VRSK - Verisk Analytics Stock: Overvalued But The Outlook Is Bright

2023-08-15 20:50:51 ET

Summary

- Verisk Analytics is a market-leading company underpinned by a strong moat.

- The company's recent shift to only focus on insurance will strengthen its data set, which in turn will help them provide customers with superior products.

- I believe the company has very little risk considering the high retention rates (+95%) and 81% of revenue comes from subscription/long-term contracts.

- My valuation indicates the stock is currently overvalued, but it is understandable considering D. E. Shaw's involvement.

Investment Thesis

Verisk Analytics ( VRSK ) is a highly attractive business underpinned by a strong moat. The firm has a sticky customer base (95% retention rate), and 81% of revenue comes from subscriptions or long-term contracts. This will enable a predictable revenue stream and cash flow. The company's high switching costs and strong pricing power have allowed it to post strong organic growth and maintain high margins. VRSK has grown at a 6.5% organic constant currency rate for the past five years and maintained a 64% gross margin.

The firm's insurance segment is of high quality due to its large data set. The company has more than 30 billion records. VRSK uses this data to create new products. Over the past few years, This segment has been able to grow in the high single digits and gradually enhance margins. VRSK's strategy to use its large data sets to understand what its customers need has been serving them well, as the top 10 customers used an average of 16.3 of the firm's products in 2022. According to the company, its markets are expected to grow in the low single digits annually.

I assign a hold because the valuation ($198.44 value per share) isn't as attractive to me as the business. The firm is currently trading at a price which I would describe as overvalued, I believe the main reason for this is D. E. Shaw's involvement. In its letter to VRSK's board on March 17, 2022, the investment firm mentioned the stock can appreciate by 70% If management implements the right changes (more on this later). On that date, the stock's trading range was between $200.70 and $193.31 a share. Now let me explain the main points of my thesis in more detail.

{kind=link}

Strong Moat

I would like to attribute VRSK's strong moat to four things: Switching costs, retention rates, pricing power, and its huge data set.

I believe VRSK's high switching costs result from its solutions and services being sold primarily through annual subscriptions or long-term agreements. Offering multiple services as a bundle to customers makes it hard for them to find similar services for the same price elsewhere, especially from an industry leader such as VRSK.

{kind=link}

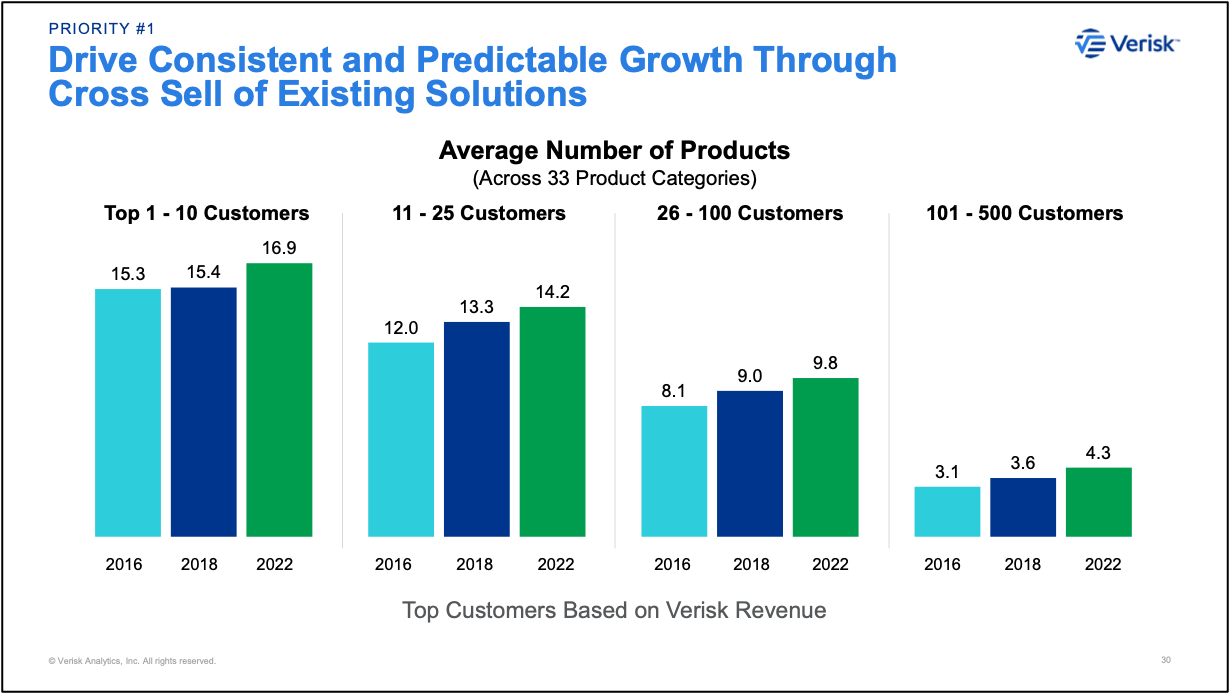

As you can see from the graph above, I think it is safe to assume that VRSK has done a good job of hooking in their customers and making them dependent on them. The top 100 customers used an average of ~13 products in 2022. This figure has been gradually growing over the years. The more products customers adopt, the stronger the company's pricing power gets and the higher the switching cost.

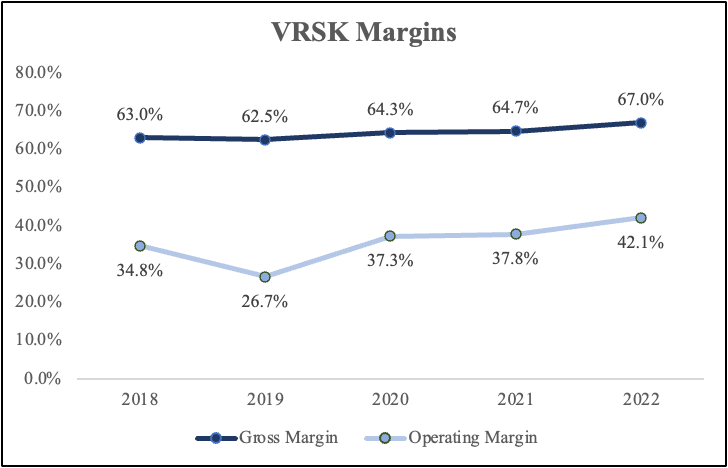

As a result of the company's strong moat, specifically its pricing power, they have been able to maintain very high margins over the years. As of the latest report, the firm's Gross margin was 67.53%, and the sector median was 30.14%. The company has said that it is focused on margin enhancement.

{kind=link}

I believe VRSK's strongest asset is its database, The company has been involved in the insurance industry for more than 50 years; during this time VRSK has amassed a huge data set (+30 billion records) from its customers. Which helps them develop predictive analytics and transformative models to understand what customers need and provide them with it. The high retention rates indicate that this strategy is working.

Growth

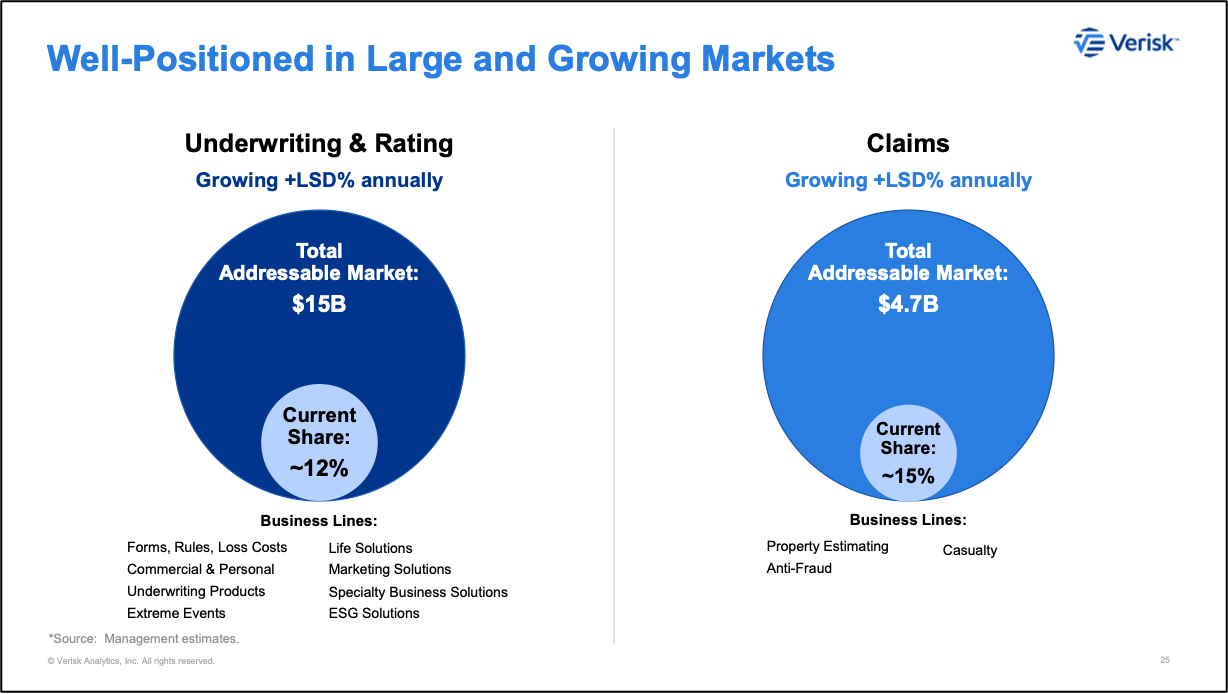

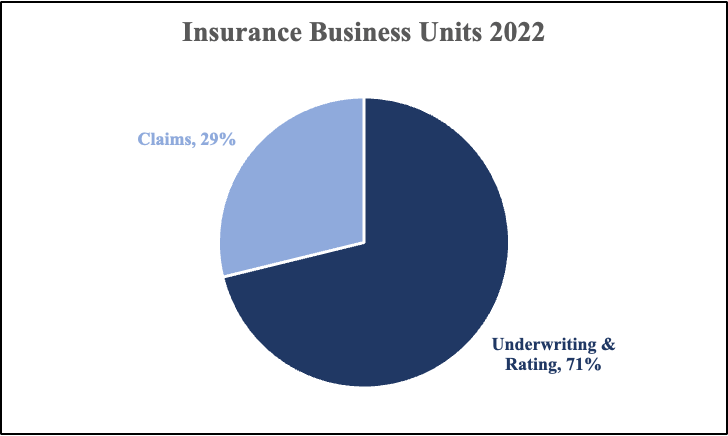

The firm has previously shifted its focus 100% toward the insurance business (more on this later). VRSK's insurance segment is made up of two business units: Underwriting & Rating and Claims. The total addressable market for underwriting & rating is $15 billion (VRSK has a ~12% market share) and for claims is $4.7 billion (~15% market share).

{kind=link}

Both of these markets are growing in the low single digits annually. I expect the company's growth in these markets to accelerate as they devote all of their resources to insurance, leverage their customer base to attract new ones, and introduce new products.

{kind=link}

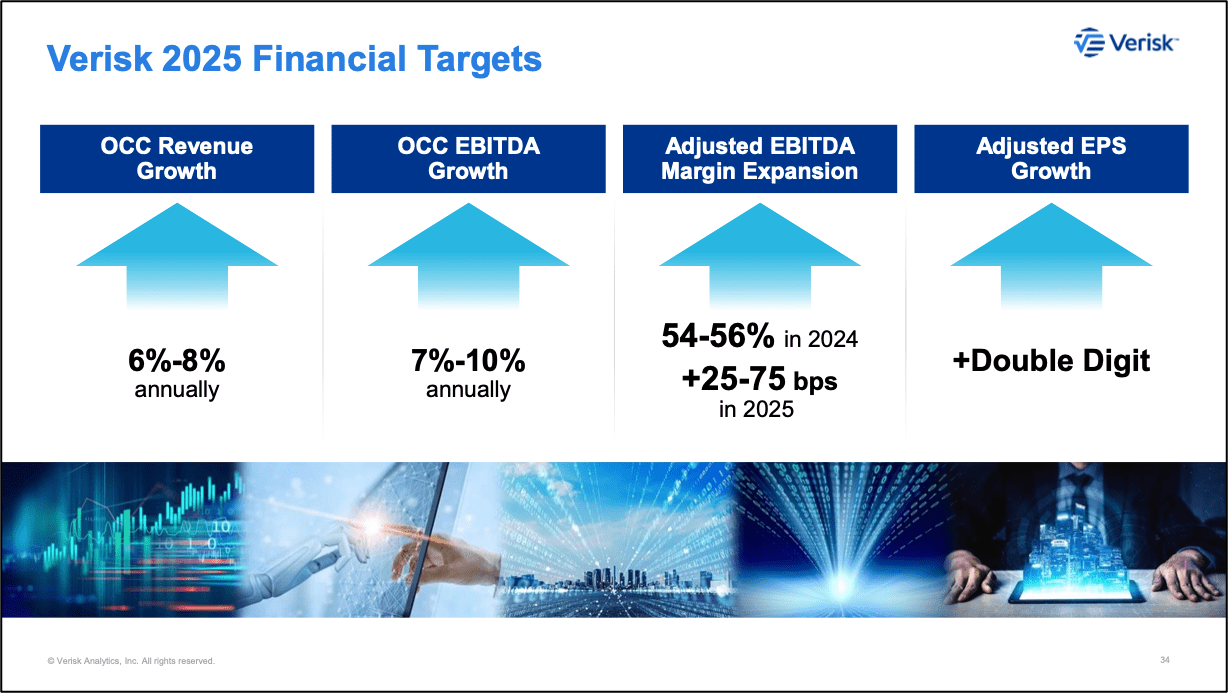

Above are the company's financial targets for 2025. Revenue is expected to grow between 6 and 8% annually occ, with EBITDA growing by 7–10% annually OCC and adjusted EPS by double digits. The firm expects to reach an ADJ EBITDA margin of 54-56% in 2024. All in all, I think the company is well positioned in terms of growth; it can cross-sell to its customers and use its large data set to create new products. International expansion is also an opportunity since 85% of revenue comes from the U.S. VRSK recently acquired SV Krug, a Germany-based motor claims solutions provider. This acquisition will expand Verisk’s claims offerings across Europe.

Business Overview

Verisk Analytics provides predictive analytics and decision support solutions to insurance companies, but most of its customers are in property and casualty insurance (P&C). Around 69% of revenue was derived from solutions provided to U.S. P&C primary issuers. The firm is now fully focused on Insurance as it sold its Financial Services unit to TransUnion for $515 million. The transaction was completed in Q1 2022. The firm also sold its Energy and Specialized Markets business segment (Wood Mackenzie) to private equity firm Veritas Capital for $3.1 billion in February 2023.

So what kind of solutions does VRSK offer to customers in insurance? VRSK uses billions of records of data to analyze and help clients assess how risky prospective customers are and what price to ensure them at. The segment also develops and utilizes machine learning and artificially intelligent models to forecast scenarios and produce both standard and customized analytics that help customers better manage their businesses. Insurance has two business units: Underwriting & rating, and claims.

{kind=link}

D. E. Shaw's Involvement

A couple of changes have recently taken place in the company. The letter sent by D. E. Shaw is six pages long, but I think what's quoted below is the most crucial part:

This set of recommendations included that Verisk commit to becoming a pure-play insurance business through separation of all non-insurance assets; renew its focus on organic revenue growth initiatives and profit margin expansion within the insurance franchise; undertake several governance changes; and appoint new, independent directors whom shareholders would trust to help oversee the change that is required.

As of today, I think we can say that the company is acting on the recommendations made by the investment firm, and I believe this is why the stock is trading at a premium. Investors are confident about the company's future and believe that since the company implemented the changes recommended by D. E. Shaw, The stock price might appreciate by 70% from the price level of $200. VRSK also instituted a $2.5 billion accelerated share repurchase program in March 2023. Below is a checklist of the recommendations made by D. E. Shaw.

? Pure-play insurance business. As of Q1 23, the company now derives 100% of its revenue from its insurance segment.

? Focus on organic revenue growth and profit margin expansion. The company mentioned in its investor presentation that is now focused on organic growth and margin expansion. Shifting from data centers into AWS will help with the margin enhancement.

? Governance changes. VRSK appointed a new CEO and three new directors to its board.

Valuation

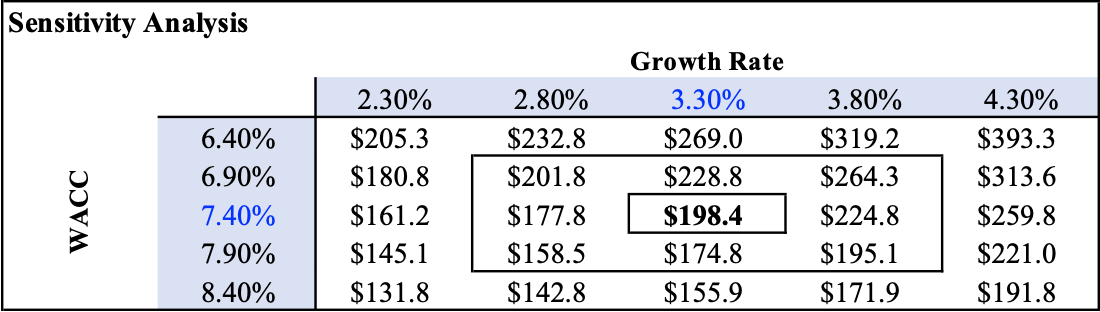

My fair value using a discounted cash flow analysis is $198.44, which equates to a downside of 15% from the current price. I model revenue to grow at a CAGR of 7.6% for the next five years, driven by cross-selling and new products. I expect Gross Margin to expand by 200 bps and EBITDA to grow at a CAGR of 8.5% in the same period.

For my EBITDA growth, I decided to follow the company's targets for the most part because their guidance history has been solid throughout the years. As for gross margin, My assumption is mainly based on historic performance and the firm's pricing power. The company has also started shifting away from data centers to AWS. This will help them minimize costs, thus improving margins. Using a 7.40% WACC and a terminal growth rate of 3.3%, I based my growth rate on the TAM's expected growth (underwriting & risks and claims).

I arrived at an equity value of $28.8 billion. I estimate that the company will generate $5 billion in free cash flow in the next five years. I expect it to be used in ways from which shareholders can benefit, such as dividends, buybacks, and attractive acquisitions. I also project 8.3% of revenue to be used on CapEx.

Created by the author

Below is a sensitivity table that shows how a different WACC and terminal growth rate can affect the share price.

{kind=link}

Recent Performance

VRSK reported second-quarter earnings on August 2, 2023. Revenue came in at $675 million vs. FactSet's estimate of $654.5 million, and EPS was $1.51 vs. FactSet's estimate of $1.41. Underwriting sales rose by +9.2% YoY and Claims by +14.3%, resulting in total insurance sales increasing by +10.7% YoY. Organic constant currency revenue grew 9.8%. VRSK returned $50 million to shareholders in the form of dividends, while the $2.5 billion share repurchase program is still underway.

All in all, I think VRSK reported solid second quarter earnings, beating expectations on the top and bottom lines. The firm's shift towards being a pure insurance player seems to be off to a great start. I believe the company's valuable products are what make it possible for them to outperform in tough macro conditions.

Risks

I believe VRSK has very little risk due to its high retention rate, and switching costs, and 81% of its revenue comes from subscriptions or long-term contracts. A major risk could be that if the P&C insurance industry was to have a downturn, VRSK's revenue would probably drop and take a hit.

Takeaway

The bottom line is that VRSK is a high-quality business with a leading position in the insurance industry. I attribute the company's strong moat to its high switching costs, large data set, pricing power, and retention rates. The firm still has a long runway for growth. The involvement of D. E. Shaw will perhaps boost investor confidence. I believe the company's strong moat will allow them to retain customers and keep competitors at bay. The more customers VRSK has, the more data it can collect and use to create new products.

I assign a hold because VRSK stock is not trading at a price that I would rate as "Buy". However, the valuation is understandable because D. E. Shaw is one of the best-performing hedge funds out there, and according to their 13F , they first took a position in VRSK back in Q1 2009. This indicates to me that they understand the business and believe it wasn't being run well, so they pushed for some changes. I will be keeping an eye on this company, and if the stock price drops to my buy range, I might upgrade my rating, assuming nothing bad happens within the business.

For further details see:

Verisk Analytics Stock: Overvalued But The Outlook Is Bright