VRSK - Verisk Analytics: Industry-Leading Data Analytics For Insurance And Claims Stock Overvalued

2023-09-17 22:07:41 ET

Summary

- Verisk Analytics has divested its troubled Financial Services Business, focusing on its core insurance markets.

- The company has also sold its Wood Mackenzie business, which faced challenges in the energy sector.

- Verisk's dedicated focus on the insurance industry and strong financial performance make it a high-quality growth company, but the stock is currently overvalued.

Verisk Analytics ( VRSK ) is an industry-leading data analytics company serving the insurance industry. They offer predictive analytics and decision-making solutions to help insurance companies manage their costs and underwriting risks. In February 2022, Verisk divested its troubled Financial Services Business. In May 2022, they appointed Lee Shavel as their new CEO, and in October 2022, they divested their Wood Mackenzie business. Following these portfolio divestitures, Verisk has transformed into a pure data analytics company dedicated to the insurance industry, with a higher growth profile and improved margins. While their stock price may currently be overvalued, I consider Verisk a high-quality growth company, and I encourage investors to consider buying it if the stock price drops below $190.

Major Divestitures

Financial Services: This business accounted for 4.8% of the group's revenue in FY21. However, due to its transaction-based business model, revenue growth has been highly cyclical in the past. Verisk Analytics also faced challenges in adjusting their customers' contracts for pricing adjustments, resulting in sluggish growth for several years.

{kind=link}

I believe the divestiture of their Financial Services division makes total sense. It has the potential to significantly boost Verisk's business growth rate, allowing them to focus more on their core insurance markets.

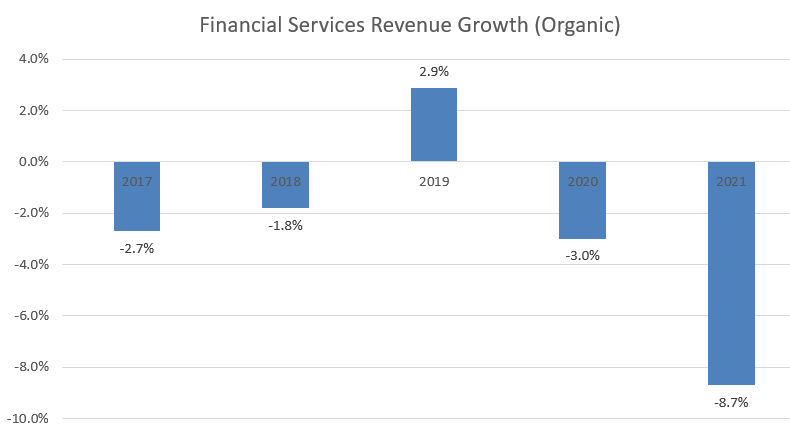

Regarding Wood Mackenzie, Verisk acquired Wood Mackenzie in 2015 for approximately $2.8 billion, and it is a leading data analytics company for the energy, chemicals, metals, and mining industries. Driven by end-market growth since the last financial crisis in 2009, their business experienced robust growth. However, starting from FY17, Wood Mackenzie's business encountered challenges, with an organic growth rate of -2.7% in FY17, -1.8% in FY18, 2.9% in FY19, -3% in FY20, and then -8.7% in FY21. As energy companies began transitioning to renewables, Wood Mackenzie's value proposition weakened, especially since they excelled in the traditional energy sector but not in renewables. Overall, I believe this divestiture also makes sense. They sold Wood Mackenzie for $3.1 billion in October 2022.

Dedicated in the Insurance Data Analytics Market

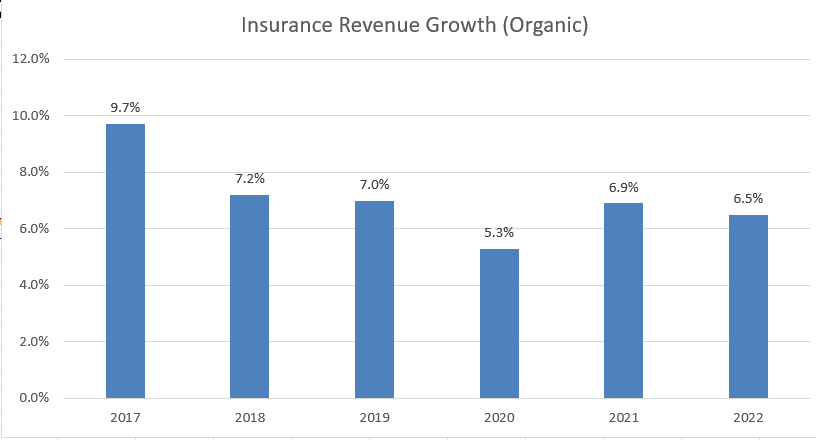

After these divestitures, Verisk has become a dedicated player in the insurance underwriting and claims end markets. Verisk's products enable insurance companies to effectively manage their costs and mitigate underwriting risks. Over the past few years, Verisk's insurance business has experienced solid growth.

{kind=link}

Their customers include most of the P&C insurance companies in the U.S. I believe P&C insurance companies are making substantial investments in AI and process automation, aiming to reduce operating costs and enhance risk management. These AI and automation projects rely on data analytics tools and data sources provided by Verisk. According to McKinsey , the insurance industry stands on the precipice of a significant, technology-driven transformation, and it is crucial for companies to develop a well-structured and actionable strategy that incorporates both internal and external data.

Furthermore, as McKinsey indicated, the way insurance companies identify, quantify, and manage risk heavily depends on the volume and quality of the data available to them. Therefore, I anticipate that Verisk's data analytics business may experience accelerated growth over the next decade.

Recent Financials and Outlook

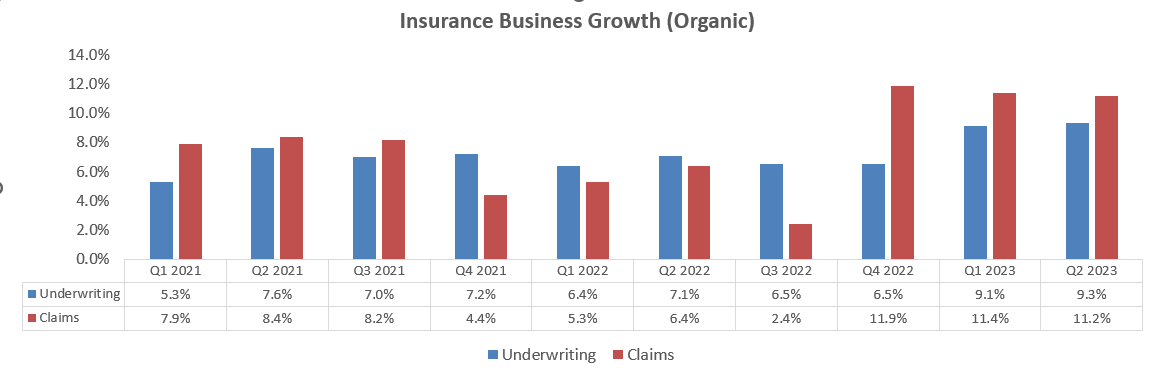

Both the Underwriting and Claims business segments have demonstrated strong growth in the past few quarters. In Q2 FY23 , the group's organic revenue expanded by 9.8%, with Underwriting achieving 9.3% growth and Claims experiencing an impressive 11.2% growth rate.

{kind=link}

They have raised their full-year guidance for FY23, anticipating revenue in the range of $2.63 billion to $2.66 billion, with an expected EPS of $5.50 to $5.70. Additionally, they continue to guide for an EBITDA margin of 53% to 54% for the full year. Regarding capital expenditure, they expect it to fall within the range of $220 million to $240 million, with a significant portion allocated to cloud-native infrastructure and system modernization projects. Considering their strong cash flow generation, I believe these capital expenditures are strategically sound. Furthermore, Verisk maintains a robust balance sheet, with gross debt leverage of only 2.1x in FY22.

Risks

Verisk's growth can indeed be influenced by the profitability and underwriting cycles of P&C insurers. As disclosed in their FY22 annual report , the total direct written premiums for P&C insurers exhibited fluctuations, with a peak of $14.8% in 2002, declining to -3.1% in 2009, and subsequently recovering to 5.1% in 2019. There was a decline of 2.3% in 2020 due to the pandemic, followed by a rebound to 9.5% in 2021. These underwriting cycles are notoriously difficult to predict, and Verisk's revenue growth may be impacted by these cycles.

On a positive note, 79% of Verisk's revenue is subscription-based, with only 21% derived from transactional sources. This substantial portion of subscription-based revenue could help the company maintain stability in its revenue growth over time, making its business more resilient during economic downturns.

Valuation

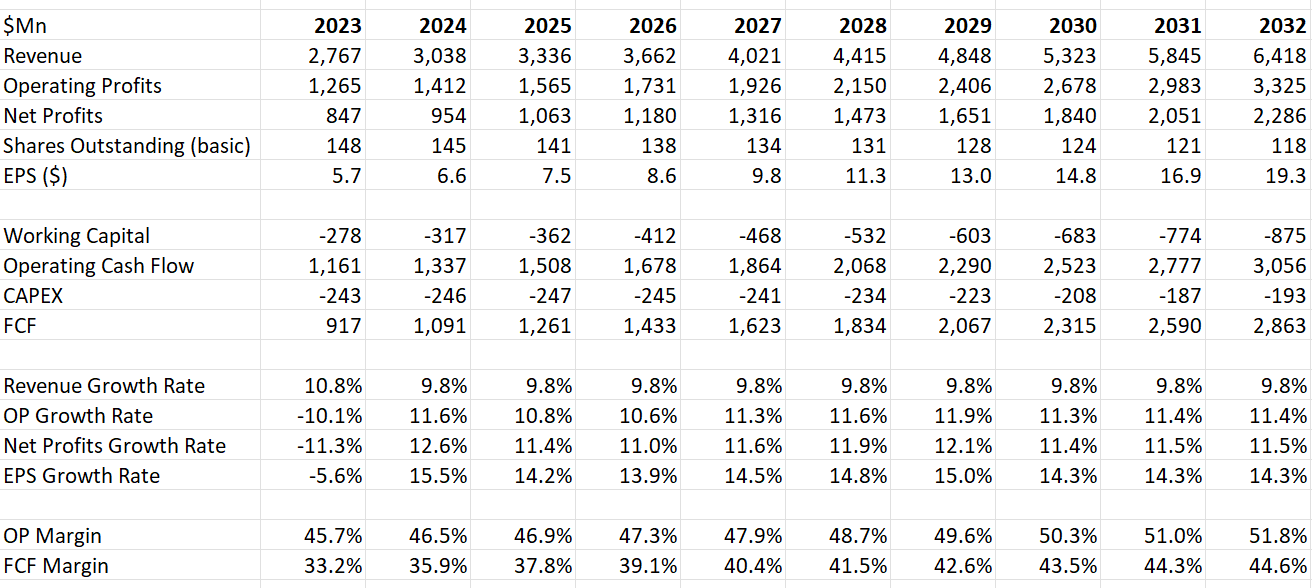

As a data analytics company, Verisk maintains a significantly high operating margin and free cash conversion ratio. In the model, I estimate that their operating margin will reach 51.8% by FY32, with the free cash margin expanding to 44.6%.

I assume a 10.8% revenue growth in FY23, followed by 8% organic revenue growth and 1.8% growth from acquisitions in the subsequent years. Verisk operates with a negative working capital business model, primarily due to the subscription-based nature of most of its services.

{kind=link}

Applying 10% discount rate, 4% terminal growth rate, and 24% tax rate, the discounted value of their free cash flow from the firm is estimated to be $30 billion in my model. After adjusting cash and debt, the fair value of their stock price is calculated to be $190 per share as per my estimates.

Wrap-Up

I believe Verisk Analytics is a highly respectable data company, and its growth and margin profile are superior. Their divestitures of Financial Services and Wood Mackenzie make their business more resilient with a better growth profile. However, their stock price is currently overvalued, and I am assigning it a 'Hold' rating.

For further details see:

Verisk Analytics: Industry-Leading Data Analytics For Insurance And Claims, Stock Overvalued