VRSK - Verisk Analytics: Maintained Full Year Guidance; Still Rich Valuation; 'Hold' Rating

2023-11-03 09:56:31 ET

Summary

- Verisk Analytics reported a 9.4% organic revenue growth and a 26.7% adjusted EPS growth in Q3, with strong year-over-year margin expansion.

- The company reaffirmed its full-year guidance, indicating an implied full-year revenue growth rate higher than their long-term expectations.

- Despite positive results, the stock price remains high, leading to a 'Hold' rating with a fair value of $190 per share.

Verisk Analytics ( VRSK ) reported its Q3 FY23 results on November 1st. They posted a 9.4% organic revenue growth and a 26.7% adjusted EPS growth, accompanied by strong year-over-year margin expansion. The company reaffirmed its full-year guidance, indicating an implied full-year revenue growth rate higher than their long-term expectations of 8-9%. Despite these positive results, the stock price remains high at the current level. Based on my estimates, I have calculated the fair value to be $190. Therefore, I maintain a 'Hold' rating on the stock.

Q3 Review and Outlook

The organic revenue growth was 9.4% in Q3 FY23, with strong claims growth of 12.1% year over year. Their EBITDA margin expanded to 54% this quarter and their EPS grew 26.7% year over year. It is a quite strong quarter, slightly higher than the market and management's previous expectations.

{kind=link}

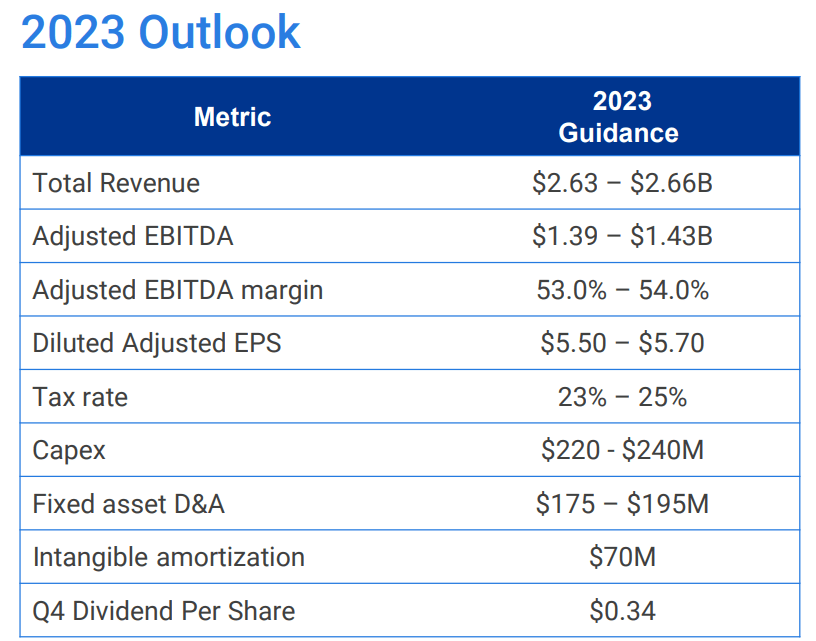

They haven't made any changes to their full-year guidance: revenue of $2.63-$2.66 billion, adjusted EBITDA between $1.39-$1.43 billion, adjusted EBITDA margin in the 53%-54% range, and adjusted EPS of $5.50-$5.70.

{kind=link}

Specifically, subscription revenue, which represents 80% of the total, grew organically by 9.3%. The management noted that the growth in subscriptions was bolstered by strong net premium growth. On the other hand, transactional service revenue grew organically by 10.2%, primarily driven by automotive solutions.

In terms of free cash flow, there was a 9% decline to $196 million this quarter due to the impact of the previous divestiture and cash taxes. However, it's worth noting that excluding the divestiture and cash tax impact, both cash flow from operations and free cash flow showed year-over-year growth.

Overall, the company delivered a solid quarterly result without significant surprises. Their organic growth was accelerated, thanks in part to the divestiture of their Energy and Financial Services divisions. For readers interested in more details about these divestitures, please refer to my initiation article .

Challenges in U.S. Property and Casualty Insurance Industry

Verisk Analytics offers solutions and data analytics to the property and casualty insurance industry, making it reliant on net premium growth and prevailing market conditions. During the Q3 earnings call , the management highlighted the deep challenges in the insurance industry caused by high inflation and increased losses. These factors are adversely affecting industry profitability, leading insurance players to exit unprofitable sectors, reduce staff, and raise insurance rates to counter rising inflation and losses. This trend drove net written premium growth up by 9.7% in the first six months of 2023.

A Best's Special Report in September 2023 revealed that the U.S. property and casualty insurance industry incurred a net underwriting loss of $24.5 billion in the first half of 2023, nearly surpassing the $26.5 billion total losses recorded for the entire 2022. The combination of high interest rates and inflation presents significant challenges to insurance companies. Rising interest rates lead to unrealized losses on fixed income investments, while high inflation results in increased costs for insurance claims.

Given the industry's challenging environment, it may be difficult for Verisk Analytics to outperform. While Verisk Analytics' services are essential to property and casualty insurance companies, with 80% of its revenues being subscription-based and highly recurring, an unstable and challenging market could pose headwinds in the future. This might explain why the company's management refrained from raising the full-year guidance, despite a strong growth quarter.

Withdrawn Underwriting in Florida and California

According to media reports , major insurers are exiting markets in Florida and California due to increased risks of hurricanes and wildfires, respectively. In Florida, insurers are facing losses due to heightened hurricane risks, while in California, wildfires pose significant challenges. Verisk Analytics' management addressed these concerns during the earnings call.

According to the management, in Florida, insurers are experiencing losses, but there is still insurance carrier availability in the state. The state-run insurer is utilizing Verisk Analytics' aerial imagery data to assess properties, indicating that Verisk Analytics remains relevant in the Florida market despite some insurers ceasing underwriting activities. In California, local regulators are evaluating underwriting challenges and actively seeking data analytics tools to assess wildfire risks. Although there are challenges in the state, Verisk Analytics' expertise in data analytics positions it as a valuable resource in addressing these issues.

In the short term, Verisk Analytics may face headwinds in these regions due to property and casualty challenges. However, I am not concerned about the long-term prospects. Verisk Analytics will remain relevant as long as there are insurance carriers in the market, whether private or state-owned. If private insurers are unwilling to operate in a region, local governments will intervene, as insurance coverage is essential for homeowners to protect their properties.

Valuation

My assumptions for FY23 align with their management's full-year guidance, and I continue to trust their ability to deliver 8% organic revenue growth, along with a 1.8% growth from tuck-in acquisitions. Their margin expansion was driven by operating leverage and new solution offerings, including AI-related solutions. They emphasized that generative AI would broaden their ecosystem and integrate other partners, adding value to their customers. After discounting all the free cash flow, my model calculates the fair value to be $190 per share, making their current stock price appear expensive.

{kind=link}

Conclusions

I continue to believe Verisk Analytics is a high-quality growth company, with strong profitability and growth potential. However, the stock price is richly valued and I maintain a "Hold" rating with a $190 per share fair value target.

For further details see:

Verisk Analytics: Maintained Full Year Guidance; Still Rich Valuation; 'Hold' Rating