CXM - Verint Sees AI-Chatbot Demand But Needs To Produce Meaningful Growth

2023-12-13 12:30:21 ET

Summary

- Verint Systems Inc. reported better-than-expected financial results for Q3 2024, beating revenue and earnings estimates.

- The company offers customer and stakeholder engagement software globally and is transitioning to a SaaS-based delivery and revenue model.

- Verint's financial trends have been volatile, and management needs to demonstrate consistent growth and earnings results.

- While the AI-chatbot growth is intriguing, I remain Neutral [Hold] on Verint Systems Inc. stock for the near term.

A Quick Take On Verint

Verint Systems Inc. (VRNT) reported its FQ3 2024 financial results on December 6, 2023, beating both revenue and consensus earnings estimates.

The firm provides customer and stakeholder engagement software to businesses globally.

I previously wrote about Verint in June 2023 with a Hold outlook on slowing customer activity amid the company's transition to a SaaS focus.

While the company is producing intriguing results via demand for its AI-enabled chatbots, Verint Systems Inc. management needs to prove it can reignite growth and produce more predictable earnings results.

I remain Neutral [Hold] on VRNT in the near term.

Verint Overview And Market

New York-based Verint provides various customer and stakeholder experience tools for organizations to improve their engagement and customer service capabilities.

The firm is led by founder and CEO Dan Bodner. He became Chairman of the Board of the company in 2017.

Verint’s primary offerings include:

-

Forecasting and Scheduling

-

Quality and Compliance

-

Conversational AI

-

Engagement Orchestration

-

Experience Management

-

Interaction Insights

-

Real-Time Work

-

Engagement Channels

-

Knowledge Management

-

Fraud and Security Solutions.

VRNT seeks new customers via a direct sales model as well as through partner referrals, with customers typically starting off with a subset of its offerings and then growing in the number of products they use over time, known as a "land and expand" approach.

According to a recent market research report by Mordor Intelligence, the market for customer engagement solutions was an estimated $19.7 billion in 2023 and is forecast to reach nearly $33.1 billion by 2028.

This represents a forecast CAGR of 11% from 2023 to 2028.

The primary reasons for this expected growth are the increasing usage of customers of smartphones and a desire by businesses to connect more frequently and meaningfully with prospects and customers in a more automated and cost-efficient manner.

Also, the Retail and Consumer Goods industries are expected to account for a large part of the market share of demand for solutions, while the North American region will likely retain the highest market share by region.

Major competitive or other industry participants include:

-

Avaya

-

Aspect Software

-

Calabrio

-

Genesys

-

IBM

-

Nice Systems

-

Nuance Communications

-

OpenText

-

Oracle

-

Pegasystems.

Verint’s Recent Financial Trends

Total revenue by quarter (blue columns) has dropped YoY due to lengthening sales cycles; Operating income by quarter (red line) has been volatile:

Seeking Alpha

Gross profit margin by quarter (green line) has turned up recently, likely as a result of increased SaaS revenues, which have a higher margin. Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have fluctuated materially recently:

Seeking Alpha

Earnings per share (Diluted) have been highly variable in recent quarters:

Seeking Alpha

(All data in the above charts is GAAP.)

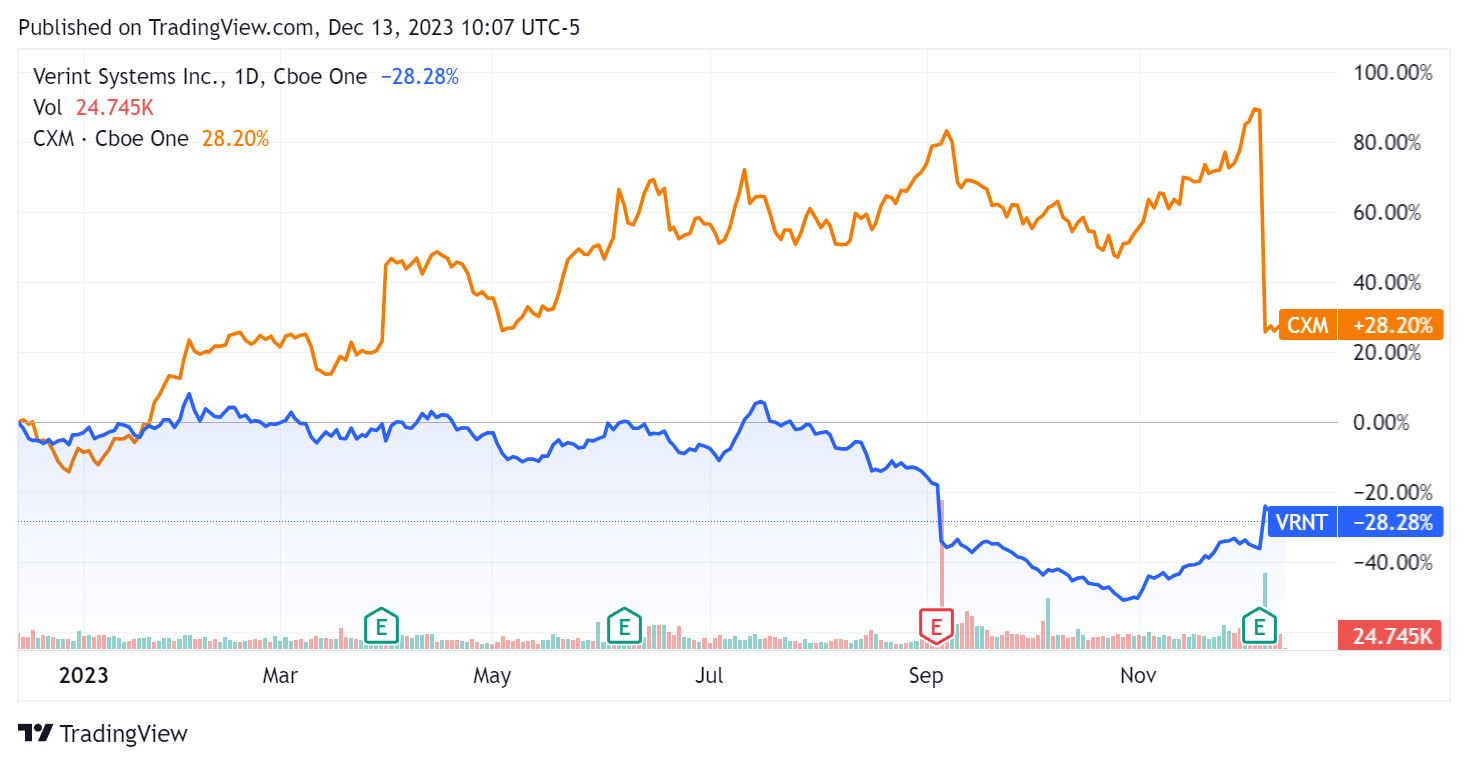

In the past 12 months, VRNT’s stock price has fallen 28.28% vs. that of Sprinklr, Inc.'s (CXM) gain of 28.2%:

{kind=link}

For balance sheet results, the firm ended the quarter with $210.3 million in cash, equivalents and short-term investments and $410.5 million in total debt, none of which was categorized as short-term.

Over the trailing twelve months, free cash flow was $130.0 million, during which capital expenditures were $22.9 million. The company paid $62.6 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Verint

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| 2.7 |

| Enterprise Value / EBITDA |

| 17.5 |

| Price / Sales |

| 2.0 |

| Revenue Growth Rate |

| -2.1% |

| Net Income Margin |

| 2.6% |

| EBITDA % |

| 15.6% |

| Market Capitalization |

| $1,720,000,000 |

| Enterprise Value |

| $2,400,000,000 |

| Operating Cash Flow |

| $152,880,000 |

| Earnings Per Share (Fully Diluted) |

| $0.04 |

| Forward EPS Estimate |

| $2.65 |

| Free Cash Flow Per Share |

| $1.55 |

| SA Quant Score |

| Hold - 2.86 |

(Source - Seeking Alpha.)

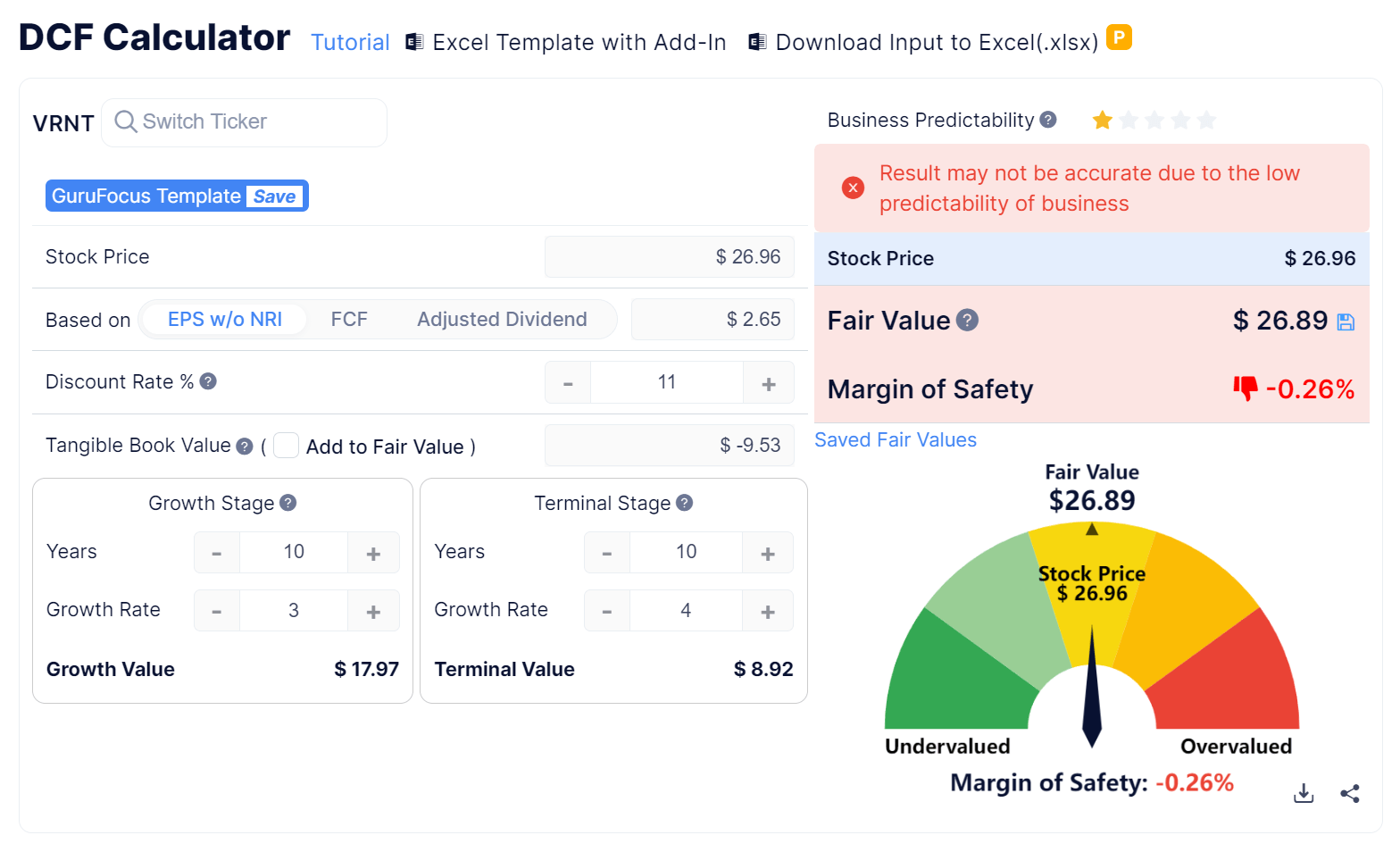

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

{kind=link}

Based on the DCF, using a discount rate of 11% (10-year Treasury (US10Y) at 5% plus 6% equity risk premium) and forward earnings per share assumption of $2.65, the firm’s shares would be valued at approximately $26.89 versus the current price of $26.96, indicating they are potentially currently fully valued.

As a reference, a relevant partial public comparable would be Sprinklr:

| Metric (Trailing Twelve Months) |

| Sprinklr |

| Verint |

| Variance |

| Enterprise Value / Sales |

| 3.4 |

| 2.7 |

| -20.9% |

| Enterprise Value / EBITDA |

| 121.8 |

| 17.5 |

| -85.7% |

| Revenue Growth Rate |

| 19.5% |

| -2.1% |

| -110.6% |

| Net Income Margin |

| 4.2% |

| 2.6% |

| -38.5% |

| Operating Cash Flow |

| $76,240,000 |

| $152,880,000 |

| 100.5% |

(Source - Seeking Alpha.)

VRNT’s most recent unadjusted Rule of 40 calculation dropped to 11.8% as of FQ3 2024’s results, so the firm needs improvement in this regard, per the table below:

| Rule of 40 Performance (Unadjusted) |

| FQ4 2023 |

| FQ3 2024 |

| Revenue Growth % |

| 3.2% |

| -2.1% |

| Operating Margin |

| 13.3% |

| 13.9% |

| Total |

| 16.5% |

| 11.8% |

(Source - Seeking Alpha.)

Commentary On Verint

In its last earnings call (Source - Seeking Alpha ), covering FQ3 2024’s results, management’s prepared remarks highlighted revenue and non-GAAP EPS exceeding previous expectations.

Leadership noted positive trends, with more than 50% of SaaS bookings related to its AI-enabled chatbots, a material increase from the previous year.

The firm added over 30 orders in excess of $1 million total contract value, and its 12-month SaaS pipeline grew by over 20% YoY, reflecting what it is seeing as strong demand for AI and related customer experience automation.

Analysts questioned the leadership about sales cycles, the ongoing transition to SaaS, and its gross margin and revenue guidance.

Management replied that sales cycles remain elongated, but they see growth next year due to customers focusing on reducing labor costs through automation, which AI helps.

Notably, the firm continues to see strength in unbundled SaaS demand, as many customers don’t want to "rip and replace" everything.

On gross margins, management sees a path to growing margins next year from growth in its SaaS offerings as customers focus on unbundled approaches.

For the quarter’s results, total revenue fell by 3.0% year-over-year, while gross profit margin increased by 0.5%.

Selling and G&A expenses as a percentage of revenue dropped 1.3% YoY, indicating increased efficiencies, and operating income increased by an impressive 25.6%.

The company's financial position is relatively strong, with significant liquidity, and some debt but strong free cash flow.

VRNT’s Rule of 40 performance has been worsening and in need of substantial improvement, dragged down by revenue decline.

Management didn’t disclose any customer or revenue retention rate metrics for its SaaS segment.

Looking ahead, FY 2024 full-year revenue growth is expected to be only 0.7% over fiscal 2023.

If achieved, this would represent a decline in revenue growth rate versus FY 2023’s growth rate of 3.17% over FY 2022.

As for valuation, my discounted cash flow calculation suggests the stock may be fully valued at its current level.

Compared to Sprinklr, Verint is being valued at lower valuation metrics, likely due to its current negative revenue growth trajectory and lower net income margin.

A potential upside catalyst to the stock could include increasing demand for its AI chatbots and other customer experience capabilities.

While the "AI story" is encouraging, management needs to prove it can reignite revenue growth to a meaningful degree.

Until then, I remain Neutral [Hold] on Verint Systems Inc. shares.

For further details see:

Verint Sees AI-Chatbot Demand, But Needs To Produce Meaningful Growth