VRSK - Verisk: Get Long The Breakout

2023-04-12 11:40:07 ET

Summary

- Verisk appears to have broken out.

- So long as support holds, the stock is a long.

- The valuation is okay, but the ASR and potential for better out years revenue growth are positives.

Verisk Analytics ( VRSK ) has rallied sharply in the past few weeks, and in my view, has broken out on what is likely a sustainable basis. The company has had its struggles in terms of growth in revenue, but earnings growth has been solid, and the company has a new buyback authorization that will soak up more than 8% of the current float. This one is not a screaming buy from a fundamental perspective, but the balance of the evidence suggests the risk here is to the upside.

Follow the money

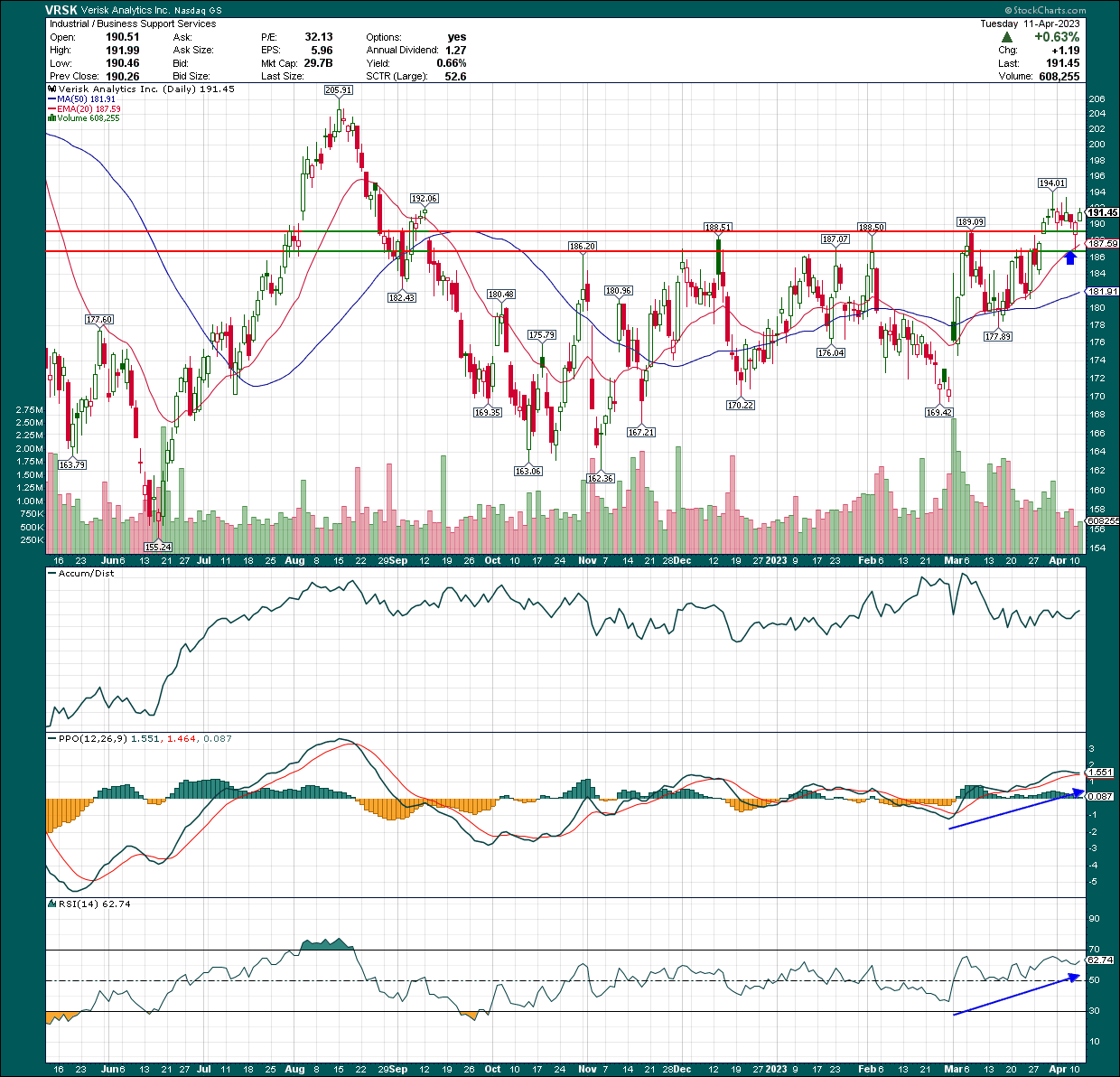

As we always do, we'll begin with a chart. Verisk consolidated for several months, beginning last year, after hitting a high of just over $200 late last summer. That rally was absolutely immense and took place in virtually a straight line, and needed to be consolidated. That has happened, and to my eye, the stock has broken out again.

{kind=link}

I've highlighted a zone of support that used to be resistance and encompasses roughly $185 to $190. I'll be clear that the bull case on the shorter time frames requires this level to be held. On the plus side for the bulls, the moving averages are rising, and the 20-day exponential moving average is within the zone of support. That makes it all the more likely this level should hold, but it also means that if it doesn't, that's a stronger statement from the bears, and that's when stops should be used to get out of the trade.

The PPO is showing a lot of strength from the bulls, as it broke out over the centerline several weeks ago, and has continued to strengthen. The 14-day RSI is showing similar behavior and remains elevated throughout this most recent rally. These are bull market behaviors and, in my view, add credence to the idea that Verisk has broken out.

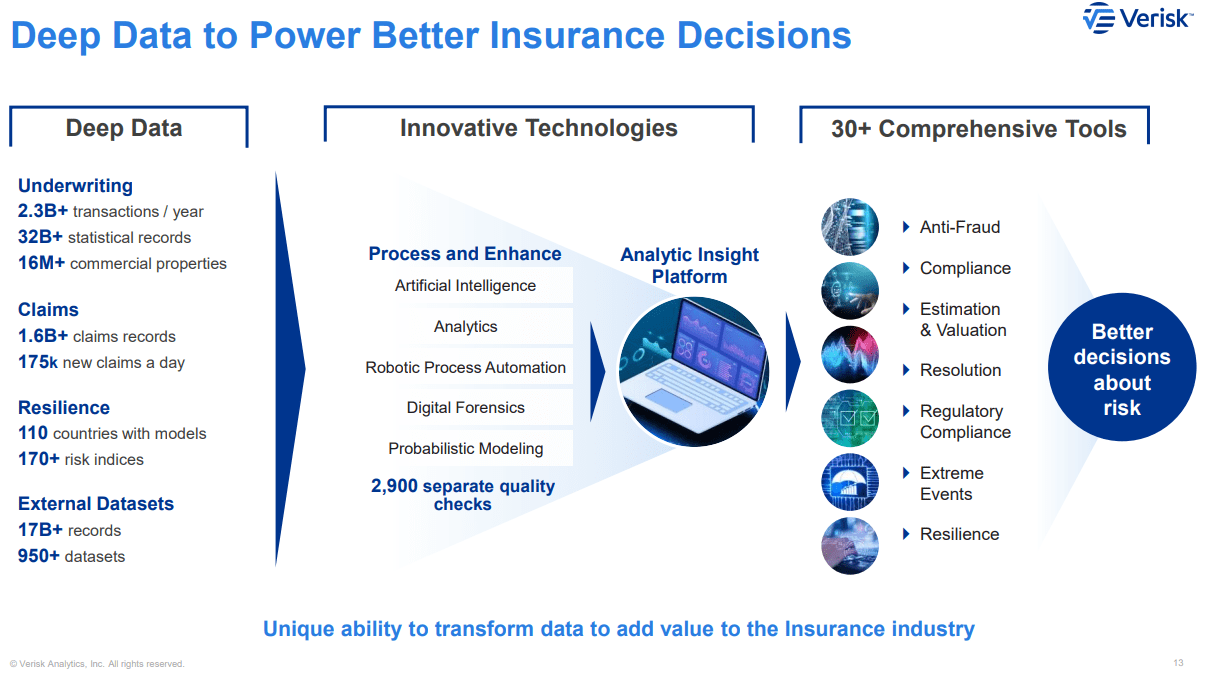

A strong niche, but not necessarily a growing one

Verisk has built itself a very nice spot in a specialized market. The company only serves the insurance sector, but does so with 50+ years of experience and expertise.

{kind=link}

The model is one that's familiar as Verisk essentially takes huge amounts of data, synthesizes it, and makes it easier for customers to make better risk decisions with their underwriting policies. This model is used in all industries, and we know it works, and Verisk has more experience here than perhaps any other player in insurance. That means it has a nice niche built out, but growth hasn't necessarily been easy. We know insurance is highly cyclical in that certain events related to weather or other catastrophes can drive big moves in revenue and earnings, and that's translated to relatively modest growth for Verisk over time.

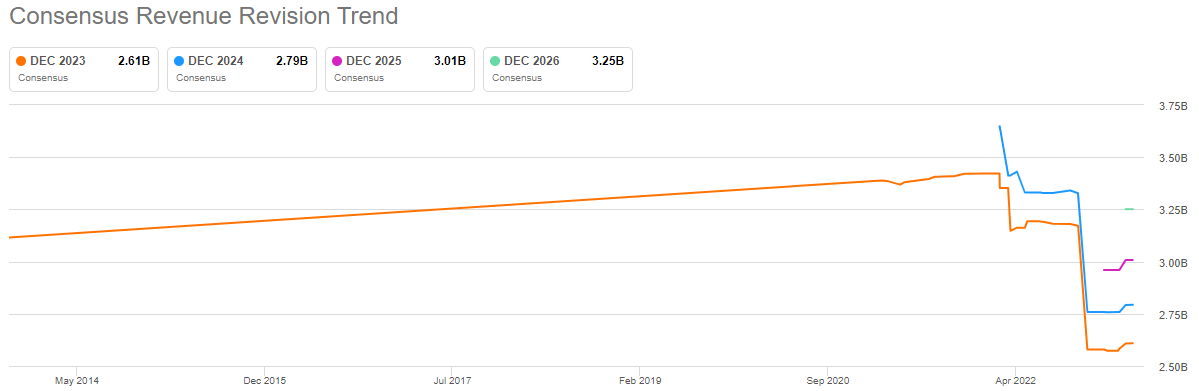

Below we have revenue revisions, and while the headline look here is ugly, there is a bit of silver lining at the end.

{kind=link}

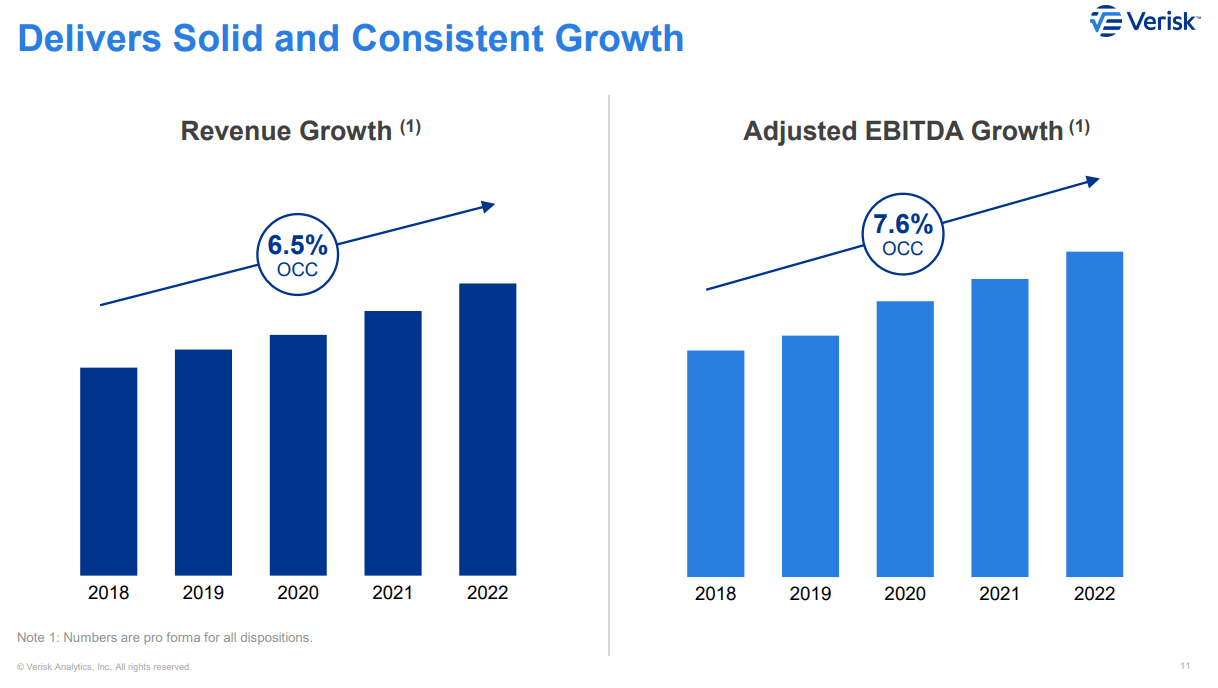

We can see recent revisions have been higher, so it appears the worst is over on this front. Over time, the company has managed to grow revenue on a pro forma basis, as we can see below.

{kind=link}

Estimates are for 4%+ growth this year and high-single-digit growth in the years to come. Should that come to fruition, I think there's a fairly significant upside for shares of Verisk from today's levels. The reason is because the company has a proven capability to grow earnings more quickly than revenue, and if revenue growth picks up, EPS growth could be quite substantial.

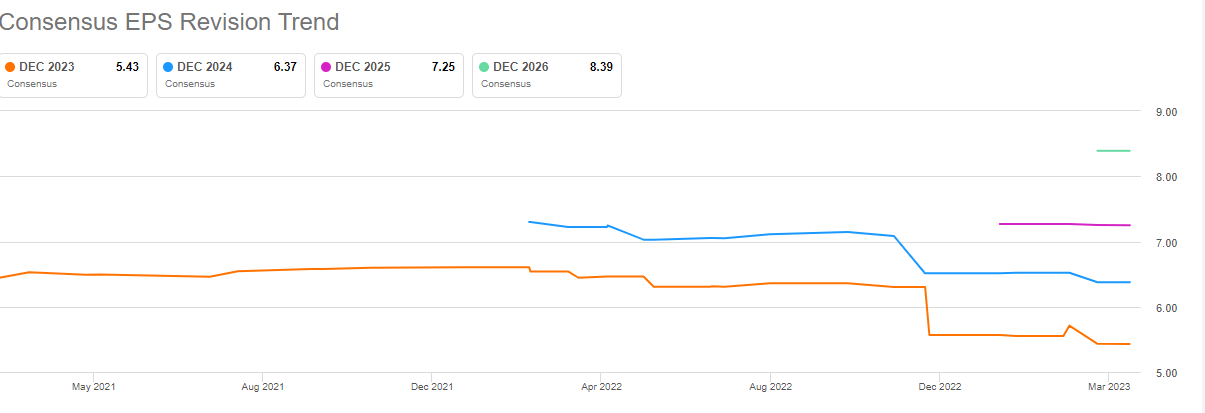

If we look at the revision trend for EPS, we can see that revisions have flattened out after some harsh down moves and that year-over-year growth is expected to be quite strong.

{kind=link}

The gap between the lines here indicates that growth from year to year is expected to be substantial, and that's because Verisk has strong operating leverage. That essentially just means that its cost structure is largely fixed, so when incremental revenue comes in, there's little incremental cost. That works out to better margins the higher revenue goes, which is why it is so critical for Verisk to see revenue growth accelerate again. Keep in mind these EPS estimates are based upon the relatively modest revenue growth estimates we looked at above, so if there's even a bit of upside to revenue, there could be quite a meaningful upside to EPS as well.

I mentioned the company's $2.5 billion accelerated share repurchase program above, and that's a big feather in the cap of the bulls. That will reduce the float by about 8%, which means future EPS numbers will be permanently higher by the same amount, all else equal. That will accelerate growth on an EPS basis, which should lead to a higher share price. This is why I love buybacks, and Verisk is doing exactly the right thing. I actually wish the company would stop with its dividend that yields less than 1%, and instead of paying a pointless cash distribution to shareholders, use that money to buy back more shares. No one is buying this stock for the 0.7% yield, which is why I think the dividend is a waste of money in this case. But the $2.5 billion ASR program is a great start.

A murky valuation picture emerges

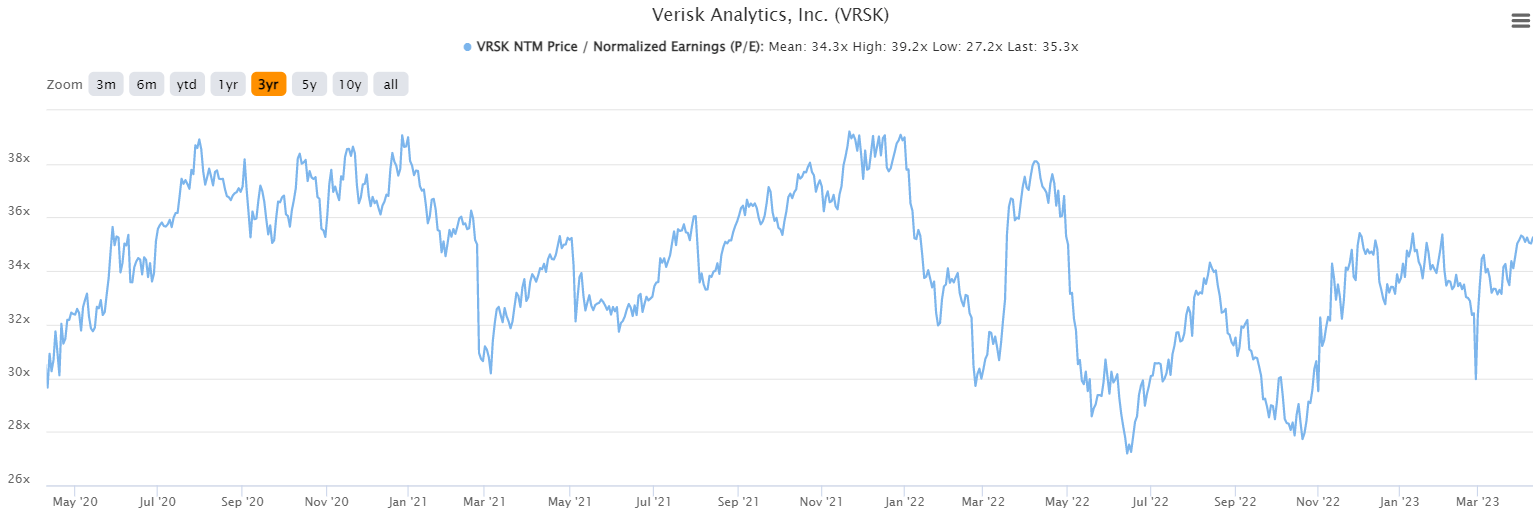

Verisk has a long history of profitability, so unlike some similar companies, we can use P/E reliably to examine the valuation. This company has never been cheap on an absolute basis, so traditional value investors are probably not interested. However, the stock looks pretty fairly valued today based upon current assumptions for earnings.

{kind=link}

Shares go for about 35X forward earnings, which is right in line with the average over the past three years. We can see the valuation has been choppy, both because the share price has moved around a lot, but also because earnings estimates have been somewhat volatile. My assessment of the valuation picture is that today, it's fairly valued; I don't see it as cheap or expensive. However, the future state of the valuation is contingent upon the path forward for EPS estimates. If we do see higher estimates for EPS from the ASR and/or higher revenue, I see upside risk to both the EPS portion of the P/E ratio, as well as the price investors will be willing to pay for those earnings.

Final thoughts

If we sum this up, we have a business with a nice niche, but one that is not going to see massive growth. Verisk is mature in its market position in a mature sector, so this is not a 30% or 40% growth story by any means. However, it has reliable earnings and a reasonable valuation on those earnings.

The ASR program is a great start in terms of returning capital in a shareholder-friendly way, and it appears to my eye that the risk for revenue and EPS estimates is up from here. The key is that we use the levels on the chart effectively, meaning that if the stock loses the support levels identified above, we use stops and get out. On the whole, I'm putting a buy rating on Verisk as the balance of evidence suggests a higher likelihood of upside than downside.

For further details see:

Verisk: Get Long The Breakout