VRE - Veris's Future Profitability Is Unclear During Transition To Multifamily REIT

2023-12-29 09:00:22 ET

Summary

- Veris is a luxury residential REIT focusing on Class A properties in high density urban areas.

- Overvalued relative to peers on a P/AFFO basis.

- $12 price target based on application of peer P/AFFO multiple to Veris's current AFFO per share.

Investors should sell shares of Veris Residential ( VRE ). The firm's year-to-date performance has been relatively flat. However, Veris has garnered short interest from investors looking to profit on additional declines in the firm's share price. Short interest currently stands at 4% of Veris's share float.

Background

Veris is a residential REIT based in Greater Boston and Greater New York City. The company owns numerous luxury properties, all Class A multifamily, and offers rental options of studio to four-bedroom apartments. Moreover, living in a Veris property is not cheap. Prices range from ~$1,600 for the company's most affordable studio apartment in Worcester, Massachusetts to ~$9,000 for a three-bedroom apartment in one of its Jersey City, New Jersey properties.

The company traces its origins to the late 1940s, when John Cali formed Cali Associates as a development company in Northern New Jersey. A subsequent growth period of almost 40 years saw Cali Associates become a formidable facet of the Greater New York City real estate industry. In 1997, Cali Associates merged with Patriot American Office Group and the Mack Company to form Mack-Cali Realty Corporation as a real estate investment trust. This arrangement was initially beneficial as the firm's shares traded up to ~$55 by early 2007. Mack-Cali was then squeezed by the 2008 Global Financial Crisis and has yet to return to its January 2007 high. A steady thirteen-year decline in share price contributed to the firm rebranding as Veris Residential in December 2021 as part of its new strategy. Declining share price and an ~-34% five-year dividend growth rate have hampered the company's efforts to attract new investors, and continued strategic improvements will be needed to stabilize operations.

Outlook

Veris has been beaten down by the market, but the firm's leadership team has still been working hard on creating value for shareholders. Here are some key considerations for prospective investors prior to investing in Veris:

1. Reorganization as a Pure-Play Multifamily REIT

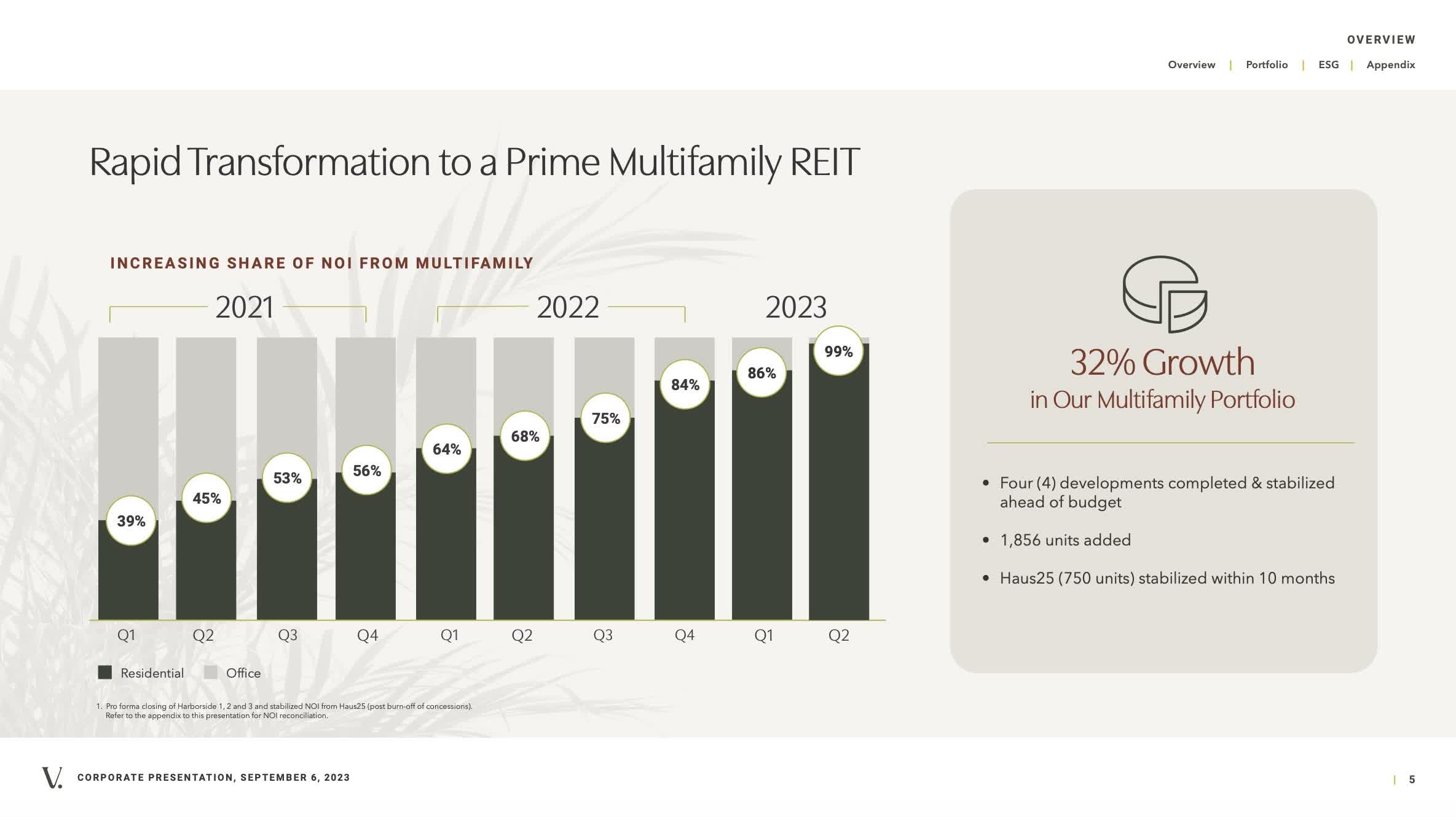

Veris's current strategy is to shift its property portfolio to 100% residential multifamily properties. In 2021 , the firm reported 39% of its net operating income ((NOI)) from multifamily units. However, Veris's most recent filings indicate that 99% of NOI is tied to multifamily rent. This transitional strategy appears to have the goal of streamlining the company's operations so that Veris can develop a competitive advantage in residential multifamily. Focusing on both office and residential properties might have been spreading the company's resources too thin and hampering the firm's ability to fully utilize assets. Veris has quantified this strategy via ~$2 billion of proceeds from sales of office and hotel properties since Q1 2021 plus the plowback of these funds to add ~2,000 residential units over the same period. Moreover, the firm has ~$300 million of land either being developed or held for future development to further bolster the number of residential properties in Veris's portfolio.

Veris Residential Q3 2023 Investor Presentation

{kind=link}

2. Debt Maturity Schedule

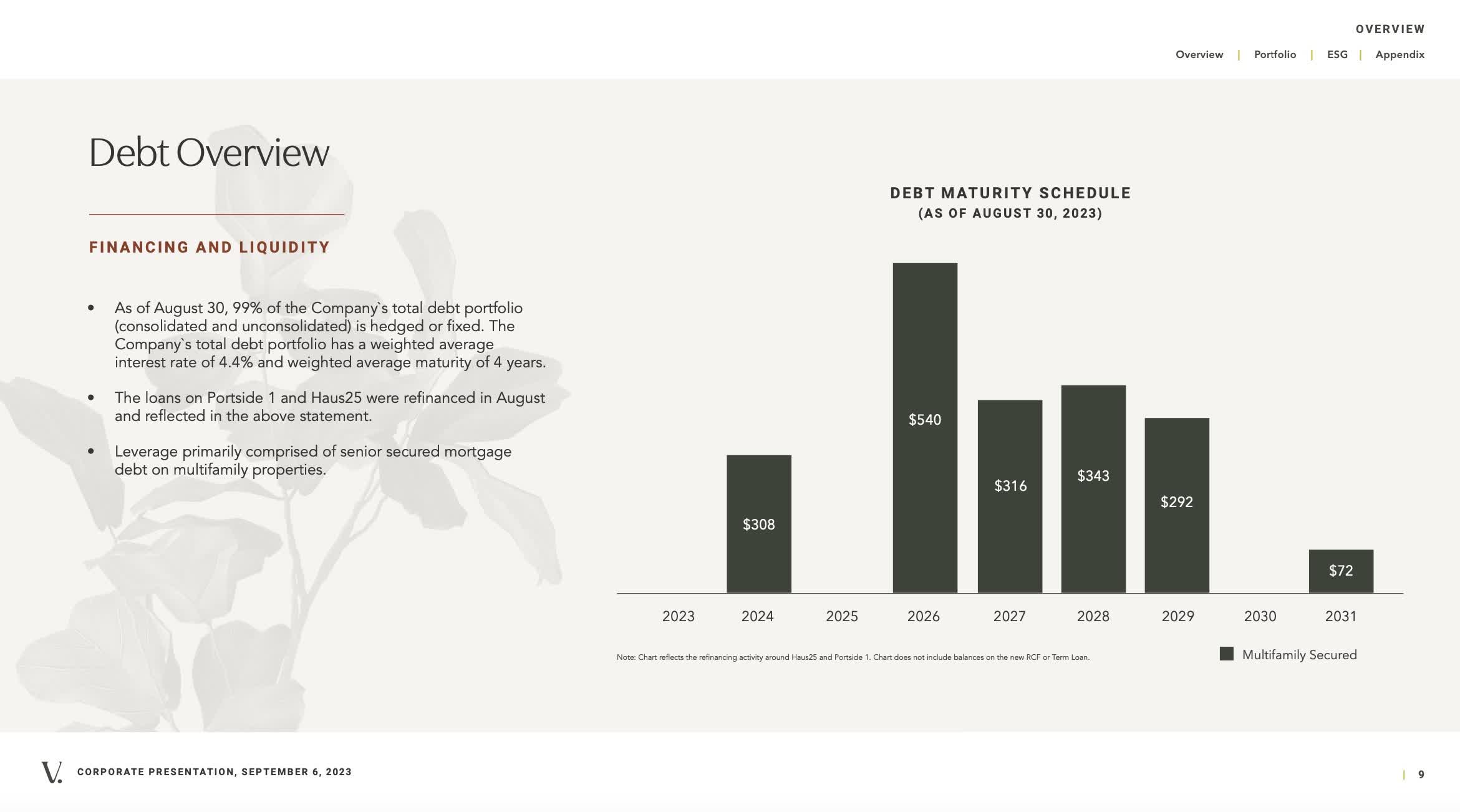

Per industry standards, Veris finances many of its properties with debt. The firm has decreased its mortgage borrowing slightly over the past year due to tightened credit availability. Most of Veris's outstanding loans are senior unsecured debts with a weighted average interest rate of 4.4% and a weighted average maturity of 4 years. The firm also utilizes a revolving credit facility and term loans to meet immediate obligations. Despite restrictive covenants stemming from these agreements, the firm is in good standing with its creditors.

Veris Residential Q3 2023 Investor Presentation

{kind=link}

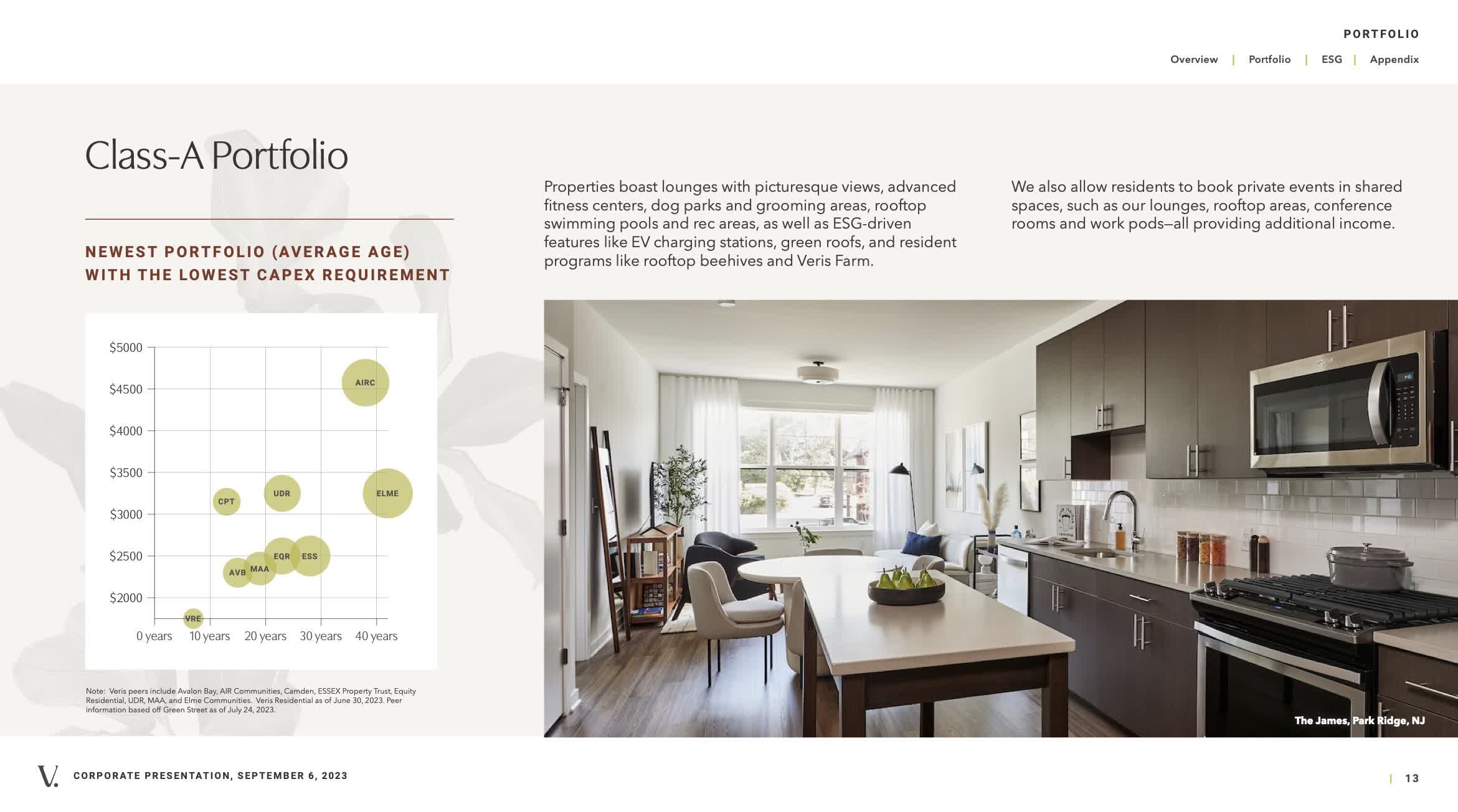

3. Class-A Properties

Veris boasts a property portfolio of Class-A real estate with perceived lower capital intensity than competitors. According to Veris, these buildings feature:

...lounges with picturesque views, advanced fitness centers, dog parks, and grooming areas, rooftop swimming pools and rec areas, as well as ESG-driven features like EV charging stations, green roofs, and resident programs like rooftop beehives and Veris Farm.

Since Veris invests in Class-A properties, the firm derives much of its rental revenue from high-income individuals. Should the buying behaviors of this group change, Veris will be detrimentally affected. Moreover, as long as commerce in Veris's operating geographies continues to support high-paying jobs and rising property values, then Veris should be able to support high rents in addition to future rent increases.

Veris Residential Q3 2023 Investor Presentation

{kind=link}

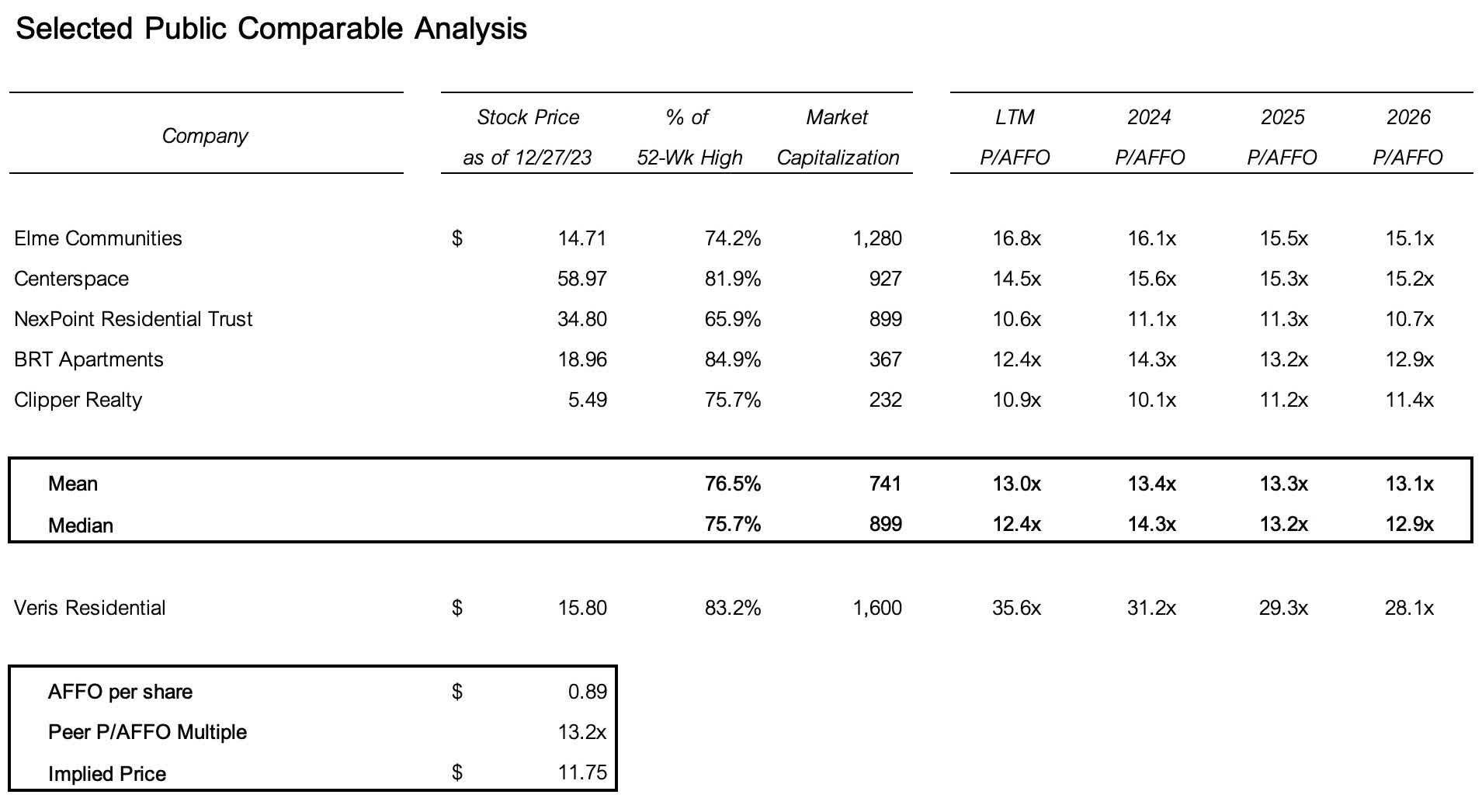

Valuation

Veris was valued using a price to adjusted funds from operations multiple. To accomplish this, a peer group of firms comparable to Veris was created. The following firms were selected based on their similar business model and market capitalizations: Elme Communities ( ELME ), Centerspace ( CSR ), NexPoint Residential Trust ( NXRT ), BRT Apartments ( BRT ), and Clipper Realty ( CLPR ). The P/AFFO multiples from these firms were then aggregated on a forward basis to value Veris at $11.75 per share. Veris's higher P/AFFO multiple relative to its competitors implies that the firm is overvalued.

Incorporating risk adjustments into the valuation is important. I am arguing that Veris is simply not worth holding relative to peers because of the relatively higher valuation that it commands. This could change in a case where Veris shows increased profitability that would support higher valuations.

{kind=link}

Conclusion

Despite Veris Residential's quality customer base, the firm's financial situation is confusing. The firm's restructuring as a pure-play multifamily REIT is not yet complete, and the remnants of Veris's office portfolio are still dragging on the firm's operating performance. Relative comparisons to pure-play multifamily peers indicate that the firm's share price needs to fall before buying should continue.

For further details see:

Veris's Future Profitability Is Unclear During Transition To Multifamily REIT