VNQ - Veris Residential: Sell For Short Run Hold For Long

2023-03-10 04:03:42 ET

Summary

- Veris Residential shares are up more than 50% over the past 5 months, mostly due to takeover speculation.

- Over the past 10 years, the company's shares have lost over 40%of their value.

- Veris is shedding its office and hotel properties and morphing into a pure apartment REIT.

- This article examines the growth, balance sheet, dividend, and valuation metrics for this intriguing small-cap REIT.

Veris Residential (VRE) shares are up more than 50% over the past 5 months, mostly due to two factors:

- A transformation in the company's business model

- Speculation about a takeover bid

A little historical data will put this run-up in perspective. According to MarketWatch.com, the company's high for the past 20 years came on January 29, 2007, at $56.52. From that point, it gradually lost altitude for the next 15 years, reaching its nadir October 7, 2022, at $10.22. Investors in VRE over that period reaped an appalling annual return of (-10.3)%.

By contrast, the average REIT, as represented by the Vanguard Real Estate ETF ( VNQ ), went from $82.80 to $79.04, for an essentially flat 15-year CAGR of (-0.3)%. Simply put, for the past 15 years, until last October, VRE was a serious loser.

The market as a whole has rebounded since early October. Yet while the VNQ is up about 12% from its October 7 low of $76.92 to its March 8 close, VRE has leapt over 50% in that same period.

Company Q4 Supplemental

So can the remarkable recent spike in VRE shares be justified by the company's transformation alone?

Meet the company

Veris Residential

Founded in 1994 and headquartered in Jersey City, New Jersey, Veris Residential owns a 6,931-unit portfolio of Class A multifamily residential properties, all in Massachusetts and New Jersey, currently enjoying 95.3% occupancy and an eye-popping average monthly rent of $3482.

By NOI (net operating income), nearly half of this portfolio (47%) is from New Jersey Waterfront property (10 locations). About 12% of NOI comes from 4 properties in Massachusetts, and 16% from the newly-acquired Haus25 high rise apartment complex in Jersey City.

Company Q4 Supplemental

VRE unfortunately also owned 5 office buildings as of December 31, comprising some 3.0 msf (million square feet) of office space, enjoying only 67.9% occupancy. They are actively selling these off. VRE also owned 6 retail and parking garage properties in New Jersey, totaling 0.7 msf and enjoying only 73.5% occupancy.

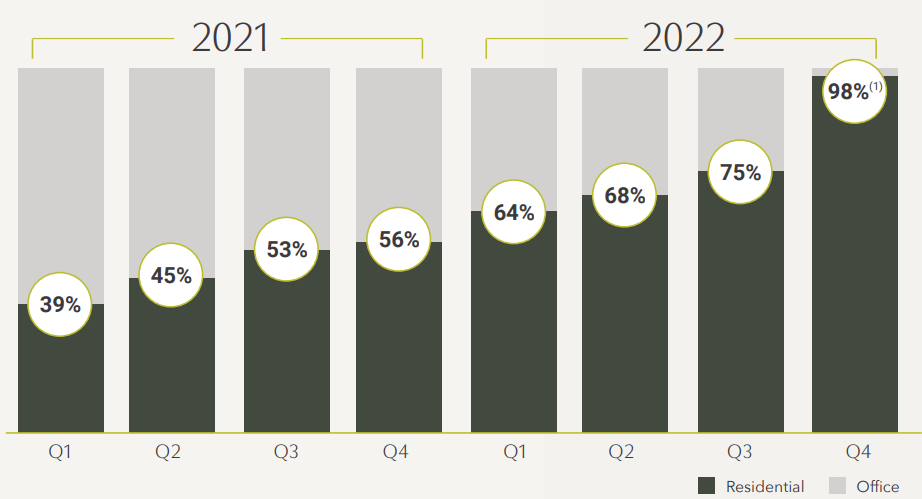

Until recently, Veris also owned hotels. However, they sold the last of those on February 10 of this year. Thus, Veris is morphing into a pure apartment REIT.

According to CEO Mahbod Nia on the Q4 2022 earnings call:

I would like to take a moment to acknowledge the tremendous progress our team made during 2022 on our path to becoming a pure-play multi-family company . . . we successfully executed on $1.4 billion of non-strategic asset sales, $925 million of which has closed since the beginning of 2022, significantly reducing our office exposure and fully exiting the hotel segment.

The company's holdings as of December 31 were 98% concentrated in multifamily residential properties.

{kind=link}

Judged from the standpoint of revenue alone, the transformation seems to be working. VRE's multifamily portfolio is out-earning its much-larger peers in the thriving Apartment REIT sector on a same-store basis, over the past 5 quarters.

Company investor presentation

Importantly, the average age of VRE's apartment buildings is less than 10 years, which is far younger than the average Apartment REIT portfolio. That means considerably lower capex.

Company investor presentation

Unfortunately, 18.7% of the company's ABR (annual base rent) and 28.0% of their total square footage is tied up in leases that expire in 2023. They will have to have a good year in leasing, to make this transition work.

The company is making good use of 21st century technology. Their app allows residents to pay rent and manage maintenance requests. VRE offers self-service leasing and virtual tours on its website, and their revenue optimization platform allows precise pricing.

Quarterly results

Q4 same-store NOI was up 12.6% YoY (year over year), despite hefty increases in taxes, insurance, and utility costs, and up 20.1% for the full year. VRE was not profitable in 2022, losing $22.4 million in net income. However, this was a major improvement from the $119.0 million operating loss the company took in 2021. Because of the aggressive disposition of hotel and office properties, core FFO shrank from $68.1 million to $44.3 over the course of 2022, and adjusted EBITDA fell from $157.4 million to $145.5 million, while Debt/EBITDA rose from an already-appalling 12.8 to 13.3.

Growth metrics

VRE's 3-year growth figures for FFO (funds from operations), TCFO (total cash from operations), and market cap are truly awful. The company has been shrinking rapidly, until this past year.

| Metric |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 3-year CAGR |

| FFO (millions) |

| $116.1 |

| $68.1 |

| (-$22.8) |

| $89.6 |

| -- |

| FFO Growth % |

| -- |

| (-41.3) |

| NA |

| NA |

| (-8.3)% |

| FFO per share |

| $1.62 |

| $1.07 |

| $0.68 |

| $0.44 |

| -- |

| FFO per share growth % |

| -- |

| (-34.0) |

| (-36.5) |

| (-35.3) |

| (-35.2)% |

| TCFO (millions) |

| $132 |

| $85 |

| $56 |

| $66 |

| -- |

| TCFO Growth % |

| -- |

| (-35.6) |

| (-34.1) |

| 17.9 |

| (-20.6)% |

| Market Cap (billions) |

| $1.77 |

| $1.13 |

| $1.67 |

| $1.58 |

| -- |

| Market Cap Growth % |

| -- |

| (-36.2) |

| 47.8 |

| (-5.4) |

| (-3.7)% |

Source: TD Ameritrade, CompaniesMarketCap.com, and author calculations

VRE was hammered by the pandemic, of course, and although its share price recovered nicely in red-hot 2021, its revenues and cash flow did not, continuing to shrink by high double digits. FFO went from negative to positive in 2022, but FFO per share continued to slide, reflecting a large issuance of new shares, which kept market cap nearly even with 2021.

Meanwhile, here is how the stock price has done over the past 3 twelve-month periods, compared to the REIT average as represented by the Vanguard Real Estate ETF ( VNQ ).

| Metric |

| 2020 |

| 2021 |

| 2022 |

| 2023 |

| 3-yr CAGR |

| VRE share price March 8 |

| $20.47 |

| $15.92 |

| $17.20 |

| $16.05 |

| -- |

| VRE share price Gain % |

| -- |

| (-22.2) |

| 8.0 |

| (-6.7) |

| (-7.8)% |

| VNQ share price March 8 |

| $90.67 |

| $87.61 |

| $102.66 |

| $85.54 |

| -- |

| VNQ share price Gain % |

| -- |

| (-3.4) |

| 17.2 |

| (-16.7) |

| (-1.9)% |

Source: MarketWatch.com and author calculations

Until the recent speculative run-up in VRE shares, the company had underperformed the VNQ in each of the two preceding 12-month periods, and even with the recent spike, its 3-year CAGR of (-7.8)% is considerably worse than the VNQ's disappointing (-1.9)%.

Balance sheet metrics

VRE's balance sheet does not present a pretty picture.

| Company |

| Liquidity Ratio |

| Debt Ratio |

| Debt/EBITDA |

| Bond Rating |

| VRE |

| 1.46 |

| 48% |

| 25.0 |

| NR |

Source: Hoya Capital Income Builder, TD Ameritrade, and author calculations

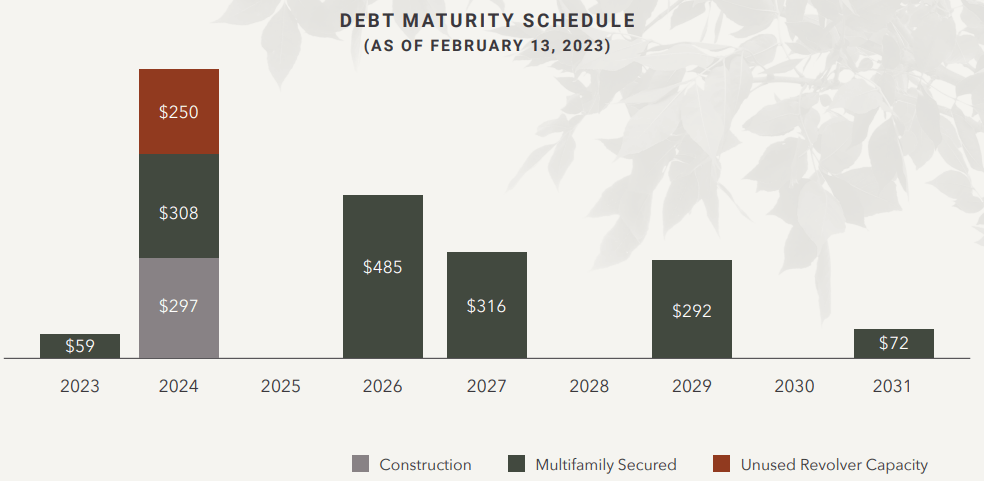

Veris owes a little over $2 billion in debt, at fairly high interest rates, and it is coming due pretty soon. According to the company's Q4 2022 supplemental the weighted average interest rate on its fixed rate debt is 4.27%, and the weighted average maturity of that segment is 3.7 years. Meanwhile, 7.7% of the total debt is held at variable rates, currently costing 6.86%, but exposed to further increases, with an average term to maturity of just 1.8 years. Overall, the weighted average interest rate is 4.47%, and the weighted average term to maturity is 3.6 years.

{kind=link}

VRE may need to refinance to meet its 2024 obligations, and this is not an especially good time to do it.

VRE also owes $588 million on 7 unconsolidated multifamily joint ventures.

Dividend metrics

Veris has not paid a dividend since July of 2020.

| Company |

| Div. Yield |

| 3-yr Div. Growth |

| Div. Score |

| Payout |

| Div. Safety |

| VRE |

| 0.00% |

| (-33.0)% |

| 0.00 |

| 0.00 |

| NA |

Source: Hoya Capital Income Builder, TD Ameritrade, Seeking Alpha Premium

Dividend Score projects the Yield three years from now, on shares bought today, assuming the Dividend Growth rate remains unchanged.

Valuation metrics

For a company that is paying no dividend, VRE shares are priced high. This is not an uncommon situation for a high-growth company, but I'm not sure VRE completely deserves that designation yet. Much of this valuation disconnect is not due to enthusiasm about the company's new business model. It is at least partly due to takeover speculation.

| Company |

| Div. Score |

| Price/FFO '23 |

| Premium to NAV |

| VRE |

| 0.00 |

| 31.7 |

| 0.5 |

Source: Hoya Capital Income Builder, TD Ameritrade, and author calculations

What could go wrong?

Investing in VRE right now is unusually risky. There are two things that could obviously go wrong.

1) The transition could fail. Despite the company's aggressive off-loading of office and hotel properties, and the sparkling performance of its small young apartment portfolio, its heavy debt load and near-term maturities could keep it struggling for several more years, while hamstringing its acquisition opportunities.

2) Much of the runup in prices since October is nothing more than speculation on a takeover by one of VRE's chief investors. The suitor could withdraw. In fact, I think that is likely, given the frosty communication disconnect between Veris and the suitor, Kushner Cos. And although other suitors might materialize, there have been none as yet, to my knowledge.

Kushner made its initial offer October 20 , to buy VRE for $16 per share, which at the time was a 29% premium over the market price. VRE shares spiked more than 20% higher the next day.

On November 3, the board of Veris unanimously rejected Kushner's offer, saying that it "grossly undervalues the Company," particularly in light of VRE's strategic transformation. The board further stated that "Kushner Companies was unable to substantiate its equity or debt financing sources."

In response, Kushner then accused VRE's board of being "uninformed at best and disingenuous at worst," claiming that their bid was "fully capitalized and committed," and further impugning VRE management's integrity. (I guess this is why they call it a hostile takeover.)

Kushner subsequently raised the offer price, but was again summarily rejected. This prompted another bitter response from Kushner, lamenting the Veris board's "failure, throughout our prior discussions, to provide even cursory guidance as to whether or at what price it might be willing" to sell.

On February 27, Veris announced that Ronald Dickerman of Madison International Realty would be appointed to the board of directors later this month, a move that Kushner applauded . But Kushner simultaneously criticized VRE management again, saying shareholders had suffered for 3 years due to VRE . . .

managing a New Jersey residential REIT with a Board of mainly non-real estate professionals led by an activist hedge fund and a highly paid CEO operating from London

Tellingly, Kushner's letter added:

Veris is only trading where it is today because of Kushner's ongoing interest in providing shareholders value for their shares.

From where I sit, it looks as though Kushner has little chance of acquiring VRE. Given the two companies' completely different versions of the facts, I don't think Veris would sell to Kushner if Kushner was the last company on earth (unless shareholders demand it).

Investor's bottom line

Veris is making an impressive turnaround, but has a long way to go. Its current price partly reflects this turnaround, and partly reflects speculation over a hostile takeover offer. Hoya Capital estimates the merited Buy price on VRE at about $12 per share.

Where there is smoke there is fire, so if Kushner thinks the company is worth $18 per share, and Veris thinks it is worth much more than that, this may bode well for the company in the longer term. The little apartment portfolio they are stripping down to is impressive, and so are the near-term FFO growth prospects.

As to whether buying, selling, or holding is the best strategy, that depends. If you have a stake in VRE, and you are in it for the long run, by all means continue to hold your shares. When the takeover speculation dies down, so will the share price, and that would be a better time to increase your stake, if you are so inclined.

However, if you are in it for short-term speculative gain from a takeover, this would be a great time to take profits. The deal with Kushner probably will never happen, so unless another suitor materializes, you have gotten about all you are going to get.

Either way, in the short run, selling now seems like a good idea, because the price probably will be considerably lower pretty soon.

Seeking Alpha Premium

TipRanks rates VRE as Outperform (8 out of 10). Meanwhile 5 of the 6 Wall Street analysts think you should Hold, and Zacks and The Street do too.

Just remember, the opinion that matters most is yours.

For further details see:

Veris Residential: Sell For Short Run, Hold For Long