, Company filings

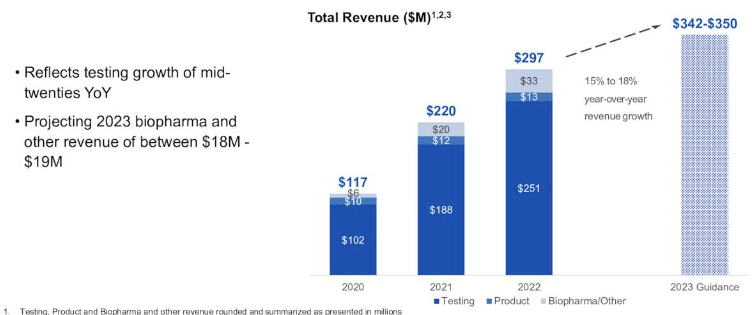

Consequent to this momentum, the firm has raised its FY'23 outlook. It now forecasts:

- Total sales in the range of $342mm-$350mm, a revision from the earlier guidance of $330mm to $340mm. This calls for 15-18% growth at the top line, around half the pace of its 5-year growth rates.

- To get there, it looks to "mid-20s growth in testing revenue" on biopharma and other sales of $18mm-$19mm.

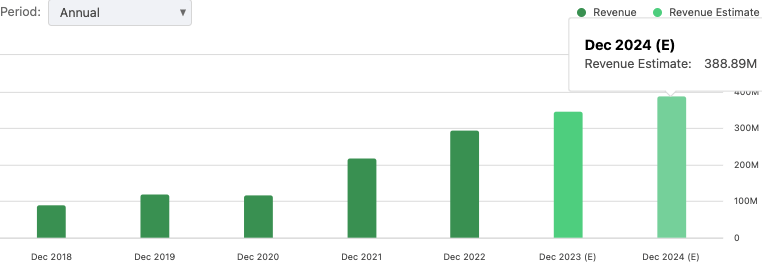

This is a decent sales ramp as seen in Figure 5, reflected in the consensus view on sales into FY'24 [Figure 6].

{kind=link}

Figure 6.

{kind=link}

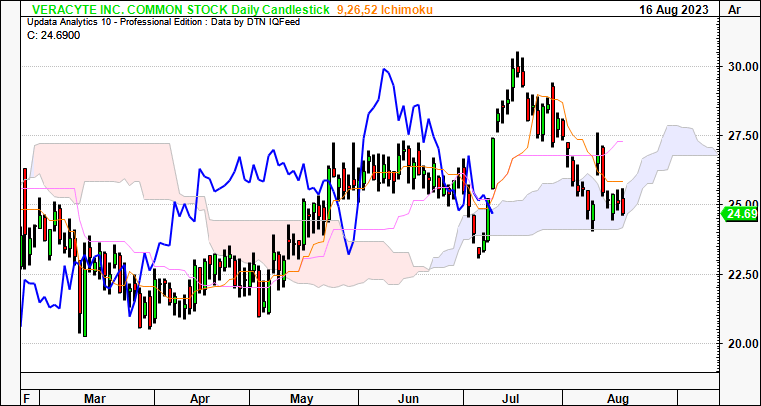

The technical take

Detailed trend analysis from the market-data doesn't support an entry at the current prices. For starters, the daily cloud chart show below, which looks to the coming weeks, is neutral in my view. The lagging line has breached the cloud top and the price line has been trading within the cloud for the past week or so. A break above $27.80 would be needed as confirmation into a bullish zone based on the chart below. The good news is, that the last 2 tests at the cloud based has resulted in the stock rebounding with authority.

Figure 7.

{kind=link}

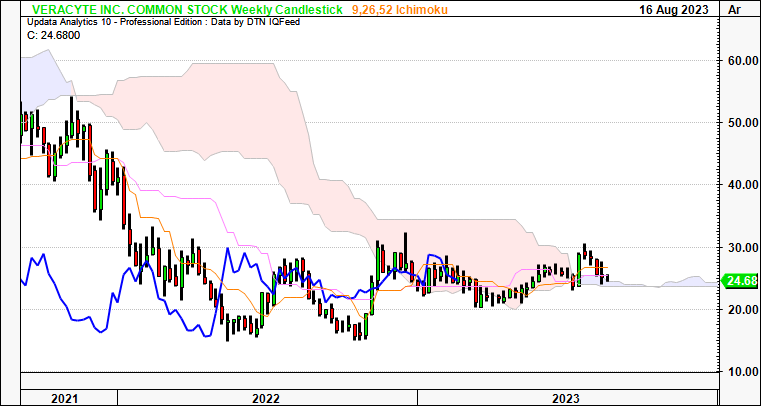

The weekly chart, that looks to the coming months, is also neutral. Both price and lagging lines are trading into the cloud, backing and filling within a tight set of closes. Without an impeding set of catalysts, it is difficult in my eyes to see VCYT catching a bid to drive the stock north from here. Not saying it isn't possible, not at all. But I'm not the one to punt on small caps in this regard.

Figure 8.

{kind=link}

As a potentially bullish point, we have upside targets to $37.50 on the point and figure studies below. But this is balanced by the breadth of additional targets to $16 or so. The breadth in price objectives thrown out by the P&F studies is also a neutral factor in my view. It shows uncertainty in price action and that the order book is likely either 1) stacked evenly on both sides, of 2) relatively shallow on both sides of the account. For the long account, you'd need demand up to $27 to activate the $37 upside target.

Figure 9.

Data: Updata

Valuation and conclusion

The stock is selling at 5x forward sales on just $1.68 for every $1 in market value. To me this is quite the premium at 5x forward. Sales growth is slipping behind 5-year averages, and the firm added just 3 cents-$0.03-in book value per share over the last 12 months to $14.90/share. In fact, valuing VCYT as a function of net asset value/share, investors have seen ~$0.70 in net worth wiped from their equity position ($15.50-$14.90 = 0.7).

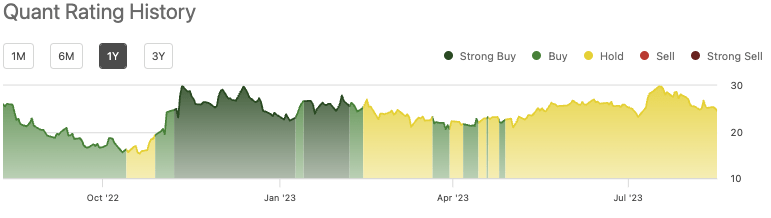

At 5x forward, at the upper end of management's estimates, this gets you to $24.05 in implied market value, a shade off the current price as I write. Say you're after a 14% return on investment, you'd need VCYT to produce $410mm in top-line sales this year to command a valuation of $28/share (5x410/72.75 = $28 ; 28/24.56-1 = 0.14). These findings are in line with estimates above, and support a neutral view in my opinion. Critically, these findings are objectively supported by findings of the Quant System, which also rates VCYT a hold on a composite of factors.

Figure 10.

{kind=link}

In short, VCYT continues winding up the compass of growth, however this is yet to pull through at the market level. Investors are selling the stock at a premium, but it's yet to catch a reasonable bid. You'd need a break to ~$27 based on technical findings to suggest it is trading on buying volume in my opinion. Moreover, FY'23 sales estimates gets you to the current market price, thereby no mispricing in my view. Net-net, I continue to rate VCYT a hold.

For further details see:

Veracyte: Testing Numbers Stretching Higher But Valuations Uncertain